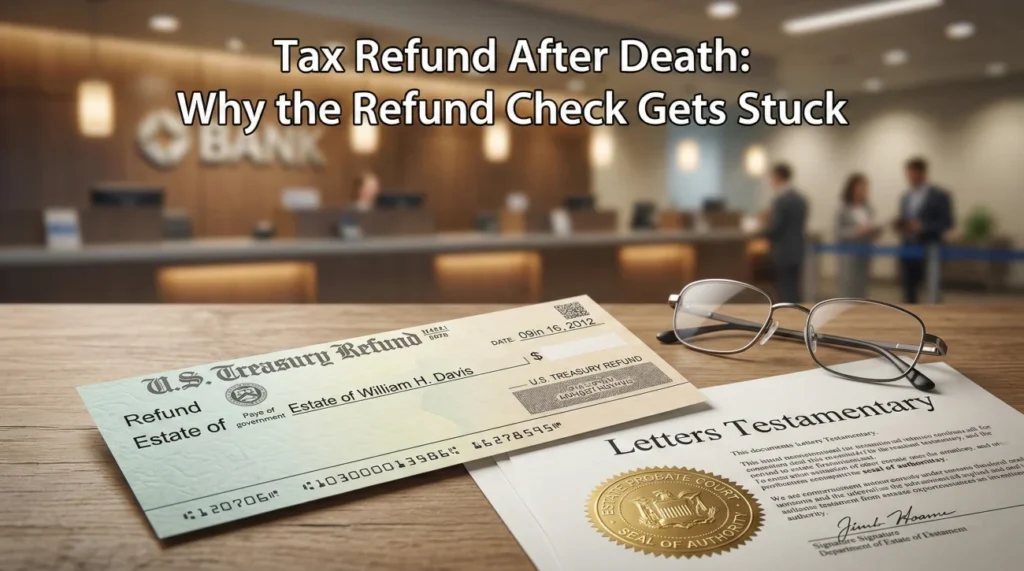

- A tax refund for a deceased person is usually issued to the “Estate of” the individual, creating a strict paperwork barrier for depositing the funds.

- Timelines often stretch for months, especially if an initial direct deposit attempt bounces and converts to a paper check.

- Banks require a specific “paperwork bridge” proving your legal authority before they will allow the check to clear into an official estate account.

- Late-arriving checks or joint-filer situations require specific handling to avoid reopening closed estate accounts.

The Paperwork Trap of a Final Tax Refund

Opening a piece of mail to find a tax refund check is usually a moment of relief. For an executor, however, that relief is often short-lived. A very common pattern in estate administration occurs when someone takes that final refund check to the bank, expects a simple deposit, and instead walks out confused and empty-handed.

If you are wondering about a tax refund after death who gets it, the short answer is that the refund belongs to the estate, not directly to the heirs. The long answer involves strict compliance rules that trap many well-meaning families.

Tax agencies do not know who the beneficiaries are, and banks are heavily penalized if they allow the wrong person to cash a check. Because of this, the refund almost always gets stuck in a paperwork bottleneck. Drawing from patterns I see regularly, my goal here is to help you understand why this bottleneck exists, how to build the exact document packet banks need, and what timelines to expect so you can track this asset without losing your patience.

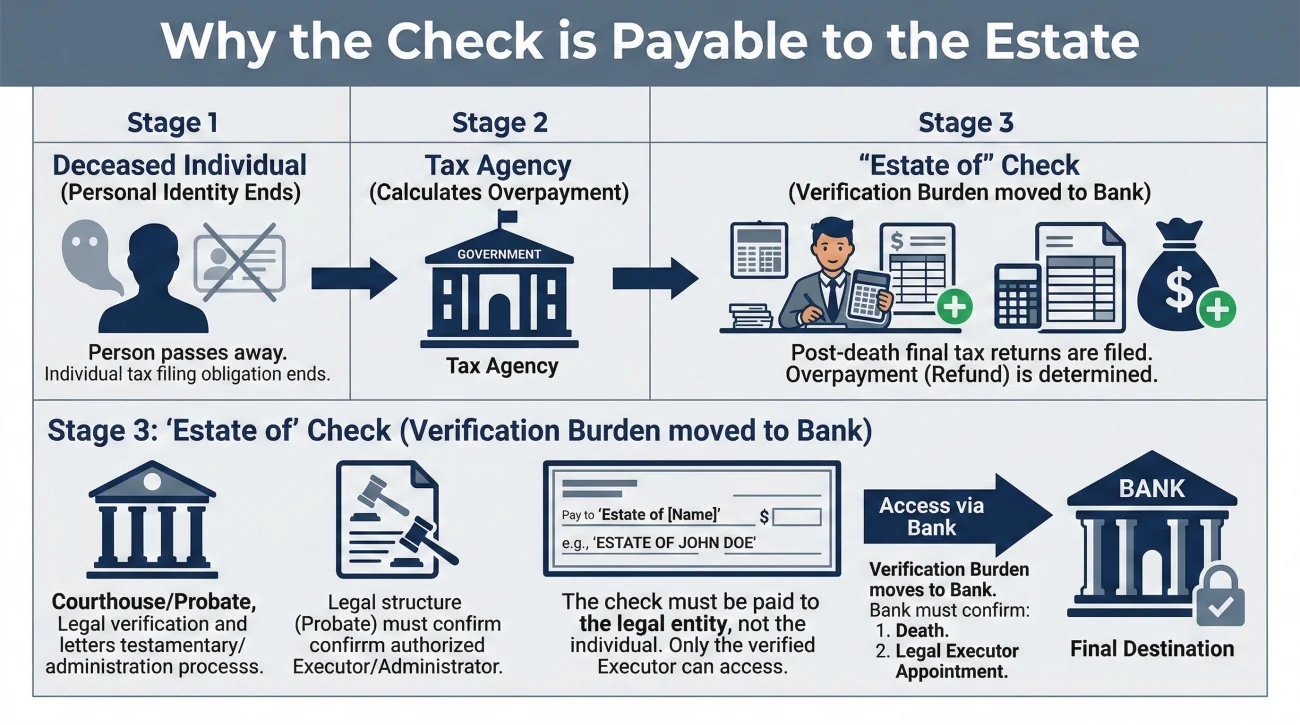

Why the Check is Payable to the Estate

The core of the friction starts with understanding the “payee line” printed on the front of the check. When an individual passes away, their personal financial identity effectively ends, but the tax system still needs to settle their final balances. If they overpaid, the government issues a refund.

However, the government cannot write a check to a deceased person because that person can no longer legally endorse it. They also will not write the check out to “the surviving children” or the “named executor” because the tax agency has no mechanism to verify the validity of a will or a family tree. That is the court’s job.

To solve this jurisdictional problem, tax agencies issue the refund payable to the “Estate of” the deceased person. By doing this, the government passes the responsibility of verification over to the banking system. They are essentially saying, “We owe this money to the estate; we will let the local bank verify who holds the legal authority to claim it.”

Assuming that holding a valid will or being the closest living relative gives you automatic clearance to endorse the back of the check.

Recognizing that a check made out to “The Estate Of” is locked until formal, court-validated authority is presented.

Common Delivery Paths and Why Direct Deposits Bounce

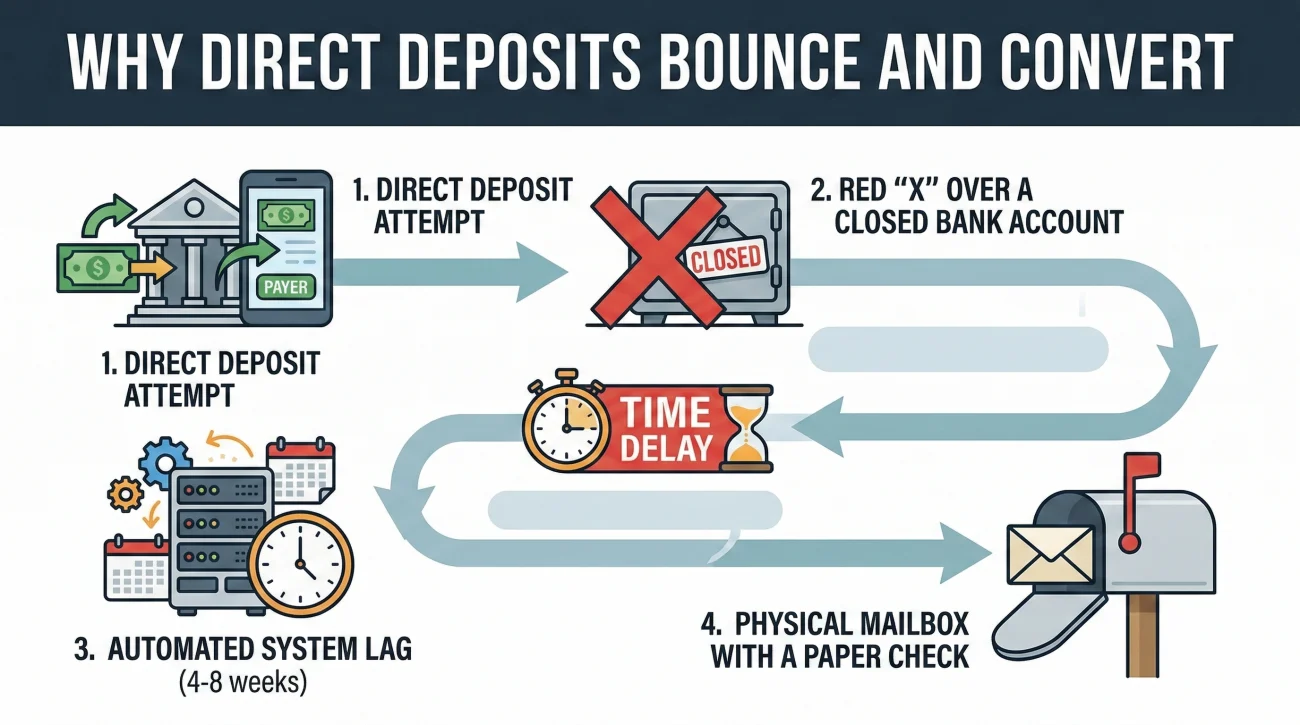

How and when the refund physically arrives is another area that causes significant anxiety. If the deceased person had their taxes set up for direct deposit for years, families naturally expect the final refund to follow that same invisible, automatic path. Unfortunately, the timeline is rarely that smooth.

Here is what typically happens behind the scenes:

- 📄 The account is already closed: If the executor has already notified the bank of the death and closed personal checking accounts to consolidate funds, the tax agency’s direct deposit attempt will hit a wall. The bank’s system automatically rejects the transfer.

- ✅ The account is frozen: Even if the account remains open, banks often place an automatic freeze upon receiving a death notification. A frozen account generally cannot accept incoming automated clearing house (ACH) transfers, causing the refund to bounce back.

- ⏳ The paper check conversion timeline: When a direct deposit fails, the tax agency’s automated system does not immediately mail a check. It usually waits a few weeks, logs the failed transfer, and eventually triggers the printing of a physical check. This conversion process alone commonly adds four to eight weeks to your waiting period.

Key Point: If you are waiting on a direct deposit refund that seems delayed, it is highly likely that the transfer bounced. Do not panic; a paper check is likely making its way through the mail system. Once you finally have that physical check in hand, the real challenge begins.

The Paperwork Bridge: What Unblocks the Deposit

With the check finally in your possession, the next step is getting the banking system to accept it. Because the check is payable to the estate, it generally must be deposited into an official estate bank account. You cannot simply drop it into your personal checking account or the deceased’s old joint account.

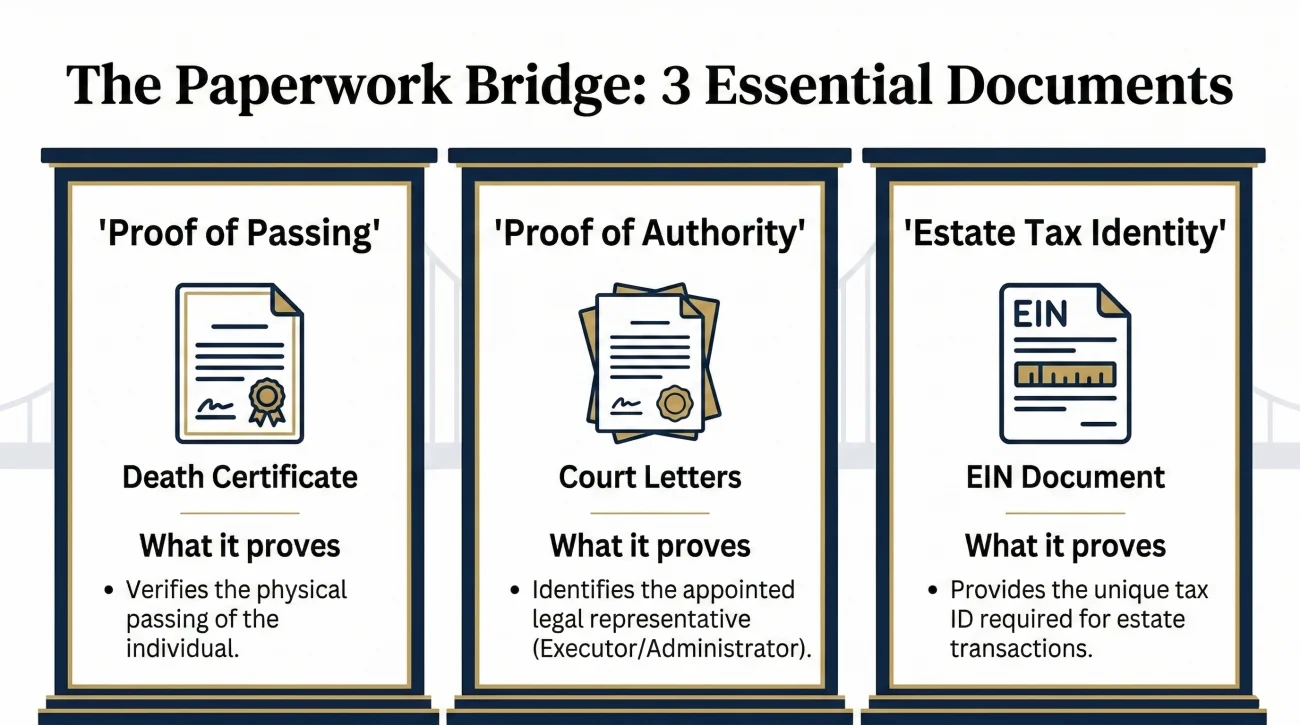

To open that estate account and clear the check, you must build what I call a “paperwork bridge.” This bridge proves to the bank’s compliance department that you are the legally authorized person to handle the funds. While every institution has slightly different rules, the required documents generally fall into three strict categories.

| Document Category | What It Proves to the Bank | Common Real-World Examples |

|---|---|---|

| Proof of Passing | Confirms that the individual is no longer living and their personal accounts should be transitioned. | A certified death certificate (banks usually want to see the original physical stamp or seal). |

| Proof of Authority | Proves that a court or local jurisdiction has officially appointed you to handle the financial matters. | Letters of administration, letters testamentary, or a validated small estate affidavit. |

| Estate Tax Identity | Gives the estate its own unique tracking number for financial reporting, separate from the deceased person’s old identity. | An Employer Identification Number (EIN) issued specifically for the estate. |

In practice, organizing these documents into a single, clean folder before you walk into the branch often makes the conversation with the bank manager much more productive. It signals that you are organized and understand their compliance needs.

The Exception: Surviving Spouses and Joint Returns

There is one major scenario where the standard “Estate Of” rules often bend: when a surviving spouse files a joint final tax return. This is a very common situation, but it still has its own set of hurdles.

When a joint return is filed for the year the death occurred, the tax agency will typically issue the refund check made out to both spouses (e.g., “John Doe Deceased & Jane Doe”). Because the surviving spouse’s name is explicitly on the check, they often bypass the need to open a formal estate account.

However, depositing a joint check when one payee is deceased still triggers standard bank compliance checks. A surviving spouse usually cannot just use an ATM or a mobile deposit app for this. They typically need to visit a branch in person, present their ID, and provide a certified copy of the death certificate to prove why the second signature is missing. Always check with the specific bank first, as some conservative institutions may still require additional paperwork to clear a joint check.

How to Communicate Safely About the Refund

Even with a paperwork bridge prepared, interactions at the bank can sometimes stall. Bank tellers are trained to follow rigid compliance rules, and if they feel pressured or unsure about an estate check, their default action is to freeze the process and escalate it to a risk department.

Instead of arguing over the counter, a safer approach is to request their specific written requirements before you even attempt the deposit. If you call the bank ahead of time or send a secure message, use a calm, procedural tone. I always find it helpful to frame the request using a simple structure: [Action] + [What you need in writing] + [Confirmation request].

Here is an example of how that looks in practice:

Subject: Request for estate deposit requirements

Hello, I am the appointed executor for the estate. I have received a tax refund check made payable to the estate, and I need to open an estate account to deposit it.

Could you please provide a written checklist of the exact documents your legal department requires to open the account and accept this specific type of deposit?

I want to make sure I bring exactly what your compliance team needs on my first visit. Please let me know if you need to schedule an appointment for this.

This approach works because it removes emotion and frustration from the equation. You are simply asking for their operating procedure, which creates a helpful paper trail that protects you if there are administrative delays later.

Fitting the Refund into Your Recordkeeping System

A tax refund is an asset, and like any other asset, it must be properly tracked. Executors sometimes lose track of the details because they are so focused on just getting the check cleared. Once the money hits the account, the paper trail goes cold.

Disputes can arise months later if a beneficiary questions the exact amount of the tax refund, and the executor has no proof other than a vague line item on a bank statement.

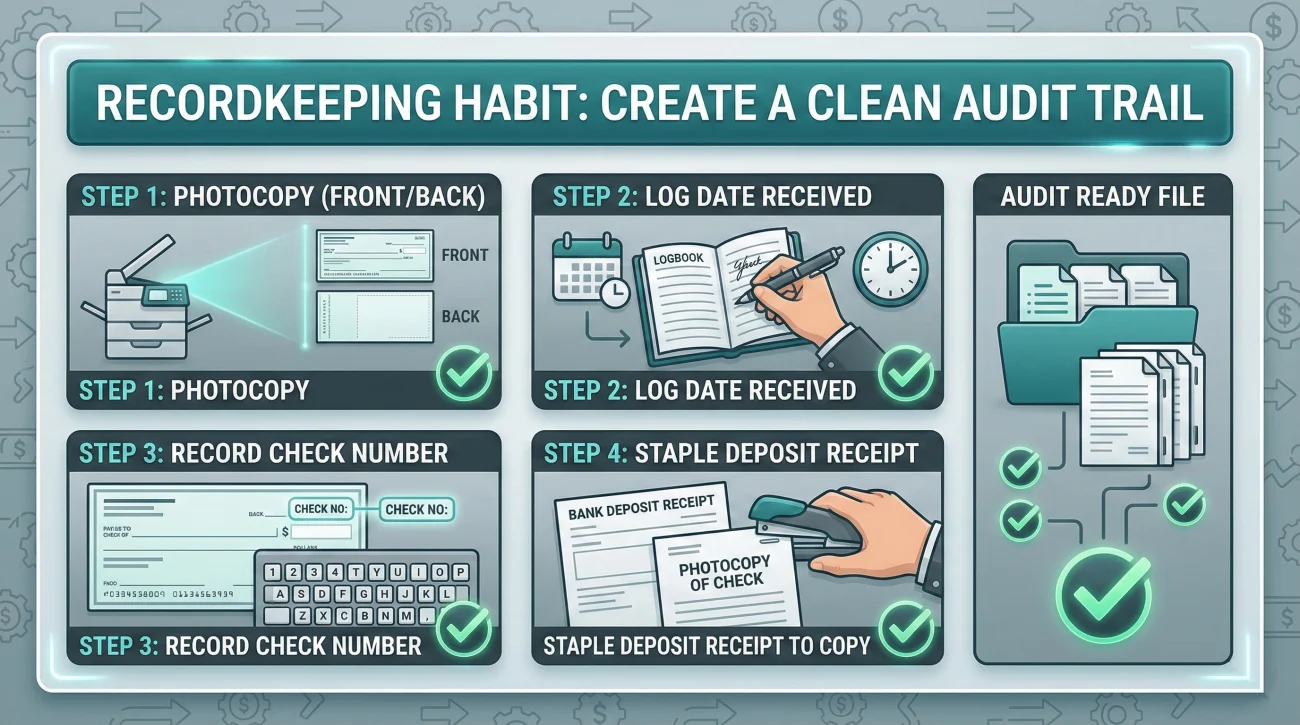

⚠️ Warning: Never hand over a tax refund check to a bank teller without making a front-and-back photocopy first. Once the bank takes it, you will likely never see the physical document again, and requesting an archival copy from the bank can take weeks.

Here is the standard logging habit that creates a clean audit trail:

- ✅ Make a clear copy of the front of the check immediately.

- ✅ Log the date the check was physically received in the mail.

- ✅ Log the exact dollar amount and the check number in your asset inventory.

- ✅ After the bank visit, staple the bank deposit receipt directly to your photocopy of the check.

If anyone ever asks to verify the source of those funds, you can simply pull the file, show the photocopy of the check, and show the deposit receipt matching it perfectly to the estate account balance.

Common Stalls and Missing Information Loops

Even when you do everything right, things can stall at the tax agency level. Knowing what these administrative hiccups look like can save you weeks of panic and confusion.

One frequent issue is a name mismatch. If the court documents list the person as “Robert J. Smith,” but the tax agency issues the check to the “Estate of Bob Smith,” the bank’s fraud software might flag the deposit. In these cases, you cannot just cross out the name and rewrite it.

❌ Note: Do not attempt to use white-out, alter the payee line, or add secondary endorsements to a tax check. Altering a government-issued check is a massive red flag and will almost certainly result in the check being confiscated pending a fraud investigation.

Another incredibly common stall involves missing representative paperwork during the initial tax filing. Tax agencies do not just take your word for it that you are the executor. They often require specific supplementary documents, usually a statement of person claiming refund or a notice of fiduciary relationship, to officially link your name to the deceased person’s tax profile.

If these forms are missing when the final return is filed, the agency usually will not call you to ask for them. Instead, the process silently halts. Weeks or months later, you might receive a vague rejection letter stating that your authority could not be verified. To avoid this loop, ensure your tax professional explicitly includes all required representative documentation when filing the final return, and always keep certified mail receipts of what was sent.

The Nightmare Scenario: The Check Arrives After the Estate is Closed

There is one situation that is one of the most disruptive situations an executor can face: the estate is fully settled, the bank accounts are closed, the money has been distributed, and then, six months later, a straggler tax refund check arrives in the mail.

Because the check is payable to the estate, you cannot cash it, but the estate account no longer exists to accept it. In these cases, you generally have two paths, depending on local rules and the size of the check.

For larger amounts, you may have to petition the court to temporarily reopen the estate just to process the check, a slow and sometimes costly process. For smaller amounts, some jurisdictions allow you to use a small estate affidavit or a specific banking waiver to bypass reopening the estate. If this happens to you, do not attempt to force the check through a personal account. Pause, hold the check safely, and contact the attorney or clerk who helped you close the estate to ask for the most efficient local workaround.

Final Thoughts: A Buffer, Not a Windfall

Successfully navigating the paperwork bridge and getting the refund deposited is a major milestone, but it is critical to remember the mental model of estate administration: a tax refund is a recovery of estate assets, not an immediate windfall for the beneficiaries.

A common mistake is assuming that because the tax money is finally in the bank, it is safe to immediately write checks to the heirs. That money is subject to the estate’s overall obligations. Before any distribution happens, you must ensure you have followed a safe order of operations.

Have all administrative costs been reimbursed? Are there other outstanding creditor claims? Is there a possibility of an estate-level income tax bill later in the year? The Executor Creditor and Debt Checklist covers exactly this order of operations in detail. Treat the refund as a protective buffer within the estate account, keeping it secure until you are absolutely certain the entire debt and tax landscape has been cleared.

❓ FAQ

🕒 How long does a deceased tax refund check take to arrive?

It can take anywhere from a few weeks to several months. If an initial direct deposit bounces, the automated system can take an additional four to eight weeks just to convert the refund into a physical paper check.

🏦 Can I deposit an estate check into my personal account?

Generally, no. Banks require a check made payable to an “Estate of” to be deposited into a formal, dedicated estate bank account to prevent commingling of funds and ensure proper tracking.

✍️ Who signs a tax refund check for a deceased person?

The officially appointed executor typically endorses the check, often signing their own name followed by their legal title (e.g., “Jane Doe, Executor”). Always verify the exact endorsement format with your specific bank.

🛑 Why did the bank reject the direct deposit for the tax refund?

Direct deposits usually fail if the deceased person’s personal checking account was closed during early administration, or if the bank placed an automatic freeze on the account upon receiving a death notification.

📝 Do I need a special tax ID to cash an estate refund?

Yes. To open the estate bank account required to deposit the check, banks typically require an Employer Identification Number (EIN) issued specifically for the estate.

👨👩👧👦 Can a surviving spouse just deposit a joint tax refund?

If the refund is issued jointly (to both spouses), the surviving spouse can often deposit it, but they usually must visit a branch in person with a certified death certificate to bypass fraud flags for the missing second signature.

⚖️ Does a tax refund have to go through probate?

Often, yes. Because the refund is money owed to the individual prior to death, it becomes an official asset of the estate and is typically subject to local probate rules and creditor claims.

🔒 What happens if the check arrives after the estate is closed?

You cannot cash it directly. Depending on the amount and local rules, you may need to temporarily reopen the estate through the court, or use a specific small estate affidavit to claim the funds.

📩 What if the deceased tax refund check gets lost in the mail?

You must contact the issuing tax agency to report it lost. They will initiate a trace on the original check and eventually reissue a new one, which restarts a potentially lengthy waiting period.

📑 What documents do I bring to the bank to deposit an estate refund?

You typically need to bring a certified death certificate, your court-issued documents proving your authority (like letters testamentary), the estate’s EIN documentation, and your own personal ID.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.