- The debt follows the asset: Secured debts are tied to a specific physical item, meaning the lender typically retains rights to that property if payments stop.

- Ownership dictates action: Before worrying about payments, verify if there is a surviving co-signer, if the property is in a trust, or if mortgage protection insurance exists to clear the balance automatically.

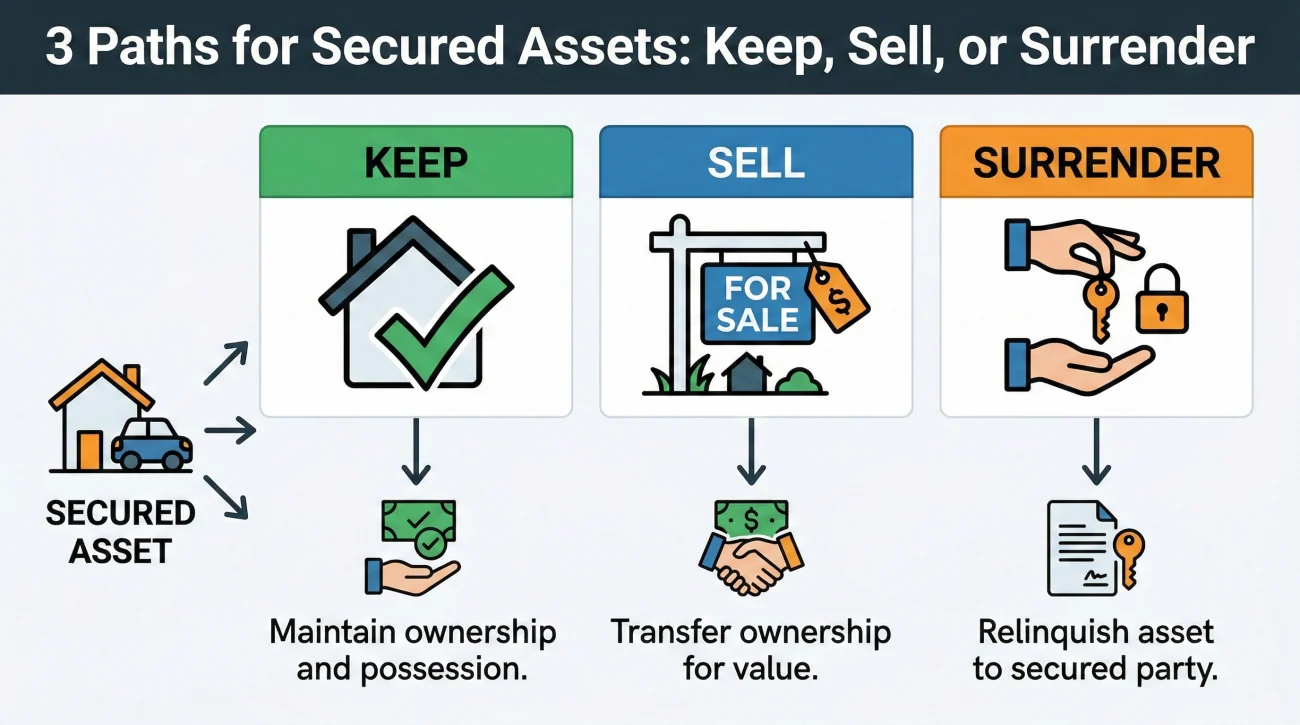

- Three main operational paths: Executors typically deal with secured property by either arranging to keep it, preparing to sell it, or letting it go (surrendering it).

- Documentation is your shield: Never guess a payoff amount. Always request formal, written payoff statements and track every interaction with lenders in a dedicated log.

- Timing matters differently: Pausing payments on mortgages or car loans can trigger rapid consequences like foreclosure or repossession, requiring careful triage compared to regular unsecured bills.

Navigating Debts Tied to Physical Assets

In my experience supporting estate administration workflows, the moment an executor opens a statement showing a massive mortgage balance or a hefty car loan, a specific kind of panic sets in. The numbers are often the largest they will see during the entire process. It is completely normal to feel a sudden weight of responsibility, wondering if you are personally on the hook or if the bank is going to show up tomorrow to take the house.

When dealing with secured debts after death, the most important thing I tell executors is to separate the panic from the paperwork. The rules of engagement change entirely when a debt is attached to a physical piece of property. You are no longer just dealing with numbers on a ledger; you are dealing with a house, a vehicle, or a piece of equipment that holds both financial and emotional value.

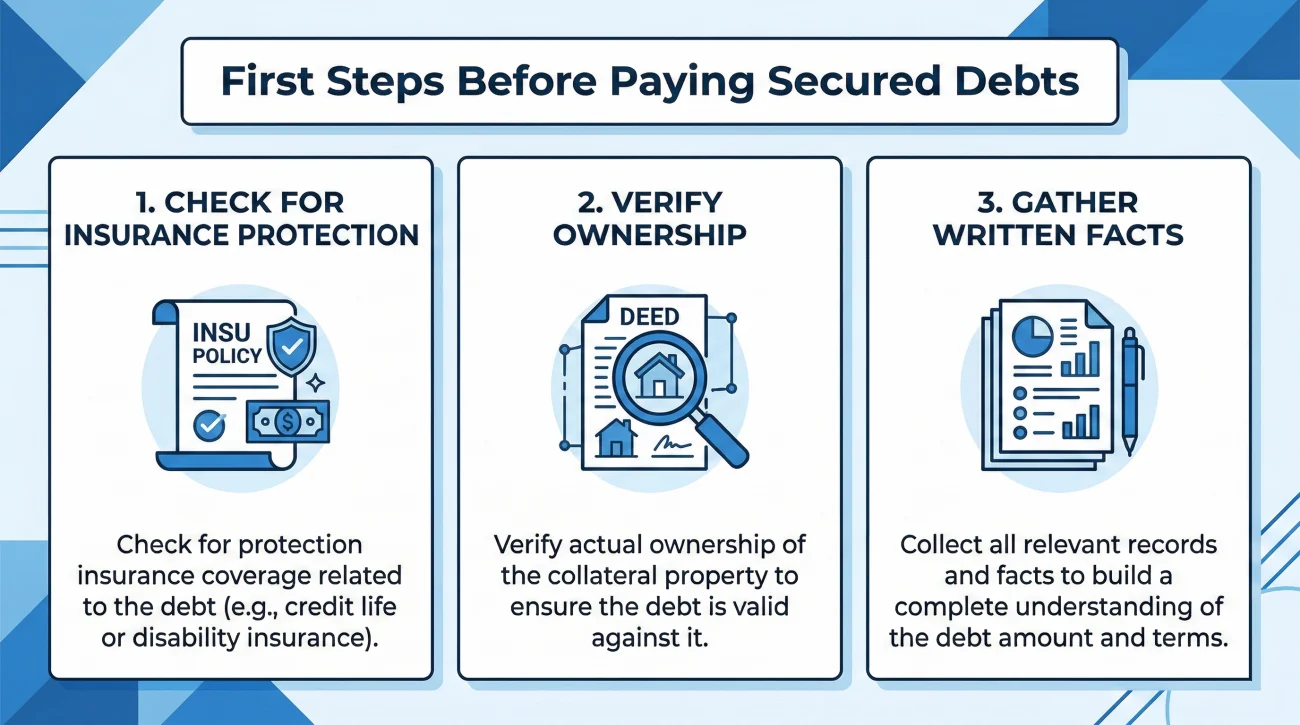

Before that panic turns into action, the first thing to check is whether the debt might already be covered. Look through the deceased person’s paperwork for a mortgage protection insurance policy or a life insurance policy tied specifically to the loan. Many people purchase these policies so that if they pass away, the insurance automatically pays off the remaining balance. If this exists, your workflow changes from managing a debt to filing an insurance claim.

Key Point: Do not rush to pay a secured debt from your personal funds just to make the lender go away. Your first job is to secure the asset, gather the exact written facts, and understand the estate’s overall financial health before moving money.

What Makes a Debt “Secured” (In Plain English)

Before you can make any decisions, it helps to properly categorize the mail you are receiving. In the administrative work I do, I often see families treat all bills as equal. A credit card bill and a car loan statement arrive in the same mailbox, so they go into the same pile. But operationally, they belong in completely different categories.

A secured debt is a loan backed by collateral. The lender essentially says they will lend the money, but if payments stop according to the agreement, they have the legal right to take the specific item to recover their losses. The most common examples you will encounter are mortgages tied to real estate and auto loans tied to a vehicle. You might also see loans tied to boats, RVs, or expensive heavy equipment, which are collectively treated as lien debt in the estate.

An unsecured debt, like a standard credit card or a medical bill, has no collateral attached. If the estate cannot pay an unsecured debt, the creditor has to go through a formal claims process to try to get paid out of the estate’s general funds. They cannot simply drive up and tow away the living room furniture.

Understanding this distinction changes how you prioritize your time. An unsecured debt can often wait while you sort through paperwork. A secured debt requires you to actively decide how to manage the physical asset to prevent immediate loss.

Who Else is Involved? Checking Ownership and Co-Signers

Before mapping out a plan for the house or the car, you must confirm exactly who actually owns it and who signed the loan. The answers to these questions can sometimes remove the burden from your shoulders entirely.

Joint Ownership: Look at the deed to the house. If the deceased owned the property jointly with a spouse or someone else “with right of survivorship,” the property usually passes directly to that surviving owner outside of the probate process. The surviving owner is typically the one who must figure out how to handle the mortgage moving forward, not the executor of the estate.

Co-Signers on the Loan: If a son co-signed his father’s car loan, that son is still 100 percent responsible for the payments after the father passes away. The lender will look directly to the living co-signer to keep the account current. As the executor, you need to communicate with that co-signer to ensure they understand their obligation so the asset doesn’t get repossessed.

Assets in a Trust: If the house or car is titled in the name of a Revocable Living Trust, the rules change. Assets in a trust bypass the probate court. The designated Successor Trustee is the person responsible for handling the property and the debt attached to it, not the executor (though sometimes this is the same person wearing two different hats).

Once you confirm that the asset and the debt actually belong squarely in the estate’s lap, you can begin planning the next operational steps.

The Three Common Operational Paths

When you are looking at a mortgage after death executor scenario, or trying to manage an estate-owned car loan, there are typically three conceptual paths. Your job early on is not necessarily to finalize the choice, but to gather enough information so that you, the beneficiaries, and your legal advisors can make an informed decision.

Path 1: Keeping the Asset

Sometimes, a family member wants to keep the house or the car. This means the underlying debt has to be managed. In many cases, federal regulations provide certain protections that allow relatives who inherit a property to take over the mortgage without triggering a “due on sale” clause. If the plan is to keep the asset, your administrative focus shifts to ensuring payments do not lapse in the gap between the death and the formal transfer of the title. I often see executors coordinate with the intended beneficiary to ensure the monthly payments are made, while logging every single transaction clearly to show it was not an improper gift from the estate.

Path 2: Selling the Asset

Often, the estate simply needs the cash, or no one wants the property. In this scenario, the asset will be sold, and the secured debt will be paid off using the proceeds of the sale. If the house sells for $300,000 and the mortgage is $100,000, the lender gets their portion directly at the closing table, and the estate keeps the remaining equity. Your primary job here is maintenance. You have to keep the asset safe, insured, and structurally sound until it sells.

Path 3: Surrendering the Asset

There are times when an estate is “underwater,” meaning more is owed on the loan than the asset is worth. In these cases, it often makes no sense to keep paying. The administrative decision may be to simply let the lender take the asset back.

If you suspect this is the case, you need to understand the concept of a deficiency balance. If you surrender a car worth $15,000 but the loan is $25,000, the lender sells the car and applies the $15,000 to the account. That remaining $10,000 does not usually disappear. It typically becomes an unsecured claim against the estate. You must track this potential remaining debt before you decide to simply hand over the keys.

💡 Pro Tip: Even if you plan to surrender a vehicle, do not just leave it parked on the street. Keep it secure, remove all personal belongings, and document its condition with photographs on the day of death. This prevents lenders from claiming the estate caused damage prior to repossession.

Now that you know which direction the estate might take, the immediate next step is gathering the exact numbers needed to execute that plan.

What Information Usually Matters: Building the File

One of the most common points of friction I see is an executor trying to make decisions based on outdated information. A statement from six months ago is useless. Interest accrues daily. Late fees may have been applied. Escrow balances fluctuate.

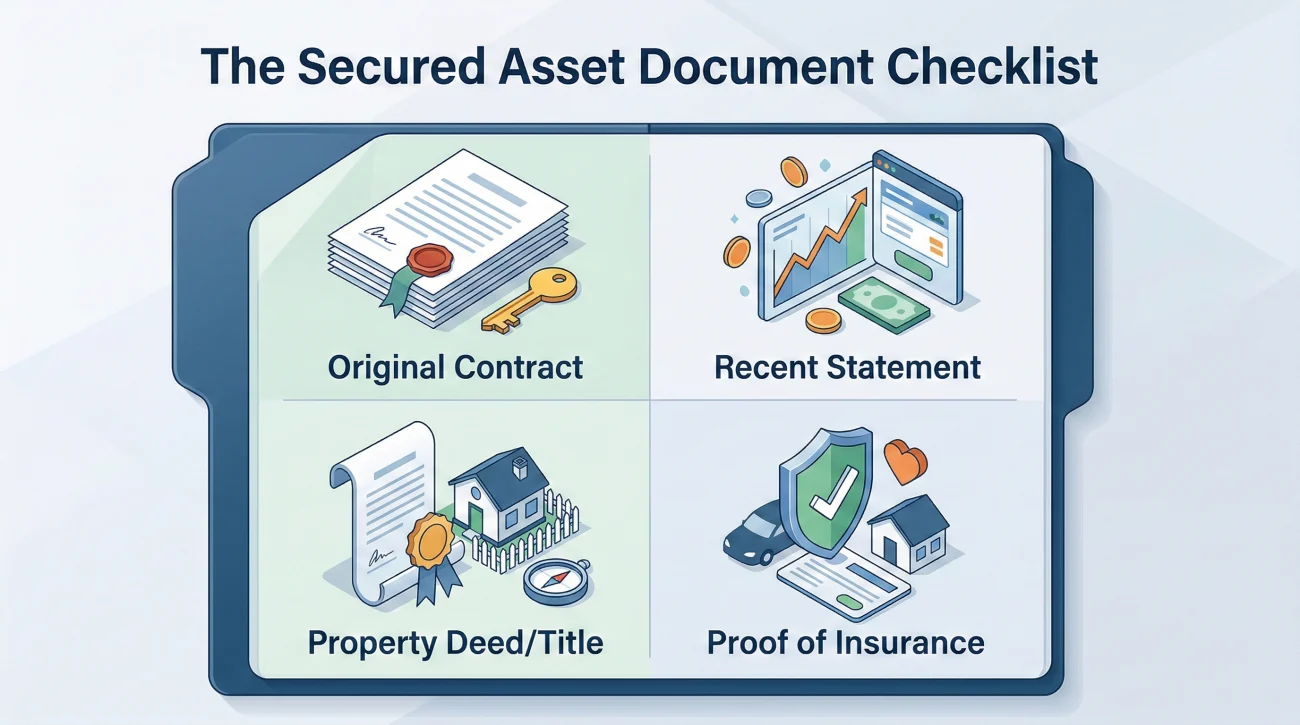

To get a true picture, you need to build a dedicated physical or digital folder for every single secured asset. Here is exactly what you should be systematically hunting for and filing away.

- 📄 The Original Contract or Promissory Note: You need to know exactly what was agreed to. What are the default terms and any prepayment penalties?

- ✅ The Most Recent Monthly Statement: This gives you the account number, the servicer’s contact info, and the current apparent balance.

- 📄 The Title or Deed: You must confirm how the property is actually owned to ensure you have the authority to act.

- ✅ Proof of Insurance: If there is a loan, there is almost always a requirement for insurance. You need the declarations page to prove the asset is protected.

Requesting the Formal Payoff Statement

Once you have your court documents establishing your authority, you need to request a formal payoff statement. Do not accept a verbal estimate over the phone. You want a document on the lender’s letterhead stating the exact amount required to satisfy the loan as of a specific date.

Here is a neutral, professional script you can use to start this process in writing. Sending requests like this via certified mail with a return receipt gives you absolute proof of when they received it.

Subject: Request for Payoff Information and Account Status – Estate of [Deceased Name]

To Whom It May Concern at [Lender Name],

I am the appointed Executor for the Estate of [Deceased Name], who passed away on [Date]. Please see the attached death certificate and my court appointment documents establishing my authority to act on behalf of the estate.

Regarding account number [Account Number] secured by [Property Address or Vehicle VIN]:

Please provide a formal, written payoff statement valid through [Date, usually 15-30 days out]. Additionally, please provide a clear history of the account for the last 90 days, including any escrow balances, suspense accounts, or outstanding fees.

Please send all future correspondence regarding this account directly to my address listed below. Do not attempt to process any automated drafts from the deceased’s previously associated bank accounts.

Thank you for your prompt assistance.

Sincerely,

[Your Name]

Executor, Estate of [Deceased Name]

[Your Mailing Address]

Special Cases: Reverse Mortgages and HOA Liens

As you gather this paperwork, be on the lookout for two specific situations that require immediate attention because they operate on entirely different timelines than standard loans.

Reverse Mortgages: If you discover a reverse mortgage, the clock is already ticking. Unlike a traditional loan, a reverse mortgage becomes due and payable when the borrower passes away. You do not have years to figure this out. Usually, the estate has six months to either sell the property, pay off the balance to keep it, or hand the deed over to the lender. Communication with the reverse mortgage servicer must happen immediately to request extensions if you are actively trying to sell.

HOA Dues and Liens: If the house is in a Homeowners Association, treat the HOA dues with the exact same urgency as the mortgage. HOA fees do not pause at death. If the estate stops paying the monthly dues, the HOA can often place an aggressive lien on the property. When it comes time to sell the house, that HOA lien will completely halt the transaction until it is paid, often with heavy late fees and attorney costs attached.

How Secured Debts Interact with the Broader Workflow

It is very easy to get tunnel vision when dealing with a massive property loan. You spend hours on hold with the bank and fret over the insurance policy. But in estate administration, no asset or debt exists in a vacuum. Everything is connected to the estate’s overall cash flow.

To avoid trouble, you need to calculate the “burn rate” of keeping the asset. Create a simple log that lists the monthly mortgage payment, the HOA fee, the insurance premium, and the average utility cost to keep the lights on. Add those up. If it costs $2,500 a month just to keep the house standing, and the estate only has $10,000 in liquid bank accounts, you mathematically only have four months to sell the house before the estate runs out of money.

This is where maintaining a wide-angle view is critical. As you map out these secured obligations, you must see how they fit into the broader executor creditor and debt checklist. Without a master map comparing your monthly carrying costs against your available cash, you risk draining the estate account on the wrong priorities.

Common Mistakes When Handling Secured Property

In my daily work, I see patterns. The executors who struggle the most are usually the ones who apply the wrong operational rules to the right problems. The mistakes are rarely malicious; they are just misunderstandings of how lenders operate after a death.

Mistake 1: Relying on the Deceased’s Autopay

Many executors assume that if a car loan is on autopay from the deceased’s checking account, they can just leave it alone while they figure things out. This is highly risky. Once the bank learns of the death, they typically freeze the accounts. The autopay will fail, the car loan will go into default, and late fees will cascade. You must proactively intervene, pause unauthorized automatic drafts, and set up a clean, documented payment method from the official estate account if you intend to keep paying.

Mistake 2: Forgetting to Update the Insurance

What many people do not realize is that standard homeowner’s or auto policies often change their coverage parameters once the owner dies or if a house becomes vacant. If the house burns down and the insurance company denies the claim because they weren’t notified of the vacancy, the estate still owes the mortgage, but the asset is gone. Always contact the insurance broker immediately to confirm coverage requirements for an estate-owned or vacant property.

Mistake 3: Treating It Like a Credit Card

Executors often read that they shouldn’t pay any bills until the formal creditor claim period ends. Applying that unsecured-debt logic to a mortgage is dangerous. Secured lenders operate on strict default timelines to protect their collateral. If you pause a mortgage payment for 90 days waiting for a court to give you permission to pay bills, you might trigger a foreclosure process that is very difficult and costly to reverse.

| Debt Category | Executor’s Immediate Action Rule |

|---|---|

| Unsecured (e.g., Credit Card) | Log the claim and wait for formal probate instructions. |

| Secured (e.g., Mortgage, Car) | Secure the asset, verify insurance, and triage payments immediately. |

Communication Hygiene with Lenders

When you call a mortgage servicer or an auto finance company, you are usually routed to a specialized “deceased accounts” or “estate management” department. These representatives are trained to protect the lender’s interests, not yours. Your job is to communicate clearly, neutrally, and always in writing whenever possible.

Every time you call a secured lender, you need to execute a simple tracking formula:

[Date/Time] + [Rep Name/ID] + [What was asked] + [What they stated] + [Follow-up action required]

If you tell the mortgage company over the phone that the estate intends to sell the house, and the representative says, “Okay, we will put a 90-day hold on foreclosure actions while you list it,” you cannot just hang up and trust that it is done. You must request that confirmation in writing. If they won’t send it, you send a letter confirming your understanding of the call.

Sample Call Log Entry:

Date: October 12, 2:15 PM

Lender: Apex Auto Finance

Rep: Sarah, ID #4492

Discussion: Informed them of the death. Sarah stated the account is currently 15 days past due. She noted that repossession processes automatically trigger at 60 days past due.

Action: I requested a payoff statement be mailed to the estate address. Sarah confirmed it will be mailed within 5 business days. Set calendar reminder for Oct 19 to check mail.

⚠️ Warning: Never promise a lender that “I will pay you out of my own pocket” just to buy time. Keep your language strictly focused on the estate: “The estate is currently evaluating assets,” or “I am gathering payoff information on behalf of the estate.” Maintain that boundary fiercely.

Wrapping Up the Secured Debt Strategy

Handling secured debts after death requires a shift from passive observation to active management. You cannot simply file the statements away and hope for the best. By immediately identifying what property is tied to what debt, building a comprehensive file with accurate payoff numbers, and maintaining strict communication hygiene with lenders, you protect the estate’s most valuable assets.

Stay calm, document every interaction in writing, and focus on gathering the exact facts needed to make clear, defensible decisions about the property.

❓ FAQ

🏠 What happens to a mortgage when someone dies?

The mortgage debt remains attached to the property. The estate, or the person inheriting the home, must typically continue payments, pay off the loan by selling the house, or assume the mortgage under specific federal protections.

🚗 Do I have to pay my dad’s car loan after he dies?

Unless you co-signed the loan, you are not personally responsible for paying it from your own funds. However, if the estate wants to keep the car, the estate must pay the loan. If payments stop, the lender will usually repossess the vehicle.

⏳ What makes a reverse mortgage different after death?

A reverse mortgage becomes due and payable almost immediately upon the borrower’s death. The estate typically has up to six months to sell the home, repay the balance, or deed the property to the lender, making swift communication essential.

✍️ What if someone co-signed the deceased person’s loan?

The surviving co-signer remains legally responsible for the entire debt. If the estate does not or cannot make payments, the lender will expect the living co-signer to keep the account current to avoid default.

🏦 Can the bank take the house if the executor doesn’t pay?

Yes. Because a mortgage is a secured debt, if monthly payments cease and no arrangement is made with the lender, the bank has the legal right to begin foreclosure proceedings to recover their collateral.

📉 What is a deficiency balance if we surrender an asset?

If you surrender a car or house and the lender sells it for less than what is owed, the leftover amount is the deficiency balance. This remaining debt typically becomes an unsecured claim against the estate that must still be addressed.

📄 How do I find out the exact payoff amount for a car?

You must contact the lender’s estate department, provide a death certificate and your official executor court appointment documents, and request a formal, written payoff statement valid for a specific date range.

⚠️ Will the lender repossess the car if we miss one payment?

While one missed payment might not trigger immediate repossession, late fees will apply, and lenders can act quickly on deceased accounts if they feel the collateral is at risk. Always communicate proactively.

🏷️ Can we sell a house that has a mortgage on it during probate?

Yes, this is very common. The executor generally coordinates the sale of the property, and the outstanding mortgage balance is paid off directly from the proceeds at the closing table before the remaining funds enter the estate.

💡 Should I use my own money to pay the deceased person’s mortgage?

It is generally advised to pay estate expenses only from estate funds to keep accounting clean. If you must use personal funds to prevent immediate foreclosure, document the transaction clearly as an administration expense to seek reimbursement later, though reimbursement requires proper legal procedures.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.