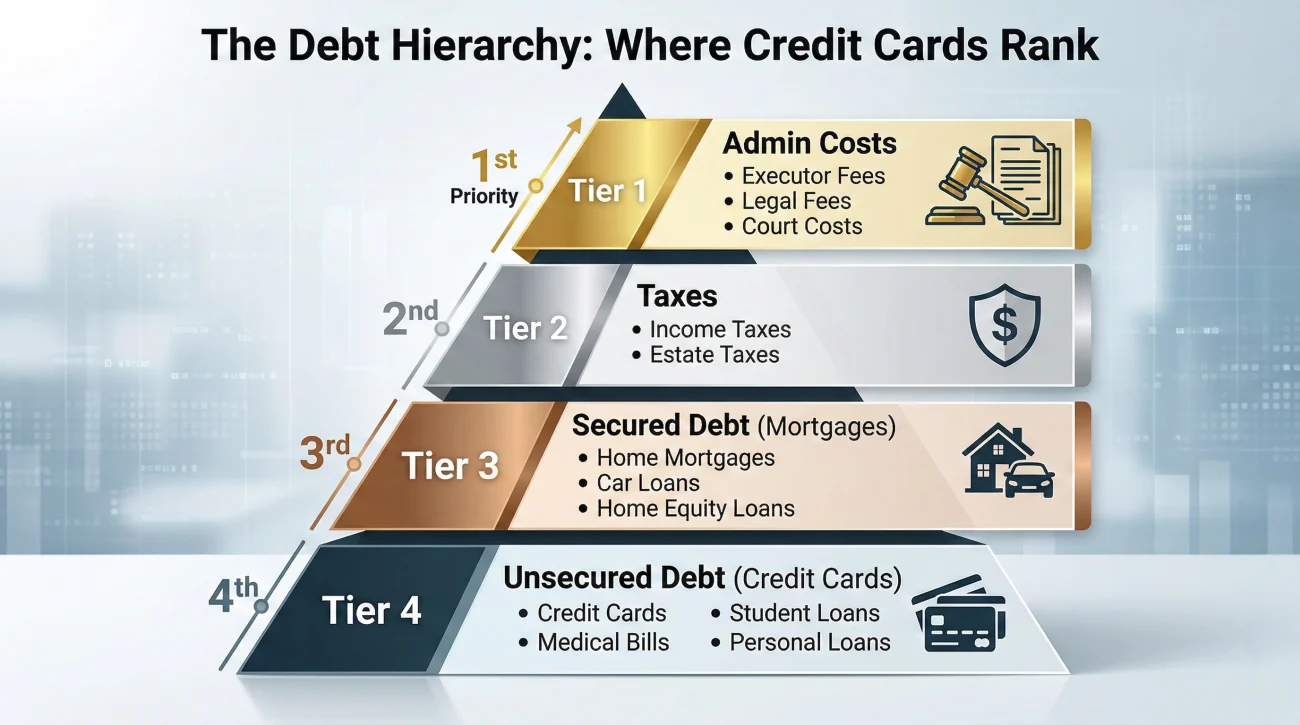

- Credit card balances are unsecured claims against the estate, meaning they typically sit near the bottom of the payment priority list.

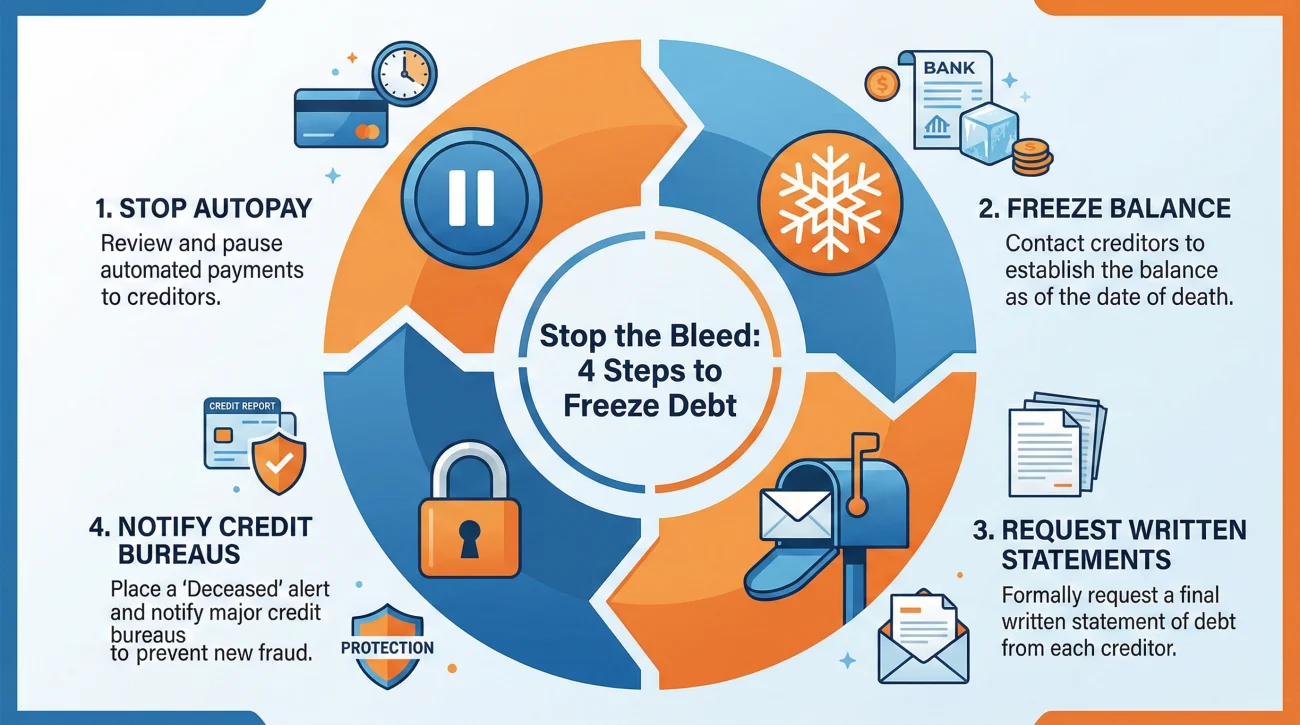

- Stop the bleed immediately by pausing autopay subscriptions and notifying the major credit bureaus to lock the deceased’s profile against fraud.

- Debt collectors rely on creating urgency. Shift the burden back to them by proactively sending your formal notification of death and request for balance via certified mail.

- Never use your personal funds to pay off the deceased person’s credit card, and hold off on using estate funds until you are certain the estate is solvent.

The Ringing Phone and the Stack of Statements

In my experience working alongside executors, one of the most stressful moments happens about a month after the passing. The mail starts arriving, and the phone starts ringing. Suddenly, dealing with credit card debt after death executor duties feels less like a quiet administrative task and more like putting out fires. A debt collector calls, their tone is urgent, and they make it sound like you need to write a check by the end of the business day.

When someone passes away, their credit card debt does not magically disappear, but it also does not instantly become an emergency. The debt typically belongs to the estate, not to you personally. The person calling you is doing their job, which is to collect money as fast as possible. Your job as the executor is entirely different: you are there to gather information, protect the assets, and ensure everything is handled systematically.

Often, executors make honest mistakes simply because they want to “do the right thing” and stop the phone from ringing. They might pay a $500 Visa bill out of their own pocket, assuming they will get reimbursed later. In estate administration, paying things out of order or from the wrong account is a common way files get messy and families start asking questions. Before you write a single check, you need a clear view of the board.

Separating Facts from Collector Pressure

When you answer a call from a credit card company or a collection agency, the conversation is designed to end with a payment commitment. In day-to-day admin work, I see a clear pattern: the longer an executor stays on the phone, the more confused they get about what they are actually required to do.

You need to separate the pressure from the process. The goal is to shift the burden of proof back to the creditor. You are not refusing to acknowledge the debt; you are simply requiring them to follow formal procedures. And you do this by moving the conversation off the phone and into the mail.

Answering a collection call, feeling pressured to explain the estate’s financial status, and promising to send a payment “as soon as the bank account opens.”

Politely informing the caller of the passing, refusing to discuss account balances over the phone, and requesting that all formal claims be sent to you via certified mail.

Securing the Date-of-Death Balance and Stopping the Bleed

Before any funds leave the estate account, you need to establish the exact “date of death balance.” This is the precise amount owed on the day the person passed away. I have seen countless situations where an executor paid a balance based on an old statement they found on a kitchen counter, only to find out later that the balance included late fees applied after the date of death, or worse, fraudulent charges.

To freeze this balance accurately, you must also look for recurring charges. If the deceased had a Netflix account, a gym membership, or a utility bill on autopay, those services will continue to charge the credit card every month, artificially inflating the debt. Your first operational step is to identify and cancel these subscriptions directly with the service providers.

⚠️ Warning: The “Right of Setoff” Trap. There is one major exception to your ability to freeze payments safely. If the deceased had a credit card and a checking account at the exact same bank, the institution often has a legal “right of setoff.” They can automatically sweep funds from the checking account to pay the credit card balance without asking your permission. If you discover this setup, those funds are highly vulnerable until you establish a proper, separate estate account.

Script for Handling the First Creditor Call

When a credit card representative calls, keep it brief and professional. Do not offer extra information about the estate’s total value.

“Hello, I am calling regarding the balance on Mr. Smith’s account. When can we expect payment?”

“Hello. I am the executor for Mr. Smith’s estate. Please be advised that he passed away on [Date]. I cannot process any phone payments or discuss estate assets at this time. Please freeze the account to prevent further fees and mail a formal, written statement showing the exact date-of-death balance to my mailing address at [Your Address]. Once received, it will be added to the estate’s formal review process.”

This script stops the immediate pressure, but you should not stop there. To build a true defensive paper trail, you must proactively send a formal notification of death to the credit card company via certified mail with a return receipt. Do not just passively wait for them to mail you. Sending your own certified letter proves exactly when the creditor was formally notified and legally forces them to acknowledge your timeline.

Building Your Credit Card Documentation Log

Once you have successfully paused the autopays and requested statements, your next immediate task is organizing the responses. A common mistake I see is the “scattered file” approach: one bill in the car, an email forward from a family member, and a voicemal saved on a phone. This makes tracking nearly impossible.

You need a central log. If a beneficiary ever asks why a specific card was paid a certain amount, or why the estate took so long to close, this log is your shield. Here are the minimum fields you should track for every discovered account:

| Institution Name | Account Details | Date of Death Balance | Status / Action Taken |

|---|---|---|---|

| Example Bank Visa | Ending in 1234 | Pending written confirmation | Called 10/12 to notify of death. Sent certified letter 10/13. |

| Store Credit Card | Ending in 9876 | $450.00 (Confirmed via mail) | Logged on 10/15. Placed in “Hold for Payment” folder. |

💡 Pro Tip: When you find physical credit cards in a wallet, the safest practical step is to cut them up immediately to prevent accidental use. Just remember to write down the issuing bank, the customer service phone number on the back, and the last four digits of the card for your log first.

The Reality Check: Where Credit Cards Sit in the Pay Order

One of the most vital concepts for an executor to grasp is that bills are not paid simply in the order they arrive in the mailbox. If you treat estate administration like your personal monthly budget, you will run into trouble. Estates must follow a specific sequence for paying obligations to ensure fairness and compliance.

While local rules vary, the general hierarchy of estate payments typically looks like this:

- 🥇 Stage 1: Estate Administration Costs. (Court fees, legal help, executor bonds, protecting physical property). You have to keep the estate running to settle it.

- 🥈 Stage 2: Taxes. (Federal and state). The government gets paid before private companies.

- 🥉 Stage 3: Secured Debt. (Mortgages, auto loans). Debts tied directly to a physical asset.

- 📉 Stage 4: Unsecured Debt. (Credit cards, medical bills, personal loans).

Notice where credit cards sit? At the very bottom. This is exactly why you must gather information rather than rushing to write checks. If you pay a credit card bill on day two, and realize on day sixty that the estate does not have enough cash to pay its taxes, you are in a difficult spot. To understand this hierarchy deeply, review our executor creditor and debt checklist.

Protecting the Estate: The Credit Bureau Step

Dealing with existing credit cards is only half the battle; preventing new ones from being opened is the other. Unfortunately, identity thieves routinely monitor obituaries to open fraudulent accounts under a deceased person’s name.

As an executor, it is a highly recommended best practice to contact the three major credit reporting agencies (Equifax, Experian, and TransUnion) to notify them of the death. You will usually need to send a copy of the death certificate via certified mail. This action places a “deceased notice” on the credit file, effectively locking the profile so no new lines of credit can be issued. This single step prevents massive administrative headaches down the road.

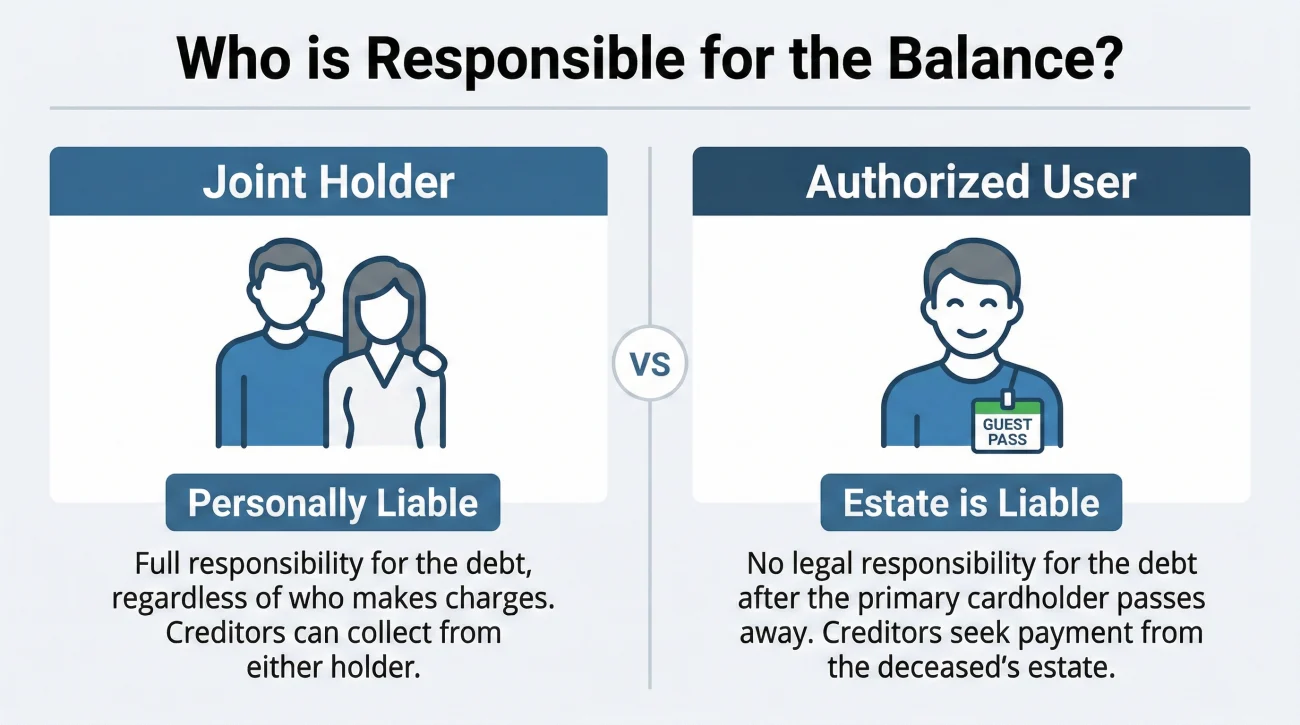

Common Misconceptions: Joint Accounts vs. Authorized Users

A major point of confusion is understanding exactly whose name is tied to the debt. I frequently see surviving spouses mistakenly drain their own savings to pay off a card they were merely an “authorized user” on, believing they were legally forced to do so.

There is a massive operational difference between the two:

- ✅ Joint Account Holder: This means two people applied for the credit together based on both of their credit histories. If one person passes away, the surviving joint account holder is typically fully responsible for the remaining balance.

- 📄 Authorized User: This is someone who was given a card to use, but the main account was entirely in the deceased person’s name. The authorized user is generally not responsible for the balance. The estate is.

⚠️ Warning: Even if you are an authorized user, you must stop using the card immediately upon the primary cardholder’s passing. Continuing to make purchases on a deceased person’s credit account is considered fraud and severely complicates the estate accounting.

When the Money Runs Short (The Insolvent Estate)

While logging phone calls is standard administrative work, finding out the estate is out of money requires a hard stop. If you add up the bank accounts and the total is $5,000, but the credit card debt alone totals $20,000, the estate is likely insolvent.

During the first 30 days of realizing an estate might be insolvent, your primary job is to pause absolutely all outward payments. When there is not enough money to go around, you cannot just pick and choose which credit cards to pay based on who is yelling the loudest on the phone. Doing so (paying Visa but ignoring Discover) can expose you to personal liability for playing favorites.

If you suspect insolvency, you must rely on local professional guidance to understand the proper, legal way to prorate payments or notify creditors that the estate is dry. Do not attempt to negotiate debt settlements on your own until a professional confirms the estate’s status.

Taking Control of the Narrative

Handling credit card debt as an executor is rarely about having all the answers on day one. It is about taking control of the communication flow. Every time a bill arrives, it should go through your filter: log the arrival, proactively send your formal notification via certified mail, and place the claim in a holding file until you understand the entire financial landscape of the estate.

By refusing to be rushed by collection tactics and insisting on a rigid paper trail, you protect the estate’s assets, you protect the beneficiaries’ inheritance, and you protect your own peace of mind. Let the creditors follow your timeline, not the other way around.

❓ FAQ

🏦 Can the bank automatically take money from checking to pay the credit card?

Yes. As mentioned earlier, if the deceased had a credit card and a checking account at the exact same bank, the institution often has a “right of setoff.” They may automatically withdraw funds from the checking account to cover the credit card balance without asking your permission.

✈️ What happens to the deceased person’s credit card rewards points or miles?

It depends entirely on the specific credit card company’s terms of service. Some companies forfeit all points immediately upon death. Others allow the executor to transfer the points to a beneficiary or redeem them for statement credit. You must ask the provider directly.

⚰️ Can I use the deceased’s credit card to pay for their funeral expenses?

No. Using the deceased’s credit card after they have passed away is considered fraudulent, even for legitimate estate expenses like a funeral. Funeral costs should be paid from the estate account once established, or paid out-of-pocket and submitted to the estate for reimbursement later.

💳 Do I have to pay my parents’ credit card debt when they die?

Generally, children are not personally responsible for their parents’ credit card debt out of their own pockets unless they co-signed the account. The debt belongs to the estate. If the estate has no assets, the debt typically goes unpaid.

🔍 How do I find out about credit cards if the deceased hid their mail?

If there is no paper trail, the most effective method is to pull the deceased person’s credit report. By notifying the three major credit bureaus of the death, you can usually request a final credit report, which will list all open accounts and outstanding balances. Be aware that the bureaus will require proof of your legal authority, such as your Letters Testamentary or court-issued executor documents, before they release the report to you.

📈 Does the deceased person’s credit score matter anymore?

No, a credit score ceases to have practical meaning after death. Creditors are only concerned with the outstanding balance and whether the estate has enough assets to settle the claim. You do not need to worry about protecting their score.

🤝 Should I try to negotiate a lower settlement on the credit card balance?

While creditors are sometimes willing to accept a lower lump-sum payment to close a file, you should not attempt this until you fully understand the estate’s total assets and liabilities. If the estate is solvent and has plenty of cash, negotiating might be unnecessary; if insolvent, it requires professional guidance.

💸 If I inherit a house, does the credit card company put a lien on it?

Credit card debt is unsecured, meaning it is not tied to the house. However, if the executor distributes the house to you before paying off valid credit card claims, the creditors could potentially take legal action against the estate to force a sale to cover the debt.

⚖️ What is a “creditor claim period” in estate administration?

This is a specific window of time (often mandated by local court rules, ranging from a few months to a year) during which creditors are legally permitted to submit formal demands for payment. Once this period closes, older, unsubmitted claims are often barred from collection.

⏳ How long does it typically take to completely resolve estate credit cards?

It rarely happens overnight. Because executors must wait out the formal creditor claim period and ensure all higher-priority taxes and administration costs are paid first, it is common for credit card claims to remain in a “holding pattern” for six months to a year before final payment is issued.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.