- Minors usually cannot legally receive or manage inheritance directly, forcing the executor to use alternative, documented delivery methods.

- Informal handoffs to parents without a formal legal structure create massive personal liability for the executor.

- While waiting for custodial accounts or trusts to open, executors must use precise ledger entries to calculate, segregate, and protect the minor’s exact share.

The Stop Sign at the Finish Line

In my experience supporting estate administration, the final distribution phase is where executors expect to feel a massive sense of relief. You have paid the final debts, cleared out the house, and finally calculated everyone’s exact share. But then, you hit a sudden stop sign: one of the beneficiaries is a minor.

I often see executors assume they can simply write a check with the minor’s name on it, hand it to the child’s parents, and close the estate file. Unfortunately, reality is much stricter. Because a minor child does not have the legal capacity to manage significant financial assets, the standard distribution process completely changes.

When I help executors organize their final distribution packets, finding a minor on the beneficiary list means we have to pause and pivot. Our focus shifts from sending the money to setting up a documented holding pattern. If you try to bypass these controls, you expose yourself to serious liability down the road when that child becomes an adult and asks where their inheritance went.

This guide will walk you through why direct payments are restricted, the common pathways used to deliver the funds legally, and exactly what you need to document while you wait for those pathways to be established. Before diving into these specific workarounds, it helps to review the broader estate distribution checklist to ensure all other debts and administrative steps are fully cleared. Once you are certain the estate is actually ready to distribute, the first step in handling a minor’s share is understanding exactly why a standard payout is off the table.

Why Direct Payment is Usually Restricted

The primary reason you cannot simply hand cash or property to a minor relies on a concept known as the “age of majority.” In the eyes of the law, a person under a certain age (typically 18 or 21, depending on local regulations) cannot enter into binding legal contracts. This directly impacts your job and your safety as an executor.

The Threat of Personal Liability

One of your most critical duties before distributing any estate asset is to get a valid signature proving the beneficiary received their share. Because a minor cannot legally sign a binding document, any receipt they provide is essentially worthless. If you distribute funds on that basis, you are operating entirely without protection.

The Risk of Informal Handoffs

A very common mistake I see involves informal handoffs. An executor might think they know the family well enough to just give the teenager’s share to their mother to hold. This is a dangerous operational gap. If you give estate funds to someone without the proper legal framework authorizing them to receive it on the minor’s behalf, you have failed to distribute the asset properly.

If those funds are mismanaged by the parent, the child could eventually sue the estate, and you personally, for failing to secure their inheritance. This is exactly why financial institutions and probate courts place strict guardrails around these transactions.

⚠️ Warning: Even if the minor’s parent signs a basic, informal receipt on their behalf, it often does not protect the executor unless that parent has been officially appointed by a court as a legal guardian of the minor’s property.

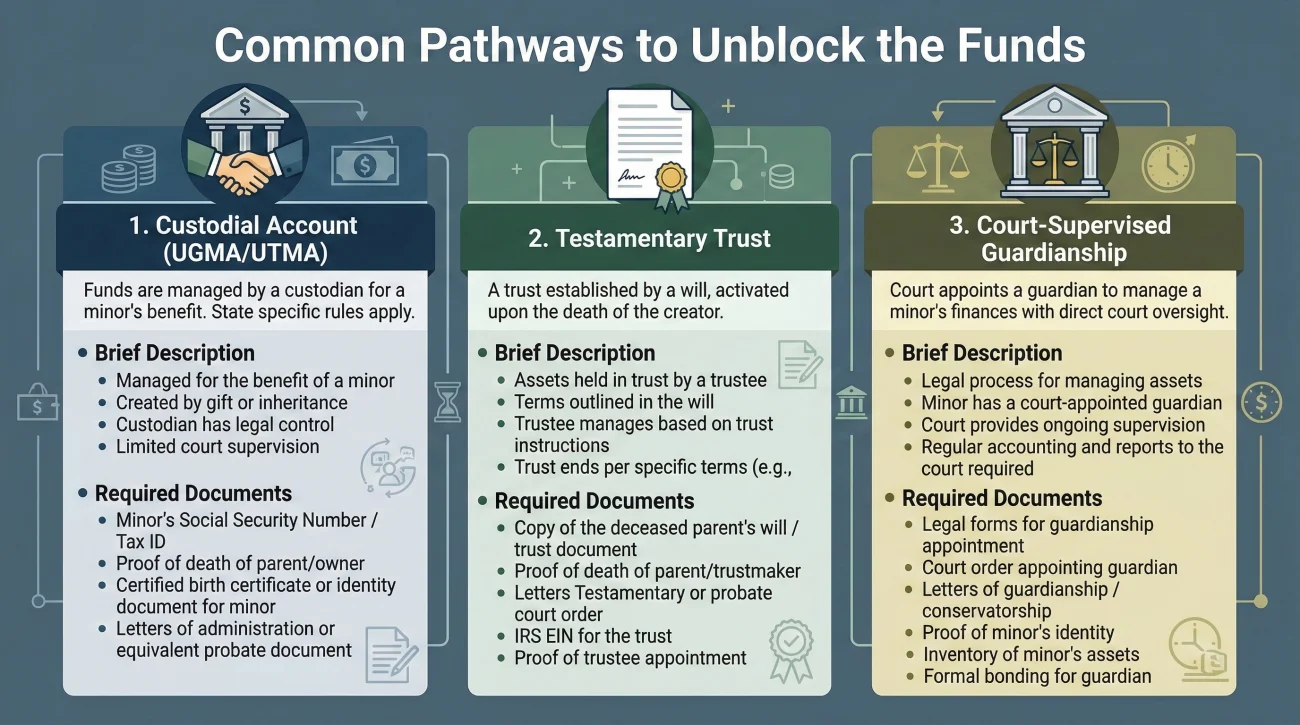

Common Pathways to Unblock the Funds

When an executor cannot distribute directly, the inheritance must be routed through a protective structure. The specific structure you use depends entirely on what the will states, local regulations, and the size of the inheritance. While you will always need local professional guidance to implement these, here is a conceptual overview of the three most common pathways.

| Distribution Pathway | How It Generally Works | Common Documentation Needed |

|---|---|---|

| Custodial Account (UGMA/UTMA) | Funds are placed in a special bank or brokerage account managed by an adult custodian until the minor reaches adulthood. Often used for smaller amounts. | Account opening confirmations, custodian acknowledgement, minor’s tax identification info. |

| Testamentary Trust | The deceased person’s will includes specific instructions to create a trust for the minor. A trustee manages the funds according to the rules in the will. | Trust establishment documents, tax ID for the trust, trustee acceptance forms. |

| Court-Supervised Guardianship | A judge appoints someone (often a parent, but not always) as the “guardian of the property” to manage the funds under strict court oversight. | Certified court orders of appointment, formal guardianship letters. |

When the Will Provides Instructions

The easiest scenario is when the deceased person anticipated the issue. Often, a well-drafted will includes a clause stating that if any beneficiary is a minor, their share should be held in trust or paid to a custodian. If your governing document includes this language, your job is to follow those instructions, work with the designated trustee or custodian, and document the transfer from the estate to that protective entity.

When the Will is Silent

The situation becomes more complex when the will simply says to leave a sum of money to a nephew, without specifying how to handle it if the nephew is a minor. In these cases, executors often have to rely on local laws that allow for transfers to a custodial account, or for larger sums, require the family to go through the process of setting up a court-supervised guardianship of the property. When faced with this silence, your immediate next step is to consult the estate’s professional advisor to determine your state’s default rules. Do not guess which account type is acceptable; get the required pathway confirmed in writing before making any promises to the family.

Key Point: You are not expected to invent a legal solution. Your operational job is to identify the blockage, communicate it clearly, and wait for the proper authority to be established before you write the check.

Communicating the Delay to the Family

Once you understand that a protective pathway must be used, your next immediate task is explaining this bottleneck to the family. When inheritance is delayed, emotions run high. Parents of a minor beneficiary often feel frustrated, assuming the executor is being difficult or withholding funds unnecessarily. In my experience, clear, neutral communication is your best tool for keeping the peace.

You need to explain that the delay is not a personal choice, but a strict compliance requirement. You are simply following the rules that protect both the child’s assets and the estate.

“I can’t give you the money for your son yet. The bank won’t let me and I need to figure out what the will says. Stop asking me about it.”

“Because he is a minor, I am legally restricted from distributing the funds directly. We need to wait for the proper custodial structure to be confirmed so I can transfer it safely.”

Script: Explaining the Legal Requirement

If you are facing pressure from a minor’s parents, you can use a script like this to set boundaries while keeping the tone professional and supportive.

Subject: Update regarding [Minor’s Name]’s distribution from the Estate

Hello [Parent’s Name],

I am writing to provide a status update on the final distributions for the estate. The accounting is moving forward, and we have calculated [Minor’s Name]’s designated share.

Because [Minor’s Name] is a minor, the estate is legally required to distribute these funds into a designated protective structure, rather than a direct payment. This ensures the inheritance is managed securely until they reach adulthood.

I am currently working with the estate’s professionals to confirm the exact documentation needed (such as custodial account details or a trust ID) to finalize this transfer. I will provide you with a written update as soon as we have the specific requirements for releasing the funds.

Thank you for your patience as we make sure everything is handled correctly.

Best regards,

[Your Name]

Executor

What Executors Must Document While Waiting

While you wait for trusts to be established or guardianships to be approved, you cannot simply let the estate file sit idle. One pattern I frequently encounter is an executor losing track of the minor’s exact share because it gets mixed back into the general operating funds of the estate.

Your job is to meticulously track the minor’s share so that your final accounting remains accurate and transparent. In my own tracking files, I never just write “Pending.” I advise executors to use a specific formatting logic in their ledgers.

Here is a simplified, text-based example of how to log the minor’s held funds on your accounting spreadsheet:

Category: Pending Beneficiary Distribution

Description: Allocation for Minor [Name] – Awaiting Custodial Account Details

Amount Allocated: $18,750.00

Status: Held in Main Estate Checking Account (Segregated on Ledger)

Notes: Share calculated after all final debts and $5k reserve holdback. Do not use for general expenses.

- 📄 Calculate the exact share: Document exactly what the minor is owed down to the penny, just as you would for an adult beneficiary.

- ✅ Log the holdback: If there are pending administrative expenses, clearly log how much of the estate’s reserve is being held back proportionally from the minor’s share.

- 📄 Segregate the funds on paper: As shown above, create a specific line item showing everyone that the money is accounted for, just not yet delivered.

- ✅ Maintain the paper trail: Save every email, letter, and note regarding your attempts to set up the proper distribution channel. If questions arise years later, this timeline log is your main defense.

💡 Pro Tip: Treat that pending line item like a locked vault. Do not mix a minor’s pending cash share with your personal funds or use it to pay unrelated estate debts once the final shares have been formally allocated.

How This Impacts the Other Adult Beneficiaries

A common operational challenge arises when an estate has a mix of adult beneficiaries and one minor beneficiary. The adults are usually eager to receive their money, but the minor’s share is caught in a holding pattern while a trust or custodial account is finalized.

In many cases, an executor can proceed with partial distributions to the adult beneficiaries, provided the accounting is pristine. If you can clearly show that the minor’s exact equal share is safely held in the estate account and protected, distributing to the adults often reduces overall friction.

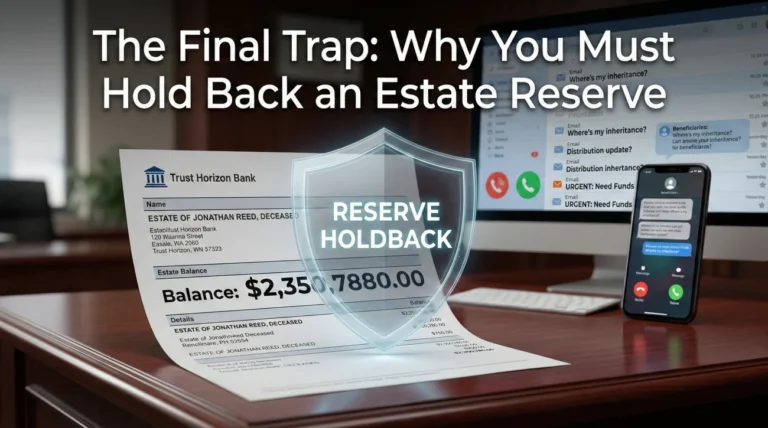

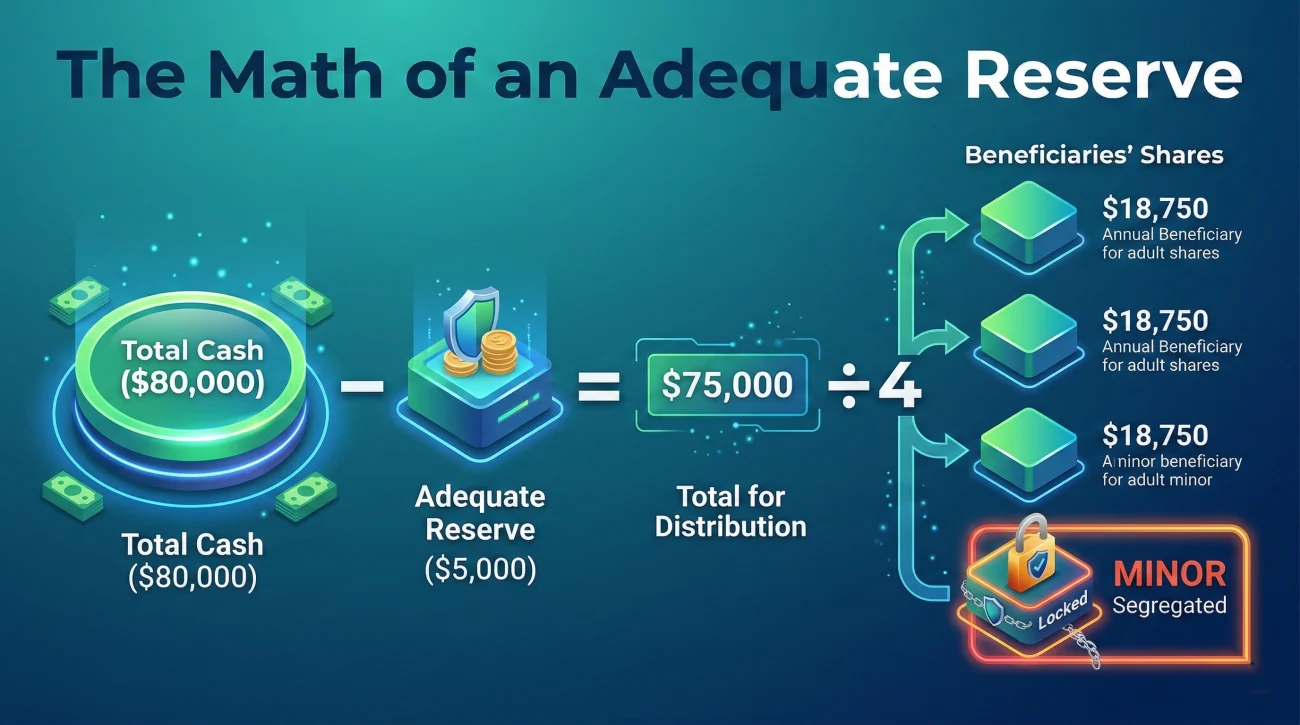

The Math of an Adequate Reserve

However, you must be absolutely certain that your reserve holdback is sufficient to cover any unexpected final taxes or administrative fees. Let us look at a practical math example that I use to explain this to executors.

Suppose the estate has $80,000 in cash after all known debts are paid. There are four equal beneficiaries: three adults and one minor. You do not simply divide $80,000 by four. First, you hold back an “adequate reserve” for final tax preparation and estate closing fees. Perhaps you hold back $5,000.

That leaves $75,000 to distribute. The adults each receive $18,750 now. The minor’s $18,750 sits safely in the estate account, neatly segregated on your ledger. The $5,000 reserve acts as a buffer for everyone. If you failed to keep that $5,000 reserve, fully distributed to the adults, and then a surprise tax bill arrived, you could not legally use the minor’s protected share to pay the adults’ portion of that debt.

[Accurate Accounting] + [Adequate Reserve] + [Segregated Minor Funds] = Safe partial distributions for adults

While this formula works perfectly for straightforward cases, you will likely run into variations that test this standard setup.

Handling Complex Minor Scenarios

In day-to-day admin work, estates rarely fit into perfectly simple boxes. Executors frequently encounter variations that require a more nuanced approach to documentation.

The Minor is Turning 18 Very Soon

If a minor beneficiary is seventeen and a half, going through the heavy legal process of setting up a court-supervised guardianship of property might seem counterproductive. Many executors in this situation, after consulting with their local professionals, choose to simply hold the funds safely in the estate account. They maintain the ledger segregation and delay the final distribution until the beneficiary legally reaches the age of majority. Once they are an adult, the executor can collect a standard, valid receipt and distribute directly.

Multiple Minors with Different Timelines

Complexity multiplies when an estate involves two or three minor beneficiaries at different ages. A five-year-old and a fifteen-year-old will hit the age of majority a decade apart. I always remind executors to maintain completely separate ledgers and communication logs for each child. Do not group them together in one “Minors Fund” on your accounting. Treat each minor as an independent file to ensure accuracy when one ages out while the others are still pending.

When the Minor is the Sole Beneficiary

When the minor is the only person inheriting the estate (for instance, the deceased person’s only child), the dynamic shifts entirely. You do not face pressure from other adult beneficiaries, but you will often face intense pressure from the surviving parent or guardian. The rule remains exactly the same: no informal handoffs. To manage this pressure effectively, focus your communication on the process rather than the delay. Provide the guardian with a clear, written list of the exact court documents or account details you need from them to release the funds, turning a potential confrontation into a collaborative checklist.

The Limbo Phase and Closing the Estate

Managing an inheritance for a protected beneficiary requires stamina. One of the most frustrating realities for an executor is being stuck in a “limbo phase.” You might have finished all other tasks, paid all other beneficiaries, and filed the main tax returns, but the estate cannot technically close because you are still waiting for a judge to approve a minor’s guardianship account.

During this limbo phase, the estate remains open. This means you will likely continue to incur small administrative costs, such as monthly bank fees for the checking account or fees for an annual tax return if the held funds generate interest. You must document these ongoing administrative fees clearly and deduct them proportionately according to the will or local rules, ensuring you do not unfairly penalize the minor’s share.

Your role is not to bend the rules to make the minor’s parents happy, nor is it to rush a closing at the expense of compliance. Your role is to protect the asset, follow the legal pathways available, and maintain a crystal-clear paper trail. By refusing informal handoffs and securing the proper custodial documents, you protect yourself from liability and ensure the minor receives exactly what they are entitled to when the time is right.

❓ FAQ

🏫 Can I pay the minor’s school tuition directly from the estate instead of distributing?

Usually not, unless the will explicitly includes a trust provision allowing funds to be used for the minor’s health, education, maintenance, and support. Without explicit authority, an executor’s job is to distribute assets to the legal structure, not to pay the beneficiary’s personal bills.

📉 What happens if the market drops while the minor’s funds are held?

If the minor’s inheritance is held in cash in a standard estate checking account, it is not subject to stock market drops. If the inheritance includes actual investments, executors must consult local rules on whether they have a duty to liquidate to cash or hold the assets pending the custodial transfer.

⚰️ What happens if the minor beneficiary passes away before turning 18?

If a minor passes away after outliving the deceased but before receiving their funds, their designated share typically becomes part of the minor’s own estate. You would then distribute the funds to the minor’s appointed estate representative, following local inheritance laws.

🧑⚖️ Who pays the legal fees to set up the minor’s guardianship account?

This is highly dependent on local jurisdiction. Sometimes the costs are paid out of the minor’s specific share, and sometimes they are considered a general administrative expense of the main estate. Always get professional guidance before allocating these legal fees.

💼 Do I still file a final tax return if the only remaining task is the minor’s payout?

If the estate remains officially open and the held funds generate more than the minimum threshold of income (like interest), you will generally need to continue filing estate tax returns until the funds are transferred and the estate is formally closed.

🏦 Does the FDIC insure a minor’s pending estate funds the same way?

Yes, funds held in a standard estate checking account at an FDIC-insured institution are protected up to the standard limits, regardless of whether the ultimate beneficiary is an adult or a minor.

🚗 Can I buy a car for the minor using their inheritance?

No. Purchasing personal property for a beneficiary is outside the scope of standard executor duties unless there is a specific trust instructing you to do so. Your job is to deliver the value to a legal custodian, not to act as a personal shopper.

🕰️ Is there a statutory time limit on how long an estate can stay open for a minor?

While there is no universal time limit, probate courts generally want estates closed in a timely manner. If you keep an estate open for years simply to avoid setting up a trust or custodial account, the court may intervene or demand an updated accounting.

🧾 Do I need to send the minor a copy of the final accounting?

You typically send the final accounting to the legally appointed adult representing the minor, such as the guardian of the property, the UTMA custodian, or the trustee. They review the accounting on the child’s behalf.

👶 Can a minor serve as a co-executor if they inherit?

No. Minors cannot serve as executors or co-executors because they lack the legal capacity to sign contracts, bind the estate, or manage finances. If a minor was named as an executor in the will, the court will appoint an alternate adult to serve.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.