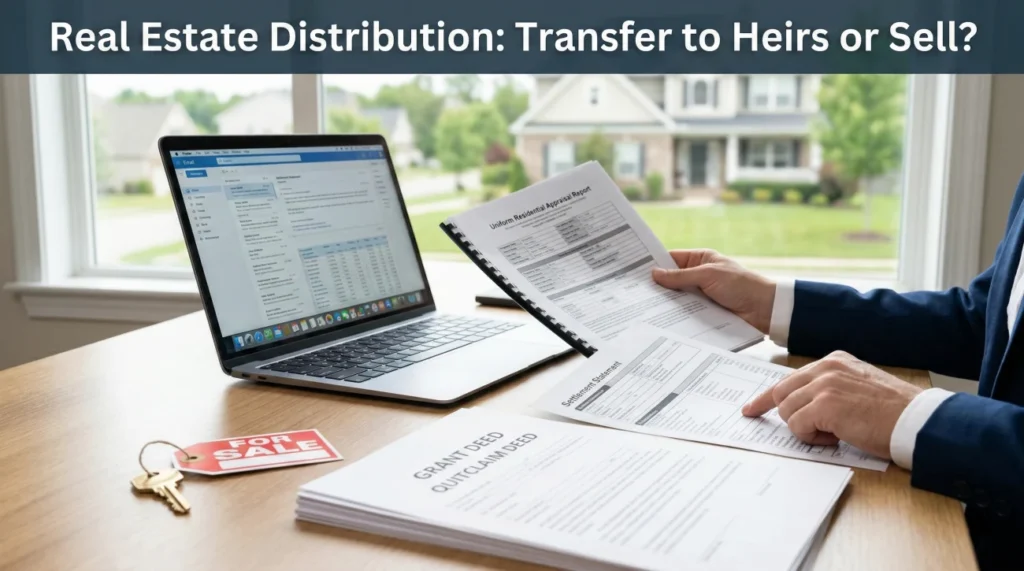

- The Core Decision: Real estate usually forces a binary choice. You either transfer the physical deed to the heirs, or you sell the property and distribute the cash proceeds.

- The Drivers: In my experience, estate debts, carrying costs, and the sheer number of beneficiaries are what actually dictate the path, rather than personal preference.

- The Friction: Occupancy by family members, debates over repair costs, and slow timelines are the most common sources of tension. You must document these issues rather than trying to force an outcome.

- The Paper Trail: Keeping rigorous records of property valuations, monthly maintenance logs, and final settlement statements is what protects your liability when closing the estate.

The Heaviest Asset: Facing the Real Estate Decision

In my daily work supporting estate administration organization, I notice a very consistent pattern. The timeline of an estate usually moves smoothly until it hits the front door of the deceased person’s house. Bank accounts can be frozen and consolidated with a few phone calls. Personal property can be sorted and boxed up over a weekend. Real estate, however, is entirely different. It is a living, breathing liability that requires electricity, insurance, tax payments, and physical security.

When you are working through your estate distribution checklist, the real property will almost always be the heaviest and most complex item you manage. The core question that arises early on is whether you will transfer house to heirs or sell it completely. This is rarely a simple, emotional choice. It is usually dictated by the cold math of the estate.

I always remind the executors I work with that you are not just managing a building. You are managing the financial drain of an empty structure and the heavy expectations attached to a family home. Every single month the house sits in limbo, the estate loses money. My goal here is to help you map out how this decision is commonly made, what you need to communicate to the beneficiaries, and exactly what paperwork you must capture for your final file to prove you acted responsibly.

⚠️ Warning: Before we dive into the operational mechanics, please note that real estate transfer rules, deed formats, and title insurance requirements vary wildly by jurisdiction. You should always use a local real estate attorney or a specialized title company to handle the actual paperwork. Trying to draft a deed yourself is a fast track to clouded titles. This guide focuses entirely on your organizational workflow, not legal court filing steps.

The Two Paths: Transferring vs. Selling

When you boil the process down, an executor distributes a house to beneficiaries through one of two primary pathways. Understanding the conceptual difference between these two paths, and the paperwork each requires, is your first administrative hurdle.

Path 1: Transferring the Property In-Kind

Transferring the property means the estate officially signs the deed over to the heir or heirs. The physical asset changes hands, not its cash value. This path is highly common when a surviving spouse inherits the home, or when an only child inherits their parent’s house and intends to live in it.

The organizational focus here is heavily on valuation and professional coordination. Even if you are just handing the house over, you commonly need a date-of-death valuation for tax basis records. The complexity spikes significantly if the will leaves one house to three siblings equally. Co-ownership among siblings is frequently the root of future lawsuits. If multiple heirs insist on keeping the property, the executor’s file should include a formal, written “Co-ownership Agreement” drafted by a professional. This agreement must detail who pays the taxes, who mows the lawn, and exactly how one sibling can force a buyout later. Without it, you are simply passing a dispute down the family line.

Field Note: I commonly see executors make the mistake of handing over the keys to an heir and assuming the house is “distributed.” Handing over keys means nothing legally. The property remains a liability of the estate until the new deed is officially recorded with the county. Always wait for written confirmation of the recording before closing your real estate file.

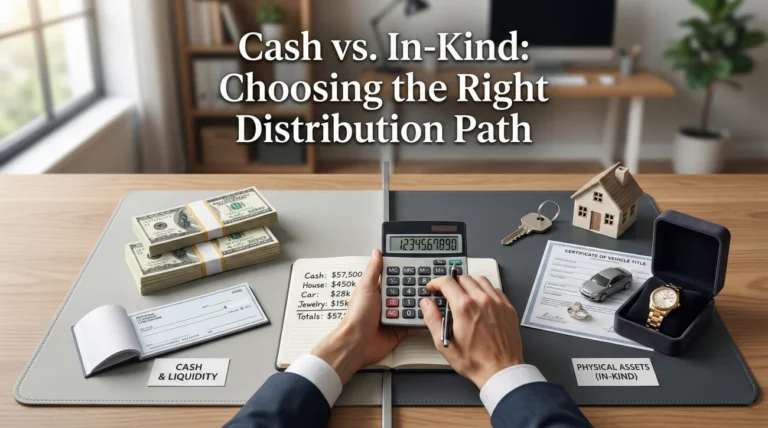

Path 2: Selling the Property and Distributing Cash

Selling the property means the estate lists the house on the open market, navigates the closing process, and deposits the net cash proceeds into the estate checking account. The real estate distribution estate process then transforms into a much simpler cash distribution.

Dividing a hundred thousand dollars in a bank account is mathematically perfect; dividing a three-bedroom house among three people is practically impossible without selling it. The paperwork focus for a sale involves keeping meticulous records of listing agreements, independent appraisals, settlement statements, and proof that the property was marketed fairly.

What Actually Drives the Real Estate Decision

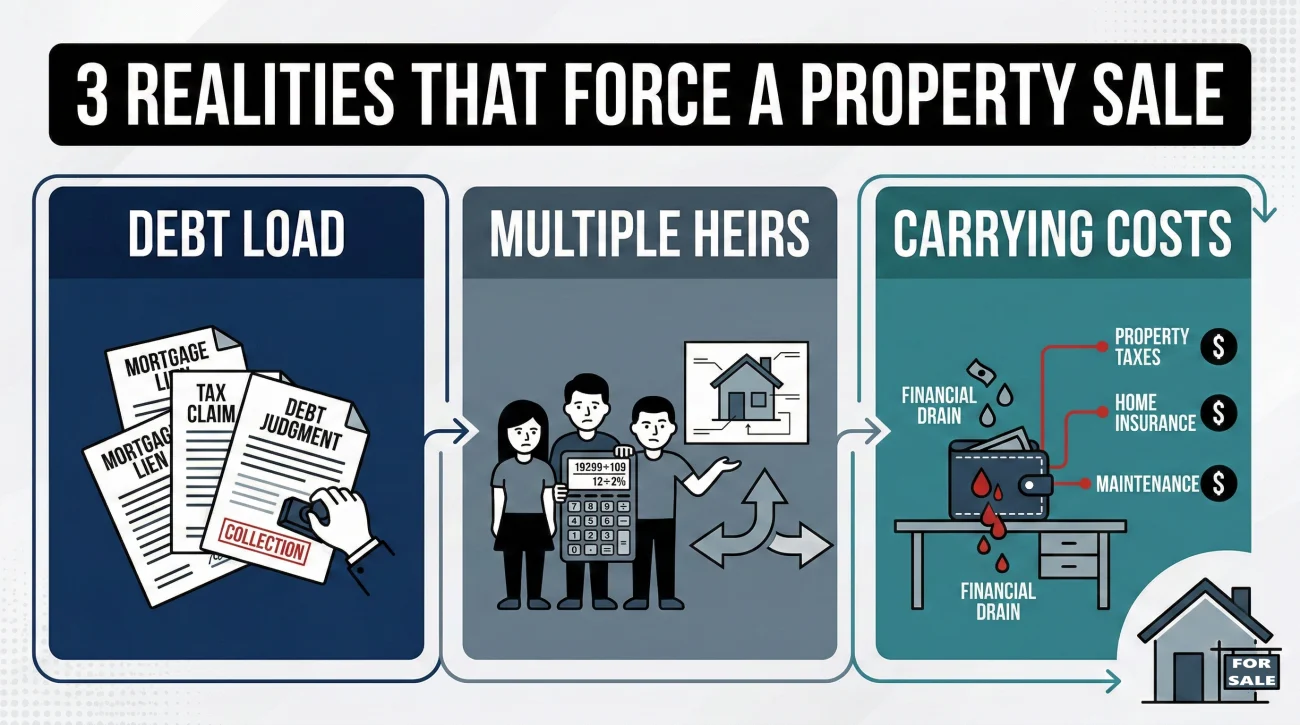

Beneficiaries often have very strong, emotional opinions. “Mom wanted us to keep it in the family” is a phrase I read in estate correspondence constantly. However, your decision as the executor is rarely driven by sentiment. It is driven by the financial reality of the estate. Here are the three primary factors that force the hand of an executor.

1. The Debt Load of the Estate

If the estate owes significant money to creditors, past-due taxes, or a Medicaid recovery program, and there is not enough liquid cash in the bank to cover those debts, the house usually must be sold. An executor simply cannot distribute an asset to an heir if the estate is functionally insolvent. In many situations, liquidating the real estate is legally mandated to satisfy valid creditor claims before the heirs see a single penny.

2. The Math of Multiple Heirs

When a will dictates that the estate is to be divided equally among several people, navigating a sell house probate vs transfer decision leans heavily toward selling. If one sibling desperately wants to keep the house, they typically have to “buy out” the other siblings’ shares.

This requires the estate to obtain a formal appraisal to set an undeniable fair market price. The purchasing sibling must then secure their own financing (like a mortgage) to put cash back into the estate account, which the executor then distributes to the others. If the sibling cannot get a mortgage, the house generally has to go on the open market.

3. The Silent Bleed of Carrying Costs and Vacant Insurance

Houses consume cash every single day. Property taxes, electricity, water, lawn care, and winterization add up astonishingly fast. But the biggest shock to most executors is insurance.

Standard homeowners insurance policies often drop coverage or refuse payouts if a house is vacant for more than 30 to 60 days. Executors are usually forced to purchase specialized “vacant property insurance.” These policies can easily cost double or triple the standard premium and often require upfront payment. If the estate bank account is low on funds, the executor may have no choice but to list the house immediately to stop this financial bleeding.

Guessing what the house costs by looking at an old utility bill from last summer and hoping the estate account has enough to cover it.

Building a strict monthly “Carrying Cost Log” spreadsheet that tracks exact outflows for vacant insurance, taxes, and utilities so you can show beneficiaries the exact math behind a quick sale.

A Realistic Real Estate Timeline

One of the hardest parts of this job is managing beneficiary expectations regarding time. TV shows make selling a house look like a weekend project. In estate administration, a realistic timeline for selling real property often looks like this:

- 📄 Months 1-2 (The Authority & Assessment Phase): Waiting for the court to grant letters of authority, changing the locks, securing vacant property insurance, and ordering the date-of-death appraisal.

- 🧹 Months 3-4 (The Clearing Phase): Sorting decades of personal belongings, holding an estate sale, hiring a clean-out crew, and getting Broker Price Opinions (BPOs) on “as-is” versus “repaired” value.

- 🤝 Months 5-6+ (The Market & Closing Phase): Listing the property, negotiating offers, waiting for the buyer’s mortgage approval, clearing any title hurdles, and finally attending the closing to deposit the check.

Sharing a high-level timeline like this early on helps prevent frantic “is it sold yet?” emails during month two.

Friction Points to Anticipate (And Document)

Because real estate represents the physical anchor of a family’s history, this is where immediate administrative friction occurs. While you cannot control how people feel, you can control how you document the situation.

The Occupancy Problem

Often, someone is already living in the house when the owner passes away. Administratively, you have to split this into two entirely different scenarios: a formal tenant versus an informal family occupant.

If there is a valid, written lease in place, the estate simply steps into the shoes of the landlord. The tenant has legal rights, and you must establish a system to collect that rental income, log it as an estate asset, and handle maintenance requests until the property is sold or the lease expires. It is a business transaction.

The nightmare scenario is an informal family member who refuses to leave, refuses to pay rent, or refuses to allow real estate agents inside. Ignoring this will stall the entire estate. You must document every single communication regarding move-out timelines and property access. If they remain uncooperative, do not rely on informal text messages. Hand the communication log to your estate attorney immediately, as you will likely need to initiate formal, local eviction procedures.

The “Fixer-Upper” Debate

Beneficiaries frequently argue over whether the estate should spend money fixing up the house before selling it. One person wants to install new carpets; another wants to sell it completely “as-is” to get their share faster.

The most practical approach is to request a “Broker Price Opinion” (BPO) from a real estate agent. Ask them to provide two numbers in writing: the “as-is” price and the price after specific repairs, minus the estimated cost of doing those repairs. If spending $10,000 only increases the sale price by $10,000, it is functionally pointless. Document the professional’s opinion and let the math end the debate.

Keeping the Family Updated

To reduce anxiety during the long timeline, your communication hygiene must be flawless. Do not make promises about closing dates. Instead, provide neutral updates on operational progress.

Here is a safe script you can use to communicate progress and keep the focus on next steps:

Subject: Estate Update – Property Status and Next Steps

Hello everyone,

I am writing to provide an update on the property at [Property Address].

We have successfully completed the initial property clearing and secured the required vacant property insurance to protect the asset. Currently, the estate is paying approximately $[Amount] per month to maintain the home safely while it is unoccupied.

To protect the estate’s overall value and move the process forward, our next operational step is [listing the property for sale / finalizing the deed transfer paperwork]. I am actively working with our real estate agent/attorney to finalize the listing agreement in the coming days.

I will provide another status update once we reach the next major milestone, such as reviewing an offer or receiving a closing schedule.

Please let me know if you would like a copy of the recent property appraisal for your records.

Best regards,

[Your Name]

Executor

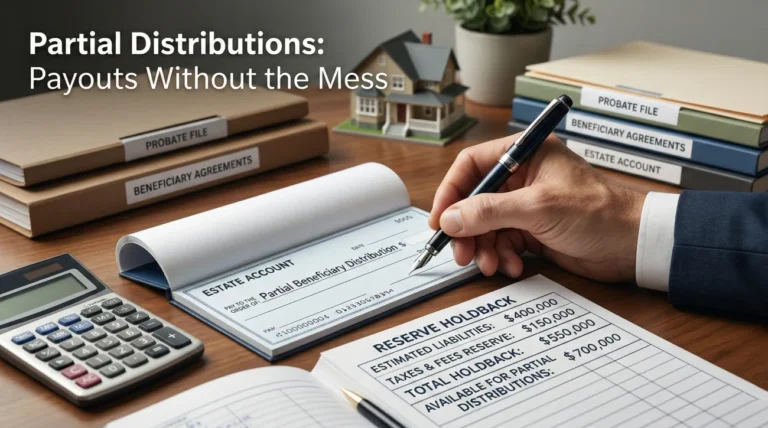

The Real Estate Closing Packet: What to Keep

Whether you choose to transfer the property in-kind or sell it, the transaction will generate a dense stack of documents. When it is time to finalize your duties, you will need specific proof to show you handled the asset fairly. I refer to this as building the “property proof packet.”

Executors often scramble at the end of the process because they threw away a settlement statement. Here is exactly what you need to capture and keep in your permanent file.

| Document Category | Why You Keep It in the Executor File |

|---|---|

| Valuation Proof | Formal Appraisals or BPOs. This definitively proves you did not sell the house below market value to a friend, or transfer it without establishing its legal tax basis for the heirs. |

| The Carrying Cost Log | A dedicated folder showing exactly what the estate paid for utilities, vacant insurance, and maintenance. This justifies the reduction in the estate’s overall cash balance. |

| Final Settlement Statements | The HUD-1, ALTA statement, or final closing disclosure. This is the ultimate proof of exactly how much gross cash came in from a sale, and exactly what fees (commissions, title fees, local taxes) were deducted before the net cash hit the estate account. |

| Recorded Deed Copies | If you are transferring the property, you must keep a copy of the new deed that features the official stamp from the county recorder’s office. This proves the estate legally no longer holds the asset. |

| Communication Logs | Saved emails proving that beneficiaries were kept informed about the listing price, the offers received, or the transfer plan. This proves administrative transparency. |

💡 Pro Tip: Do not just toss the closing settlement statement in a drawer. You will need to extract the exact numbers from that statement (gross sale price, fees paid, net cash deposited) to build your final estate accounting document later. Scan it immediately and make sure every line item is readable.

When to Pause and Get Help

Executors sometimes try to push through real estate hurdles on their own to save a few hundred dollars. With physical property, this is a dangerous game. You should immediately pause your work and consult a professional if you encounter any of these red flag signals:

- 🛑 Hostile Informal Occupants: A family member or informal occupant is living in the house and flatly refuses to move out, allow access, or pay rent to the estate.

- 🛑 Breach of Lease: A formal tenant with a valid lease stops paying rent or refuses to allow necessary access for appraisals and real estate showings.

- 🛑 Underwater Property: The mortgage balance is significantly higher than the home’s appraised value. This means pursuing a “short sale,” which is a process where the bank agrees to accept less than what is owed. It requires submitting estate financial records to the lender’s loss mitigation department. Do not try to negotiate this without a professional.

- 🛑 Hidden Liens: You run a title search and discover old liens on the property from unknown creditors, unpaid contractors, or past tax issues.

- 🛑 Beneficiary Warfare: Multiple siblings are actively fighting over who gets to buy the house, or accusing you of listing it too cheaply.

Final Thoughts: The Psychology of the Empty House

In estate administration, the house is rarely just an asset on a spreadsheet; it is the visual representation of the estate itself. Beneficiaries often feel that the estate is “stuck” until the house is dealt with, and conversely, once it is sold or the deed is transferred, they finally feel a sense of closure.

Your job as an executor is not to make everyone happy with the final sale price or the transfer arrangement. Your job is to execute the disposition legally, preserve the value of the asset while it is under your control, and maintain a pristine paper trail. Gather your appraisals, log every utility bill, communicate the operational steps clearly, and let the professionals handle the closings. When the property is finally settled, the keys handed over, and the net proceeds are safely sitting in the estate account, the entire nature of your job shifts. You go from managing a physical, decaying liability to simply managing a clean ledger of numbers.

❓ FAQ

🏠 Can the executor sell the house if I want to live in it?

In many cases, yes. If the estate lacks the cash to pay off valid debts, taxes, and final expenses, the executor often has the legal duty to sell the house to generate funds, regardless of a beneficiary’s preference to live there.

📉 What happens if the house sells for less than the appraisal?

Real estate markets fluctuate. If the house sits on the market and the executor must accept a lower offer, they typically document the market conditions, the advice of their real estate agent, and the effort made to get the best price to show they acted responsibly.

💸 Are beneficiaries responsible for property taxes before the sale?

Usually, no. The estate itself remains responsible for all holding costs, including property taxes and insurance, until the house is officially sold or the deed is legally transferred to the heirs.

🛠️ Should the estate pay to renovate the kitchen before listing?

Typically, no. Unless a real estate professional guarantees in writing that the cost of the renovation will yield a significantly higher net return, most estates sell properties “as-is” to avoid draining cash reserves and delaying the process.

📦 Who is responsible for emptying the house of personal items?

The executor is responsible for clearing the house before a sale or transfer. This often involves organizing the distribution of heirlooms, running an estate sale, or paying a clean-out crew from estate funds.

🔑 Do I need to change the locks on the estate property?

Securing the asset is a primary duty. If the house is vacant, executors commonly change the locks immediately to protect the physical property. However, if there is a legal tenant or occupant, changing locks can cause severe legal trouble.

📝 What paperwork proves I transferred the house correctly?

A copy of the newly drafted deed that features the official recording stamp or seal from the local county clerk or recorder’s office is the definitive proof that the estate no longer owns the property.

🤝 Can one sibling buy the other siblings out of the house?

Yes, this is very common. The estate usually orders an independent appraisal to set the price. The purchasing sibling then provides their own cash or secures a mortgage to pay the estate for the value of the other siblings’ shares.

🏦 What is a short sale in probate?

When the mortgage owed is higher than the property’s value, the executor may work with the lender to approve a short sale. The bank agrees to accept the sale proceeds as a settlement, though this requires formal negotiation and legal oversight.

⏱️ How long does the executor have to sell the property?

There is no universal deadline, but maintenance costs drain the estate quickly. Executors are generally expected to move diligently to prepare, list, and sell the property within the first 6 to 12 months of administration to preserve estate value.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.