- An insolvent estate simply means there is not enough money to pay all the deceased person’s debts; it changes your job from “paying bills” to “freezing payments and logging claims.”

- Do not guess who should be paid first. Paying an unsecured credit card before knowing the total medical debt can create personal liability for you as the executor.

- Your immediate action is a full pause on all distributions and debt payments until a complete financial snapshot is built.

- Communication must shift to neutral, written requests for claims. Never promise a creditor they will be paid in full.

- Because state laws dictate the strict order in which creditors must be paid when funds are short, professional legal and tax guidance is almost always necessary for an insolvent estate.

Facing the Math: When Debts Outweigh Assets

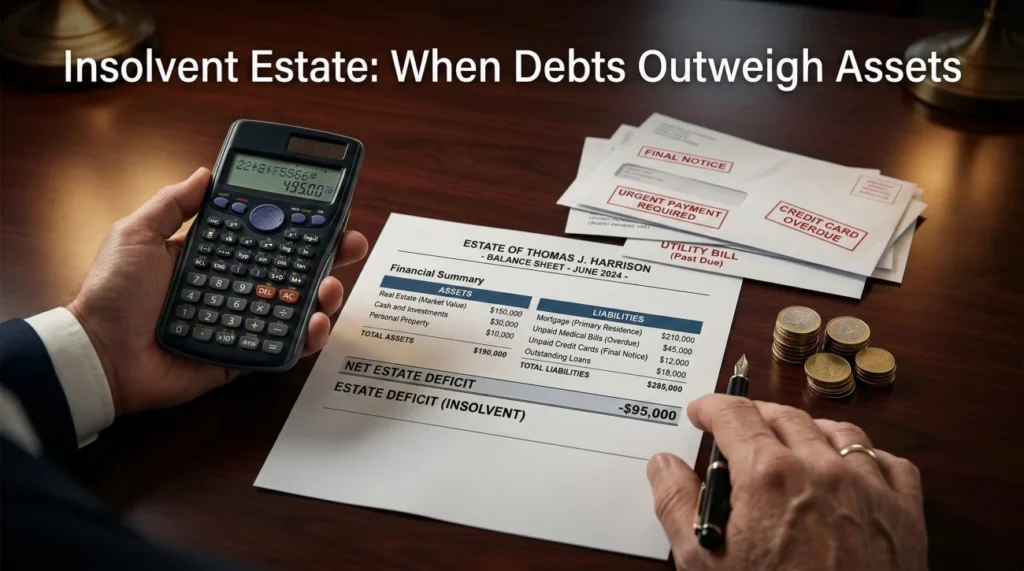

One of the most stressful moments in estate administration is the day you sit down, tally up the bank balances, look at the stack of incoming bills, and realize the math simply does not work. You are looking at what is commonly called an insolvent estate. If you are acting as an insolvent estate executor, I want you to take a deep breath. It is not your fault the money isn’t there, and you are not expected to magically produce funds to cover the shortfall.

In my experience supporting estate administration workflows, this is the exact moment where well-meaning executors make their biggest mistakes. Human nature tells us to start clearing the smallest bills to get them out of the way, or to appease the loudest debt collector just to silence the immediate pressure. But when an estate lacks the funds to make everyone whole, the rules of the game change completely.

Field Note: A common pattern I see is executors using their own personal money to pay the deceased’s utility bills or credit cards, assuming the estate will eventually reimburse them. If the estate turns out to be insolvent, that reimbursement may never happen, and the executor’s personal money is simply gone.

Your role shifts immediately. You are no longer the person who writes checks; you become the person who builds the puzzle. Your primary focus becomes gathering the pieces, documenting the claims, protecting the remaining assets, and preparing that organized data for legal review.

Early Warning Signals of an Insolvent Estate

You rarely know an estate is insolvent on day one. It usually reveals itself over the first few months as you monitor the mail and sort through the deceased’s records. Identifying the shortfall early is critical. You might realize there is an issue if you see:

- 📄 Underwater property: The mortgage balance is significantly higher than the realistic market value of the home. Action: Check recent local sales to confirm the gap, rather than relying solely on outdated tax assessments.

- 📄 Medical bill avalanches: A prolonged final illness often results in waves of hospital and specialist bills that easily dwarf a standard checking account balance. Action: Start a dedicated medical sorting folder to group these together before making any assumptions about the total.

- 📄 High-interest unsecured debt: Discovering multiple maxed-out credit cards or personal loans hidden in a home office desk. Action: Log the most recent statement balances into a single list to see the total weight of the unsecured debt.

- 📄 No liquid assets: The deceased may have owned items of value (like old vehicles or furniture), but there is less than a few hundred dollars in actual bank accounts. Action: Audit the actual cash flow before authorizing any out-of-pocket estate administration expenses.

❌ Common Mistake: Ignoring the warning signs and continuing to pay minor subscriptions because they “aren’t that much money.” Every dollar spent before the full debt picture is clear is a dollar that might legally belong to a higher-priority creditor.

The Immediate Pause: Stopping the Outflow

The moment you suspect the estate might not have enough money to pay debts, your primary operational directive is simple: stop paying.

Why is this so important? Because an executor can sometimes face personal liability if they distribute estate funds incorrectly. If you pay off your father’s credit card, but there isn’t enough money left over to pay his final income taxes or the funeral home, the IRS or the funeral director may legally ask you why you prioritized an unsecured credit card over their legally recognized claims.

Opening mail, writing checks from the estate account for every bill that arrives, and hoping there is enough left over for the beneficiaries.

Opening mail, logging the debt into a spreadsheet, filing the paper in a “Claims” folder, and keeping the estate bank account locked down.

What Needs to Stop Immediately

If you suspect insolvency, you must put a hard hold on:

1. Distributions to beneficiaries: Not a single piece of jewelry, furniture, or dollar should move to a beneficiary. Creditors almost always have a right to be paid before heirs inherit.

2. Unsecured debt payments: This includes credit cards, personal loans, and medical bills. These are often the lowest priority in the eyes of the law, but they are usually the loudest collectors.

3. Out-of-pocket spending: Halt any personal funding for estate expenses. As noted earlier, reimbursement is never guaranteed in a shortfall scenario, so do not assume you will get your money back.

For a broader view of how standard, solvent debts are normally managed before things get complicated, you can review our overarching executor creditor and debt checklist. However, remember that insolvency overwrites normal payment timelines.

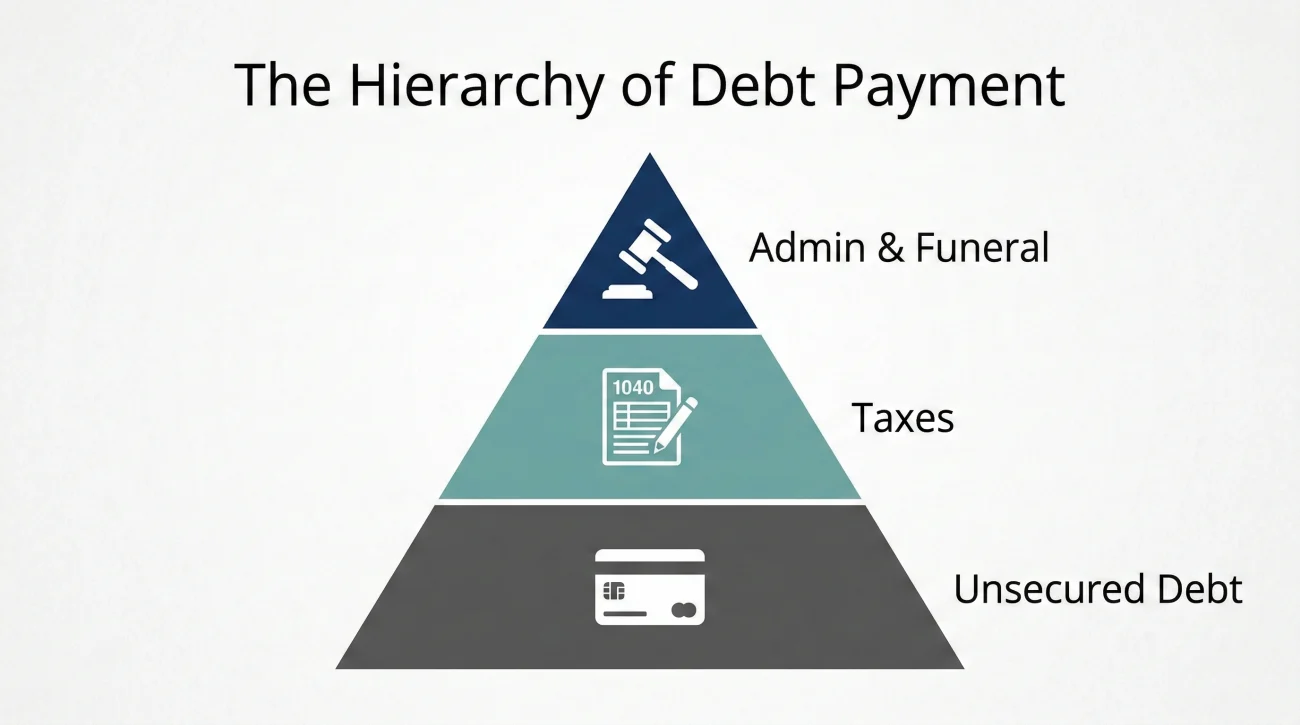

The Concept of Priority: Why All Debts Are Not Equal

When there isn’t enough pie for everyone, who gets a slice? You do not get to decide who is most deserving. Every local jurisdiction has specific laws that rank creditors into tiers or classes.

While the exact order varies depending on local rules, the system is generally designed to keep the estate functioning first, pay the government second, and deal with unsecured lenders last. First, the costs of actually administering the estate (like court fees and legal help) are often at the top. Next commonly comes funeral and burial expenses up to a certain reasonable limit. After that, federal and local taxes usually take precedence. Somewhere near the bottom of the ladder sit the unsecured creditors.

Your Action Steps for Priority Management

Knowing about priority tiers is only helpful if you act on it correctly. Instead of trying to interpret the law yourself, your job is to organize the incoming claims into conceptual folders:

- ✅ Folder A (Admin & Final Expenses): Group the funeral invoices, court filing receipts, and legal fees.

- ✅ Folder B (Taxes): Group any IRS notices or state department of revenue letters.

- ✅ Folder C (Unsecured Claims): Group the credit cards, medical bills, and personal loans.

By organizing the debts into these broad categories, you create a clean, highly readable packet. When you eventually meet with an estate attorney, you can hand them these categorized folders. They will then look up the exact state statute, map your organized folders to the legal priority tiers, and tell you exactly what percentage (if any) each tier receives.

💡 Pro Tip: If the estate cannot even cover the administration costs and the funeral (Folder A), you are dealing with a deeply insolvent estate. At this point, careful documentation is your only shield against creditor harassment.

Building Your Solvency Snapshot (What to Track)

When you cannot pay, your best defense is exceptional organization. You need to build a clear, undeniable picture of the estate’s financial reality so that when creditors demand payment, you can calmly explain the situation with data.

I always recommend setting up a dedicated “Insolvency Tracking” system using a simple spreadsheet and a physical binder.

The Three Trackers You Need

You need to document three distinct buckets of information to prove the estate is short on funds.

| Tracking Bucket | What to Log | Why It Matters |

|---|---|---|

| 1. Asset Snapshot | Bank balances, vehicle values, real estate estimates, cash on hand. | Proves the total ceiling of what is available to distribute. |

| 2. Claim Log | Creditor name, date received, account number, amount claimed. | Shows the total weight of the debt pressing against the assets. |

| 3. Admin Costs | Filing fees, postage, death certificates, professional invoices. | Often top-priority items that deplete the limited assets first. |

When a creditor calls, you aren’t just saying that the estate is broke. You are eventually able to demonstrate, through your legal representation, the exact mathematical reality: the total assets, the priority administration costs, and the remaining gap.

How to Communicate Neutrally with Creditors

Managing an insolvent estate means you will likely receive a lot of phone calls and collection letters. Creditors want their money, and their automated systems will push hard. Your communication strategy must be incredibly disciplined.

Your goal is to acknowledge receipt of their claim without ever making a promise of payment. Do not let empathy force you into a corner. I often see executors say things like, “I’ll make sure you get paid as soon as the house sells.” If the house sells and the IRS takes all the proceeds, you have just broken a promise to a creditor, which invites hostility.

Scripts for Written and Spoken Communication

Keep your language dry, factual, and process-oriented. Always request things in writing.

Sample Email/Letter Reply to a Creditor:

Subject: Estate of [Name] – Request for Written Claim

Hello,

I am writing to you regarding the estate of [Name]. We are currently in the process of auditing the estate’s assets and liabilities.

At this time, we are unable to make any disbursements. Please submit your formal, itemized claim in writing to [Mailing Address] so it can be added to the estate ledger for review.

Thank you for your patience as we navigate this process.

If you are caught on the phone, use a simple formula to end the call safely:

[Acknowledge call] + [State the current phase] + [Request written documentation]

“I understand you are calling about the balance. Right now, I am simply gathering all documentation to assess the estate’s overall status. I cannot process any payments over the phone. Please mail the final statement to my attention at…”

When to Call in Local Professionals (The Red Flags)

I firmly believe that a highly organized person can handle many parts of a standard, solvent estate. However, an insolvent estate is entirely different. Because the risk of personal liability is so high if you accidentally pay the wrong tier of creditors, dividing limited funds safely requires professional guidance.

You should immediately consult a local probate attorney or estate CPA if you encounter any of the following red flags:

- 🚩 The total known debts clearly exceed the cash in the bank, and the only asset left is a house with a mortgage.

- 🚩 You receive letters from the IRS or the state department of revenue regarding unpaid back taxes.

- 🚩 Multiple creditors are threatening to force the estate into bankruptcy or place liens on property.

- 🚩 Family members are demanding their inheritance despite the outstanding debts, creating a hostile environment.

An attorney can handle the communication with aggressive creditors, informing them legally that there is no money left to claim, which often stops the collection calls permanently.

Final Steps: Preparing for the Handoff

Serving as the executor of an insolvent estate often feels like doing a lot of paperwork just to prove to companies that they won’t get paid. The most important thing to remember is your own protection.

Your mandate is not to satisfy every debt; your mandate is to administer the remaining assets safely. Do not let aggressive creditors rush your timeline. Focus entirely on building your tracking logs, placing the claims into their appropriate conceptual folders, and preparing a clean summary for your attorney. Handing over a well-organized snapshot of the insolvency is the single best action you can take to close the estate safely and protect yourself from future disputes.

❓ FAQ

📝 Do I still have to send a notice to creditors if there is no money?

In many cases, yes. The formal notice process is often what legally starts the clock for creditors to submit claims. Confirming exactly who is owed what is a required step, even if you eventually tell them there are no funds. Always verify this requirement with local counsel.

🛑 Should I pay the funeral home out of my own pocket if the estate is broke?

You should be very cautious. While funeral expenses are often high priority, if the estate has absolutely zero assets, you may never be reimbursed. Always confirm the estate’s total liquid assets before fronting personal money.

🏠 If the estate is insolvent, do we have to sell the house?

Often, yes. If the house has equity, it is considered an asset of the estate. That equity usually must be unlocked (by selling the property) to pay off the priority creditors before beneficiaries can inherit anything.

💼 Can the executor still get paid if the estate is insolvent?

Executor fees are typically considered “costs of administration,” which generally sit at the highest tier of priority. However, if the estate has literally zero liquid assets, there may simply be no money available to pay your fee.

👨👩👧 Do family members inherit anything from an insolvent estate?

Usually, no. Creditor claims must be settled before inheritances are distributed. If the debts wipe out the assets, the beneficiaries will not receive the financial inheritances listed in the will.

🏦 What if a joint account holder takes the money before debts are paid?

True joint accounts with rights of survivorship generally pass directly to the surviving owner and bypass the probate estate entirely. They are usually not considered part of the estate’s available assets to pay general insolvent debts, though complex exceptions can exist.

🚪 How do I close an estate when there is no money left?

Closing an insolvent estate usually requires submitting a final accounting to the court that proves the assets were depleted by higher-priority claims (like admin costs or taxes). An attorney typically drafts this petition to formally discharge the executor and close the matter.

⚖️ What should I do if a creditor threatens to sue the estate?

Log the threat and immediately pass the communication to your estate attorney. Creditors can threaten legal action, but if the estate is demonstrably insolvent and following the local priority laws, a lawsuit often yields them nothing.

🛡️ Are life insurance payouts subject to insolvent estate debts?

If the life insurance policy names a specific living beneficiary, the payout usually goes directly to that person and bypasses the estate completely, making it safe from estate creditors. It only becomes an estate asset if the estate itself is named as the beneficiary. You should proactively request a status letter from the insurance company to confirm exactly who the listed beneficiary is before making any assumptions.

✈️ Can I reimburse myself for travel expenses if the estate runs out of money?

Travel expenses tied strictly to estate administration are usually high-priority claims. However, if you reimburse yourself without court or legal approval while other priority costs remain unpaid, you risk having to return those funds. Always log the expense but wait for legal clearance.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.