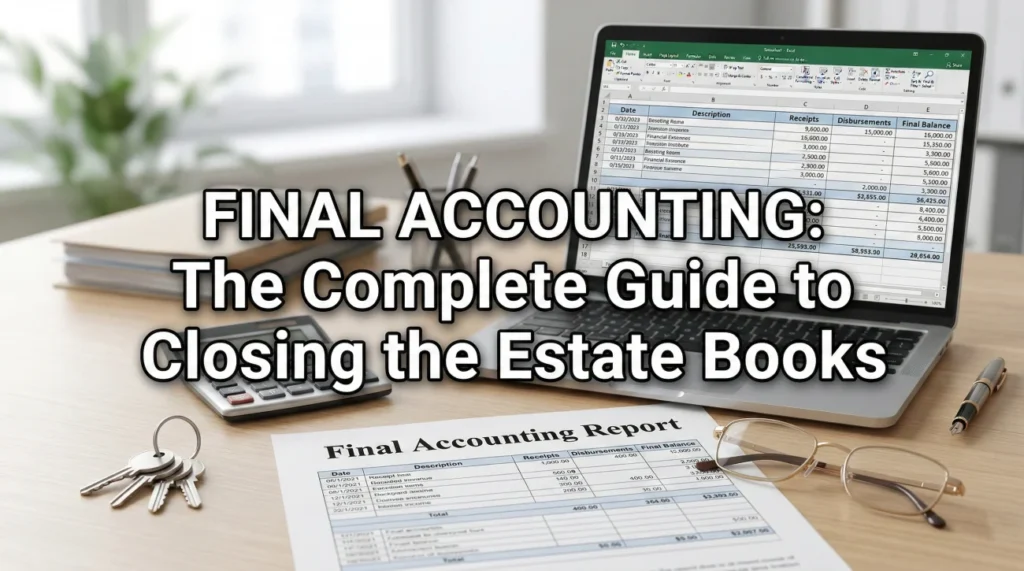

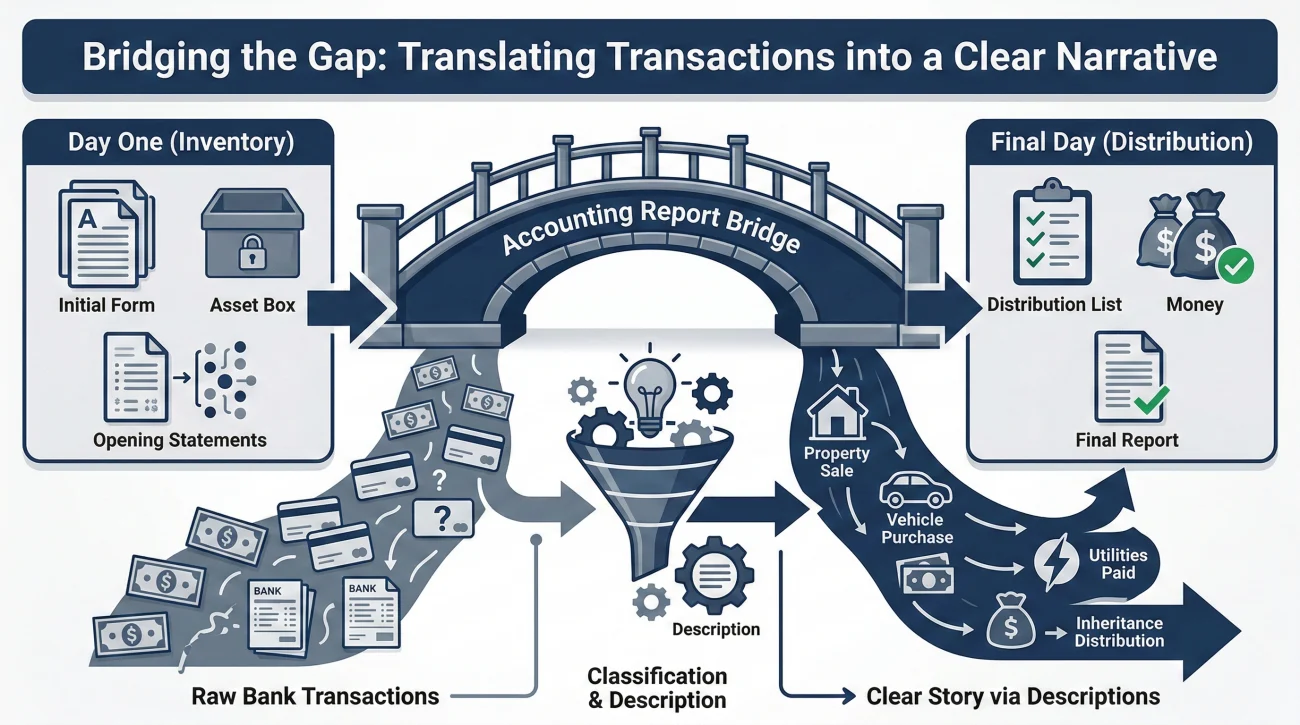

- The final accounting is the complete financial story of the estate, showing exactly what came in, what went out, and what is left for distribution.

- It typically includes four main sections: the starting inventory, money in (income), money out (expenses and debts), and the ending balance.

- Specific, readable descriptions for every transaction reduce the chances of beneficiaries questioning your work.

- A digital-first folder structure with clearly named receipt files makes assembling this report much faster and provides solid proof if asked.

The Paper Trail That Ends the Job

When I help families organize estate files, a process I have guided hundreds of executors through over the years, the moment of highest anxiety is almost always the final accounting. After months of making phone calls, tracking down assets, and dealing with creditors, you are finally nearing the finish line. But before you can close the doors and distribute the remaining funds, you have to show your work.

As an executor, you are managing someone else’s money, and standard fiduciary practice dictates that beneficiaries have a right to know how that money was handled. The final accounting in probate is simply the document that bridges the gap between the day you took over and the day you hand out the inheritances. It proves that you acted responsibly, paid the right bills, and calculated the final shares fairly.

In my day-to-day work, I often see executors freeze up at this stage because they think they need to be a certified accountant to build this report. You do not. I once reviewed a file where a closing was delayed for three weeks over an unexplained $4.12 bank fee. The issue was not that the executor lacked accounting skills, but simply that the story was incomplete. While formatting requirements can vary depending on local guidelines, the core concept is universal: it is a logical, readable summary of math.

To keep the stress levels low, it helps to understand exactly where this report fits into your overall estate distribution checklist. Once you view it as a simple narrative rather than a complex tax form, the task feels much more manageable.

What Final Accounting Actually Is (In Plain English)

Let us strip away the formal terminology. At its heart, an estate accounting is just a highly detailed story translating raw bank transactions into a narrative that a normal, stressed-out family member can read and understand.

It is not a tax return, and it is not just a stack of bank statements tossed into a folder. Raw bank statements show that money moved, but they do not explain why a transaction happened. Your job is to provide that “why.”

💡 Pro Tip: Always write your accounting draft with the “Stranger Rule” in mind. If a complete stranger were to read your report, would they understand exactly why a check was written to “Smith Hardware” without having to ask you? If the answer is no, you need more detail.

Often, beneficiaries are sitting in the dark for months while you handle the administrative heavy lifting. Their only view into your hard work is this final document. When an accounting is clean, transparent, and easy to follow, it builds trust and usually leads to a much smoother closure.

The Four Typical Sections of an Accounting

To build that transparent story, you need structure. While local jurisdictions may ask for specific layouts, almost every readable estate accountings document relies on four distinct sections. Keeping these sections separated in your own logs will make your life significantly easier when drafting the final report.

1. The Starting Inventory (Where Things Began)

This is your baseline. It lists the value of the estate on the exact day the person passed away, or the date you were officially appointed (depending on local rules). It includes bank account balances, the estimated value of real estate, investment accounts, and valuable personal property. The purpose of this section is to say, “Here is exactly what I started with.”

2. Money In (Income and Additions)

During the administration process, the estate likely generated income. This section logs every single dollar that came into the estate after the starting date.

- ✅ Refunds from canceled insurance policies or utility deposits.

- ✅ Final paychecks or delayed bonuses.

- ✅ Proceeds from the sale of a house or a vehicle.

- ✅ Dividends or interest earned on the estate checking account.

Key Point: Even pennies matter here. A common frustration I hear from beneficiaries is finding out an account earned interest, but that interest was never documented on the accounting draft. It makes the executor look sloppy, even if the amount was tiny.

3. Money Out (Debts, Expenses, and Fees)

This is usually the longest and most scrutinized section. Every time a penny leaves the estate account, it must be recorded here. Common sub-categories often include administrative expenses (like court fees), maintenance costs (like utility bills to keep a house safe), and creditor payments.

4. The Ending Balance (What is Left to Distribute)

This is the simple math at the end of the report: Starting Inventory + Money In – Money Out = The Ending Balance. This final number represents exactly what is currently sitting in the estate bank account, ready to be divided among the heirs.

What If You Inherited a Mess?

Sometimes, you step into the executor role after someone else stepped down, or you find that the deceased person left behind incredibly tangled finances with zero paper trail. If you cannot establish a clean starting inventory, do not guess. Document the exact state of the accounts on the day you gained legal access, note the missing historical data clearly in your report, and consult a local professional to help you establish a defensible baseline.

How to Keep the Report Readable and Calm

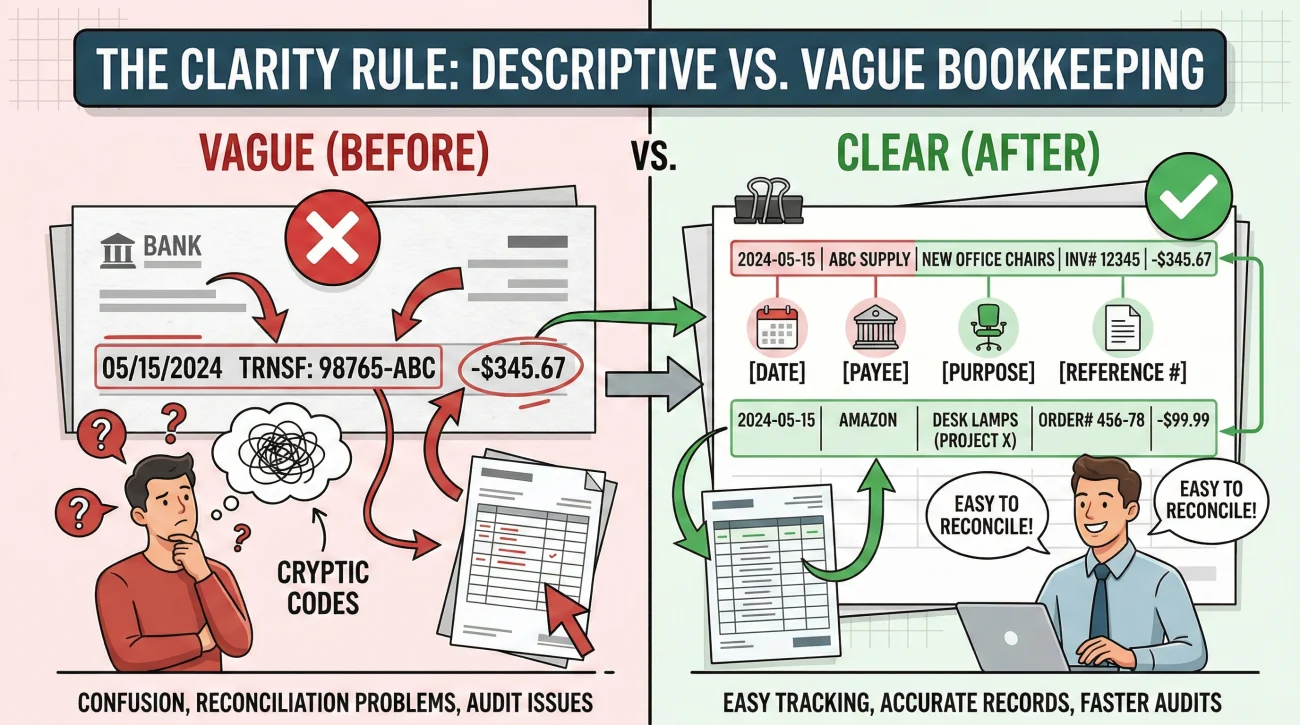

Once you have your four categories organized, the next challenge is formatting the details. As I mentioned earlier, if you hand over a document filled with vague abbreviations, you are going to get angry phone calls. The difference between a beneficiary who signs off quickly and one who demands a formal review often comes down to how line items are described.

10/12/2023 – Transfer – $450.00

10/12/2023 – Paid Joe’s Landscaping – $450.00 (Lawn maintenance for main house prior to sale, September invoice)

Notice how the “After” example leaves no room for questions. It tells the reader who was paid, what service was provided, and why it was necessary for the estate. Taking an extra thirty seconds to type out a full description saves hours of arguing later.

Furthermore, avoid using giant catch-all categories. Putting five thousand dollars under a category called “Miscellaneous” is a guaranteed way to halt your progress. Instead, break expenses out into logical sub-categories. Common groupings include administrative expenses (like court filing fees), maintenance costs (like utility bills to keep a house secure), and creditor payments (like resolving final medical bills).

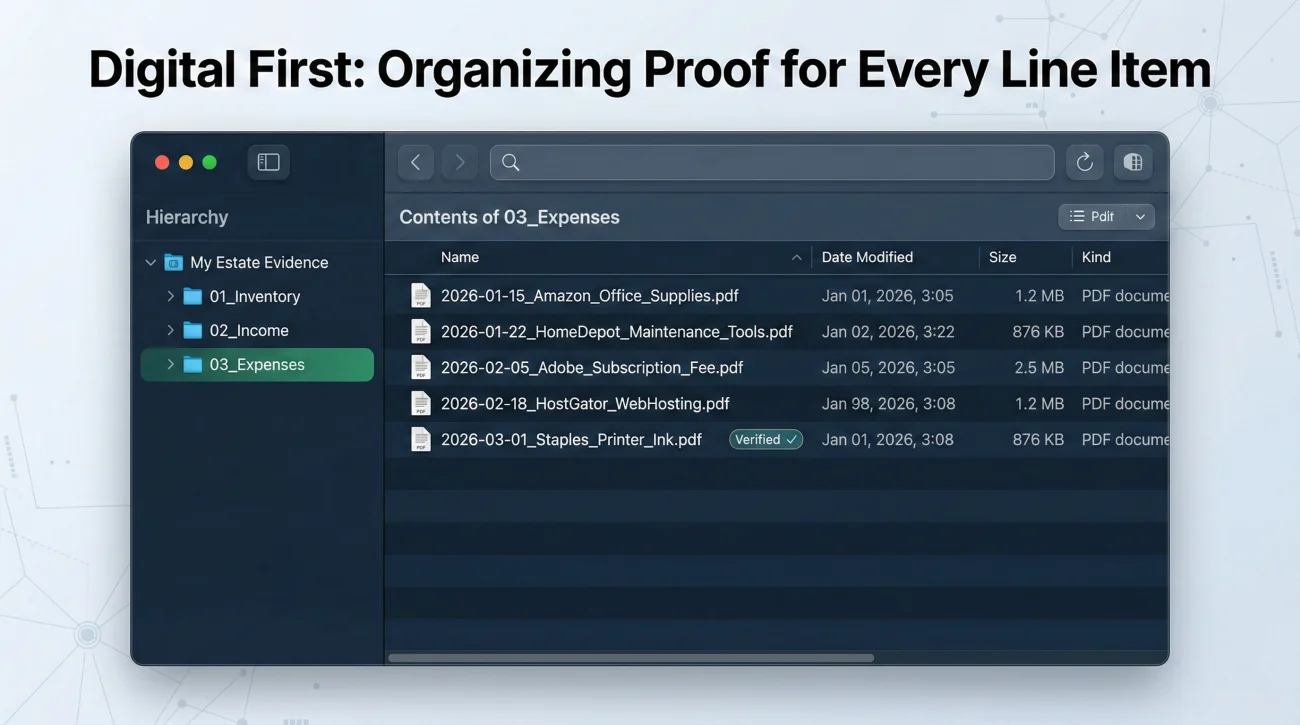

The Supporting Documents: A Digital-First Approach

A summary report is only as strong as the evidence behind it. While you may not need to mail every single receipt to every beneficiary by default, you must have them organized and ready to produce if asked. I call this the “Show Your Math” phase of the job.

| Accounting Category | What You Should Have in Your Folder |

|---|---|

| Starting Inventory | Date-of-death bank statements, professional appraisals for property. |

| Income / Money In | Closing statements from real estate sales, letters confirming refunds. |

| Expenses / Money Out | Itemized invoices from vendors, cleared check images. |

To keep this manageable, I highly recommend a digital-first folder structure. Digging through a shoebox of faded paper receipts months later is a nightmare.

💡 Digital Organization Tip: Create a master folder on your computer backed up to a secure cloud drive. Whenever you pay a bill, scan or download the invoice and the bank confirmation immediately. Use a strict naming convention, such as [YYYY-MM-DD]_[Vendor]_[Description]. For example: 2023-11-05_CityWater_FinalBillPaid.pdf. If someone questions an expense later, you can find the exact proof in seconds.

Common Mistakes That Delay the Finish Line

Even well-intentioned executors stumble when pulling these numbers together. Through my years of observing this process, I have noticed several recurring patterns where timelines slip because of accounting errors. Here is how to avoid them.

The Missing Beginning Balance

Often, an executor will diligently list all the expenses but fail to establish the exact starting value of the estate. Beneficiaries cannot verify your math if they do not know what number you started with. Always begin your report with a clear, verified inventory value so the final math has a foundation.

Mixing Personal and Estate Funds

Sometimes, an executor will accidentally use their personal credit card to buy cleaning supplies for the estate house. This makes the accounting incredibly difficult to reconcile. Keep everything strictly inside the estate checking account.

Math That Does Not Tie to the Penny

If your accounting says the ending balance is $50,000, but the estate bank statement shows $49,950, you have a problem. An accounting must balance perfectly. A $50 discrepancy might seem minor, but to a beneficiary, it signals that other mistakes might exist.

Getting the Year Wrong

Estate administration almost always crosses over into a new calendar year. A surprisingly common mistake is logging a January expense with the previous year’s date. This throws off the timeline and confuses anyone trying to match the report against bank statements.

Blurring the Tax Lines

The deceased person’s final personal income tax and the estate’s own income tax are two entirely different things. While you do not need to explain tax law in the accounting, you must label these payments clearly so beneficiaries (and the IRS) know exactly which tax burden was paid.

Forgetting Specific Bequests

If the will states that a specific car goes to a specific nephew, that distribution needs to be noted in the accounting. Executors sometimes hand over the physical items early and forget to log them, leaving a gap between the starting inventory and the ending balance.

A Working Example: How a Ledger Should Look

To make this concrete, let us look at how you might format the daily ledger that eventually builds your final report. Notice how each entry tells a complete mini-story.

Estate of Jane Doe – Administration Ledger Excerpt

Date: 04/15/2024

Type: Money Out

Payee: City Water Department

Amount: -$85.50

Description: Final water bill for Elm Street property, covering usage prior to the sale closing on April 10th. (Check #104)

Date: 04/18/2024

Type: Money In

Source: State Farm Insurance

Amount: +$210.00

Description: Prorated refund for canceled auto insurance policy after vehicle was sold. Deposited to estate checking.

When you maintain this level of discipline throughout the process, drafting the probate final account report becomes nothing more than organizing these clear, precise notes into categories.

Before You Hit Send: The Pre-Send Checklist

Before you finalize the document and mail it out, pause and run through this final quality check. I highly recommend bookmarking this list.

- ✅ Does the starting inventory exactly match the value established at the beginning of the process?

- ✅ Does the math balance out to the exact penny matching the final bank statement?

- ✅ Does every single line item have a specific date attached to it?

- ✅ Is every entry categorized clearly, avoiding vague terms like “Miscellaneous”?

- ✅ Did you include all small interest payments or micro-deposits?

- ✅ Are specific physical items that were already distributed noted in the report?

- ✅ Do you have a saved digital receipt or statement for every expense listed?

- ✅ Have you removed your own personal emotional commentary from the descriptions?

Communication Hygiene: Sending the Draft

How you present the final accounting is almost as important as the numbers themselves. Do not just attach a massive PDF to a blank email and hit send. Give the beneficiaries context, explain what they are looking at, and set clear expectations for the next steps.

Here is a polite, neutral script you can use when sharing the accounting draft for review.

Subject: Estate of [Name] – Draft Final Accounting for Your Review

Hello everyone,

As we near the final stages of the estate administration, I have prepared the draft final accounting. This document summarizes all the assets we started with, the income received, the final bills and administrative costs paid, and the current remaining balance available for distribution.

Please review the attached summary. If you have any specific questions about a line item, let me know and I can provide the supporting receipt or statement for clarity.

If everything looks correct to you, the next step will be to sign a standard receipt and release so we can process the final distributions.

Best regards,

[Your Name]

Using a script like this lowers the temperature. It shows that you are organized, transparent, and open to questions, which naturally reduces the likelihood of an aggressive confrontation and keeps the momentum moving toward a successful distribution.

Final Thoughts on Closing the Books

Building the final accounting is often the last heavy lift of the executor journey. It requires patience and a sharp eye for detail. However, if you treat it simply as a factual story of what happened, backed by solid evidence, it loses its intimidation factor.

It is also helpful to reframe how you view this document. The final accounting is not just a report card for the beneficiaries; it is your personal shield. Once this document is reviewed and the beneficiaries sign their receipts and releases, you are generally protected from future claims about how the money was handled. It is the vital step that allows you to step down from your role with a clean slate. Keep your records organized, communicate clearly, and use this document to officially close this chapter of your life.

❓ FAQ

🗣️ What does a final accounting look like in probate?

It typically looks like a structured financial summary document divided into four parts: starting estate value, income received during administration, expenses and debts paid, and the final remaining balance available to beneficiaries.

📄 Do I have to show every bank statement to beneficiaries?

Usually, you provide the summary report first. However, you must keep all bank statements and receipts organized in your files, because beneficiaries generally have the right to request proof of specific transactions.

🛑 Can beneficiaries waive the final accounting?

In many cases, if all beneficiaries agree and sign a formal waiver, a highly detailed formal accounting can be bypassed in favor of an informal summary. Always check local guidelines to see if this is allowed.

💸 What if the estate account earned interest but I didn’t track it month by month?

You will need to go back through the bank statements and add up all the interest earned, then list it as a single “Interest Earned” total line item in the Income section so the math balances perfectly.

⚠️ What happens if I make a mistake on the final accounting?

If you catch an honest math error or missing receipt, you typically just correct the draft and provide an updated version. If mistakes are hidden or intentional, it can lead to disputes and personal liability.

⏳ When should I send the final accounting report?

You generally send it only after all known debts are paid, taxes are cleared, and you are ready to make the final distributions to the heirs.

📅 How long do I need to keep these records after distribution?

While rules vary by location, it is generally recommended to keep the final accounting, signed receipts, and bank records for several years after closing. Check with a local professional for specific timelines.

📝 What if a beneficiary refuses to agree with the accounting?

If someone disputes the numbers and providing supporting receipts does not resolve it, the process may require formal court review where a judge evaluates the records. This is when local professional guidance is highly recommended.

🛋️ How do I list personal items on a probate accounting?

High-value items like art or jewelry are usually listed with their appraised value. Ordinary household items are often grouped together as a single estimated sum, unless beneficiaries request specific line-item tracking.

📫 How do I prove I sent the accounting?

It is best practice to send the document via certified mail with a return receipt requested, or via an email where the recipient acknowledges receipt in writing.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.