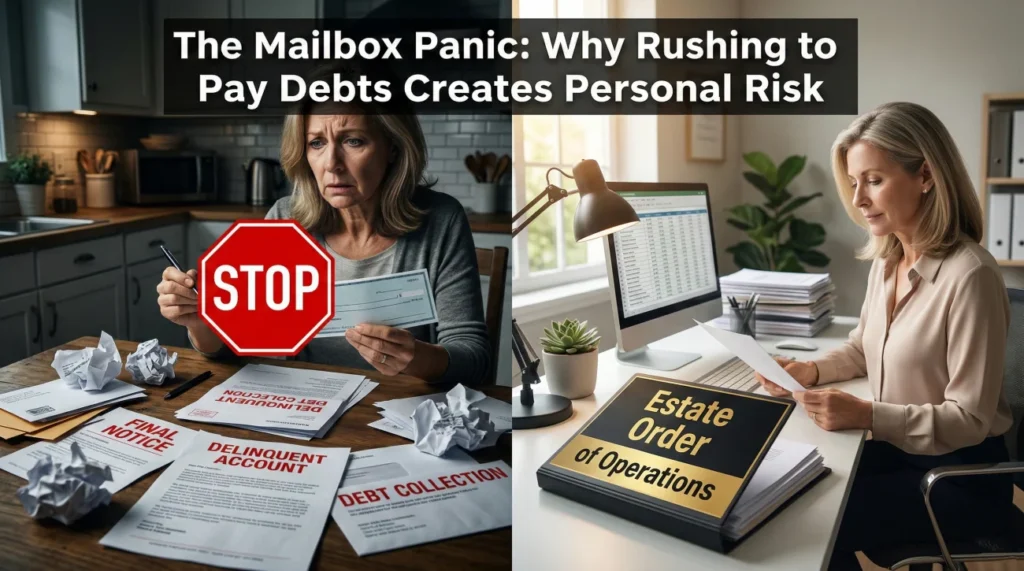

- The most common trap for a new executor is paying the loudest creditor first, which creates massive liability if the estate runs out of money later.

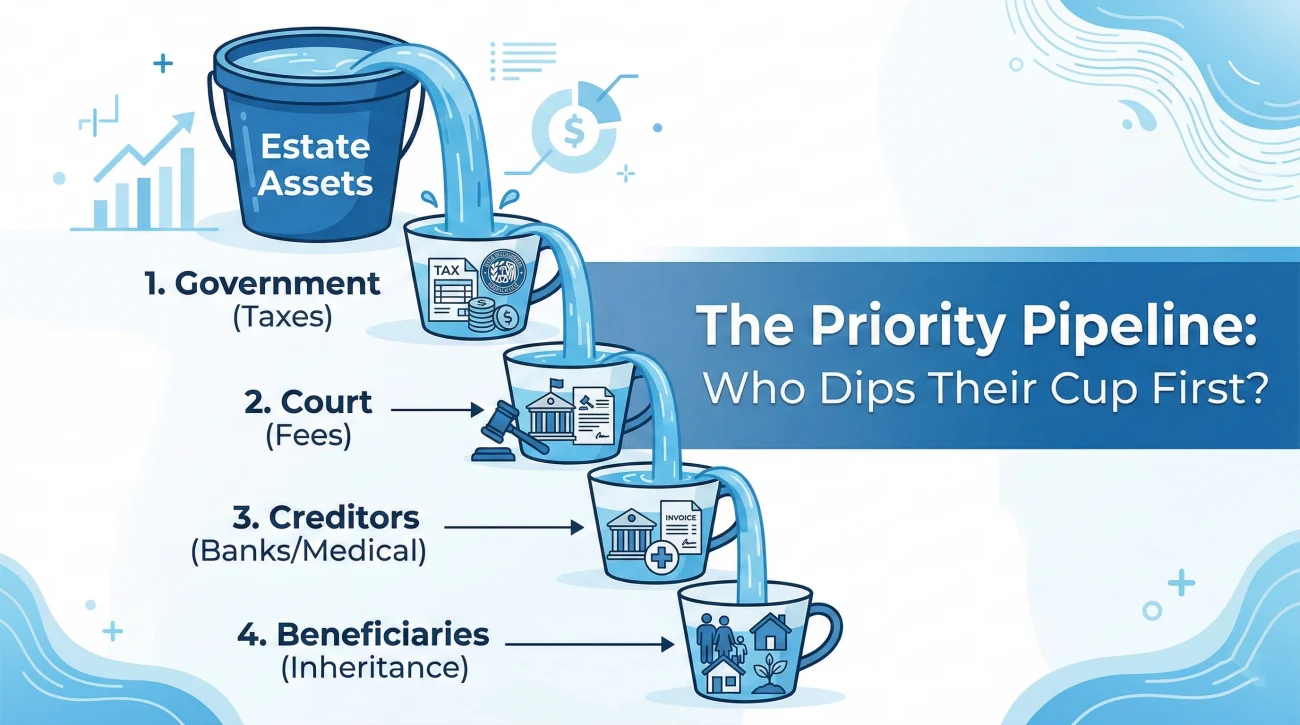

- Estate administration relies on a strict workflow order: keep the estate running, reserve for taxes, manage secured assets, and finally, evaluate unsecured claims.

- Distinguishing between “administration expenses” (costs generated after death) and “estate debts” (money owed before death) is your first operational hurdle.

- If debts exceed assets, the estate is insolvent. You must freeze all payments immediately, as local statutes will dictate how remaining pennies are divided.

- Use a simple “Pay/Hold Decision Log” to document why a debt is waiting, giving you a calm, process-driven answer for anxious beneficiaries or aggressive collectors.

The Mailbox Panic: Why Rushing to Write Checks Creates Personal Risk

In my day-to-day work helping executors organize estate files, the most panicked phone calls I receive usually happen around week three. The mail has piled up. There are five credit card statements, a threatening letter from a collection agency, a confusing property tax notice, and an auto loan statement. The natural human instinct is to grab the estate checkbook, sit down at the kitchen table, and start clearing the pile to make the stress go away. I always give them the exact same advice: put the pen down.

When you take on the role of managing an estate, you are stepping into a highly structured legal system. Figuring out the executor pay debts in what order workflow is not about deciding who you think deserves the money the most, or fulfilling a moral obligation to clear the deceased person’s name. It is about following a protective, sequential process.

I frequently see well-meaning people pay off a low-level credit card bill early because the collector was aggressive. Six months later, they realize they do not have enough money left to pay the final income taxes or the probate court fees. When the money runs dry, the IRS or the court will not accept “I was just trying to do the right thing” as an excuse. Paying things out of sequence can make you personally liable for the shortfall, meaning you have to pay those mandatory costs out of your own pocket.

This guide will not give you a state-specific statutory priority chart, because those laws vary wildly depending on where you live. Instead, I am going to walk you through the practical, safe order of operations I use to help families sort their paperwork. This framework ensures you know exactly what to process, what to pause, and how to build a defensible system.

The Logic Behind the Sequence: Fairness and Auditability

To process this mountain of paperwork without anxiety, it helps to understand why the legal system forces you to wait. The entire estate administration framework is built around two concepts: fairness among creditors and auditability for the beneficiaries.

Think of the estate’s bank account as a single bucket of water. When someone passes away, numerous parties line up with cups, waiting for their share. The government is in line for taxes. The court is in line for its fees. The credit card companies are in line. And way at the back, the beneficiaries are in line for their inheritance. The priority of claims exists to dictate exactly who gets to dip their cup into the bucket first.

Key Point: Your job is not to magically generate funds to pay everyone. Your primary responsibility is to gather the assets, identify the valid claims, and process them in the correct sequence using only the estate’s resources.

When I teach families how to organize their files, I tell them they are building an audit trail. If a medical provider questions why they only received 20 percent of their invoice, your ledger needs to clearly show that the funds were completely drained by higher-priority administrative costs and tax liabilities.

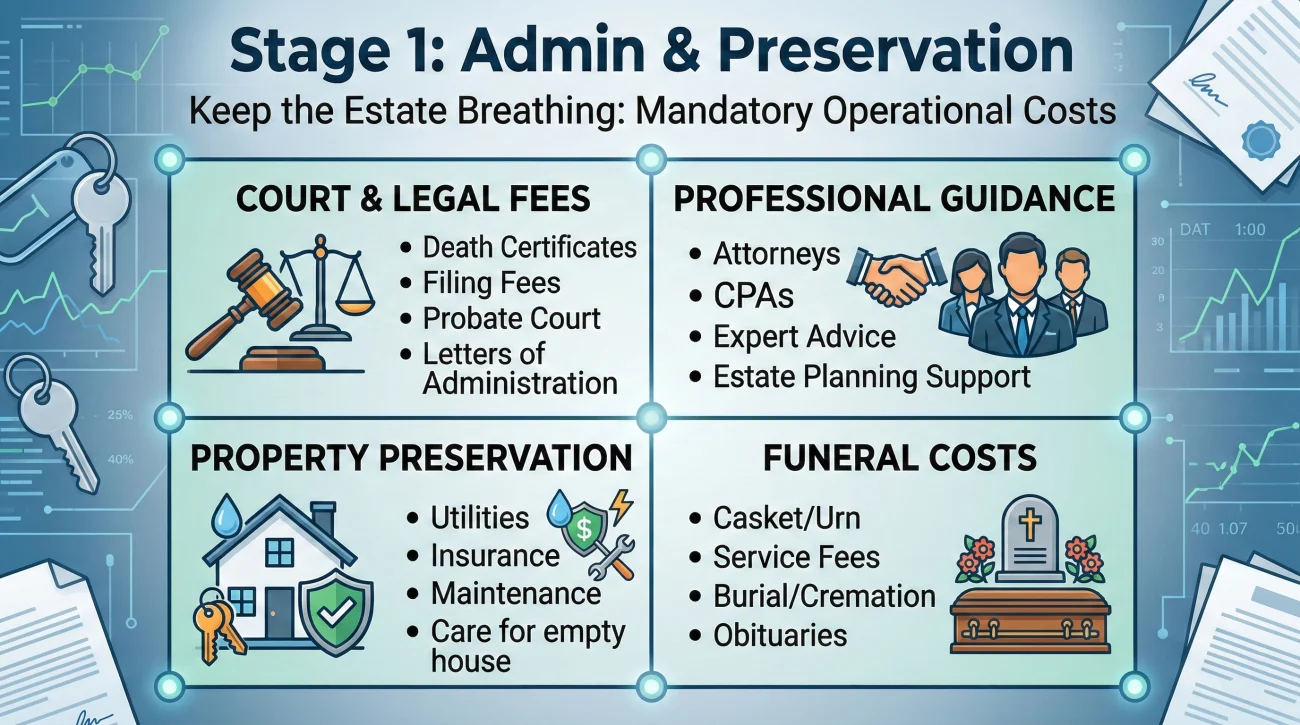

Stage 1: The “Keep the Estate Breathing” Costs

When mapping out an order of paying estate debts, the very first distinction you must make is the difference between an estate debt and an estate administration expense.

An estate debt is a financial obligation the person accumulated while they were alive, like an old medical bill. An estate administration expense is a cost generated after death to keep the estate secure, legal, and functional. Because the estate cannot be settled without these services, administration costs almost always sit at the very top of the priority list.

In my workflow, I have people create a brightly colored physical folder labeled “Stage 1: Admin & Preservation.” This separates vital operational costs from the general pile of past-due notices.

What Usually Goes Into the Stage 1 Folder

- 📄 Court and Legal Fees: Probate filing fees, costs for certified death certificates, and mandatory legal notice publication fees.

- ✅ Professional Guidance: Attorney retainers, CPA fees for tax preparation, and professional appraiser fees.

- 🏠 Property Preservation: Utility bills required to keep an empty house climate-controlled, homeowner’s insurance premiums, and basic lawn care to avoid municipal fines.

- ⚰️ Funeral Costs: In many jurisdictions, reasonable funeral and burial expenses hold a very high priority status, often grouped alongside direct administration costs.

A frequent error I notice is executors paying an electric bill for an empty house but failing to document the purpose. If you just write “electric bill” on the ledger, a beneficiary might argue it was a waste of estate money. You must label it clearly in your records: “Property Preservation: required to keep security system active pending house sale.”

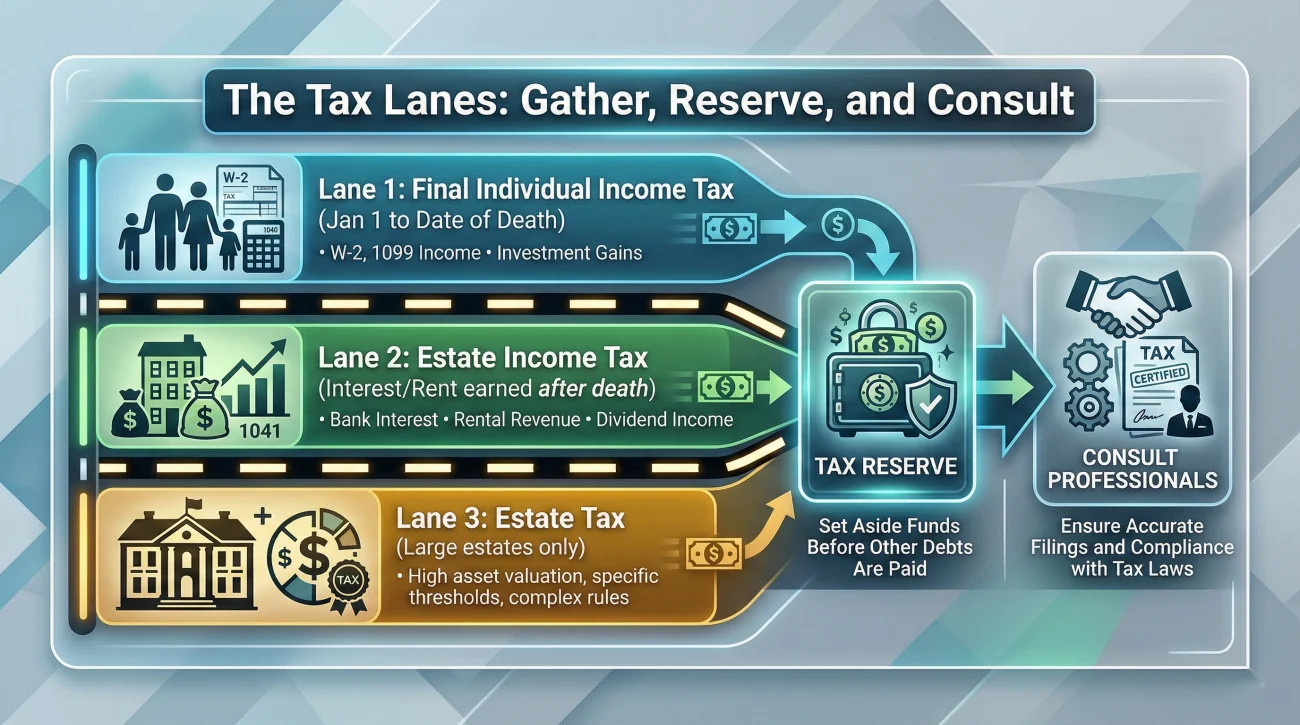

Stage 2: The Tax Lanes (The Silent Roadblock)

Once you have secured the property and paid the filing fees, the next major hurdle is the tax lane. You simply cannot safely distribute an estate if the government is still owed money. State and federal tax agencies are not creditors you want to leave underfunded.

Tax obligations can be stealthy. You might not get a bill in the mail immediately, which makes it easy to forget about them and spend the available cash balance on lower-tier debts. Instead of assuming the CPA will handle it later, you need to create a “Tax Reserve” column in your tracking ledger and actively hold those funds untouched until the returns are filed.

Taxes generally fall into three lanes, and you need to gather the paperwork for all of them. First is the final individual income tax return, covering January 1st to the date of death. Second is the estate income tax return. If the estate’s bank account generates interest, or a rental property continues to generate rent after the person dies, the estate itself may owe taxes. Third, for a very small percentage of large estates, there is an estate tax return.

Do not try to calculate these priorities yourself. Your operational task is strictly organizational: gather the prior year returns, collect the incoming 1099s, place them in your Stage 2 folder, and hand them to a qualified professional.

Stage 3: Secured Obligations (The Asset Dictates the Action)

The third phase of the workflow shifts focus to secured debts. A secured debt is an obligation directly tied to a specific piece of physical collateral, like a mortgage on a house or an auto loan on a car.

Secured debts require an entirely different mental approach. If you stop paying a basic unsecured credit card, the company sends a letter. If you stop paying a secured car loan, the lender has the legal right to eventually repossess the car, completely removing that asset from the estate’s inventory. Therefore, your decision-making here is routed entirely through what you plan to do with the collateral.

Let’s look at a practical scenario: The deceased left behind a vehicle with a $15,000 loan balance. As the executor, you have to investigate the context. If the car is “underwater” (worth only $10,000), surrendering the vehicle back to the lender might be the cleanest administrative choice. If the estate intends to sell the car to capture $5,000 in equity, you likely need to maintain the loan payments and the auto insurance to preserve that asset until the sale clears.

This is also where joint obligations complicate the workflow. If a family member co-signed that auto loan, the lender will look to that co-signer for payment immediately, regardless of the probate timeline. The estate does not automatically shield a co-signer from their contractual obligations, which often requires careful communication between the executor and the family member to decide who is making the monthly payment during administration.

To keep this organized, set up a specific “Secured Asset Log.” For every piece of collateral, document the lender name, the monthly payment amount, the estimated payoff balance, and where the physical asset is currently located. This helps you clearly see the monthly “burn rate” of holding onto the estate’s property.

Stage 4: Unsecured Claims, General Debts, and Subscriptions

Once you have secured the physical assets, reserved funds for taxes, and covered the operational costs of the estate, the landscape shifts. You move away from protecting property and transition entirely into managing paper trails. This brings us to the final, and often most stressful, category of creditor management.

At the bottom of the typical priority ladder sits unsecured debt. These are obligations not tied to any physical collateral. This bucket commonly includes standard credit cards, personal signature loans, older medical bills, and general consumer debt.

Because unsecured creditors are acutely aware that they are last in line to get paid, some collection agencies will apply tremendous pressure. They want you to pay early, before you realize the estate might run out of money. They will call constantly and sometimes imply that you are doing something legally wrong by making them wait.

My strict rule for this phase is: collect, log, and pause. Do not write a check for an unsecured debt just because the invoice looks urgent. You must wait until the formal creditor claim period has completely closed. To manage this safely, I advise executors to put a hard calendar alert on their phone for 30 days before the local creditor claim window ends, giving them time to review the entire stack of claims at once.

When an unsecured creditor calls you, keep your emotions out of it. You are an administrator gathering data, nothing more.

Phone Script: Replying to an unsecured collection call

“Hello. I am the executor managing this estate. We are currently in the administrative gathering phase and are not dispersing any funds for unsecured claims at this time. Please submit a complete, written statement of the claim to the estate’s official mailing address for our records. I cannot discuss this further on the phone. Thank you.”

If a creditor continues to push or refuses to accept a verbal explanation, you can formalize your stance by shifting entirely to written correspondence. Having a standard template ready will save you hours of anxiety.

Written Template: Requesting Formal Claim Documentation

Subject: Estate of [Name] – Account #[Number]

To Whom It May Concern:

I am the appointed executor for the Estate of [Name]. I am writing in response to your recent inquiry regarding the above-referenced account.

The estate is currently in the initial administrative phase. No distributions for unsecured claims are being processed at this time. To ensure your claim is properly logged for future review, please send a complete, itemized statement of the account, including proof of the original agreement, to the estate’s mailing address at [Address].

Please direct all future communication regarding this matter in writing to the address provided above.

Sincerely,

[Your Name], Executor

Finally, do not forget the invisible unsecured debts: digital subscriptions. Annual software licenses, streaming services, and gym memberships will quietly drain the estate account if left unchecked. Treat these like any other unsecured debt. If you cannot access the deceased’s portal to cancel them, you may need to instruct the estate’s bank to block the recurring charges, logging each cancellation in your file.

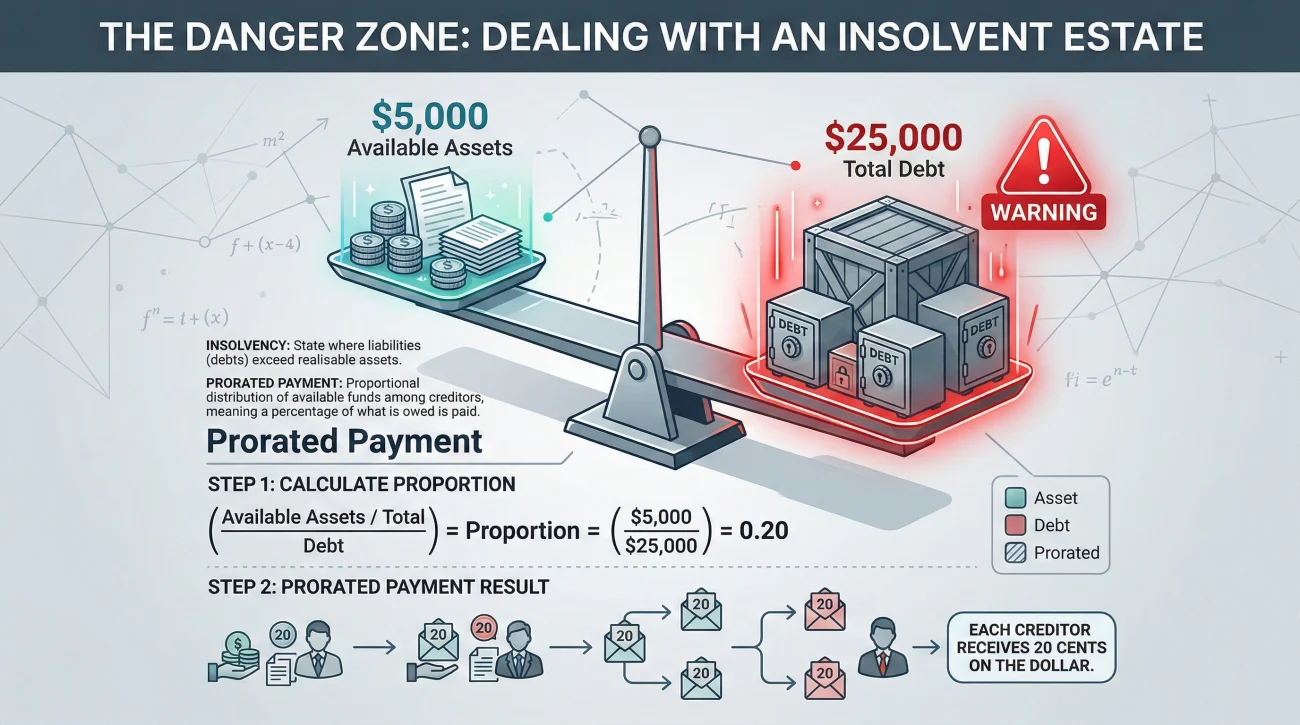

The Danger Zone: Insolvent Estate Signals

What happens if you map out all four of these stages and realize the math does not work? If the total amount of money the estate owes is greater than the total liquid assets available, the estate is considered “insolvent.”

Insolvency completely changes the rules. You can no longer just pay bills in full as they arrive. Strict state laws dictate exactly how remaining funds are prorated among creditors in the same class.

Let’s look at the math. Imagine the estate has exactly $5,000 left after paying administration costs and taxes, but there is $25,000 in credit card debt spread across four different cards. You do not get to pick your favorite card and pay it off completely. Usually, those creditors must be paid on a prorated basis. In this example, each creditor might only receive 20 cents for every dollar they are owed. If you accidentally pay one card $5,000 and leave the other three with zero, the unpaid creditors can petition the court to hold you personally responsible for the mistake.

If your ledger shows that debts are piling up faster than assets, pause all payments, lock the estate checking account, and consult with a local probate attorney immediately to get formal, written instructions on how to handle the prorated disbursements.

Building the Pay/Hold Decision Log

Throughout this entire process, your greatest shield against beneficiary complaints and creditor disputes is a clean, hyper-organized paper trail.

I advise building a simple “Pay/Hold Decision Log” using a basic spreadsheet or a dedicated notebook. The goal is to track the status of every single piece of paper that demands money.

| Creditor / Payee | Type of Debt | Date Received | Amount | Decision / Status Notes |

|---|---|---|---|---|

| County Probate Court | Stage 1: Admin Cost | Nov 02 | $350.00 | PAID (Check #102) – Required to open estate |

| CPA Firm Services | Stage 2: Taxes | Nov 10 | Pending | HOLD – Awaiting final tax return prep |

| First National Bank (Visa) | Stage 4: Unsecured | Nov 14 | $5,100.00 | HOLD – Logged in Stage 4, sent letter req. written proof |

| City Water Dept | Stage 1: Preservation | Nov 18 | $65.00 | PAID (Check #103) – Keep pipes active for showing house |

This level of strict documentation removes all emotion from the job. When a frustrated beneficiary asks why the credit card balances are accumulating interest and have not been paid, you do not have to argue. You simply show them the log and explain: “We are holding Stage 4 unsecured debts until the Stage 2 tax liabilities are finalized by the accountant.” It is a calm, process-driven answer that shuts down arguments immediately.

Final Thoughts: Keeping Your Records Closed and Clean

The debt phase of estate administration is not about clearing your desk quickly; it is about building a closed, defensible file. The pressure to act will come at you from all sides, but rushing is the enemy of a safe administration. By mentally sorting every single bill into its proper stage—administration costs, taxes, secured debt, and unsecured claims—you protect the estate’s remaining assets.

Even after the checks are written and the estate is formally closed, your job is not entirely erased. Standard practice dictates that executors should retain the estate’s financial records, including the Pay/Hold log, canceled checks, and written creditor communications, for several years (often 3 to 7 years depending on tax rules) just in case a dormant issue resurfaces.

For a complete view of how all these debts, taxes, and record-keeping requirements map out across the entire administration timeline, review our core executor creditor and debt checklist. It serves as the master map for keeping your estate files perfectly aligned.

❓ FAQ

🗂️ How long do I need to keep these debt records after the estate closes?

It is generally recommended to keep estate financial records, including creditor correspondence and tax filings, for 3 to 7 years after the estate is formally closed, depending on your local tax agency’s audit windows.

💻 What should I do about digital subscriptions if I cannot access the deceased’s computer?

If you cannot log in to cancel services directly, you can instruct the bank managing the estate account to block recurring charges from those specific merchants, or formally close the deceased’s original debit/credit cards.

🤝 Does a co-signer have to wait for the estate to pay the debt?

No. A co-signer is equally and immediately responsible for the debt based on their original contract with the lender. The lender will likely pursue the co-signer for monthly payments without waiting for the probate process to conclude.

💳 What is the difference between an authorized user and a joint account holder on a credit card?

A joint account holder co-owns the debt and is personally responsible for the balance after the co-owner dies. An authorized user only had permission to use the card and is typically not responsible for paying the balance.

📉 Can an executor negotiate a lower payoff amount with a collection agency?

Yes. During the Stage 4 unsecured claims phase, especially if estate funds are tight, executors sometimes negotiate a lump-sum settlement for less than the total owed. Always get the settlement agreement in writing before paying.

⏳ What happens if a creditor sends a bill months after the formal claim period closes?

If the executor properly published the notice to creditors and followed local rules, claims submitted after the deadline are typically barred (rejected) by the court, meaning the estate no longer legally owes them.

🗣️ What if a collection agency refuses to accept my “hold” status and becomes aggressive?

You have the right to send a formal “cease and desist” communication requesting that they stop calling and direct all future communication in writing to the estate’s mailing address. Document every interaction.

🏥 Are old medical bills treated the same as “final illness” hospital bills?

Often, no. In many jurisdictions, expenses directly related to the “last illness” (the days/weeks immediately prior to death) are given a higher priority status, while medical bills from years ago drop to the bottom as general unsecured claims.

🏠 Do I have to keep paying the mortgage if the house is “underwater” and cannot be sold for a profit?

If the property lacks equity and holding it drains estate resources, executors sometimes choose to pause payments and coordinate a “deed in lieu of foreclosure” or short sale with the lender, rather than throwing good money after bad.

📝 Should I use the deceased’s online portal credentials to pay their bills?

It is highly discouraged. Using someone else’s login can violate terms of service and obscures the audit trail. Open a formal estate account and pay via official estate checks or the estate’s own bank portal to keep records perfectly clean.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.