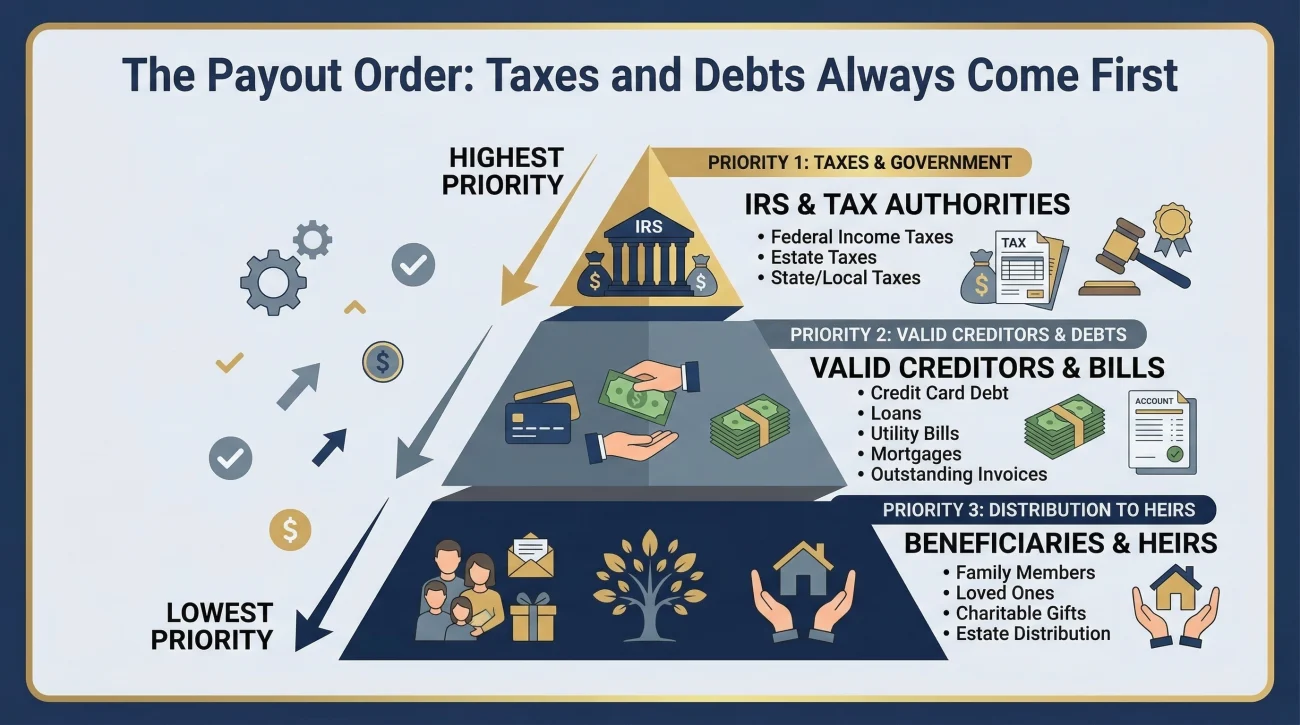

- The big picture: Distribution is not the first step of estate administration; it is the final milestone after all legal and financial obligations are cleared.

- The core rule: You must clear known debts, wait out the statutory creditor claim window, and handle tax filings before moving any money to heirs.

- The documentation packet: A clear, structured final accounting report protects you from beneficiary disputes and misunderstandings.

- The reserve strategy: Seasoned executors rarely distribute 100% of the funds at once. Holding back a small “buffer” prevents out-of-pocket costs for trailing expenses.

The Pressure to Payout: Balancing Beneficiary Expectations and Executor Duty

In my experience supporting estate administration workflows, the single most common question people ask is: when can an executor distribute money? Often, this question does not come from the executor, but from anxious family members texting or calling every week to ask when they will receive their share.

I completely understand the pressure. You want to honor the deceased person’s wishes, help out family members who might need the funds, and frankly, you want to close the project and move on. It is incredibly stressful to be the gatekeeper of an inheritance.

However, handing out money too quickly disrupts the entire legal sequence of an estate. The law generally views the estate’s money as belonging to its creditors and the tax authorities first, and the beneficiaries second. This guide is a practical, calm map of the milestones you typically need to clear before you can safely write those final checks without putting yourself in a compromised position.

“When do we get the money?” is the hardest question to answer. The best response is usually a calm explanation of the required clearance steps remaining, rather than guessing a specific date.

The Sequence of Estate Funds and The Risk of Skipping Ahead

To understand the timeline, we have to talk about why the sequence exists. An executor’s primary job in the early stages is not distributing wealth; it is gathering assets, protecting them, and paying valid obligations. Only what is left over belongs to the heirs.

I frequently see executors who feel bad for a sibling or a friend and decide to hand out a “small” portion of the estate early on. The problem arises three months later when an unexpected medical bill, a lingering utility adjustment, or an unanticipated tax liability arrives in the mail.

If the estate bank account is empty because the funds were already distributed, you face a terrible choice. You either have to ask the beneficiaries to give the money back (which almost never works), or you become personally liable and have to pay the estate’s bill out of your own pocket.

Guessing the timeline based on when the house sells, sending checks immediately, and leaving the estate account empty while assuming no more bills will arrive.

Using the expiration of the statutory creditor claim window as a hard boundary, and transferring funds only after receiving written tax clearance.

This is why understanding your overall executor creditor and debt checklist is so critical. You have to know exactly what the estate owes before you can safely determine the final number to distribute.

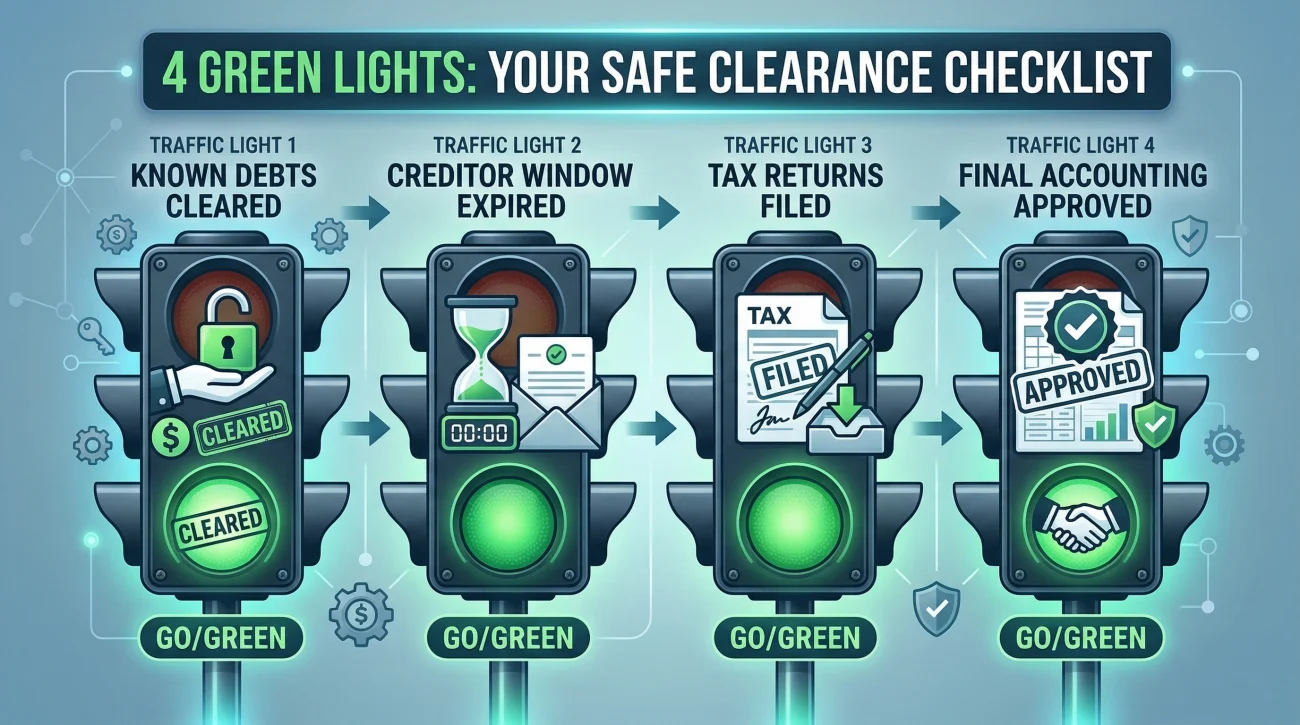

The Executor’s Pre-Distribution Clearance Checklist

So, how do you know when it is actually safe to move forward? In day-to-day admin work, I encourage executors to look for four specific clearance milestones. Think of these as traffic lights that must turn green before you can proceed with the final transfer.

1. Mapping and Clearing Known Debts

The first milestone is resolving the bills you know about. This means tracking down the everyday obligations: final utility bills, credit cards, medical invoices from a final illness, and any outstanding loans.

The goal here is not just paying them, but getting written confirmation that the accounts are closed with a zero balance. I have seen cases where an executor paid a final credit card bill online, assumed it was done, and distributed the estate. Weeks later, a new statement arrived with residual interest charges. Always get it in writing.

Here is a safe, polite script you can use to request final closure from a known creditor:

Subject: Request for Final Payoff Statement – Estate of [Name]

Hello,

I am the executor for the estate of [Name]. I am writing to request a final payoff statement for account ending in [XXXX].

Please provide a written statement showing the exact amount required to settle this account in full, valid through [Date]. Once paid, please also confirm the process for receiving a written notice that the account is closed with a zero balance.

Thank you,

[Your Name]

Executor

2. Waiting Out the Creditor Claim Window

Resolving known debts is only half the battle. You also have to protect yourself against unknown creditors. When I guide executors through this phase, the biggest blind spot is usually the “silent” waiting period.

This window typically starts the day you publish a formal notice to creditors in a local paper. While you wait (often for several months), your job is not to proactively search for every possible obscure debt, but rather to monitor the mail and log any formal claims that arrive. If the window closes and no unknown creditors have filed a valid claim, you have effectively cleared this hurdle. You do not have to wait forever, just until the statutory clock runs out.

3. The Tax Clearance Lane

Taxes are the quietest but most rigid hurdle in the estate distribution timeline. Tax authorities generally hold priority over beneficiaries, meaning the estate must be tax-compliant before the wealth transfers.

This usually involves two separate lanes: the deceased person’s final individual income tax return, and an estate income tax return. This second lane is a common blind spot. For example, if you manage a probate property and collect rent from tenants for six months before selling it, or if estate investment accounts generate significant dividends while you are gathering assets, the estate itself may need to file a separate tax return for that new income.

You want to have these returns filed, the taxes paid, and ideally, documentation from your tax professional confirming that the obligations are satisfied before you release the funds.

4. Preparing the Final Accounting

Before money changes hands, beneficiaries have a right to see the math. A final accounting is not just a casual email saying “here is what is left.” It is a structured, easy-to-read report that proves you handled the funds responsibly.

When I help build these packets, I always recommend including:

- 📄 Starting Inventory: The total value of the estate on the day the person died.

- 📈 Income: Any money the estate earned while open (property sales, refunds, dividends).

- 📉 Disbursements: An itemized list of every debt, administrative expense, and tax bill paid.

- ✅ Proposed Distribution: The final math showing exactly how the remaining balance is divided.

If a beneficiary disputes the math, you pause. You do not distribute until they sign a receipt and release form, or until the issue is formally resolved.

Is a Preliminary or Partial Distribution Safe?

Executors dealing with very large, clearly solvent estates often ask if they can make a partial distribution early on to ease family tension. While this is sometimes done, it requires extreme caution.

A preliminary distribution means handing out a portion of the inheritance before the final tax returns are filed or the creditor window is completely closed. If you choose this route, you must retain a massive safety margin in the estate account. I usually see operators hold back double or triple the estimated remaining costs just to be safe. For most standard estates, the cleanest and safest path is to simply wait and do one comprehensive final distribution.

The “Reserve” Concept: Holding a Buffer Before the Final Transfer

Even with a signed final accounting in hand, seasoned operators know better than to drain the estate bank account to zero immediately. Instead, they hold back a safety net called a reserve.

A reserve is a calculated buffer amount that you leave in the estate bank account while the bulk of the money is distributed. Why do this? Because trailing expenses are incredibly common. You might need to pay a CPA to file a final tax return the following spring, cover a minor bank fee to close the account, or handle a lingering final invoice from an appraiser.

Key Point: A reserve protects you from having to ask beneficiaries to open their wallets to cover a $300 final administrative expense six months after you thought the estate was closed.

Communicating this to beneficiaries requires clarity so they do not think you are withholding money for no reason. Here is a practical way to phrase it in an update email:

Subject: Estate Update: Upcoming Distribution and Final Reserve

Hello everyone,

I am pleased to report that we have cleared the formal creditor period and finalized the main tax filings. We are now preparing for the primary distribution.

I will be distributing the bulk of the estate funds shortly. However, as is standard practice, I will be holding a small reserve of [Amount/Percentage] in the estate account for the next few months. This buffer is strictly to cover any trailing administrative costs, such as the final tax preparation fee next spring.

Once those final, minor expenses are cleared and the estate account is ready to be fully closed, the remaining balance of this reserve will be distributed equally among you.

I will send out the final accounting documents next week for your review.

Best regards,

Executor

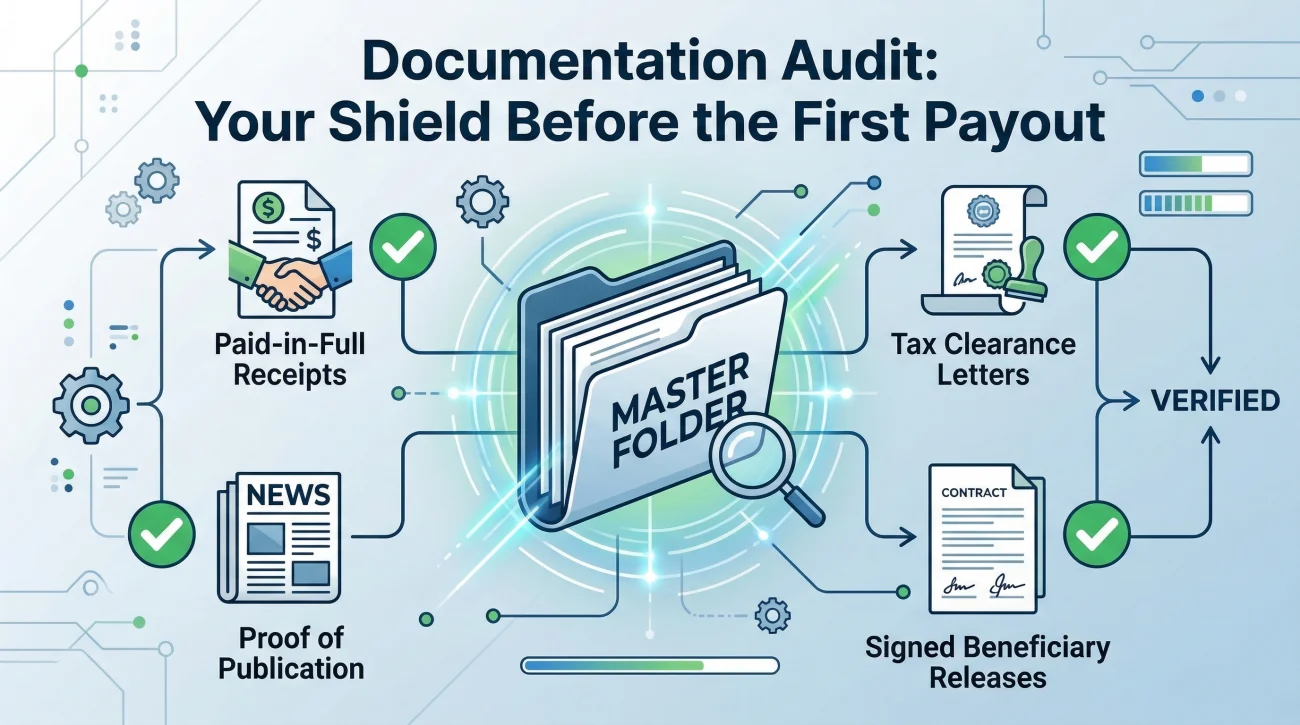

What to Keep on File Before Any Money Moves

Documentation is your shield. Before you write a single distribution check, you must ensure your paper trail is flawless. If questions arise a year later, your memory will not protect you, but your organized files will.

When preparing to execute your estate distribution checklist, I recommend doing a quick audit of your own files. Make sure you have clean digital or physical copies of the following items:

| Document Category | What to Confirm Before Distributing |

|---|---|

| Creditor Receipts | Confirm you have a “paid in full” or zero-balance statement for every debt you resolved. |

| Tax Clearances | Save copies of all filed returns, proofs of payment, and any closing letters or CPA confirmations. |

| Claim Window Proof | Keep the proof of publication from the newspaper and any records showing the waiting period expired. |

| Beneficiary Signatures | Log the signed receipts and releases from beneficiaries acknowledging they reviewed the accounting. |

💡 Pro Tip: Create a dedicated master folder called “Pre-Distribution Clearances.” Do not distribute funds until that folder contains the documentation proving that all prerequisite steps are fully completed.

Final Thoughts on Reaching the Finish Line

Figuring out when to distribute money is the ultimate test of an executor’s discipline. Throughout the process, you have had to act as a project manager, a record keeper, and a mediator. Holding back funds while family members ask for updates requires a thick skin.

But when you finally reach this stage, having respected the waiting periods, cleared the taxes, and built a transparent final accounting, the dynamic shifts. You are no longer just managing a stressful checklist; you are successfully bringing the estate to a secure close. Take the time to finalize your paper trail. That careful, measured approach is exactly what ensures the final distribution brings peace of mind for everyone involved, especially you.

❓ FAQ

🕰️ How long does the entire distribution phase typically take?

There is no universal timeline. Because you must wait out local creditor claim windows and process tax returns, a standard timeline often spans anywhere from nine months to over a year before the primary distribution can happen safely.

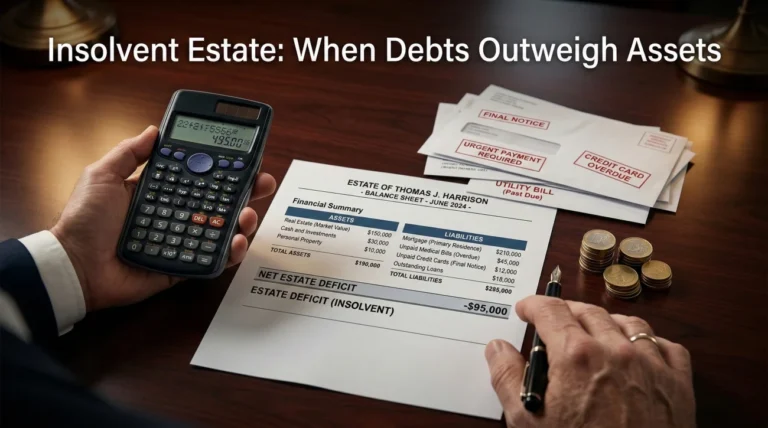

📉 What happens if the estate does not have enough money to pay everyone?

This is called an insolvent estate. In this case, beneficiaries usually receive nothing. You must pause all payouts and typically follow a strict legal priority list to pay certain creditors (like funeral homes or the IRS) before others.

👶 How does an executor distribute inheritance to a minor?

You generally cannot hand a check directly to a minor. Depending on the will and local rules, funds are usually routed into a custodial account, a trust, or held by a legally appointed guardian for the minor’s benefit.

👻 What should I do if a beneficiary cannot be located?

You cannot simply divide their share among the others. You must make a documented, good-faith effort to find them. If they still cannot be found, their share is usually deposited with the court or state unclaimed property division.

💻 Do digital assets and online accounts impact the distribution timeline?

Yes. Digital assets (like cryptocurrency or income-generating online accounts) must be located, valued, and converted or transferred just like physical assets. Skipping them can result in an inaccurate final accounting.

✍️ What if a beneficiary refuses to sign the final release form?

If a beneficiary disputes your accounting and refuses to sign a receipt and release, do not distribute their funds. You will likely need to present your accounting to the probate court and have a judge formally approve it before moving forward.

🏦 Can I use my personal bank account for the final estate distributions?

Absolutely not. Estate funds must remain in a dedicated estate bank account (using the estate’s EIN) until the moment they are distributed. Mixing estate money with your personal funds is highly improper and invites immediate suspicion.

🏡 If the main asset is a house, do I have to sell it to distribute?

It depends on the will and the estate’s cash flow. If the estate has enough liquid cash to pay all debts and taxes, the house might be transferred directly to the heirs. If there is no cash, selling the house is usually required to cover the obligations.

📑 Do beneficiaries have to pay income tax on the inheritance they receive?

In most standard cases, the core inheritance itself is not subject to income tax for the beneficiary. However, if they inherit a pre-tax retirement account (like a traditional IRA) or if the estate distributes income earned during the probate process, tax rules change.

🛑 Is there any situation where an executor can be forced to pay early?

Beneficiaries cannot force an executor to skip mandatory debt clearance or tax payments. The only authority that can order an early distribution is the probate judge, and they rarely do so if debts are still outstanding.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.