- Every method has a cost: Cash distributions divide easily but depend on unpredictable market timelines. In-kind distributions transfer instantly but require heavy paperwork to prove fair valuation.

- Equalization requires math: If one person takes a large asset like a house, they often have to use personal funds to buy out the estate so the other beneficiaries receive their equal share.

- Reserve comes first: Never distribute liquid funds or high-value physical assets until you have secured enough cash in the estate account to cover final taxes and administrative bills.

The Crossroads of Estate Distribution

Not long ago, I reviewed a file where an executor was managing an estate for three siblings. The estate was heavily lopsided: the family home accounted for two-thirds of the total value, with a small amount of cash making up the rest. One sibling desperately wanted to keep the house. Another sibling wanted their inheritance in cash immediately to pay off debt. The third sibling lived out of state and just wanted the process to be over.

The executor was completely paralyzed. They wanted to honor everyone’s wishes, but the math simply did not work. This is the core of the cash vs in-kind estate distribution decision. It sounds like a basic administrative choice on paper, but in reality, it is where strict spreadsheets collide with messy family emotions.

A cash distribution means you liquidate the estate’s assets, put the proceeds into the main estate bank account, and eventually write clear, divisible checks. An in-kind distribution means you transfer the physical asset directly into a beneficiary’s name. I often see executors get stuck here because they fail to realize that handing over a physical item requires just as much rigorous documentation as selling it to a stranger.

My goal in this guide is to give you a practical framework for navigating these tradeoffs. We will walk through exactly how to balance unequal asset values, how to estimate the timelines for each path, and how to protect yourself from accusations of unfairness.

Understanding the Operational Tradeoffs

Before you guide your beneficiaries through this phase, you need to understand the administrative weight of both paths. Neither option is inherently superior, but each requires a completely different workflow from you as the executor.

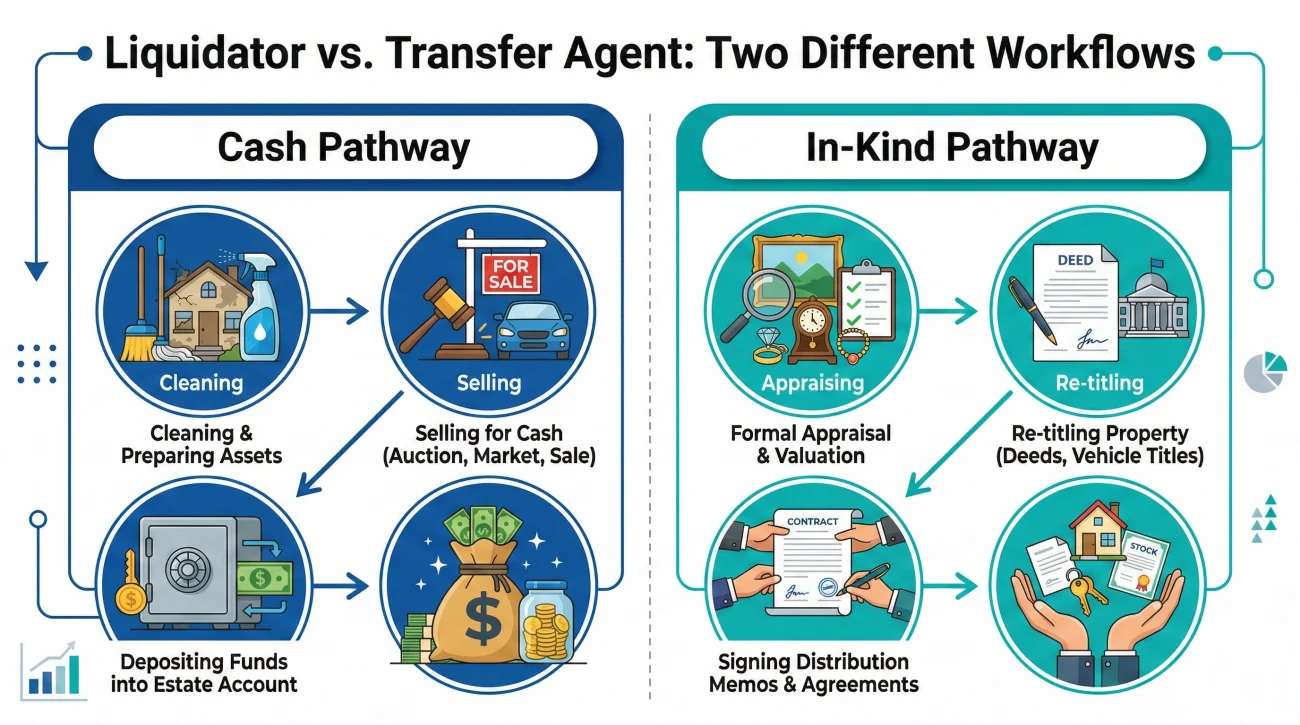

Your job is to act as a liquidator. You clean out properties, hire agents or auctioneers, monitor sales, and deposit funds. The heavy lifting happens before the distribution. The math is incredibly simple, but the timeline is dictated by outside buyers.

Your job is to act as a transfer agent. You research how to re-title specific assets, gather appraisals to prove the item’s value, draft agreement memos, and collect signatures. The physical transfer is fast, but the paperwork is heavy.

Comparing the Realistic Timelines

Beneficiaries often push for whichever option they believe will get them their inheritance faster. As the executor, you have to set realistic expectations about what actually causes delays.

If you choose to sell a house (cash distribution), you are looking at weeks of clearing it out, weeks on the market, and a 30 to 60 day closing period. The timeline is entirely dependent on the market. If you transfer the house directly to a beneficiary (in-kind distribution), the physical transfer can happen as quickly as a deed is drafted and recorded, which might only take a few weeks. However, the internal paperwork required to get all siblings to agree on the appraisal value before that deed is signed can sometimes drag on for months if there is a dispute.

The Cash Reserve Guardrail

Before we dive deeper into the mechanics of giving things away, we need to address the biggest operational trap in estate distribution: the asset-rich, cash-poor estate.

If you decide to distribute large assets in-kind, you must ensure you are not giving away the very value you need to pay the estate’s final bills. Even if everyone agrees to take property instead of cash, the estate itself still owes potential taxes, professional fees, and administrative costs. You cannot pay a final utility bill with a percentage of a vintage car.

❌ Note: Never distribute all of your liquid cash to beneficiaries if you still hold illiquid property that might incur maintenance costs. Once money leaves the estate account, it is incredibly difficult to get it back.

Before you approve any transfers, you must map out your projected final expenses. This is a massive part of your overall Estate Distribution Checklist. You must hold back enough cash to cover every known and potential final liability before anyone gets anything.

Why Cash Distributions Keep the Math Simple

Many professionals lean heavily toward liquidating assets because cash is undisputed. When you are sitting at your desk trying to balance the final spreadsheet, a bank statement showing a clear balance of funds is much easier to divide by three than a house, a car, and a collection of power tools.

Key Point: Cash is perfectly divisible. It does not require appraisals, it does not require maintenance while it sits in the estate account, and it removes your personal judgment from the equation entirely.

When you liquidate, you create a very clean operational narrative. You can point to the closing statement of a house sale or the receipt from an estate sale and say, “This is exactly what the open market paid.”

The Administrative Costs of Selling

The cash route does come with its own administrative friction. Selling assets incurs costs. Realtor commissions, auctioneer fees, staging costs, and junk removal services will eat into the final total. You have to be prepared to explain these administrative expenses clearly when you present your final numbers.

⚠️ Warning: A common mistake I see executors make is failing to log the costs of liquidation as they happen. If you pay a cleaning crew to prepare a house for sale, that invoice must be saved and logged immediately. Unexplained expenses will make your final accounting look disorganized and invite suspicion.

The Mechanics of In-Kind Transfers

Distributing assets in kind is incredibly common when an estate holds a family home or assets that would lose significant value if sold in a rush. But this is where you must put your administrative defenses up. The danger of in-kind transfers is the perception of unfairness. If Beneficiary A gets the house, Beneficiary B is going to watch the valuation of that house very closely.

If you distribute assets in kind, your primary job is to build a documented valuation record. You cannot simply guess what something is worth. You need external, objective data. To keep this process organized, I highly recommend following a strict sequence for every item.

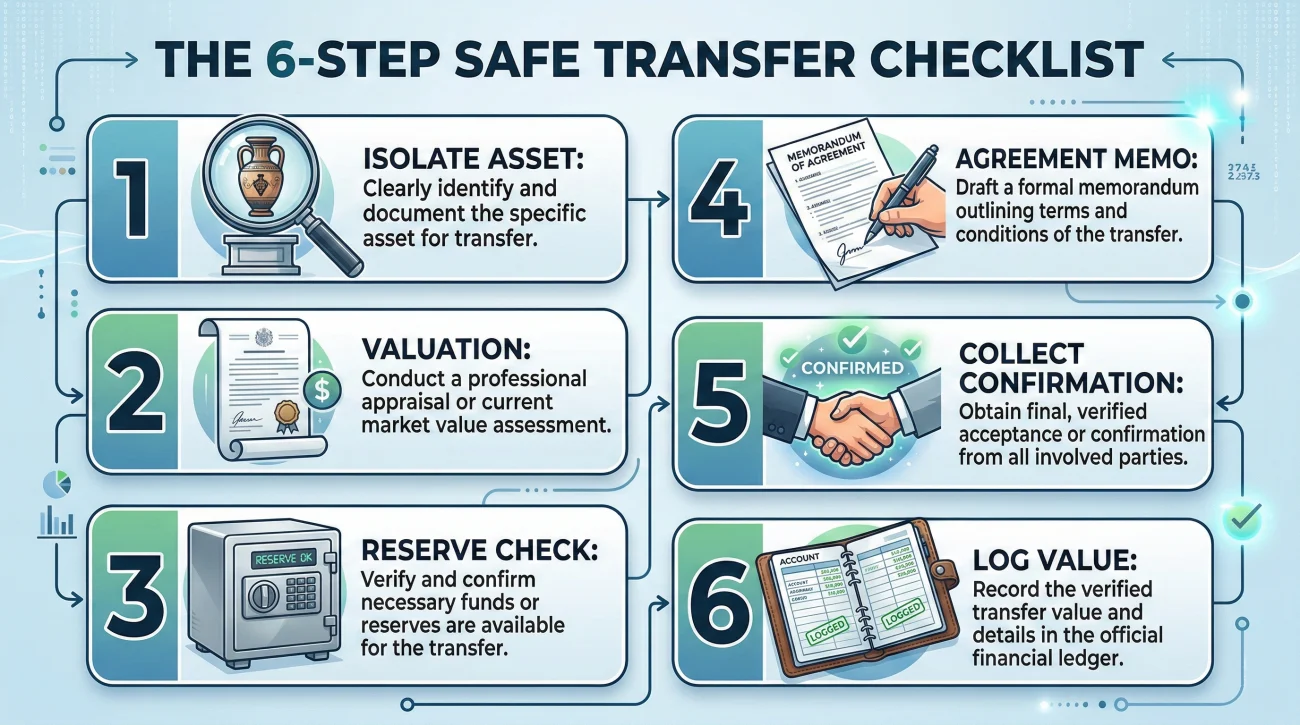

The 6-Step In-Kind Transfer Checklist

When a beneficiary requests to take a specific item instead of cash, follow this operational path to protect the estate:

- 📄 Step 1: Isolate the asset. Confirm it is fully owned by the estate and has no hidden liens.

- 📄 Step 2: Pull an objective valuation. Get a formal appraisal for real estate, or print a screenshot of an industry guide (like Kelley Blue Book) for vehicles on a specific date.

- 📄 Step 3: Calculate the reserve impact. Ensure giving this asset away does not leave the estate without enough cash to pay its bills.

- 📄 Step 4: Draft the agreement memo. Document the exact dollar value assigned to the item.

- 📄 Step 5: Collect confirmations. Get written agreement from the receiving beneficiary that this value will be deducted from their total share.

- 📄 Step 6: Log the value immediately. Add the agreed dollar amount to your final distribution ledger as if it were a cash payment.

The Concept of Equalization (With Real Math)

Understanding how to process an in-kind transfer naturally leads to the most common hurdle executors face: equalization. When values are unequal, you have to use cash to balance the scales. This is a concept many beneficiaries struggle to understand until they see the actual numbers.

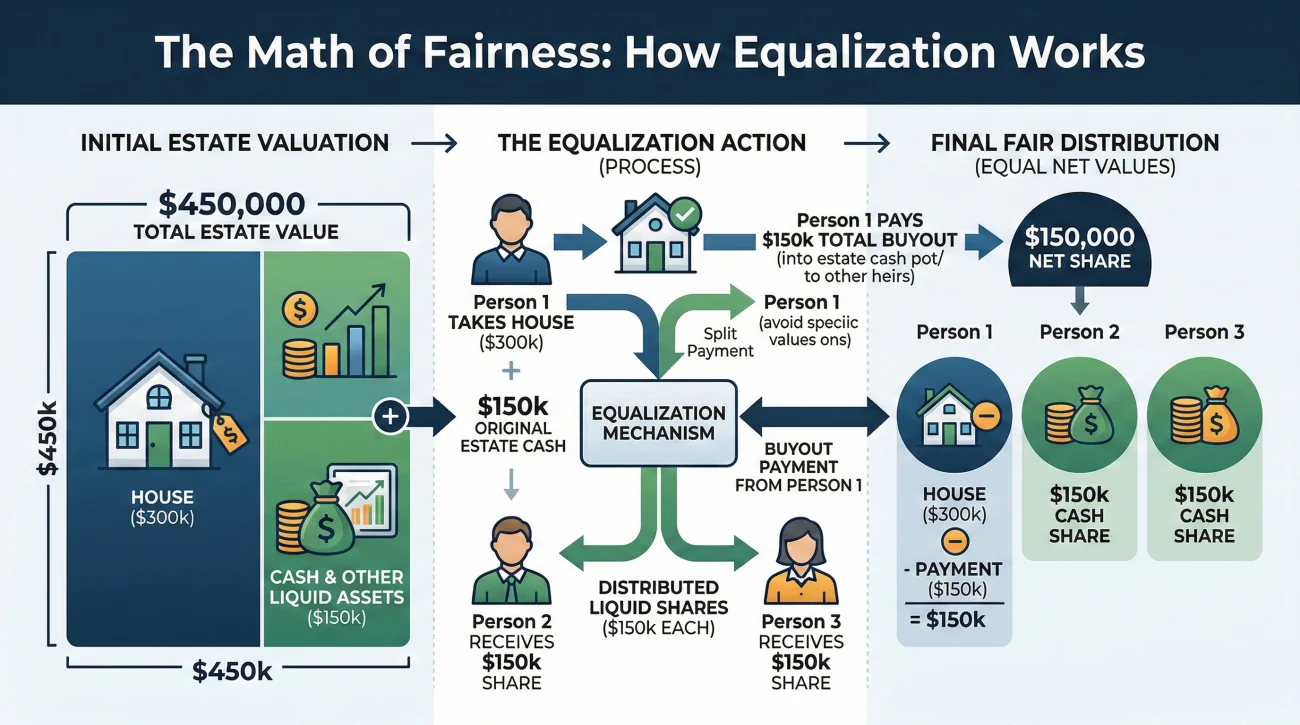

Let’s return to the three siblings from the beginning of this guide. Imagine their estate has a total settled value of $450,000. It consists of the house worth $300,000 and a bank account holding $150,000 in cash. Divided by three, each sibling is entitled to exactly $150,000.

The first sibling wants to keep the house. The operational problem is immediately obvious: the house is worth $300,000, which is double their rightful share. You cannot simply give that sibling the house and split the $150,000 cash between the sibling with debt and the out-of-state sibling. If you did, the first sibling would walk away with $300,000 in value, while the other two would only get $75,000 each.

Executing the Buyout

To equalize this estate, the sibling keeping the house must use their own personal money to “buy out” the difference. Here is how the math actually works on your distribution ledger:

- ✅ The sibling keeping the house receives the property (Value: $300,000).

- ✅ That sibling receives $0 from the estate’s cash account.

- ✅ That sibling must pay $150,000 out of their own pocket into the estate’s bank account.

Now, the estate’s bank account holds the original $150,000 plus the new $150,000 buyout, making a total of $300,000 in cash. The sibling paying off debt and the out-of-state sibling can now each receive a clean cash check for $150,000. Every single person receives exactly $150,000 in total value, and the accounting is perfectly balanced.

💡 Pro Tip: In the real world, your numbers will rarely be this clean. An estate might be worth $431,215, and a house might appraise at $289,500. But the operational logic remains exactly the same: whatever value someone receives in physical property is subtracted from their target share, and if they take more than their share, they must buy out the difference.

What If a Beneficiary Refuses Property?

Executors often encounter the opposite problem: the estate contains physical assets, but no one wants them. I frequently see situations where an estate includes a piece of rural land or a house packed with antique furniture, and all the beneficiaries tell the executor, “I don’t want the items, just send me my percentage in cash.”

If a beneficiary refuses an in-kind distribution, you generally cannot force them to take a deed to a property or a truckload of furniture. Your operational duty is to the estate’s value, not its physical form.

When this happens, the path forward is straightforward, though labor-intensive. You revert to the cash distribution pathway. You must hire the estate liquidators, list the property on the market, sell the assets for whatever fair market value they can command, and distribute the resulting cash. Be sure to document the refusal in writing, so if a beneficiary later complains about how long the sale took or the final sale price, you have a record showing that liquidation was required because an in-kind transfer was rejected.

Communicating Tradeoffs to Beneficiaries

Often, beneficiaries do not understand the administrative burden behind these choices. They might be frustrated that a house is taking months to sell, or they might be annoyed that you are demanding appraisals before handing over a piece of jewelry. Your job is to communicate the “why” calmly and neutrally, keeping the focus entirely on the math.

Script: Explaining the Need for Valuation

If a beneficiary wants to take an item directly but is resisting the appraisal step, use a message like this to establish your boundaries:

Subject: Next steps regarding the [Asset Name]

Hello [Name],

I know you are interested in taking the [Asset Name] as part of your distribution. To make that happen, I need to ensure the estate accounting remains perfectly balanced for everyone.

Before we can transfer it, I need to secure an objective valuation for the item so I can accurately record it on the final spreadsheet. I am currently gathering [estimates/appraisals] and will share that number with you once I have it.

Once we all agree on that value in writing, we can move forward with the transfer. Let me know if you have any questions about how this fits into the overall accounting.

Best regards,

[Your Name]

Script: Explaining the Decision to Liquidate

If you have decided that selling an asset is the safest and cleanest operational path, despite some beneficiaries wanting to handle things informally, explain the decision using process-focused language.

Subject: Update on estate assets and liquidation plan

Hello everyone,

I want to provide an update on the [Asset Name]. After reviewing the estate’s current requirements and the timeline for closing, I have determined that the most transparent path forward is to sell the asset on the open market.

This will allow us to convert the asset to cash, which establishes an exact, undisputed value for the final accounting and makes the final distribution mathematically straightforward.

I will be listing the item in the coming weeks and will keep all proceeds in the main estate account until the final distributions are ready.

Thank you for your patience as we work through these steps.

Best,

[Your Name]

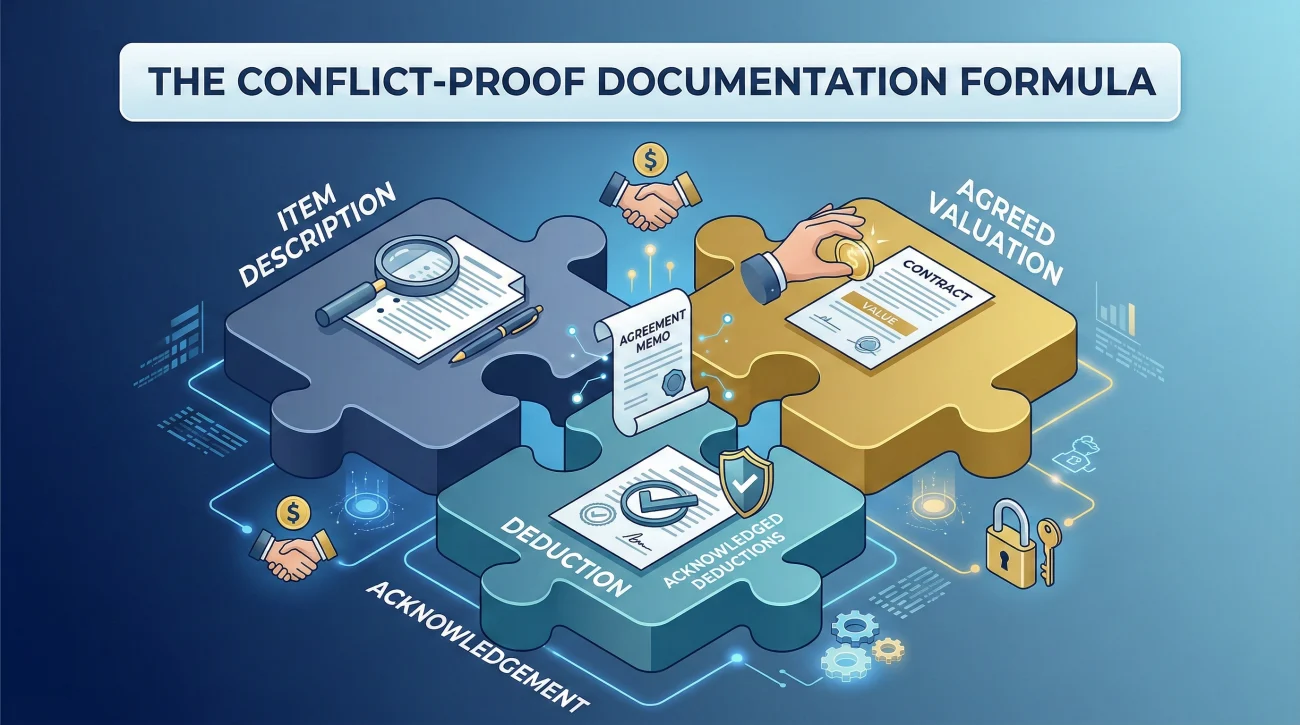

The Documentation That Reduces Conflict

If you take the in-kind route, your safety as an executor relies entirely on your paper trail. If a beneficiary questions an estate distribution option a year from now, your memory will not protect you. The most critical piece of paper you will generate during this phase is the agreement memo.

Before any physical item leaves the estate’s control, you must have a written record indicating that the receiving beneficiary agrees to take the item at a specific, stated value. This does not always need to be a formal legal contract wrapped in legalese, but it must be clear. For everyday personal property, an email trail is often sufficient, provided it is confirmed.

If you are writing an email to confirm an item transfer, use this simple formula to ensure you capture all the necessary administrative data:

[Item Description] + [Agreed Valuation Amount] + [Acknowledgement of deduction from final share]

💡 Pro Tip: Establish a strict file-naming habit early. When you save these agreements alongside your Estate Asset Inventory Checklist, name your files so you know exactly what they are without opening them. A good format is `YYYY-MM-DD_[Asset_Name]_[Document_Type]`. For example: `2024-06-01_Silverware_BeneficiaryAgreement.pdf`.

Closing the Loop on Distributions

Choosing between cash and in-kind distribution is rarely an all-or-nothing scenario. In most estates, you will end up executing a mix of both. You might sell the house and the vehicles to generate liquid cash, while distributing personal household items directly to family members.

The secret to surviving this phase without burning out is to treat every distribution exactly the same way. Whether you are writing a check or handing over a piece of furniture, the operational sequence does not change: determine the value, subtract it from the beneficiary’s total share, log the transfer, and close the loop.

If you communicate your reasons clearly and refuse to bypass the equalization math just to save time, you will protect the integrity of the estate and ensure a fair finish line for everyone involved.

❓ FAQ

🤔 What does distributing in kind actually mean?

Distributing in kind means transferring the actual, physical asset (like a house, a car, or shares of stock) directly into a beneficiary’s name, rather than selling the asset first and giving them the cash proceeds.

🏠 Can a beneficiary just take the house instead of us selling it?

Often, yes. However, the value of the house must be objectively determined, and that value is deducted from their total share. If the house is worth more than their share, they typically have to use personal funds to pay the difference into the estate.

⚖️ How do I make things fair if one person gets a car and the other gets cash?

You ensure fairness through objective valuation and strict accounting. You record the exact market value of the car on your ledger as a distribution to that person. This acts identically to a cash payment, reducing the amount of remaining cash they are owed.

💬 What do I say when two people want the exact same item?

Keep it neutral. Inform both parties that since an agreement cannot be reached, you will either use a documented disposition pathway (like a rotating selection process) or you will sell the item on the open market and divide the cash to ensure equality.

📉 Do I have to get a formal appraisal for every single item we distribute in kind?

Not always. For everyday household items, a written agreement among beneficiaries on a reasonable estimated value is often enough. High-value items like real estate, jewelry, or art typically require formal appraisals to protect your records.

⏳ Does it take longer to sell an asset or transfer it directly?

Selling assets usually takes longer because you are at the mercy of market demand and closing schedules. Transferring in-kind is faster physically, but the internal paperwork, valuations, and gathering signatures can still cause significant administrative delays.

📝 What paperwork do I need if a beneficiary takes furniture instead of cash?

You need a written record confirming what the item is, the agreed-upon dollar value of the item, and an explicit acknowledgement that the beneficiary is accepting it as part of their total estate share.

🚫 Can I force a beneficiary to take an item they do not want?

Generally, no. If a beneficiary refuses to accept an item as part of their share, the standard operational path is for the executor to liquidate the item on the open market and distribute the resulting cash proceeds.

💼 Do in-kind transfers skip the final accounting?

Absolutely not. An in-kind asset must be listed at its documented market value on the final accounting summary. It acts exactly like a cash payment, ensuring the final numbers balance out for all parties.

🏦 Should I empty the estate bank account before doing in-kind transfers?

No. You must always maintain a cash reserve in the estate account to cover final taxes, professional fees, and unexpected bills. Never distribute liquid cash until you are certain every final liability is paid.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.