- Handling creditor calls and collection letters as executor is primarily a sorting and documentation task, not a negotiation.

- Never argue or admit liability on the phone; your only goal is to verify the caller’s identity and shift the interaction to mail.

- Keep a dedicated communication log to track every interaction, noting dates, names, and claimed reference numbers.

- Build a physical folder system to separate raw incoming mail from verified claims and duplicate bills.

- Shield non-executor family members by giving them a simple script to redirect aggressive collectors to your central estate address.

The Phone Starts Ringing Before You Are Ready

In my experience supporting estate administration, one of the most stressful phases for a new executor happens right after the individual passes away. Before you have even found the will, set up a filing system, or had a chance to breathe, the phone might start ringing. Collection letters begin appearing in the mail alongside condolence cards. This sudden influx of demands can make you feel like you are already behind schedule.

When you are appointed to handle an estate, debt collectors and creditors will naturally reach out. It is their job to find out who is in charge of the accounts. However, a common mistake I see is executors feeling pressured to have answers immediately. You might answer the phone in the car, get caught off guard by a firm-sounding collection agent, and make a verbal promise to “look into paying it next week.”

You do not need to have answers right away. Handling creditor calls and collection letters as executor is an organizational process. Your job is not to act as a debater, a negotiator, or an immediate problem solver. Your role, especially in the early weeks, is simply to act as an intake clerk. You are gathering the pieces of a puzzle so that later, you can look at the whole picture safely.

Key Point: When dealing with creditors after a death, your goal is to transition all communication from verbal pressure to auditable records.

The Document-First Approach and Escalation Scripts

The fastest way to lose control of estate communications is to engage in back-and-forth arguments with callers. A collector might tell you that a debt is urgently past due. They might sound impatient. It is incredibly tempting to explain why the accounts are frozen or to argue that the balance they are quoting seems wrong based on the statements you found.

I always encourage executors to resist the urge to explain. Explaining leads to conversational loops, and conversational loops often lead to misunderstandings. Instead, pivot the conversation to your administrative boundaries.

The Initial Boundary Script

If you answer the phone and realize it is a debt collector, use this neutral, repetitive response:

“Hello. I am handling the administration for this estate. We are currently in the initial review phase and cannot discuss accounts over the phone. Please submit your claim and all supporting documentation by mail to [Mailing Address]. We will review it once received.”

Handling Pushback: The Escalation Path

A common operational reality is that some collectors will refuse to move to mail. They might claim their system “requires a verbal confirmation” or that “mail takes too long.” If the caller pushes back, you need an escalation path that ends the conversation without conceding.

Attempt 2 (Firm): “I understand your timeline, but the estate requires formal documentation for any review. I cannot help you further on the phone.”

Attempt 3 (End Call): “I am noting in my file that you are refusing to send a mailed claim. I am ending this call now. Goodbye.”

You do not need their permission to hang up. By setting this boundary firmly, you train the legitimate creditors to use your system while filtering out aggressive or unstructured demands.

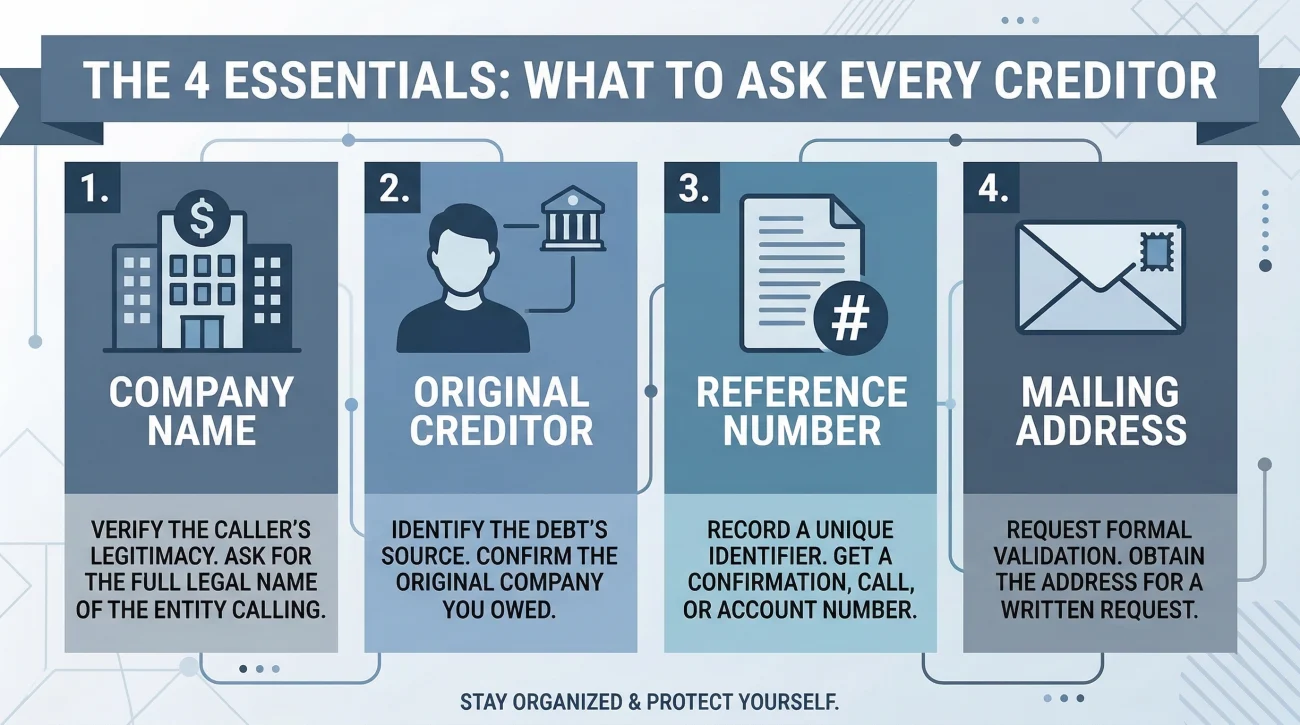

What to Confirm Before You Hang Up

While you should not discuss the merits of a debt over the phone, you do need to extract basic information from the caller before you end the conversation. This ensures you have a record of who is attempting to contact the estate.

In day-to-day admin work, I see files get disorganized when an executor writes down “someone called about a medical bill” on a sticky note. A month later, no one remembers which hospital or agency called. To prevent this, treat every call as a simple data-entry task.

Ask the caller for the following details so you can log them:

- ✅ The name of the company calling.

- ✅ The name of the original creditor (if they are a third-party collection agency).

- ✅ A reference number or account number.

- ✅ A mailing address where you can expect their claim to come from.

Once you have these four pieces of information, the call is over.

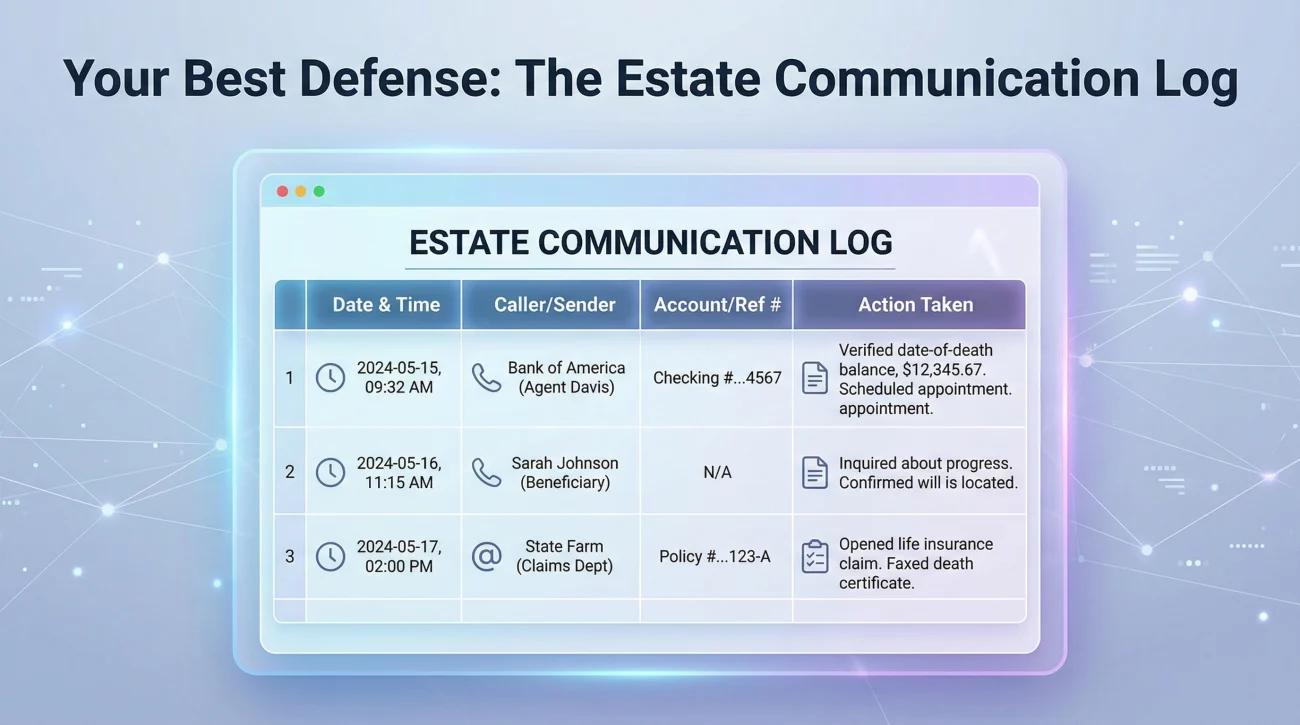

Creating Your Estate Communication Log

A central pillar of the document-first approach is keeping a dedicated log. Whether you prefer a cheap spiral notebook kept right by the phone or a digital spreadsheet, the tool matters less than the habit.

If a question arises later about whether a specific creditor was trying to reach the estate, your log is your best defense and your clearest organizational tool.

| Date & Time | Caller / Sender | Account / Ref # | Action Taken |

|---|---|---|---|

| Oct 12, 10:00 AM | ABC Collections (for City Hospital) | Ref: 9988-XY | Answered call. Requested mailed claim. |

| Oct 14, Mail | XYZ Credit Card | Acct ending 1234 | Received past due notice. Placed in ‘Pending Review’ folder. |

| Oct 15, 2:30 PM | Unknown number | None given | Caller refused to provide company name. Hung up. |

💡 Pro Tip: Keep your log purely factual. Write down what happened, not how you felt about it. A clean, objective log is a powerful tool if you ever need to show a professional how you have been managing incoming inquiries.

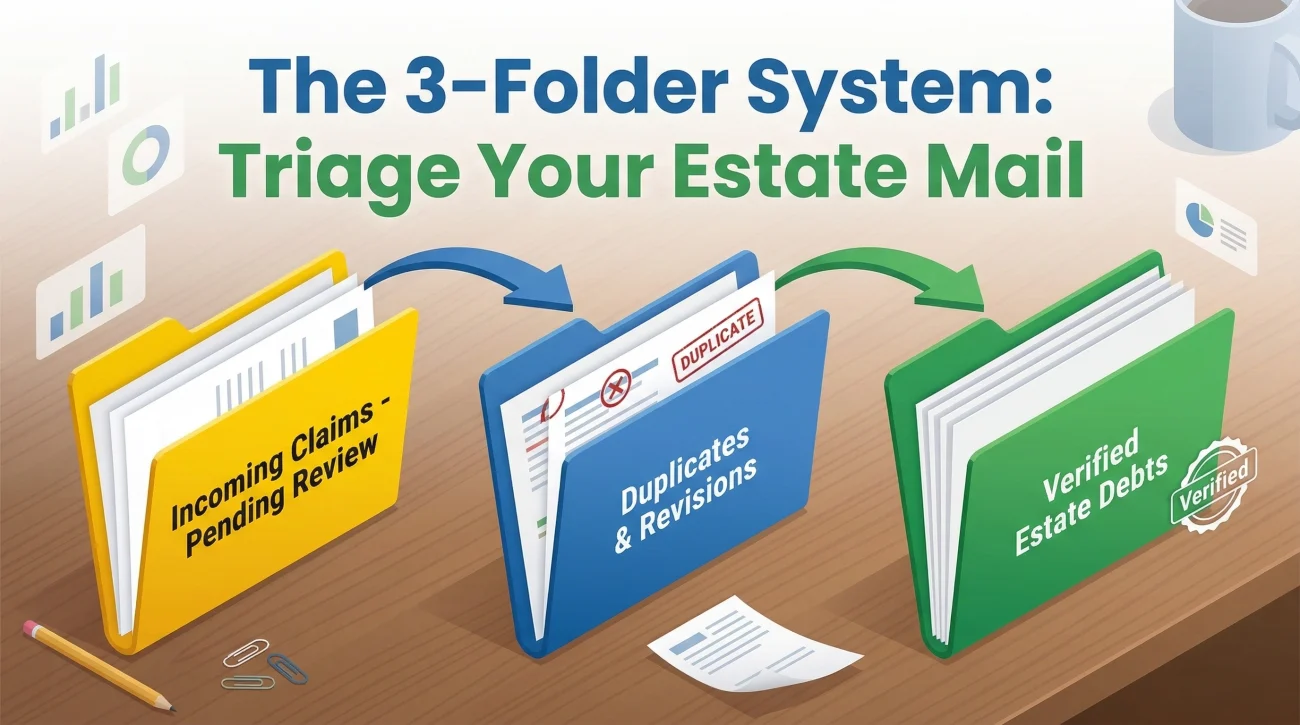

Handling the Mail: Folder Systems and Duplicate Bills

Phone calls are immediate and disruptive, but physical mail is often where the real administrative work happens. After a death, the mailbox will likely fill up with statements, final bills, and collection letters.

My strategy for this is triage. Do not try to solve a letter the moment you open it. First, staple the physical envelope to the back of the letter to preserve the postmark date and return address. Then, sort the mail into a structured physical folder system.

The Three-Folder System

Executors need a way to track the status of paper claims at a glance. I recommend setting up three distinct folders:

1. Incoming Claims (Pending Review): Every new bill or demand letter goes here first. You are not paying it. You are simply storing it until the estate has a complete financial picture.

2. Duplicates and Revisions: Medical billing is notoriously messy after a passing. You might receive three different invoices for the same hospital stay, or notices that cross paths with insurance adjustments. When a bill looks like something you already have, place it here to cross-reference later so you do not accidentally pay the same debt twice.

3. Verified Estate Debts: Once you sit down to review the “Pending” folder, cross-check the claims against the deceased’s records, and confirm the debt is real and accurate, it moves here. This is the stack you will eventually evaluate for payment.

By moving paper through these specific stages, you prevent the overwhelming feeling of having a loose stack of demands sitting on your kitchen counter.

Shielding Co-Executors and Family Members

If you are serving alongside a co-executor, or if the deceased person’s spouse or children are receiving mail and calls, handling incoming claims becomes more complex. Creditors will frequently call anyone associated with the deceased trying to locate the decision-maker.

Inconsistencies create confusion. If a collector calls you and is told to send a letter, but then calls your sister and she accidentally says “we are selling the house soon,” the collector will flag the file for aggressive follow-up. To avoid this, you must establish a strict “single point of contact” rule early on.

“I’m not really handling the bills, my brother is doing that. Try calling back next month.”

“My co-executor is the central point of contact. Please direct all inquiries to our estate address at [Address].”

It helps to send a quick email to your co-executor and close family members to formalize this process.

Subject: Estate Admin: How to handle bill collectors

Hi everyone,

As we start getting more mail and phone calls for the estate, I want to make sure we are all protected from harassment. I am keeping a central log for all incoming claims.

If anyone calls you asking for payment or account details, please do not confirm any information or discuss the estate. Just tell them: “Morgan is the point of contact. Please mail any formal claims to [Address].”

If you get any collection letters in your mail, please don’t throw them away or call the number. Just hand them to me so I can log them. This keeps our records clean.

Thanks,

Red Flags, Scams, and Impersonations

Unfortunately, the estate administration process is not immune to bad actors. In many cases, obituaries are public, and probate filings are public records. This means scammers often have enough basic information to attempt to extract money from an overwhelmed executor.

This is why demanding formal documentation is so protective. Legitimate creditors understand the estate process. They know it takes months. Scammers, on the other hand, rely on urgency, fear, and confusion.

As you log calls and sort mail, watch out for these common red flags:

- ❌ The “Urgent Today” tactic: A caller insists that if a specific fee is not paid immediately, legal action will be taken against you personally by the end of the day. Legitimate estate claims do not work on hourly deadlines.

- ❌ Refusal to provide written proof: If you ask a caller to mail their claim and they say, “We don’t do that,” or “I just need a credit card to clear this up now,” hang up and log the interaction.

- ❌ Vague details: A letter arrives demanding payment but contains no account number, no dates of service, and no breakdown of charges. Treat these highly suspiciously and never pay an unverified invoice.

⚠️ Warning: Never use your personal credit card or bank account to pay a creditor over the phone just to make them stop calling. Mixing your personal funds with estate claims can create severe complications and personal liability.

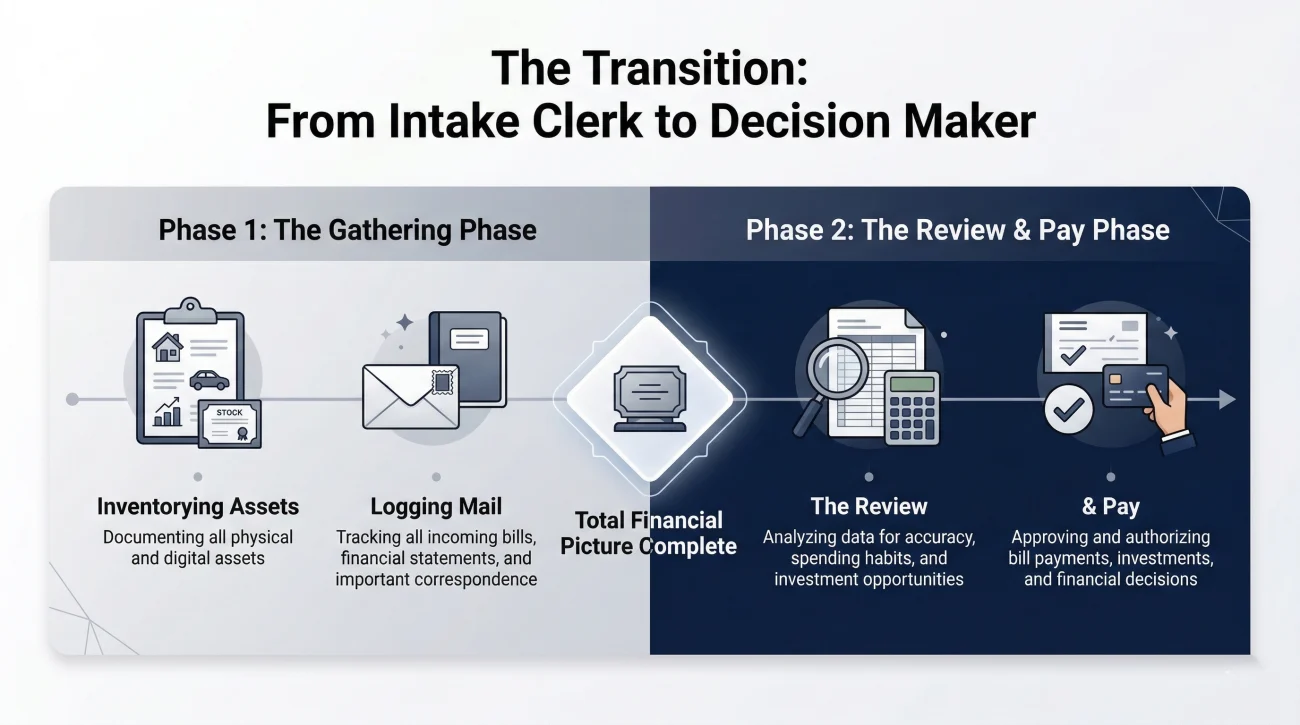

Timing: When Do You Stop Gathering and Start Reviewing?

A frequent question executors ask is, “How long do I just sit here gathering mail before I actually do something about it?”

It is normal to feel anxious watching the “Pending Review” folder grow thicker. However, estate administration is not about paying bills as they arrive. It is about assessing the total debt against the total assets. If you pay a credit card in month one, but discover a massive, unexpected tax bill in month four, you may have just created a severe problem.

Rather than guessing at a timeframe, anchor this transition to a milestone. The gathering phase lasts until you have secured the estate’s financial accounts and completely inventoried all assets. You transition into the “review and pay” phase only after you have a complete, accurate picture of both the property and the obligations. You must be certain the estate is solvent (has enough money to cover everything) before funds start moving outward. For a deeper look at the exact sequence of resolving these obligations safely, you should review our executor creditor and debt checklist.

Final

Acting as an executor places you directly in the crosshairs of companies whose entire business model relies on applying pressure. Recognizing that their urgency is not your emergency is the most important mental shift you can make.

By enforcing strict communication boundaries, utilizing a structured folder system, and refusing to engage in verbal debates, you neutralize the stress of collection efforts. Protect your time, protect your family members, and let the paperwork flow into your systems until you are genuinely ready to review the estate’s full financial reality.

❓ FAQ

🛑 Can a debt collector force me to sell the estate’s house immediately?

No. Unsecured creditors (like credit card companies) cannot force an immediate sale of real estate over the phone. Real estate transactions within an estate are formal processes dictated by court timelines and available liquid assets, not by collection agency demands.

⏱️ Is there a time limit for creditors to contact the estate?

Yes. The formal probate process typically involves a specific “creditor claim window” (often a number of months after official notices are published). If creditors fail to submit a formal written claim within that timeframe, their right to collect from the estate may expire.

📬 What if a collection letter has no return address?

Log the receipt of the letter, but take no action. Legitimate creditors and agencies will always provide a clear mailing address for disputes and payments. A lack of contact information is a strong indicator of a scam or an invalid claim.

💳 Do credit card interest and late fees keep adding up after death?

Often, yes. Interest and fees may continue to accrue on unpaid balances. However, once you notify the credit card company of the death, many will freeze the account to prevent new charges, and some may pause late fees while the estate is being settled.

🗣️ Should I tell a debt collector the estate is insolvent?

If you suspect there is not enough money to pay all bills, inform them neutrally that “the estate’s solvency is currently under review.” Do not make absolute statements about insolvency until a professional has verified the estate’s complete inventory and obligations.

🕵️ How do creditors find out someone died?

Creditors monitor public records, probate court filings, obituary publications, and the Social Security Administration’s Death Master File. It is highly likely they will find out on their own, which triggers the automated letters and calls.

🧾 What if I accidentally pay a scam collection agency?

If estate funds were used, document the exact transaction and contact the estate’s bank immediately to see if the payment can be stopped or reversed. You will also need to note this loss clearly in your estate accounting logs.

🏥 Are medical bills treated differently than credit cards?

In the final order of payments, medical bills related to the deceased’s final illness often have a higher priority status than general unsecured credit card debt. This is why sorting claims into categories before paying anything is critical.

📄 What exactly counts as “proof of debt” from a collector?

A legitimate claim should include the original creditor’s name, the account number, an itemized breakdown of the balance, dates of service or transaction, and proof that the debt belongs to the deceased individual.

🏦 Can creditors automatically take money from the deceased’s bank account?

If the deceased had auto-pay set up, the bank might continue processing payments until notified of the death. Once the bank is notified and the accounts are frozen or moved to an estate account, external creditors cannot pull funds without authorization.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.