- Distributing an estate is not a single event; it is a multi-phase process of readiness, accounting, payout, and documentation.

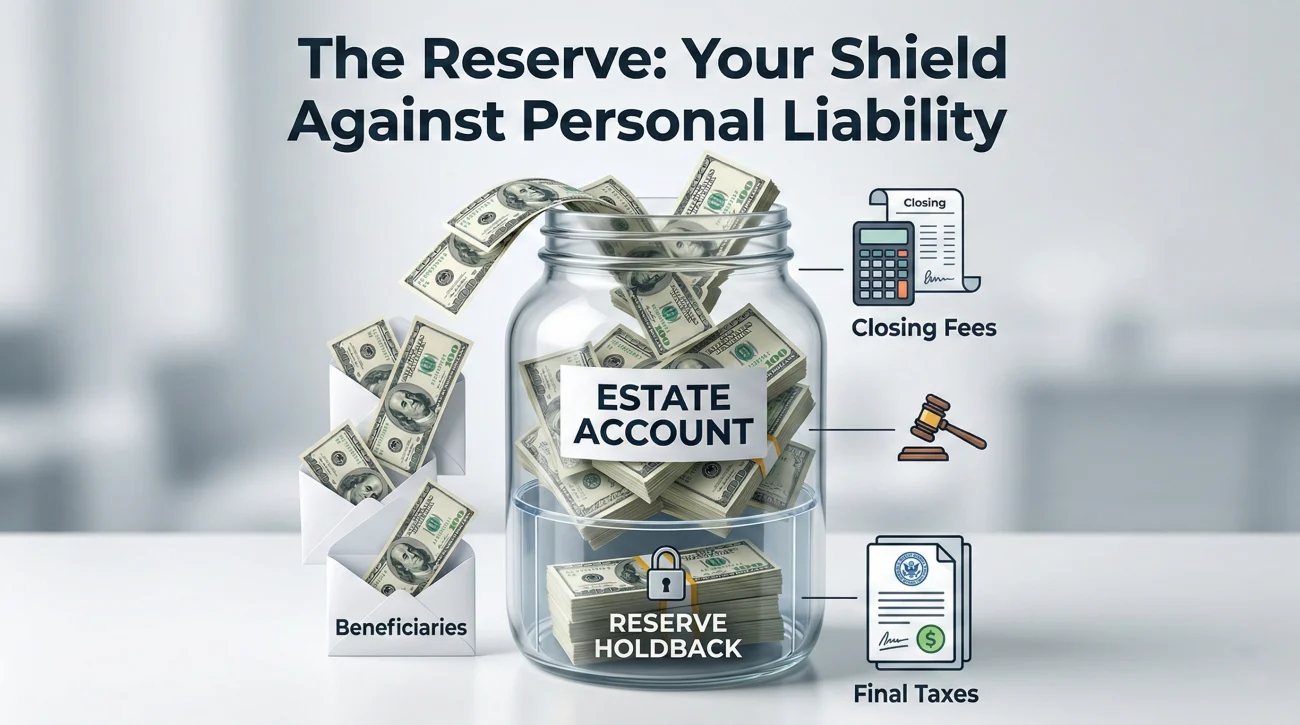

- Never distribute funds down to zero. Always calculate a reserve holdback for unexpected final bills, delayed taxes, or late administrative costs.

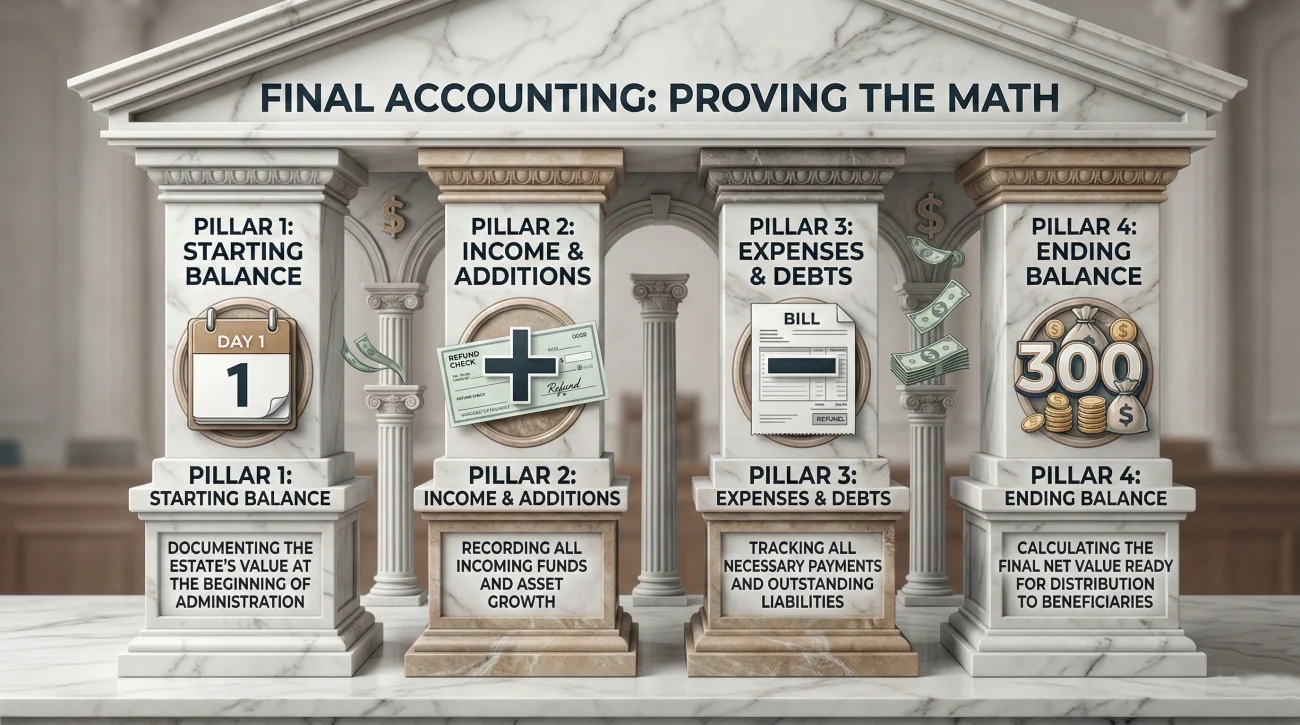

- A final accounting is simply the financial story of the estate in numbers, showing exactly what came in, what went out, and what is left for distribution.

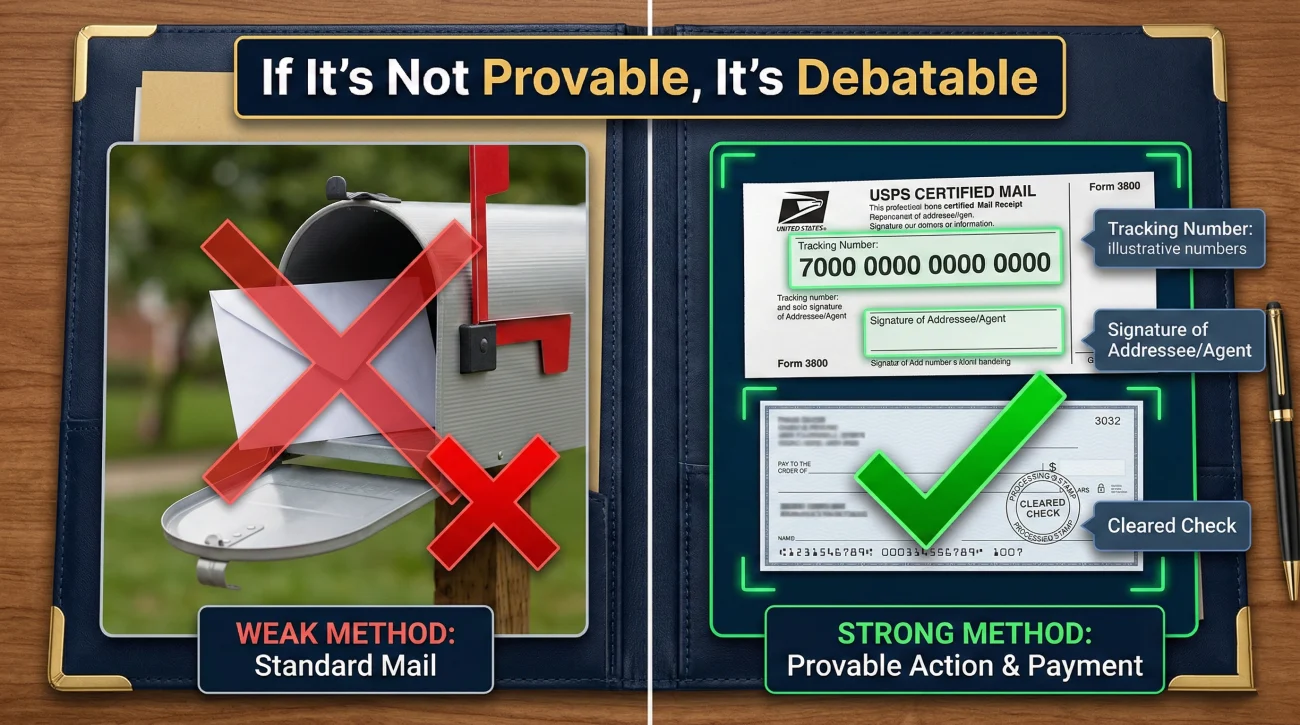

- If a distribution is not provable, it is debatable. Always collect receipts, written releases, and tracking confirmations before closing your files.

- Consistent, neutral communication with beneficiaries prevents the vast majority of end-of-process disputes and suspicions.

Reaching the Finish Line Without Stumbling

In my years of experience supporting estate administration workflows and helping executors untangle messy files, the final stretch is often where executors feel the most pressure. You have spent months gathering assets, paying creditors, and organizing paperwork. Now, the beneficiaries are asking when they will receive their share, and the temptation to simply write checks and walk away is incredibly high. I see this exact scenario play out constantly.

However, closing an estate cleanly requires a disciplined approach. An estate distribution checklist is not just a list of people to pay; it is a defensive framework. It ensures you do not pay out money prematurely, leaving yourself personally exposed to a forgotten tax bill or a late creditor claim. It also ensures you build a bulletproof paper trail so that no one can question your actions years down the line.

Key Point: Most executor stress happens at the finish line because the desire to be done clashes with the necessity of being thorough. Pace yourself, document everything, and rely on a structured process rather than rushing the final payouts.

This guide serves as your universal map for the final phases of estate administration. Because local regulations, specific court procedures, and tax thresholds vary wildly, I will not give you state-specific legal advice or tax instructions. Instead, I will walk you through the operational habits, the communication strategies, and the documentation workflows that seasoned administrators use to safely close an estate.

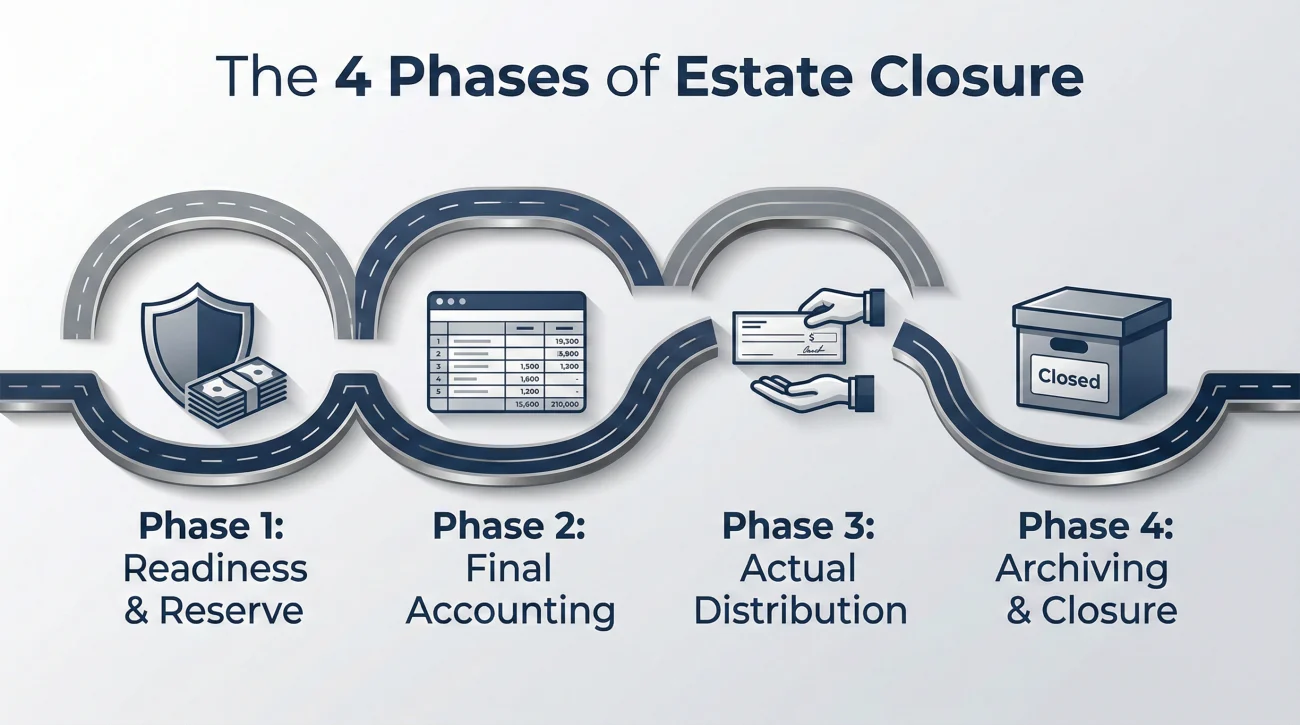

The Four Phases of Estate Closure

One of the most common mistakes I see executors make is viewing distribution as step one of the closing process. In reality, handing over assets is step three. When you skip the foundational work, you invite confusion, disputes, and potential liability. To keep things organized, I always recommend breaking the finish line into four distinct operational phases.

- ✅ Phase 1: Readiness and the Reserve. Confirming that all incoming money is collected, all known debts are resolved, and a safety buffer is calculated before a single dollar moves to a beneficiary.

- 📄 Phase 2: The Final Accounting. Translating months of bank statements and receipts into a readable, clear summary that proves the math is fair and accurate.

- 💸 Phase 3: The Actual Distribution. Executing the transfer of cash, personal items, or real property, while collecting the mandatory proof of delivery.

- 🗄️ Phase 4: Archiving and Closure. Organizing the final packet of records, confirming bank account closures, and safely storing the history of the estate.

If you try to execute Phase 3 while you are still dealing with Phase 1, the paperwork gets tangled. Beneficiaries become confused because the numbers keep changing, and you end up doing twice the work to explain the discrepancies. Stick to the sequence.

Phase 1: The Distribution Readiness Checklist

Before you even draft a distribution plan, you must pass the readiness gate. I call this the “snapshot moment.” You need to look at the estate and confidently say that the financial picture is stable and highly unlikely to change. If you still have pending lawsuits, unsold real estate with ongoing maintenance costs, or unresolved tax returns, the estate is usually not ready for a full final distribution.

When I review files that have gone off track, it is almost always because the executor distributed funds before clearing these three fundamental hurdles.

Clearing the Creditor and Tax Lanes

The first hurdle is confirming that the estate’s obligations are handled. As an executor, your primary duty is to the estate’s valid creditors and the tax authorities, not the beneficiaries. Money only flows to the heirs after the required debts are settled.

You need documented proof that you have researched, validated, and paid (or formally rejected) creditor claims according to your local guidelines. Similarly, you must ensure that final income taxes and any potential estate taxes are accounted for. For general educational background on how the federal government views estate tax responsibilities, you can review the IRS official overview on estate taxes. Knowing the broad concepts helps you ask your local tax professional the right questions.

You think all the hospital bills are paid because you have not received mail in a month, so you start writing distribution checks to the heirs.

You maintain a master log of all known creditors, mark each one as “Paid in Full” with a corresponding date and check number, and consult with a tax preparer to confirm no further returns are due before planning any payouts.

Finalizing the Asset Inventory

The second hurdle is the asset list. You cannot distribute what you have not fully defined. Every bank account must be consolidated, every physical asset must be appraised or assigned a documented value, and every final dividend or refund check must be deposited.

I often see executors forget about utility deposit refunds or trailing insurance reimbursements. Wait until the dust settles on the administrative accounts. Ensure your master inventory list is complete and matches the current balance of the estate checking account.

📌 Note: Do not attempt a final distribution if you are still waiting on a house to close escrow or a vehicle to be sold. The transaction costs, agent fees, and surprise repairs will inevitably change your final numbers.

Once you have cleared these two hurdles, the third and most operationally critical step of Phase 1 is sizing your reserve holdback.

The Reserve Holdback: Why You Never Distribute to Zero

If there is one piece of operational advice I emphasize above all else, it is this: never, ever drain the estate account to zero during the initial distribution phase. You must calculate and hold back a reserve fund. A reserve is a specific amount of money kept safely in the estate account to cover unexpected final costs.

Why is this so critical? Because estates have a habit of generating surprise expenses at the very end. You might receive a final invoice from an accountant, a bill for closing a storage unit, or a minor tax adjustment. If you have already distributed all the money to the beneficiaries, you will find yourself in the uncomfortable position of asking them to return a portion of their inheritance to cover these bills. In my experience, clawing back money is extremely difficult and heavily damages trust.

How to Conceptually Size a Reserve

While I cannot give you a specific dollar amount or percentage (as every estate is different), executors commonly build their holdback buffer by estimating:

- Pending professional fees (CPA, legal advisor, appraiser final invoices).

- Administrative closing costs (final bank fees, mailing costs, recording fees).

- A buffer for unexpected tax liabilities or late-arriving minor claims.

Once the final administrative tasks are entirely complete and all professionals are paid, this reserve is simply distributed to the beneficiaries in a small, final “true-up” payout.

Communicating the Holdback

Beneficiaries often misunderstand the reserve. If you do not explain it clearly, they may assume you are hiding money or paying yourself secretly. Transparency is your best tool here.

Subject: Estate Update: Upcoming Initial Distribution and Reserve Fund

Hello everyone,

I am writing to provide an update on the estate distribution. We have cleared the major expenses and are preparing for the primary distribution phase.

To ensure the estate remains safe from any final administrative costs (such as the final tax preparation fee and closing account fees), I will be holding back a reserve of [Amount] in the estate account.

The remaining balance of [Amount] will be distributed according to the will/estate plan next week. Once the final administrative tasks are fully closed out and the CPA confirms we are clear, the unused portion of this reserve will be distributed to you in a final payout.

Please let me know if you have any questions.

Best regards,

[Your Name]

Notice how calm and structural that script is. It sets a clear boundary, walks them through the reasoning, and reassures them that any leftover money will still come to them.

Phase 2: Final Accounting in Plain English

Before any distribution checks are written, you must show your math. A final accounting is simply a comprehensive summary that tells the financial story of the estate from the day you took over to the present moment. It proves to the beneficiaries that every dollar is accounted for.

I cannot stress enough how many conflicts are prevented by a clean, readable accounting. When beneficiaries suspect mismanagement, it is rarely because the executor actually stole money; it is almost always because the executor handed over a confusing pile of receipts instead of a clear summary.

The Core Components of an Accounting

While local courts may have specific forms if you are navigating a formal court process, the universal operational structure of an accounting always includes four basic pillars:

| Accounting Component | What It Represents (Plain English) |

|---|---|

| 1. Starting Balance / Inventory | The exact value of all estate assets on the day you officially took control. This is your baseline. |

| 2. Income and Additions | Any new money that came in during your administration (e.g., interest, refunds, sale of a car for more than the estimated value). |

| 3. Expenses and Debts Paid | Every dollar spent to settle debts, maintain property, pay taxes, or cover administrative costs. (This is also where any transparent, documented executor compensation must be listed; never take a fee secretly without recording it here.) |

| 4. Ending Balance / On Hand | The remaining assets currently sitting in the estate, which represents the amount available for the reserve and final distribution. |

The golden rule of an accounting is traceability. If a beneficiary points to a line item that says “House preparation expenses: $4,000,” you must be able to open a folder and produce the exact invoices and canceled checks that equal $4,000. Keep your categories broad enough to be readable, but specific enough to be transparent.

Phase 3: Distribution Methods and Complex Assets

Once the accounting is drafted and approved (or at least shared and unquestioned), you move to the actual distribution. In my day-to-day admin work, I see executors struggle primarily with the method of distribution, specifically choosing between cash, transferring real property, or handing out physical items.

Each method carries a different operational burden. Understanding these tradeoffs helps you plan your paperwork accordingly.

Cash Distributions

Liquidating assets and distributing pure cash is operationally the cleanest method. The math is undeniable. If three people share an estate equally, dividing a $90,000 bank balance into three $30,000 checks leaves no room for debate about who got a better deal. The primary documentation required is a simple receipt confirming the funds were deposited.

In-Kind Distributions (Personal Property)

Distributing items “in-kind” means handing over the actual asset, like a vehicle, a piece of jewelry, or a collection of tools, instead of selling it. This is where emotions often override logic. The difficulty here is valuation. If one sibling takes a vintage watch and another takes a collection of silver coins, they must agree on the documented value of those items so it can be deducted from their overall share of the estate fairly.

💡 Pro Tip: Never distribute significant personal property without a written agreement on its value. If beneficiaries cannot agree on a value, the safest operational path is often to sell the item on the open market and distribute the resulting cash, completely removing personal bias from the equation.

Real Property Transfers

Distributing a house is rarely as simple as handing over the keys. You must decide whether to transfer the title directly to the heirs or sell the property and distribute the cash. Selling often creates the cleanest math, but if heirs want to keep the home, you must meticulously document how the transfer affects their overall share, especially if one beneficiary is taking the house while others take cash. The paperwork burden shifts heavily to deeds, title companies, and closing costs.

Digital Assets, Minors, and Missing Heirs

Modern estates are full of edge cases that can stall a distribution. If you are dealing with digital assets (like cryptocurrency wallets or monetized accounts), they must be valued and transferred through the platform’s specific protocols, not just by sharing passwords. Furthermore, if a beneficiary is a minor, or if an heir is completely missing, you generally cannot distribute funds directly. You will almost always need local legal guidance to set up a protective trust or a court-supervised holding account.

The Concept of Partial Distributions

Sometimes, an estate administration drags on for a year or more due to real estate sales or complex taxes. In these cases, executors may consider a partial (or interim) distribution. This means handing out a portion of the inheritance early, while keeping a massive reserve to cover the remaining unresolved issues.

If you choose this route, extreme recordkeeping discipline is mandatory. You must carefully log every partial payment so that when it comes time for the final accounting, the early payouts are accurately subtracted from each beneficiary’s final total. A simple formula to keep in mind for your logs is:

Phase 3 Continued: Receipts, Releases, and Proof of Delivery

Handing over a check or a set of house keys is not the end of a transaction. The transaction is only complete when you have written proof that the beneficiary received it and accepts it as their proper share. I cannot overstate the importance of this paperwork.

A “receipt and release” is a common concept in estate administration. While the exact legal phrasing depends heavily on your local jurisdiction and you should consult a professional for drafting formal documents, the operational goal is always twofold:

- The Receipt: A signed acknowledgment that the beneficiary physically received specific assets or a specific amount of money on a specific date.

- The Release: A broad acknowledgment that the beneficiary has reviewed the final accounting, agrees with the math, accepts the distribution as their full entitlement (or partial, if an interim payout), and agrees not to hold the executor liable for future claims regarding those funds.

Without proof of delivery, a beneficiary could claim a year later that a check was lost in the mail or that they never received the family heirlooms. Do not rely on verbal thank-yous. Do not rely on text messages with a thumbs-up emoji. Use formal, traceable documentation.

Mailing a $10,000 check via standard mail and assuming it arrived because the bank balance dropped.

Sending the check via certified mail with a tracking number, requiring a signature upon delivery, and keeping a copy of the signed receipt alongside the cleared bank image in your estate folder.

Common Dispute Triggers at the End

In my line of work, I see a pattern: the most aggressive beneficiary disputes do not happen at the beginning of the estate process; they happen right at the distribution phase. They are almost always triggered by poor communication hygiene, not actual theft.

When an executor goes silent for three months while trying to figure out a complex tax return, the beneficiaries sitting in the dark start to imagine the worst. They assume the executor is hiding money. By the time the distribution check arrives, they are already angry and ready to scrutinize every penny.

Maintaining Communication Hygiene

The easiest way to prevent finish-line disputes is to proactively narrate your progress. You do not need to send daily updates, but a brief, factual monthly email keeps the temperature low.

Subject: Estate Status Update: [Month]

Hello,

I want to provide a quick update on the estate administration.

This past month, I successfully closed the final utility accounts for the house and received the tax clearance letter from the accountant.

Our next steps are to finalize the formal accounting spreadsheet and prepare the receipt documents. I anticipate having the accounting draft ready for your review by [Date].

I will send another update when the documents are ready. Thank you for your continued patience as we finalize these administrative steps.

Best regards,

[Your Name]

If someone challenges your distribution math or demands an item that another beneficiary wants, do not engage in emotional text battles. Revert to your documentation. “Here is the professional appraisal for the item,” or “Here is the spreadsheet showing exactly how the cash was divided.” Keep it structural.

Phase 4: Closing the Estate and Archiving Records

When the communication is clean and the receipts are signed, you are finally ready to move into the last phase: closing the doors. Now that the distributions are completed and the checks have cleared, your final task is purely administrative. I call this building the “peace of mind packet.”

The goal is to create a single, unified file (both physical and digital) that contains the complete history of the estate. If a beneficiary asks a question three years from now, or if a tax agency sends an inquiry, you should not have to dig through your garage. You simply open this packet.

What to Keep in Your Final Packet

- A copy of the formal Final Accounting spreadsheet.

- All signed Receipts and Releases from the beneficiaries.

- The final bank statement showing a $0.00 balance and an official “Account Closed” confirmation letter from the bank.

- The master debt log, including proof of payment for all settled claims.

- Copies of all filed tax returns and clearance letters.

For a complete breakdown of how to transition from active administration to permanent archiving, you should review our comprehensive guide on estate distribution and closing procedures. It ties the entire lifecycle of your administrative duties into a tidy, manageable conclusion.

Final Thoughts on Crossing the Finish Line

Administering an estate is an exhausting marathon of paperwork, phone calls, and emotional management. When you reach the distribution phase, it is entirely normal to feel fatigued. However, this is the exact moment when you must lean heavily on your processes. Do not cut corners to save a few days. Calculate your reserve, draft a clear accounting, demand signed receipts, and keep your communication strictly neutral. By treating the final payout as a structured operational phase rather than a casual handover, you protect yourself from liability and ensure that the legacy you are managing is resolved cleanly, quietly, and completely.

“Closing an estate is not marked by a grand ceremony; it is marked by receiving a bank statement that reads zero and placing the final signed receipt into a well-organized folder.”

Deep Dive: The Distribution Library

If you need more specific guidance on any single step mentioned above, I have built a cluster of deep-dive guides. Think of this table as your extended reference library. Instead of repeating all the details here, these links will take you to focused, step-by-step frameworks for specific challenges, such as dealing with a missing heir or figuring out exactly what proof of delivery looks like.

| Topic / Guide Title | What You Will Learn |

|---|---|

| Distribution Readiness Checklist: What to Clear Before Money Moves | The specific gates you must pass (debts, taxes, inventory) before safely distributing funds. |

| Final Accounting for Executors: What It Includes and How to Keep It Readable | How to structure the estate’s financial story into a clear, unquestionable summary. |

| Receipts and Releases: Why Executors Collect Them Before Closing | The purpose behind these documents and how they act as your final shield against liability. |

| Estate Reserve Holdback: How Executors Decide What to Keep Back (Concept Map) | How to logically size your safety buffer and explain it to impatient beneficiaries. |

| Partial Distributions: How Executors Do It Without Creating a Mess | The frameworks for handing out money early while keeping the final math perfectly traceable. |

| Cash vs In-Kind Distribution: The Tradeoffs Executors Explain to Beneficiaries | Navigating the friction between selling everything for cash versus handing over physical items. |

| Distributing Personal Property: A Simple, Low-Drama Process (Concepts Only) | Documented pathways for dividing household items when sentimental value is high. |

| Real Property Distribution: Transfer to Heirs or Sell, and What Changes at Closing | The decision map for dealing with a house, tracking valuations, and closing costs. |

| Missing Beneficiary or Heir: How Executors Handle Distribution When Someone Cannot Be Found | Risk awareness and documentation rules when a beneficiary vanishes from the grid. |

| Distribution to Minors or Protected Beneficiaries: Why It Usually Cannot Be Handed Over Directly | Why direct payments are restricted and the high-level pathways used to protect the funds. |

| Preventing Beneficiary Disputes at Distribution: The Paper Trail That Keeps Things Calm | Communication strategies and summary reports that stop accusations before they start. |

| Closing the Estate: The Final Packet Executors Keep for Peace of Mind | The exact records and confirmations you need to box up and save for the future. |

| Proof of Distribution Checklist: How Executors Show What Was Delivered | Actionable ways to label and track payments so they perfectly match your accounting. |

| Closing the Estate Bank Account at the End: What Changes After Final Distributions | What to capture before the bank shuts down the account and access is lost. |

| Executor Compensation: How It’s Commonly Handled (Without Numbers or State Rules) | General models for addressing the executor’s fee transparently at the finish line. |

Sources and Educational Reading

I rely on a few trusted, authoritative sources when guiding executors through the administrative maze. Below are the foundational resources that inform the frameworks in this guide:

- 📄 IRS.gov: Overview of Estate Tax Responsibilities

I always point executors here first when tax questions arise. While it does not replace a CPA, this page provides the official federal thresholds. It helps you quickly understand if the estate is large enough to trigger federal tax complications before you start writing distribution checks. - 📄 American Bar Association (ABA): The Probate Process Overview

The ABA offers a neutral, highly reliable breakdown of the probate timeline. I included this because reading their consumer guide gives you a solid grasp of the legal vocabulary, making your conversations with local attorneys much more efficient and less intimidating.

❓ FAQ

📋 What is an estate distribution checklist?

It is an operational roadmap that ensures an executor has paid all debts, filed taxes, and secured a reserve fund before transferring any remaining assets or money to the beneficiaries.

⏱️ How long does an executor have to distribute funds?

There is no single universal timeline. Distribution typically only happens after the creditor claim period ends, all taxes are filed, and assets are fully liquidated. Rushing this timeline increases personal liability for the executor.

🚪 Can an executor distribute assets before probate is closed?

In many cases, partial distributions are allowed before full closure, provided the executor keeps a large enough reserve holdback to cover all remaining debts, taxes, and final administrative fees.

💸 What happens if an executor distributes money too early?

If the executor drains the estate account and a surprise tax bill or valid creditor claim arrives later, the executor is often held personally responsible for paying that debt if they cannot recover the funds from the beneficiaries.

🏦 Do I have to show beneficiaries the bank statements?

While handing over raw bank statements is not always mandatory, you must provide a Final Accounting (a clear, readable summary of all income and expenses) so they can verify the math before receiving their share.

📦 How do I prove I sent the inheritance?

Always use traceable methods. Require beneficiaries to sign a formal Receipt and Release document, use certified mail for physical checks, and keep copies of cleared checks from the estate bank account.

🖋️ What if a beneficiary refuses to sign a receipt?

If a beneficiary refuses to sign a receipt or release, the executor should pause the distribution to that individual and seek local professional guidance, as handing over funds without proof is a massive administrative risk.

🛡️ Why do executors hold back money at the end?

It acts as a safety buffer for final accountant fees, account closing costs, and unexpected minor claims, ensuring the executor does not have to pay out of pocket.

⚖️ Can I pay myself an executor fee before distributing?

Compensation must be transparent. It is typically calculated and paid out near the end of the process as an administrative expense, explicitly listed on the Final Accounting, and often requires beneficiary agreement or court approval.

🧑⚖️ Do I need an attorney to close the estate?

While simple estates can sometimes be closed without one, consulting an attorney at the finish line ensures your final accounting is formatted correctly and your receipt documents legally protect you from future liability.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.