- Closing the account is not just about emptying the funds; it is about officially severing the estate’s financial existence and securing the final paper trail.

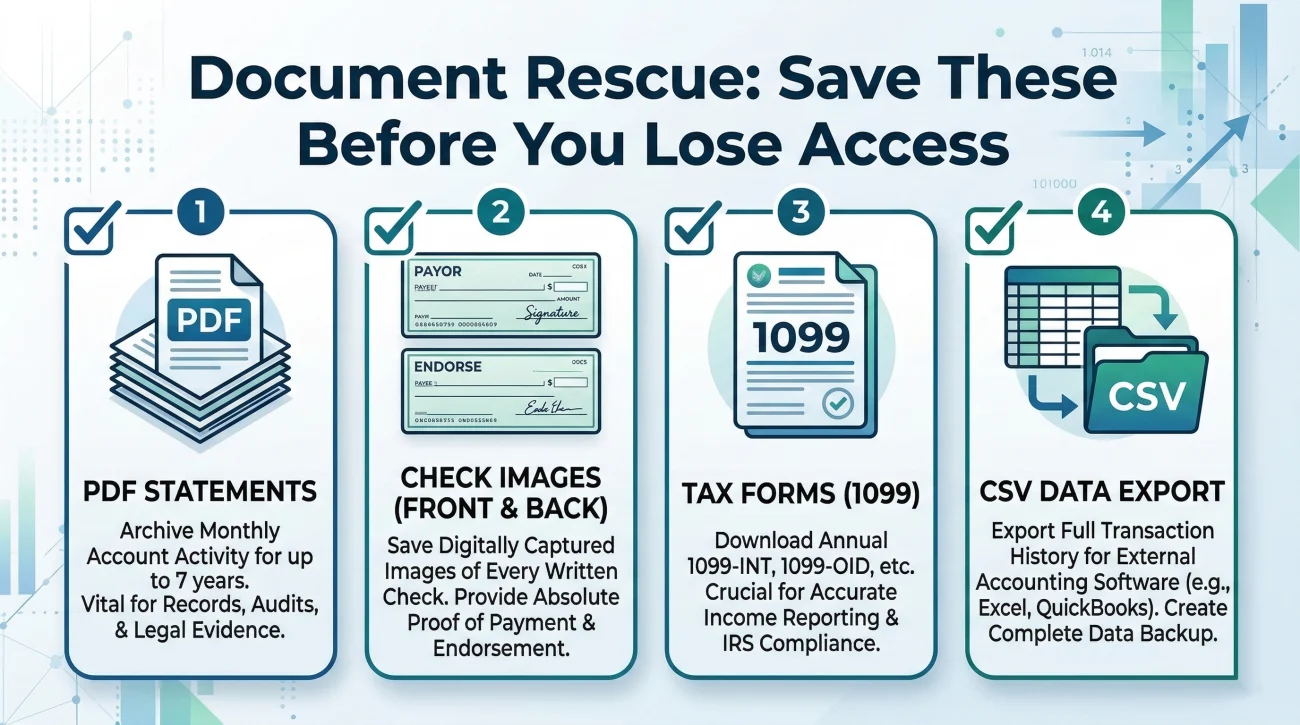

- Online access is often revoked the moment an account is closed. You must download all historical statements, check images, and tax documents before you make the final request.

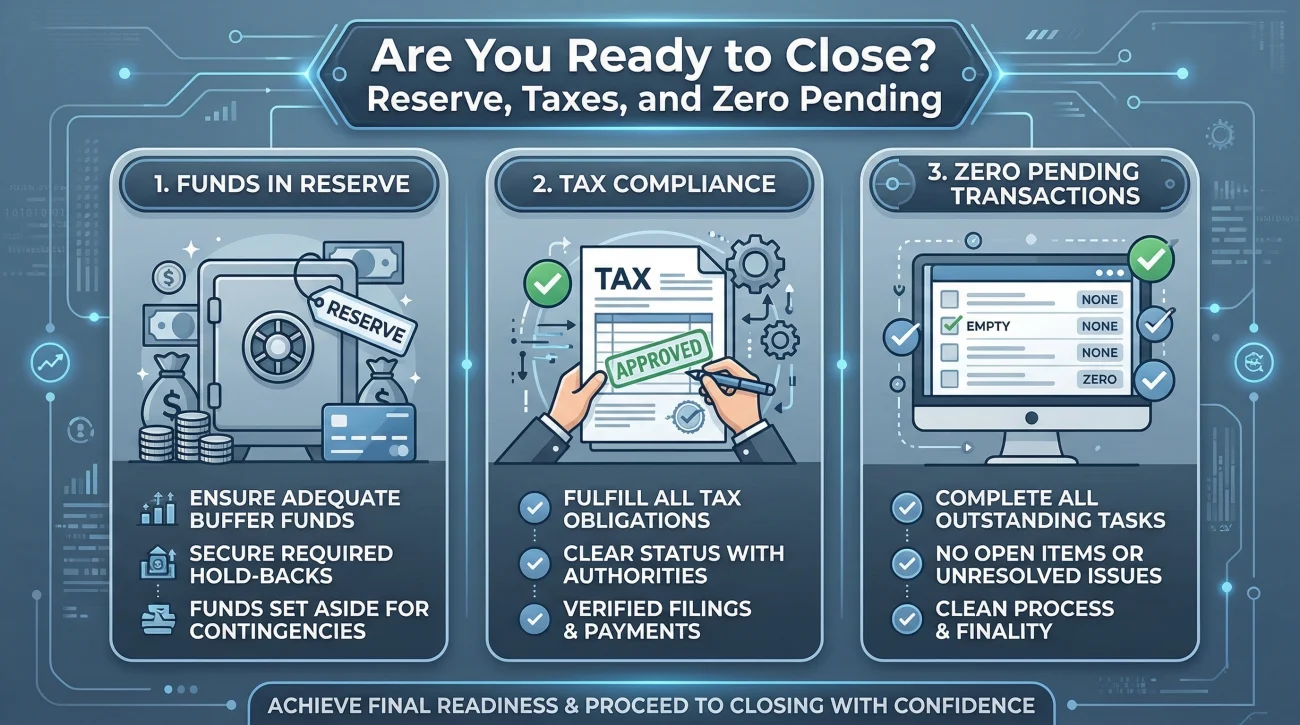

- Your final accounting math must perfectly match the final bank statement. Resolve pending interest and final fees at the branch on the exact day you close it.

- Never close the account if you have an uncashed beneficiary check floating around. You must either get them to cash it or follow unclaimed property procedures first.

The Story the Bank Account Tells at the Finish Line

I often tell executors that the bank account is the ultimate truth-teller. Beneficiaries might argue over the value of a dining room table, but bank statements deal in hard numbers.

In my experience supporting estate administration workflows, closing the estate bank account is often the moment when the reality of the finish line finally sets in for an executor. For months, or sometimes years, this single account has been the central nervous system of the estate. Every final paycheck, every sold asset, every paid utility bill, and every distribution check has flowed through it.

Now, you are looking at a balance that is either zero or very close to it. But deciding to close estate bank account operations is not as simple as walking up to a teller and asking them to shut it down. The closure of this account is the final punctuation mark on your documentation. If you close it too early, you might bounce a final distribution check. If you close it too late, monthly maintenance fees can eat into the remaining funds, throwing off your final accounting math.

Shutting down this account requires a very specific sequence of document preservation and communication. You are not just closing an account; you are archiving the estate’s financial history so that it can never be questioned later.

Timing the Closure and Holding a Reserve

One of the most common questions I hear is about timing. Executors often feel intense pressure to wrap things up and shut down the account as fast as possible. However, the timing is dictated by external factors and risk management, not just your desire to be done with the paperwork.

Before you even think about pulling the plug, you must ensure that every single final debit has cleared the transaction log. But beyond cleared checks, you also need to consider the “holdback” phase. In practice, seasoned executors rarely distribute every single penny in the first wave. They hold a reserve fund in the account to cover surprise late bills, final tax preparation fees, or unexpected administrative costs.

Once this reserve is established, the account must remain open and active. You cannot hold back funds for safety and then immediately shut down the account. You have to wait out the risk period.

Key Point: You are typically ready to close the account only when your reserve fund period has ended, all final tax returns are accepted, and the “pending transactions” column has been completely empty for several days.

Only when you are absolutely certain that no more money needs to go out, and no more refunds will come in, should you initiate the final closure.

The Document Rescue Mission: What to Save Before the Bank Cuts Access

Here is a field note from the operational side of things: banking systems are incredibly unforgiving when it comes to closed accounts. Often, the very second a bank employee clicks “close account” on their computer, your online login credentials are deactivated.

I have seen executors walk out of a bank branch, return home, and attempt to log in to print the last few months of statements for their closing packet, only to find they are locked out. Retrieving past statements from a closed account usually requires calling a customer service line, proving your identity all over again, and paying a fee per page for mailed paper copies.

Before you contact the bank to initiate the closure, you need to perform a complete digital download of the account’s history. I recommend creating a dedicated folder on your computer named “Final Bank Archives” and pulling down the following items.

- 📄 Every monthly bank statement in PDF format, from the day the account was opened to the current day.

- ✅ Front and back digital images of every cleared check, especially the distribution checks sent to beneficiaries.

- 📄 Any tax documents generated by the bank, such as 1099-INT forms for interest earned.

- ✅ A CSV or Excel export of the complete transaction history, which makes searching for specific payments much easier later.

⚠️ Warning: Do not assume the bank will automatically mail you a final statement. Many modern accounts default to paperless delivery. If you lose digital access, you lose your records. Download everything first.

Matching the Bank Zero to the Accounting Zero

The core of your job at the end of the process is proving that you did exactly what you said you were going to do. If your accounting says you distributed the remaining funds and the estate balance is zero, the final estate bank statement must also show a balance of exactly zero.

This is where many executors stumble. They prepare their accounting, get everyone to sign off, and then realize the bank account generated fourteen cents of interest on the last day of the month. Or, they realize the bank charged a fifteen-dollar monthly maintenance fee that was not accounted for. Now the bank balance does not match the accounting balance.

How do you fix this discrepancy? You have a practical operational path. For a comprehensive look at how all these final moving parts fit together, you should review the Estate Distribution Checklist. But from a purely banking perspective, you must handle the final pennies on the exact day you close the account.

Guessing the final interest amount a week in advance, writing distribution checks, and hoping the account hits exactly zero without any surprise fees.

Visiting the branch on your closing day. Asking the teller to calculate the exact final payout including pending interest up to that minute, waiving any final fees, and taking that exact final balance as a cashier’s check to distribute.

Navigating the Uncashed Check Problem and Unclaimed Property

Even with perfect planning, the final days of closing estate checking account operations can get messy. The most common operational bottleneck I see is the uncashed beneficiary check. You cannot close the account while a check is floating around, because it will bounce when they finally try to deposit it.

When this happens, your role is to document your efforts to get the transaction completed. Silence is your enemy here. If two weeks have passed and the check has not cleared, you need to initiate polite, documented follow-up. Do not use an accusatory tone; frame it as an administrative requirement.

Subject: Action needed: Status of estate distribution check

Hello [Name],

I am preparing the final paperwork to permanently close the estate bank account. Our records show that the distribution check #[Number] mailed to you on [Date] has not yet cleared the account.

Could you please let me know if you received the check safely? If you have it, please deposit it by [Date] so that the transaction clears and I can proceed with shutting down the estate account. If you did not receive it, let me know immediately so I can place a stop payment and issue a replacement.

Thank you for helping me wrap up these final administrative steps.

[Your Name]

If a beneficiary ignores the check for months despite your written warnings, you cannot keep the estate open indefinitely. Eventually, you will need to look into your state’s escheatment or unclaimed property procedures. This involves formally remitting the uncashed funds to the state’s unclaimed property division in that beneficiary’s name. You can then log the state’s receipt as your proof of distribution, which allows you to finally clear the balance and close the account safely.

The Difference Between Empty and Closed

There is a fundamental difference between an account with a zero balance and a legally closed account. Many first-time executors assume that if they transfer all the money out, the bank will automatically shut it down. This is a dangerous assumption that can lead to unexpected overdraft fees if automated charges hit an empty account.

You must explicitly instruct the bank to close the account. You cannot just drain it and walk away.

| Account Status | Bank Action | Executor Risk Level |

|---|---|---|

| Empty (Balance $0.00) | Account remains active. Fees may continue to accrue. | High. Risk of overdrafts and unexpected debt. |

| Closed (Officially requested) | Account is locked. No transactions or fees can post. | Zero. The financial trail is permanently capped. |

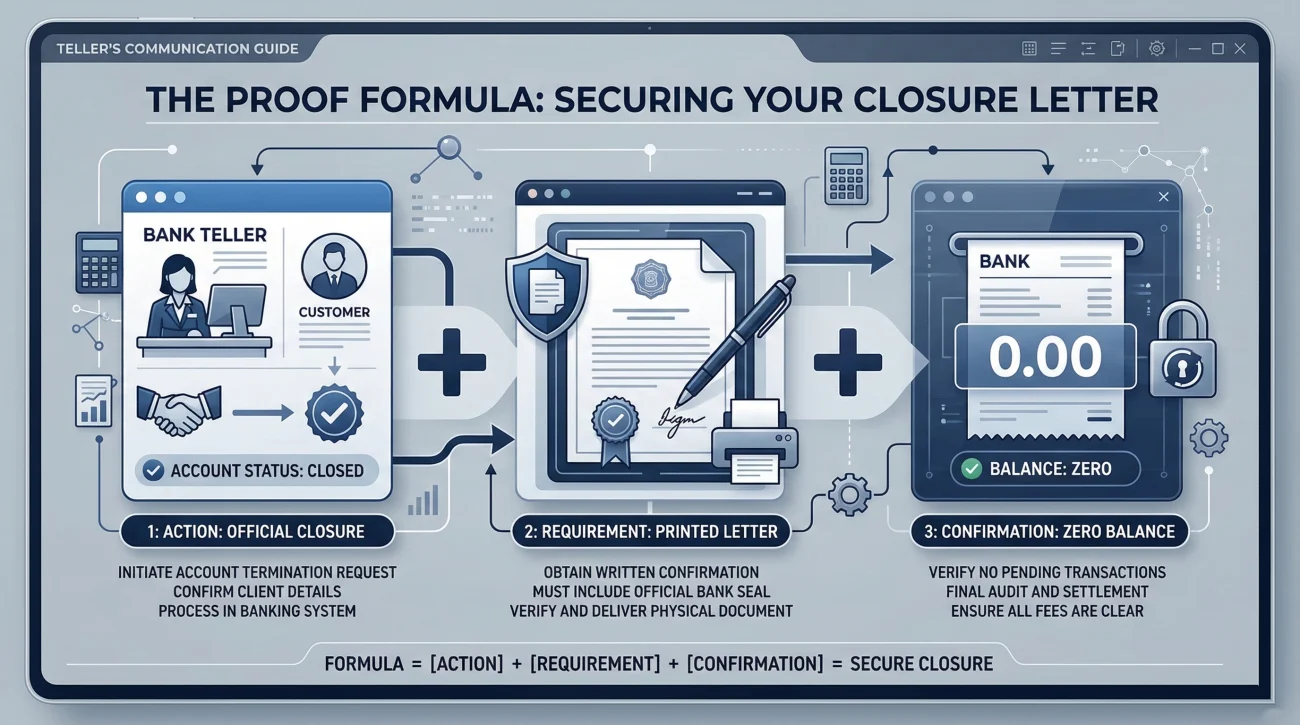

Requesting Written Proof of Closure

Because documentation is your only shield as an executor, you need proof that the account is actually dead. When you speak to the bank representative, you must request a closure confirmation document. Do not just accept a verbal confirmation.

You need a piece of paper or an official bank email that states the account number, the date of closure, and confirms that the ending balance was exactly zero.

If you are closing the account in person at a branch, you can use a formula like this when speaking to the banker.

[Action: I need to officially close this estate account today] + [What you need in writing: Please provide a printed letter showing the account is closed with a zero balance] + [Confirmation request: Can I get a copy of that before I leave the branch?]

Do not leave the bank or end the conversation until you have this physical or digital document in your possession. This confirmation letter is a vital piece of your paper trail and will go directly into your final records packet.

The Final Release of Liability

After the account is successfully closed and you have your confirmation letter in hand, your work shifts from active management to historical archiving. Closing this account is not just an administrative chore; it is the operational end of your financial liability.

Once you have a zero-balance letter, nobody can accrue new debt in the estate’s name, and no surprise automated drafts can pull funds. By combining this closure letter with your downloaded archives and cleared check images, you create an undeniable shield.

You have proved the money was gathered, distributed exactly as planned, and the financial vessel was safely dismantled. This packet becomes your final defense if a beneficiary or a late creditor ever asks questions years down the line.

❓ FAQ

🏦 How do I know it is safe to finally close the estate account?

It is generally safe when all known debts are resolved, your final accounting is prepared, your reserve period has ended, and every single check you have written has fully cleared the bank.

🛡️ Should I keep a reserve fund in the account before closing it?

Yes. Most experienced executors leave a documented reserve fund in the account even after main distributions to cover unexpected late bills, final tax preparation, or accounting fees.

📄 Will I still get bank statements after the account is closed?

Usually, no. Banks often immediately revoke online access upon closure. You must download all historical statements and check images before you ask the bank to shut down the account.

💸 Do banks charge a fee to close an estate account?

In most cases, banks do not charge a specific fee just to close the account. However, you must ask if any prorated monthly maintenance fees will be assessed on the day you choose to close it.

🛑 How do I handle a final tax refund check if the account is already closed?

If a refund check arrives made out to the estate after closure, you often have to temporarily reopen the account or work with the bank’s estate department. It is best to wait until all tax returns are fully processed before closing.

📞 Can I close an estate account over the phone?

This depends entirely on the bank’s internal policies. Some allow phone closure if the balance is exactly zero, while others require the executor to visit a local branch in person with their ID.

🧾 What if a late bill arrives after I close the estate bank account?

If you properly advertised for creditors, waited out the legal claim period, and held a reasonable reserve, late bills are typically barred. If a legitimate surprise bill arrives, you would rely on the reserve fund you held back.

📁 How long should I keep the final estate bank statement?

Executors typically keep all final financial records, including the final bank statement and closure confirmation, for several years alongside the final accounting and receipts of distribution.

⚖️ Do I need the court’s permission to close the bank account?

In many independent administrations, you do not need a specific court order just to close the bank account itself, but the closure usually happens in tandem with submitting your final reports to the court.

📝 What proof do I need to show beneficiaries the account is closed?

You should request a written “zero balance closure confirmation” letter from the bank. This document serves as undeniable proof that the account is permanently shut down.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.