- A partial distribution estate strategy allows you to release some funds early, but it requires strict tracking to prevent future conflicts.

- Never drain the estate account; you must always maintain a documented reserve holdback to protect yourself from unexpected final bills and taxes.

- Every interim distribution must be treated as a documented advance on the final inheritance, linking the early payment directly to the final accounting.

- Proportional distributions to all equal beneficiaries help maintain peace and keep your bookkeeping manageable.

- If a beneficiary cashes an advance but ignores your request to sign a receipt, you must build a secondary paper trail using bank records or wire confirmations immediately.

The Pressure to Distribute Early: Why the Math Matters First

If you are managing an estate, there is a very predictable moment that happens somewhere around month six or seven. The initial shock has passed, the major assets might be consolidated, and the estate bank account is sitting there with a seemingly large balance. Predictably, your phone rings. A beneficiary wants to know if they can get a “small advance” or if an interim distribution estate payout is possible right now.

I completely understand the pressure executors feel in this moment. You want to be helpful. You want to show progress. And frankly, you want to stop answering questions about when the money is coming. In my day-to-day work supporting estate administration organization, this is one of the most critical crossroads an executor faces.

Making a partial distribution estate payout is not inherently wrong. In many cases, it is a very common and practical way to get funds to people who need them while you wait for a final tax clearance or a slow piece of real estate to sell. However, the fastest way to turn a calm administration process into a chaotic mess is to hand out money without a rigid, mathematical framework to back it up.

When you distribute some funds early, you are changing the baseline of your final accounting. You are no longer just dividing a pie at the end; you are handing out slices now and trying to remember exactly how big they were later. In this guide, I will walk you through how I approach the tracking, the communication, and the vital guardrails that keep partial distributions from causing disputes down the line.

When Are Partial Distributions Commonly Considered?

Before we look at the mechanics, it helps to understand why executors even bother with an interim distribution. If it adds paperwork, why not just wait until the very end?

Typically, there are a few practical scenarios where holding all the money hostage simply does not make sense. The most common pattern I see is the “stuck asset” scenario. Imagine you have successfully closed all the bank accounts and liquidated a brokerage account. You have a healthy cash balance. But, the estate also includes a piece of commercial property that is taking eight months to sell.

In a situation like that, the cash is just sitting there. The creditor period might be over, the known debts might be paid, but you cannot close the estate because of that one real estate transaction. This is a textbook environment where an executor might look at the numbers, calculate a safe reserve, and release a portion of the cash to the beneficiaries.

💡 Pro Tip: Another common trigger is the end of the year. Sometimes, passing income through to beneficiaries before tax season requires a partial distribution. Whenever taxes are the driver, that is your immediate signal to stop and speak with a tax professional before moving a single dollar.

The “Loud Beneficiary” Trap

While stuck assets are a good reason to distribute early, there is a bad reason that I see executors fall for constantly: the “loud beneficiary.”

This happens when one heir is experiencing personal financial trouble and heavily pressures the executor for an advance. The executor, wanting to relieve the tension, cuts a check to that one person, intending to “balance it out later.”

This almost always backfires. It creates an accounting headache, and more dangerously, if the other beneficiaries find out, it creates an immediate breakdown of trust. The core rule of this process is that every action must be defensible on paper. Responding to pressure with uncoordinated payouts is very hard to defend.

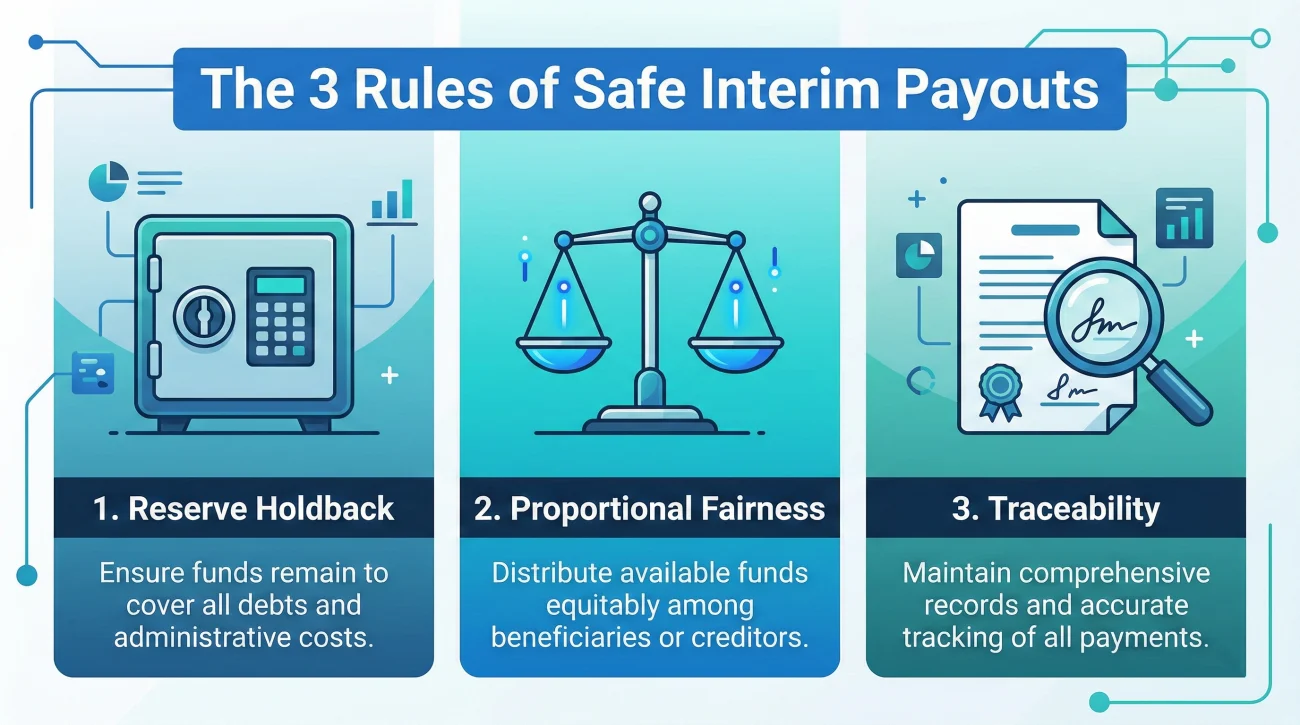

The Three Non-Negotiable Guardrails for Interim Distributions

If you decide that a partial inheritance distribution makes sense for the estate you are managing, you cannot simply guess at the amounts. You need a system. I always recommend establishing three specific guardrails before you even open your checkbook.

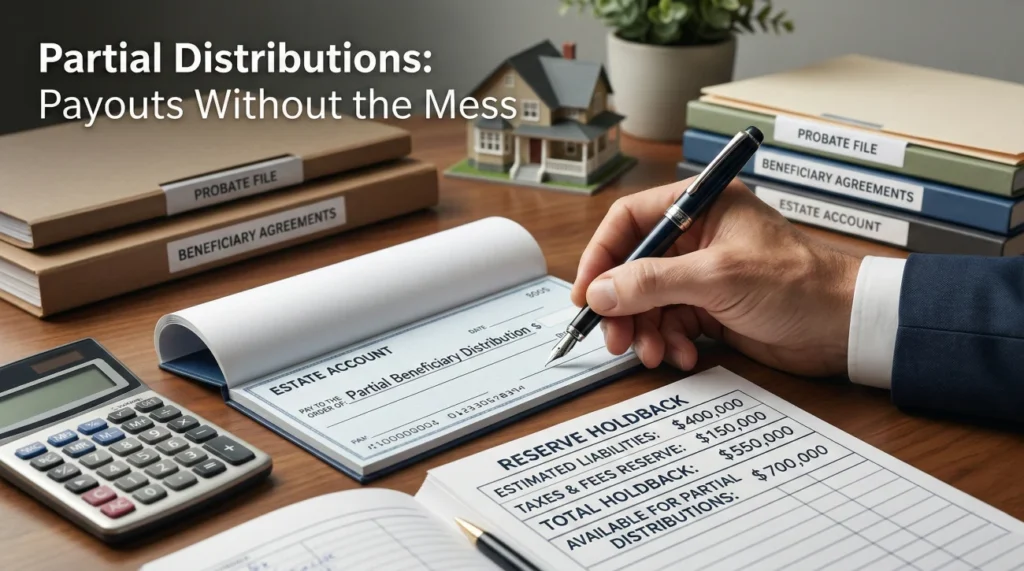

Guardrail 1: The Reserve Holdback

You can never distribute 100 percent of the funds before the estate is formally closed. There are always unknown, lingering costs. You might face a final tax preparation fee, a utility bill that arrived late, or administrative costs to close out final accounts.

The reserve holdback is a calculated buffer of cash that stays in the estate account no matter what. Executors often look at all known remaining expenses, add a comfortable cushion for surprises, and lock that money down. Only the cash sitting above that reserve line is ever considered for a partial distribution.

Guardrail 2: Proportional Fairness

If an estate is supposed to be split equally between three siblings, an interim distribution should also be split equally between those three siblings. Equality keeps the math clean and the emotions calm.

Giving Sibling A $10,000 because they asked, while giving Sibling B and C nothing, planning to deduct it from Sibling A’s final share next year.

Calculating that $30,000 can be safely distributed, and sending Sibling A, B, and C exactly $10,000 each on the exact same day.

By keeping it proportional, your bookkeeping remains incredibly simple. More importantly, you remove the psychological friction of siblings comparing timelines and wondering why one person was prioritized.

Guardrail 3: Traceability and Receipts

If you hand over money, you must be able to prove it later. An interim distribution is not a gift; it is a prepayment of an obligation. Therefore, you need the same level of documentation you would expect from a business transaction.

Key Point: A cashed check is a record of a transfer, but a signed receipt is a record of an agreement. You often need both to protect yourself at the finish line.

Tracking and Documentation: Building the Paper Trail

When I review workflow logs for estate organization, the biggest gaps usually happen right here. An executor will make a partial distribution but fail to write down the context. To avoid this missing document loop, you need to capture specific data points the exact same day you make the distribution.

Tracking Multiple Rounds of Distributions

In many estates, you might do two or even three rounds of partial distributions before closing. If you just list random check amounts in a notebook, you will be completely lost by round three. You need to maintain a “running total” or ledger for each beneficiary.

Here is an example of how executors visually track multiple phases to ensure no one is overpaid:

| Beneficiary | Estimated Total Share | Phase 1 Advance (Oct) | Phase 2 Advance (Jan) | Remaining Balance Est. |

|---|---|---|---|---|

| Sarah Jenkins | $100,000.00 | $20,000.00 | $15,000.00 | $65,000.00 |

| Mark Jenkins | $100,000.00 | $20,000.00 | $15,000.00 | $65,000.00 |

Whenever you write a check or initiate a wire transfer, the memo line is your first line of defense. Never leave a check or wire memo blank, and avoid vague words like “inheritance.”

The Uncooperative Beneficiary: What if they refuse to sign?

This is a blind spot many executors hit. You mail the payment and the receipt form. The beneficiary cashes the check immediately, but they never mail the signed receipt back. You email them; they ignore it.

If you face this, you must act to protect yourself. You cannot force them to sign, but you can build a secondary paper trail. First, log into the estate bank account and download the scanned image of the front and back of the cleared check showing their endorsement. If you used a wire transfer instead of a check, download the official bank wire confirmation PDF showing the completed transaction and the destination account. Save this directly into your estate folder. Second, send a polite, timestamped email or a certified letter stating: “This confirms the $15,000 Phase 1 advance was processed and cleared on [Date]. This amount will be deducted from your final accounting share.”

You have now documented the transfer, their acceptance of the funds, and your clear communication of the terms, even without their signature.

Handling In-Kind Advances: The Personal Property Trap

Distributing money is straightforward because a dollar is always worth a dollar. But often, beneficiaries want physical items early. A sibling might ask to take possession of a vehicle, a valuable piece of jewelry, or a collection before the estate is closed.

Giving someone an asset instead of cash is called an “in-kind distribution.” It functions exactly like a cash advance, but it introduces a massive risk: valuation disagreements.

If you allow Sibling A to take a vehicle today, you must deduct the value of that vehicle from their final inheritance. But who decides what it is worth? If you just guess the value is $5,000, Sibling B might later claim it was worth $12,000 and accuse you of shortchanging the estate.

Before any physical item leaves the estate early, you must have a documented appraisal or a written agreement from all beneficiaries agreeing to the specific dollar value being assigned to that item. If the beneficiaries cannot agree on the value of the car, do not distribute it. Your default action in a dispute over value is to keep the item in the estate until it is formally sold or the administration finishes.

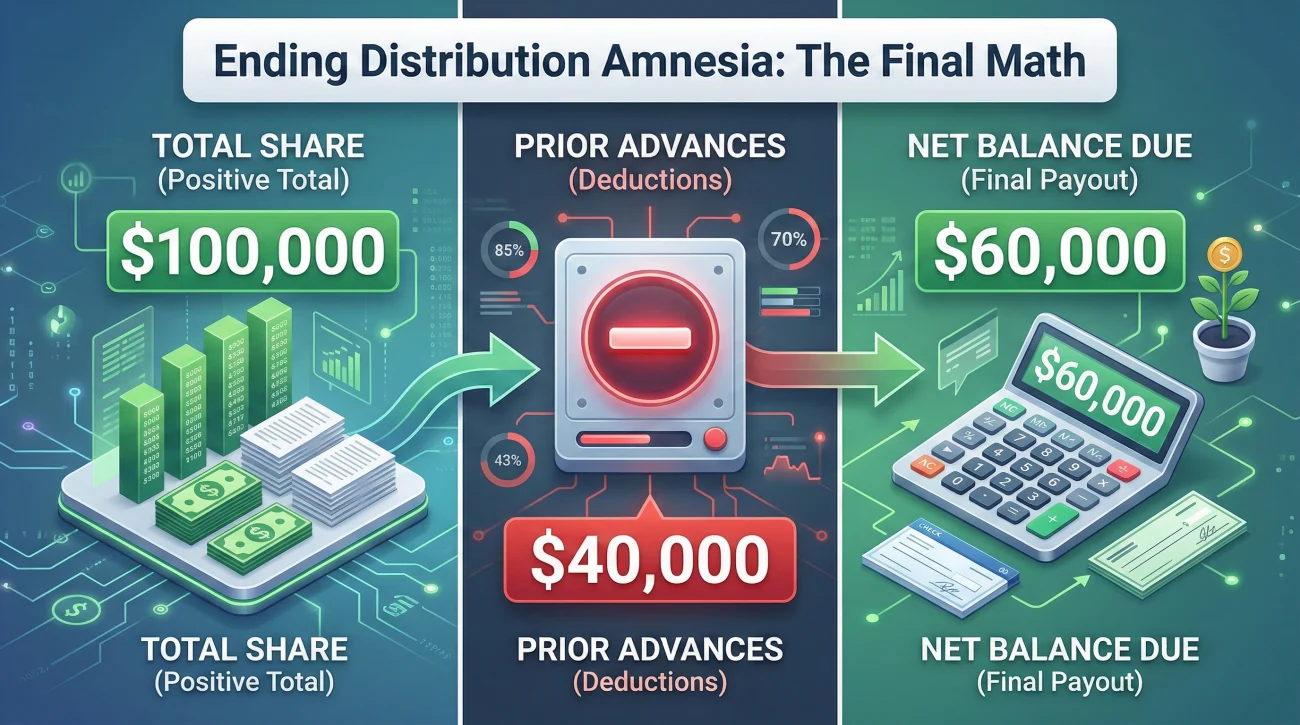

How Partial Distributions Interact with Final Accounting

The main reason we focus on tracking ledgers and receipts is for the very end of your job. When you use an Estate Distribution Checklist to close things out, you will have to present a final accounting.

In my experience, beneficiaries often suffer from “distribution amnesia.” If you gave them $20,000 nine months ago, and today you are showing them a final balance check of $10,000, their immediate reaction is often confusion about why their share is so small.

Your documentation is the bridge here. Your final accounting report should clearly list the total gross share they were entitled to. Directly underneath that, create a line item that explicitly subtracts the interim distribution they already received (referencing the exact date and check or wire number). Finally, show the remaining net balance due today. When your math is transparent and points directly to their own past withdrawals, disputes usually evaporate before they can even begin.

Communication Hygiene: Navigating Expectations and Hardships

Handling the math is only half the battle. Handling the people is the other half. The way you communicate a partial inheritance distribution sets the tone for the rest of the administration.

You need to be neutral, clear, and focused on process. You will occasionally deal with a beneficiary who is facing true financial hardship, such as medical bills or eviction, who begs for an exception. While sympathetic, you cannot risk the estate. You must maintain boundaries.

Script: Saying “Not Yet”

If the estate is not ready, you need a polite way to shut down general requests without sounding adversarial.

“I completely understand this is a difficult time and you are looking for an update on the timeline. Right now, the estate is still in the required holding period for creditor claims. Once that window closes and the final tax reserve is calculated, I will review the balances to see if an interim distribution is safe for everyone. I will send a status update in writing next month.”

Script: Denying a Hardship Advance

When a beneficiary pleads for early funds to cover a personal emergency, saying no is incredibly difficult. However, your fiduciary duty is to the estate, not to their personal financial situation. You must keep the boundary firm while remaining empathetic.

“I am so sorry to hear about the medical situation, and I completely understand why you are asking for an advance right now. Unfortunately, as the executor, I am legally bound by the probate process to hold all estate funds until the final creditor period closes and taxes are assessed. I cannot make any exceptions to release funds early without putting the estate at risk. I will notify everyone the moment the reserve calculations are cleared and it is safe to distribute.”

Script: Announcing a Partial Distribution

If you have run the numbers and are ready to send out funds, communicate the plan to everyone simultaneously. Do not surprise them with a check in the mail.

Subject: Update: Interim Distribution and Next Steps

Hello everyone,

I am writing to provide an update on the estate administration. We have cleared the major initial expenses and have established a safe reserve for remaining administrative costs and final taxes.

Because the sale of the house is still pending, I am issuing a proportional interim distribution to all beneficiaries this week. This is an advance on your final share.

You will each receive a payment for [Amount]. Included with this notice is a standard receipt form. Please sign and return the receipt so I can log it properly for the final accounting records.

I will provide another status update once the real estate transaction moves forward.

Best regards,

[Your Name]

This script works because it relies on a proven formula:

[Action being taken] + [Why the reserve exists] + [What you need in writing]

The Biggest Practical Risk: Miscalculating the Reserve

Over the years, looking at how executors track their workflows, the most dangerous situation usually comes from a single misstep regarding the reserve holdback.

Mistake: Underestimating the Reserve (The Surprise Bill)

Let us say you hold back $10,000 for final expenses and distribute the rest to the beneficiaries. Two months later, a complex tax filing results in a $15,000 bill from the IRS, or a late but valid creditor claim surfaces. The estate account is now short by $5,000.

If the money is already gone, you, as the executor, must ask the beneficiaries to give some of the money back. This is known as a clawback. Beneficiaries almost universally hate clawbacks, and some may have already spent the money and simply refuse to return it.

If you cannot recover the funds from the beneficiaries to pay a valid estate debt or tax obligation, the liability does not just disappear. In many situations, the executor can be held personally liable for the shortfall because they distributed assets before satisfying the estate’s debts. This is exactly why you must always build a heavily padded reserve and why you should never distribute down to zero until you are absolutely certain no other bills exist.

❌ Note: Never use your personal bank account to facilitate a distribution or to cover a shortfall. Always transfer funds directly from the official estate checking account to the beneficiary. Mixing estate money with personal funds destroys your traceability and can be viewed as highly improper.

Final Thoughts on Keeping the Board Clear

Managing a partial distribution estate payout is a balancing act between being helpful to the beneficiaries and being protective of yourself. As an executor, your primary duty is to safeguard the estate and execute the final instructions cleanly. You are never obligated to put yourself at risk just because someone is impatient.

If you take the time to calculate a conservative holdback reserve, treat all equal beneficiaries fairly, and demand clear, written receipts for every dollar that leaves the account, you can successfully navigate an interim distribution. It takes a little more paperwork up front, but it guarantees a much smoother, quieter finish line. Your ultimate goal is to close this chapter cleanly, and a well-documented paper trail is the best tool you have to protect your peace of mind.

❓ FAQ

🛑 Can an executor make a partial distribution before probate is closed?

Yes, in many cases, executors can release some funds before the final closure. However, this is typically only done after known debts are paid, the creditor claim period has expired, and a safe reserve is held back for final taxes and administrative costs.

⚖️ Do I have to give everyone a partial inheritance distribution at the same time?

Generally, yes. If beneficiaries are entitled to equal shares, partial distributions should be made equally and proportionally. Distributing to one person and not others creates accounting complications and often triggers severe disputes.

🏦 What should I write on the memo line of the check or wire transfer?

You should be specific. Avoid vague terms like “gift.” Instead, write something clear like “Interim Distribution 1” or “Partial Advance on Final Share.” This creates a clear paper trail for your final accounting.

📝 Do I need beneficiaries to sign a receipt for an interim distribution?

Yes, always. You must collect a written acknowledgment or receipt confirming they received the funds and understand it is an advance against their final share. This protects you during the final accounting phase.

🛡️ How much should I hold back in the estate reserve?

The reserve must cover all known unpaid bills, estimated final taxes, professional fees (like accounting or legal help), and a comfortable buffer for unexpected late claims. You should never distribute down to a zero balance early.

📉 Will a partial distribution complicate the final accounting?

It adds an extra step, but it is manageable if tracked properly. In the final accounting, you simply show the total gross share the beneficiary was entitled to, subtract the documented partial distribution they already received, and show the remaining net balance due.

🗣️ What if one person demands their share early and others do not?

You should not yield to pressure. If you determine an interim distribution is safe, you should calculate a proportional amount for everyone. If the estate is not ready, you must politely decline the request in writing, citing the need to hold funds for debts and taxes.

💸 Can we distribute personal property early instead of cash?

Yes, distributing a physical item is considered an in-kind distribution. However, you must establish and document an agreed-upon dollar value for that item before handing it over, so its value can be correctly deducted from their overall share.

📑 Does the court need to approve an interim distribution?

This depends entirely on local rules and whether you are operating under independent or dependent administration. Often, independent executors have the authority to do this, but you should always verify the requirement with local professionals before moving money.

🔄 Can I make more than one partial distribution?

Yes, it is common to do this in phases. For example, you might make a first distribution after the house sells, and a second one after a tax return is accepted, holding only a tiny reserve at the very end. The key is consistent, rigid documentation for every phase.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.