- Pause before paying: The most common mistake executors make is paying credit cards or medical bills immediately. Debts must be categorized and paid in a specific order to protect the estate.

- Document everything: Every piece of mail, every phone call, and every statement needs to be logged. Your defense against disputes is a flawless paper trail.

- Three main buckets: Estate money generally goes toward administration costs, taxes, and creditor claims. Knowing which bucket a bill falls into dictates how you handle it.

- Safety first: You are generally not personally responsible for the deceased’s debts, provided you follow the proper operational steps and do not mix your personal funds with estate funds.

The Pressure to Pay: Why Pausing is Your Safest First Move

When you step into the role of executor, the mail does not stop. In fact, it often feels like it multiplies. Within days, you are staring at a stack of credit card statements, hospital bills, mortgage notices, and utility invoices. The natural, human instinct is to start writing checks immediately to clear their name and make the paperwork go away.

I always remember a client who came to me feeling proud that she had paid a $1,200 credit card bill on day five of her administration. Three weeks later, we discovered a $14,000 IRS lien against the estate, and there was not enough cash left to cover it. She had accidentally used estate funds to pay a low-priority unsecured debt, creating a massive legal headache. That single mistake changed the entire trajectory of her workflow.

This executor creditor and debt checklist is designed to prevent exactly that scenario. We are going to build a safe, structured map for handling debts, communicating with creditors, and preparing for tax obligations without triggering unnecessary disputes. My goal is to help you shift from feeling overwhelmed by the mail stack to feeling in total control of the recordkeeping, while leaving the jurisdiction-specific legal interpretations to your local professionals.

Defining the Boundaries: What This Map Will and Won’t Do

Before we start sorting bills, we need to set some ground rules about how we approach this phase of estate administration. Often, executors get bogged down searching the internet for exact answers to highly specific legal scenarios. That is a dangerous game.

As an executor, your primary job in the early stages is not to act as a judge deciding who gets paid. Your job is to act as a highly organized investigator and record-keeper. You are gathering the facts, logging the claims, and building a clean packet of information.

Guessing which credit card to pay first, using personal money to cover an estate shortfall, or arguing with debt collectors on the phone about late fees.

Requesting all claims in writing, placing unsecured debts on a formal hold, logging every communication, and reviewing the total picture before any funds are distributed.

We are going to focus heavily on the “After” approach. We will cover the practical steps of identifying debts without panic, the plain-English way to handle creditor contact, and the working system you need to track it all. If you are looking for how to open the actual bank account to handle these funds, make sure to review the banking access procedures in our other guides. Here, we are purely focused on the outflow: managing the people asking the estate for money.

⚠️ Note on Community Property: If the deceased lived in a community property state (such as California, Texas, Washington, or Arizona), the rules can shift significantly. In these states, a surviving spouse might be responsible for certain debts incurred during the marriage, even if their name is not on the account. This makes pausing and seeking local professional advice even more critical.

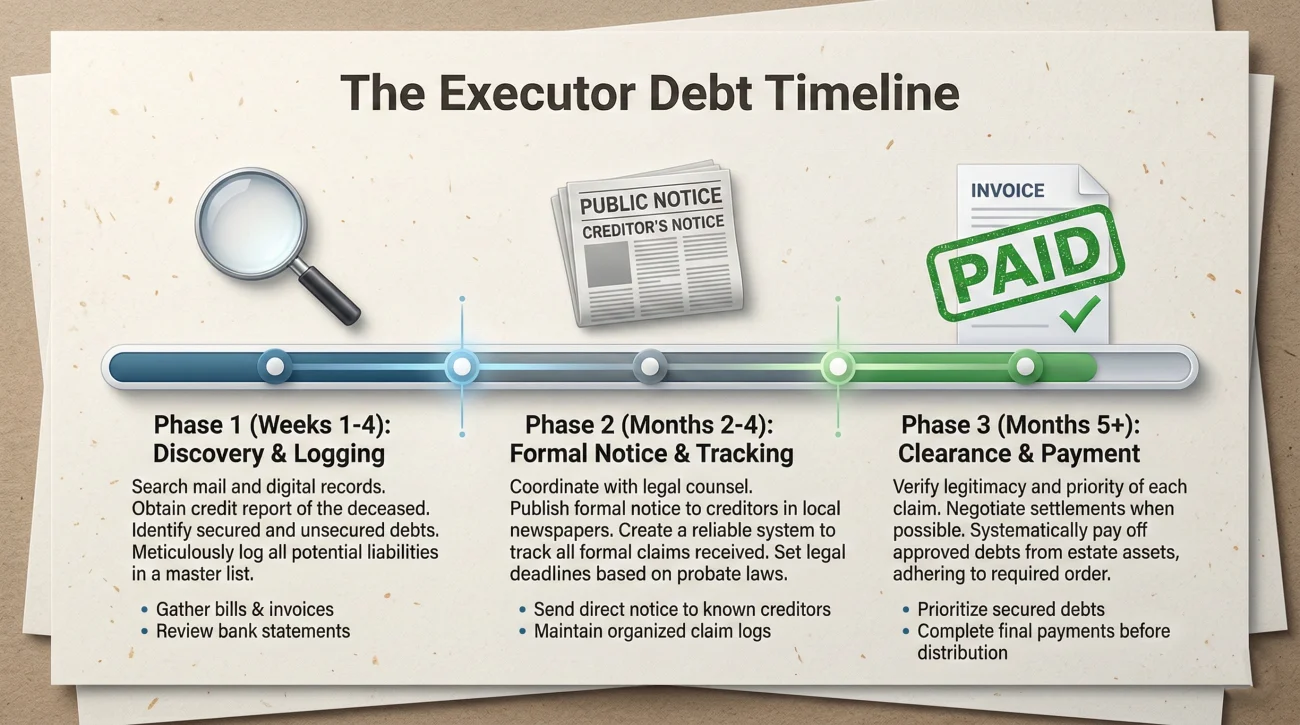

The Executor Debt Timeline: A High-Level Roadmap

Executors often feel overwhelmed because they try to solve month-three problems in week one. To keep your workflow organized, here is how the debt and creditor phase generally unfolds in practice:

| Phase | Primary Operational Goal |

|---|---|

| Week 1 to 4 (Discovery) | Set up the physical mail inbox. Log incoming bills without paying them. Identify critical secured debts (like mortgages) to prevent immediate default. Pull a credit report if necessary. |

| Month 2 to 4 (Formal Tracking) | Publish the formal notice to creditors (if required locally). Mail notices to known creditors. Build out your central Claim Log. Ensure all tax documents are being routed to your CPA. |

| Month 5+ (Clearance & Payment) | Wait for the creditor claim window to officially close. Review all verified claims against available estate funds. Pay claims in the proper legal priority order. Prepare for final distribution. |

By compartmentalizing these tasks, you stop reacting to every piece of mail and start managing a predictable process.

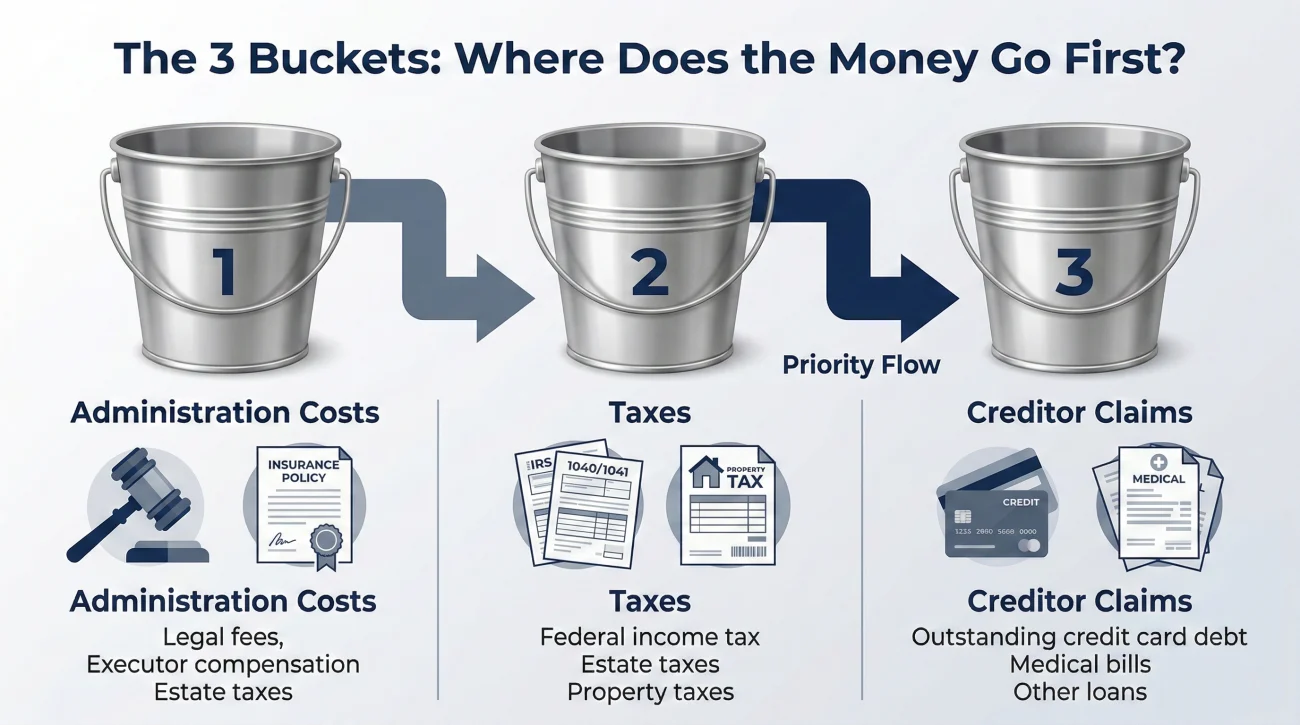

The Three Buckets of Estate Financials

Once you understand that your role early on is to gather and verify rather than immediately pay, the next step is sorting the claims. To make sense of the chaos, I always advise executors to conceptually divide any request for money into three distinct buckets. Not all bills are created equal, and treating them as if they are is a common operational mistake. When you integrate this concept with your broader workflow for debts, creditors, and taxes, the path forward becomes much clearer.

Bucket 1: Administration Costs

These are the expenses required to actually keep the estate running and secure. Think of this as the operational budget for the estate itself. Commonly, this includes court filing fees, fees for professional help (like a local attorney or CPA), property insurance to protect an empty house, and basic utilities to prevent pipes from freezing.

In many cases, these costs are prioritized because without them, the estate cannot be settled or its assets protected. Tracking these meticulously with receipts and clear labels is vital. I often see executors mix these up with the deceased’s old debts, which creates a massive headache later during the accounting phase.

Bucket 2: Taxes

Taxes are the heavy hitters. You cannot simply ignore the IRS or the state revenue department. Taxes generally fall into their own highly prioritized lane. This might include the final individual income tax return for the deceased, property taxes on real estate, or income taxes generated by the estate itself during the administration process.

Bucket 3: Creditor Claims

This is everything else the deceased owed before they passed away. It is the credit card balances, the personal loans, the old medical bills, and the utility arrears from months ago. This is the bucket that causes the most stress, but ironically, it is often the bucket that requires the least immediate action. These claims usually need to be formally submitted, verified, and placed in a holding pattern until you know exactly how much money the estate actually has.

Key Point: By mentally sorting every piece of mail into one of these three buckets, you instantly reduce your anxiety. A final notice from a streaming service (Bucket 3) requires a very different response than an expiring property insurance policy (Bucket 1).

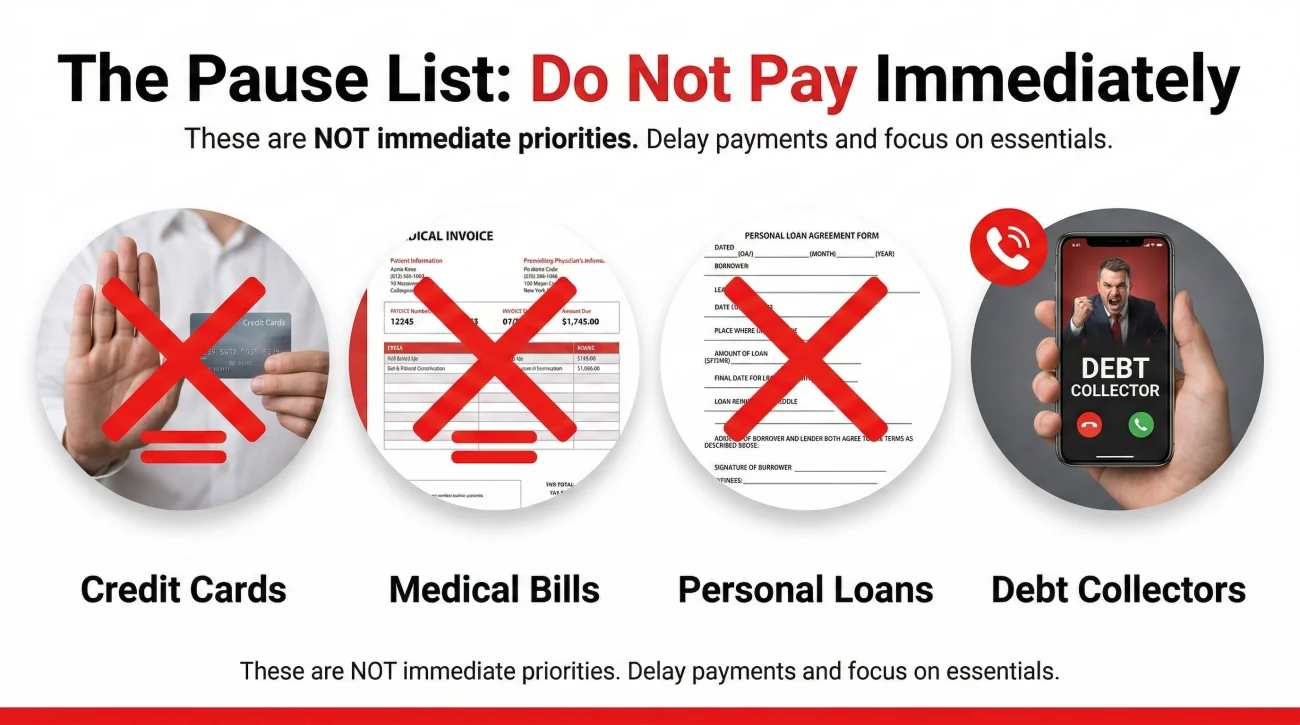

The “Pause List”: Payments to Freeze Immediately

When I review early-stage executor files, the most frequent error I spot is premature payment of unsecured debts. Therefore, the very first step in your executor creditor and debt checklist is creating a “Pause List.”

Why do we pause? Because you must have a complete picture of the estate’s financial health before paying lower-priority debts. You never want to accidentally give away money that legally belonged to a higher-priority entity like the IRS or the probate court.

Typically, executors put an immediate operational freeze on:

- 🛑 Credit Cards: These are almost always unsecured and sit lower on the priority list.

- 🛑 Medical Bills: Do not pay anything until insurance adjustments are finalized and the formal claim is reviewed.

- 🛑 Personal Unsecured Loans: Handshake deals or standard signature loans.

- 🛑 Collection Agency Demands: Never pay a debt collector based on a phone call. Demand written proof.

💡 Pro Tip: Pausing does not mean ignoring. It means you acknowledge the bill, log it in your tracking spreadsheet, and file the physical paper away safely without writing a check.

Identifying Debts Without Panic: The Discovery Phase

You cannot manage what you do not know exists. One of the most common fears I hear is, “What if I miss a debt and they come after me later?” To prevent this, you need a systematic discovery process. You do not need to be a private investigator; you just need to be observant and thorough.

The First Pass: The Paper Trail

Start with the obvious. Set up a dedicated physical inbox for estate mail. For the first 30 to 60 days, simply watch what arrives. Creditors want their money, so they will send bills. Look for statements stamped “Past Due” or letters from unfamiliar companies. Additionally, locate the deceased’s filing cabinet or desk. You are looking for recent tax returns, mortgage statements, and loan agreements.

The Second Pass: The Digital Footprint

If you have authorized access to the deceased’s bank statements (which you should, once formally appointed), review the last 12 months of transactions. This is often where the real truth lies.

Look for recurring automated clearing house (ACH) transfers. A monthly $45 charge might reveal an active storage unit holding valuable estate property. Also, pay close attention to the modern digital footprint: recurring charges for Netflix, Spotify, Adobe, gym memberships, or paid cloud storage. These digital subscriptions are often forgotten but can slowly drain estate funds if not identified and paused. Log every recurring outflow.

In many cases, checking a credit report can also provide a snapshot of formal, reported debts. The Consumer Financial Protection Bureau (CFPB) notes that debts generally do not disappear upon death, making it crucial to identify exactly what is owed by the estate.

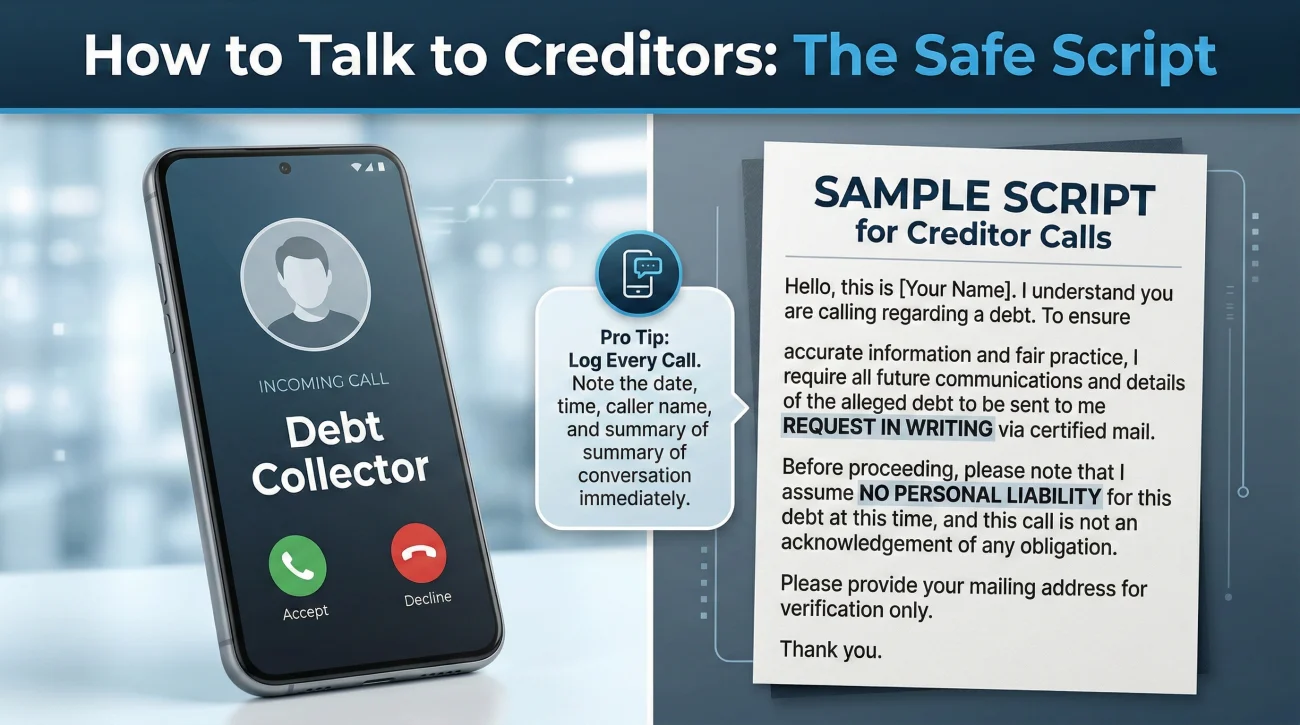

Creditor Contact in Plain English: What to Confirm and Record

Eventually, the phone will ring. Debt collectors are trained to create a sense of urgency. They want you to feel that if you do not pay right now, terrible things will happen. As an executor, you must strip the emotion out of these interactions.

Your goal on these calls is never to negotiate, never to promise payment, and definitely never to admit personal responsibility. Your goal is simply to confirm facts and request a paper trail.

Here is a common pattern I see: A collector calls, speaks rapidly about a past-due balance, and asks for a credit card number. The stressed executor, wanting to help, uses their own card. This is exactly what we want to avoid.

Sample Telephone Script for Creditors:

“Hello, I am the executor for the estate of [Name]. I am currently in the process of gathering all estate records. I cannot discuss payment at this time. Please place a hold on this account and mail a complete, itemized statement of the claim, along with proof of the debt, to [Mailing Address]. I will review it once received in writing.”

❌ What NOT to Say to a Debt Collector:

- 🚫 “I will take care of this balance next week.” (Never promise payment out of habit).

- 🚫 “I am not sure how much she owed, let me check.” (Never show uncertainty about the facts; it invites collectors to fill in the blanks for you).

- 🚫 “Can we settle this for a lower amount?” (Never negotiate over the phone).

- 🚫 “I will just put this on my personal card.” (Never mix your personal funds with estate funds).

After you hang up, immediately log the call. Write down the date, the time, the name of the representative, the company they work for, and the amount they claimed was owed. If they do not send the written proof, you have a record that you asked for it.

Notice to Creditors: Why It Exists and What to Verify

You will likely hear the phrase “notice to creditors” frequently during your administration duties. In plain English, this is the formal process of telling the world, “This person has passed away, and if they owe you money, you have a limited time to speak up.”

Why does this matter for your workflow? Because you cannot keep the estate open forever waiting to see if a random debt pops up. The notice process creates a definitive window (often a set number of months) for creditors to submit formal claims. If they miss the window, their claim is typically barred.

As an executor, your job is to track this timeline meticulously. Usually, this involves publishing a notice in a local newspaper and directly mailing notices to known creditors. Because the rules on how to publish, where to publish, and how long the window stays open vary wildly depending on local jurisdiction, this is a crucial point where you must get specific instructions from your local court or legal advisor. Do not guess on these dates. Log the exact date the notice was published and calculate the exact date the window closes.

Secured vs. Unsecured: Why the Collateral Changes the Conversation

While the notice to creditors creates a waiting period for general, unsecured claims, there is one category of debt that cannot simply be ignored while the clock ticks: secured debts. Earlier, we put credit cards on the “Pause List.” But what about a mortgage or a car loan? These are called secured debts, meaning the debt is attached to a physical asset (collateral). If the bill isn’t paid, the lender has the right to take the asset.

This reality changes how you manage the workflow. While you might ignore a credit card late fee while you sort things out, ignoring a mortgage payment could lead to foreclosure, causing the estate to lose a massive asset.

When dealing with secured debt, your immediate operational goal is to figure out the status of the asset. Is the house going to be sold? Is the car going to be returned to the bank? Is a beneficiary going to take over the payments? You often need to maintain communication with these specific lenders to prevent default while you make those larger strategic decisions. Track the monthly payment amounts, the payoff balances, and any grace periods meticulously.

“The collateral dictates the urgency. You can delay a medical bill, but you cannot easily reverse a car repossession.”

Insolvent Estate Signals: What Changes When Money is Short

Sometimes, despite your best organizational efforts, the math simply does not work. When you tally up the administration costs, the taxes, and the creditor claims, the total is higher than the cash and assets available in the estate. This is known as an insolvent estate.

If you suspect the estate might be insolvent, your operational posture must become incredibly defensive. This is the danger zone for executors.

If there is not enough money to go around, the law dictates exactly who gets paid first, second, third, and who gets nothing. If you guess the order and guess wrong, creditors who were legally entitled to that money might demand you replace it out of your own pocket.

The moment you see the “insolvency signal” (debts > assets), you must freeze all outbound payments. You stop paying everything, even seemingly small bills, and you consult a local professional to guide you through the statutory priority list. Your primary job shifts to building a flawless, airtight list of all assets and all claims so the professional can tell you how to divide the remaining pennies.

Tax Overview: The Three Lanes You Must Navigate

Taxes intimidate almost everyone, but as an executor, you can manage the stress by breaking the obligations down into three conceptual lanes. You do not need to be a CPA to gather the right documents; you just need to know what files to look for. The table below is a high-level orientation to help you organize documents. For a complete breakdown of filing requirements, see our dedicated tax overview guide in the reference section below.

| Tax Lane | What It Means (Plain English) | What to Track / Gather |

|---|---|---|

| 1. Final Individual Return | Taxes on the income the person earned in the year they died, up until the exact date of death. | Prior year tax returns, W-2s, 1099s, final pay stubs. |

| 2. Estate Income Tax | Taxes on money the estate itself makes after the person died (e.g., rent from a property, interest on an estate bank account). | Estate bank statements, property income logs, investment dividends generated post-death. |

| 3. Estate Tax (Death Tax) | A tax on the total value of everything the person owned. Often only applies to very wealthy estates, but must be verified. | Complete asset inventory, appraisals, date-of-death valuations. |

A common mistake is assuming that once the final individual return is filed, the tax job is done. However, if the estate stays open for a year and earns interest, Lane 2 comes into play. According to the IRS guidelines on deceased taxpayers, understanding the distinction between the individual’s final return and the estate’s income return is a fundamental responsibility of the executor.

Building Your Working System: The Claim Log

You cannot manage an estate from a pile of envelopes on the kitchen table. You need a centralized tracking system. Whether you use a digital spreadsheet or a physical ledger, your “Claim Log” is your single source of truth.

In my daily practice, I find that a clean, well-maintained log stops arguments before they start. If a beneficiary asks why a certain bill hasn’t been paid, you don’t guess—you point to the log. Here are the minimum columns your claim log should include:

- 📄 Creditor Name: Who is asking for money?

- 📄 Account Number: The last four digits are usually enough for reference.

- 📄 Date Received: When did the claim arrive?

- 📄 Amount Claimed: The exact dollar figure requested.

- 📄 Type of Debt: Is it secured, unsecured, medical, or a utility?

- 📄 Status: Use clear labels like “Under Review,” “Disputed,” “Hold – Awaiting Funds,” or “Paid.”

- 📄 Action Notes: E.g., “Requested itemized bill on 10/12. Awaiting reply.”

Every time you check the mail or take a phone call, update this log. When you meet with a professional or prepare to close the estate, handing them this clean, organized map will save everyone time and money.

The Finish Line: What to Keep Before Distributing

The finish line is not when the last debt is paid; the finish line is when you have absolute proof that everything was handled correctly. Before you even think about distributing remaining funds to beneficiaries, you must secure your paper trail.

I always recommend creating a “Final Clearance Packet.” This packet should contain the final, zero-balance statements from every creditor you paid. It should contain the letters from creditors whose claims were denied or barred by the notice window. It must include the final clearance letters from the tax authorities indicating that all returns have been accepted and processed.

Only when your Claim Log is completely resolved, your tax lanes are closed, and your documentation is safely archived, should you move to the distribution phase. By maintaining strict operational discipline through the debt and creditor phase, you protect both the estate’s value and your own peace of mind.

Final Thoughts on Managing Estate Debts

Handling the debts and creditors of an estate is rarely enjoyable, but it does not have to be chaotic. By refusing to be rushed, separating claims into clear buckets, and maintaining a meticulous written log, you build an invisible shield around your work as an executor.

When you first take on this role, the sheer volume of paper and demands can make you feel like you are constantly on the defensive. But if you follow this map, that dynamic shifts. You become the one dictating the pace. You force the creditors to prove their claims in writing, you lock down the deadlines, and you protect the estate’s remaining assets for the people who truly matter: the beneficiaries.

Remember, your primary tool is not a checkbook. Your primary tool is a notepad. Confirm everything in writing, track every deadline, and never hesitate to pause and get local professional help when the math gets tight. A slow, well-documented process will always win out over a fast, disorganized one.

Deep Dive Reference Guides for Specific Scenarios

Because estate administration is complex, no single checklist can cover every granular detail. Throughout your workflow, you will hit specific roadblocks that require a deeper understanding. Use the reference table below to navigate our specialized guides when you encounter these exact situations.

| Specific Topic Guide | What You Will Learn |

|---|---|

| Notice to Creditors: What It Is, Why It Matters, and What Executors Should Track | How to track the publication dates and understand what notice protects against. |

| How Executors Identify Creditors: A Safe, Practical Search Map | A step-by-step method to find debts without over-collecting or guessing. |

| Is an Executor Personally Responsible for Debts? | Understanding liability risk and how process mistakes create exposure. |

| Executor Paying Debts: A Safe Order-of-Operations | A safe workflow for paying bills that reduces disputes (without state-specific priority charts). |

| Secured Debts After Death: Mortgages and Car Loans | How to handle debts tied to collateral and what information to gather. |

| Credit Card Debt After Death: What Executors Commonly Do | A non-technical overview of how to pause, document, and handle credit card claims. |

| Medical Bills After Death: How Executors Keep Them Organized | How to avoid overpaying, spot duplicates, and build a medical bill packet. |

| Funeral Expenses and Reimbursement | Safe recordkeeping for when family members front funeral costs. |

| Estate Administration Expenses: What Usually Counts | How to document postage, locks, and travel as official operating costs. |

| Executor Tax Overview: Final Return vs Estate Income Tax | A plain-English map of the three tax lanes and what documents to gather. |

| Tax Refund After Death: Why the Refund Check Gets Stuck | Why refunds get issued to the estate and how to unblock the deposit. |

| Insolvent Estate: What Changes When There Isn’t Enough Money | What to pause and why professional guidance is needed when debts exceed assets. |

| Handling Creditor Calls and Collection Letters as Executor | A calm, document-first approach to avoid admissions and keep records. |

| When Can an Executor Distribute Money? | A conservative clearance checklist to review before moving funds to beneficiaries. |

| Utility Bills and Subscriptions After Death | What to keep running, what to pause, and how to document the triage process. |

Sources

- IRS: Managing Taxes for a Deceased Person. View Source

- Consumer Financial Protection Bureau (CFPB): Does a person’s debt go away when they die? View Source

❓ FAQ

🏦 What bills should an executor pay first?

Generally, administration costs (fees to keep the estate secure and running) and taxes take priority. Unsecured debts like credit cards are typically placed on hold until all assets and higher-priority claims are fully known.

💳 Do I have to pay my deceased parent’s credit card debt?

No, you generally do not pay it from your personal funds. The estate is responsible for the debt. If the estate does not have enough money, the credit card company typically takes a loss, but you must follow proper procedures to prove the insolvency.

📞 How do I stop debt collectors from calling after a death?

Inform them that the person has passed away, state that you are the executor, and instruct them to submit all claims and correspondence in writing to the estate’s mailing address. Log the call and do not discuss payment over the phone.

📰 Do I really have to publish a notice to creditors in the newspaper?

In many jurisdictions, yes. Publishing a formal notice starts a legal countdown clock for unknown creditors to submit claims. Once that window closes, late claims are typically barred, which protects you when you distribute funds.

🏥 What happens to medical bills after death?

They become claims against the estate. Do not pay them immediately; wait for health insurance to process their portion and provide a final Explanation of Benefits (EOB) before logging the final amount owed by the estate.

🏠 Who pays the mortgage while the estate is in probate?

The estate is responsible for maintaining the asset. Usually, executors use estate funds to keep the mortgage current to prevent foreclosure while deciding whether to sell the house or pass it to a beneficiary.

📉 What if the estate doesn’t have enough money to pay everyone?

This is an insolvent estate. You must immediately pause all payments. Local laws dictate a strict priority order of who gets paid what percentage. Guessing this order can create personal liability, so local professional help is highly recommended.

💸 Can an executor be held personally liable for estate debts?

Generally no, unless you make process mistakes like paying lower-priority debts before taxes, distributing money to beneficiaries too early, or mixing your personal money with estate funds.

🧾 What counts as an estate administration expense?

These are the costs required to settle the estate. Common examples include probate court fees, professional legal or tax advice, property insurance for an empty home, and costs to secure or appraise assets.

⏱️ When is it safe to distribute money to beneficiaries?

Only after all known debts are resolved, the formal creditor claim window has closed, all taxes have been filed and cleared, and you have set aside a reserve for final closing expenses.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.