- An estate reserve holdback is a calculated safety buffer of funds kept in the main estate account to cover final taxes, delayed bills, and closing administrative costs.

- Executors must actively plan for “ghost bills,” such as delayed medical invoices or forgotten digital subscriptions, to avoid paying out of pocket.

- A partial distribution can safely relieve pressure from eager beneficiaries, provided it is not used during active disputes, unresolved Medicaid claims, or complex tax audits, and a padded holdback is retained first.

- Releasing the holdback is a strictly sequenced process, requiring final tax clearances and signed beneficiary releases before the very last checks are written.

The Hidden Pressure of the Finish Line

In my experience supporting estate administration workflows, the heaviest pressure on an executor rarely happens at the very beginning when everyone is still grieving. The hardest part usually arrives right near the end, when the house is sold, the major accounts are gathered, and the beneficiaries know there is a pool of cash sitting in the estate bank account.

This is the exact moment when the emails and phone calls multiply. People want closure, and naturally, they want their inheritance. The temptation to simply write the final checks, zero out the account, and walk away is overwhelming. But distributing everything before you are absolutely certain all final expenses are cleared is one of the most dangerous administrative traps you can fall into.

I recently reviewed a case where an executor distributed everything shortly after the deceased’s house was sold. Eight months later, a specialized medical transport invoice arrived in the mail. The transport company had spent months fighting Medicare, failed to get coverage, and finally billed the estate. Because the estate account was already empty and closed, the executor had to pay that significant invoice from his own personal checking account when the beneficiaries stopped returning his calls.

This is where the estate reserve holdback becomes your most critical tool. It is a deliberate, documented buffer of funds retained in the estate account to handle the final, lingering costs of closing out a life. In this guide, I will walk you through how seasoned operators calculate this holdback, how to safely navigate partial distributions, and the sequence for safely releasing the funds when the job is truly done.

What Is an Estate Reserve Holdback?

An estate reserve holdback is a portion of the estate’s liquid cash that the executor deliberately shields from distribution until the estate is formally and safely closed. It is important to note the difference between an internal holdback and a formal escrow account. You do not typically need to open a separate, third-party escrow account for this; a holdback is simply tracked as an internal administrative line item while sitting safely within the main estate checking or savings account.

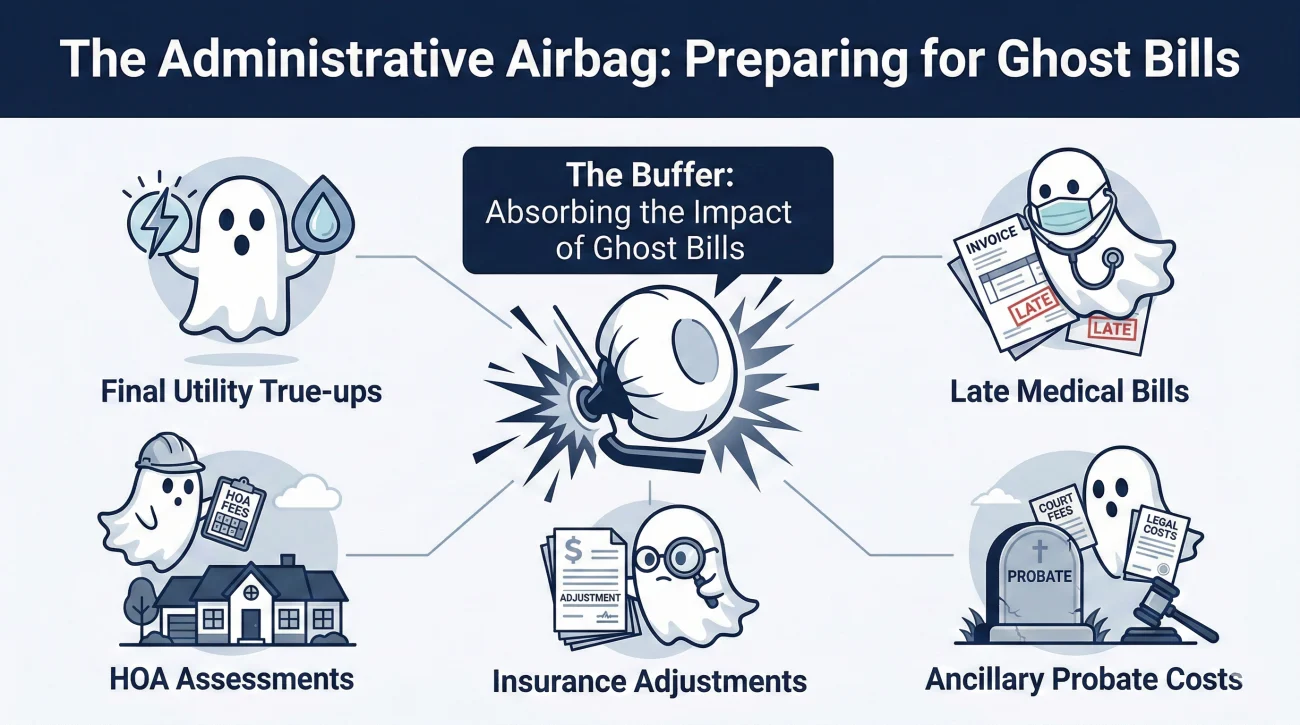

Why the Buffer Exists: The “Ghost Bills”

Think of the reserve as an administrative airbag. When closing an estate, there is always a lag between the moment you think all the bills are paid and the moment the local system officially agrees with you. The holdback exists to absorb any bumps during that lag time.

In my day-to-day admin work, the most common reason a reserve saves an executor is the arrival of “ghost bills.” These are expenses that slip through the cracks of normal mail forwarding or take months to process. If you are building a reserve, you must account for these common blind spots:

- 👻 Final utility true-ups (especially if a house was sold mid-billing cycle)

- 👻 Late-arriving ambulance, hospital, or specialized medical lab bills

- 👻 Homeowner association (HOA) special assessments passed just before the property sold

- 👻 Property insurance premium adjustments

- 👻 Fees for out-of-state property administration (ancillary probate costs)

The Core Buckets: What Are We Holding Back For?

Executors often struggle to explain to beneficiaries exactly what the holdback is meant to cover. When you keep the explanation vague, beneficiaries tend to get suspicious. When you categorize the reserve into logical business buckets, it becomes an unarguable administrative necessity.

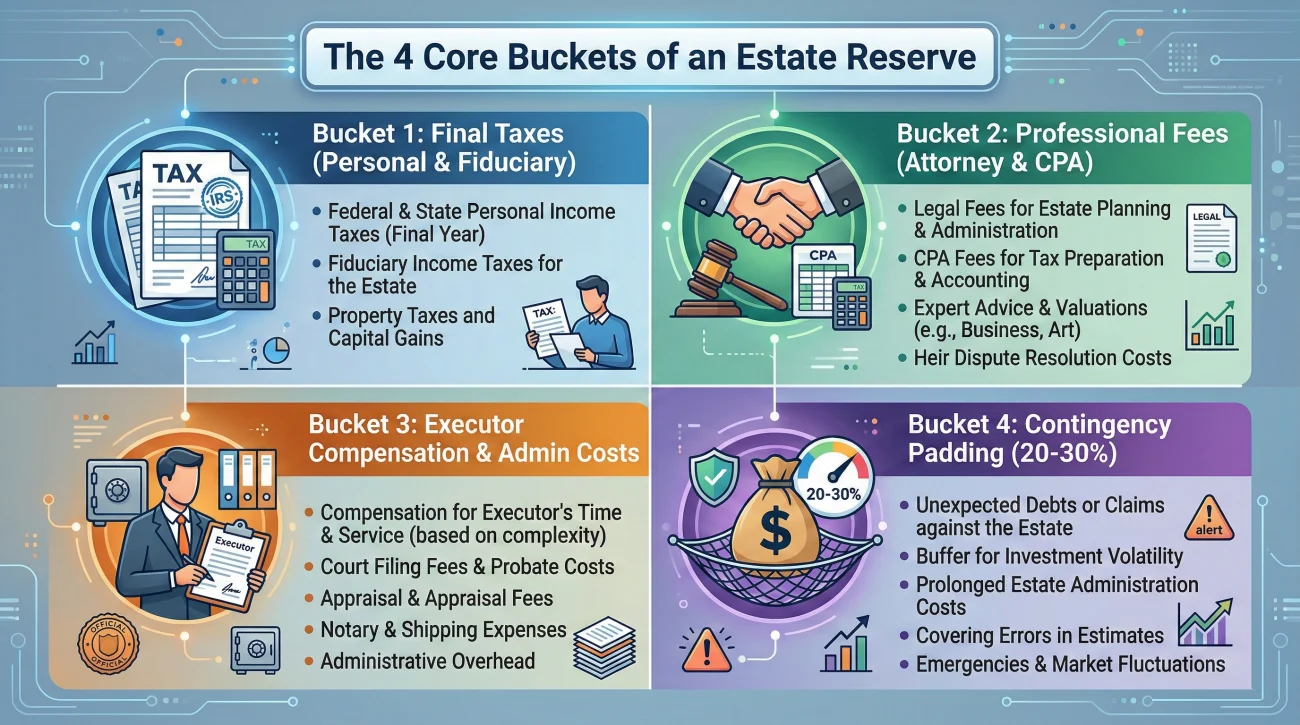

1. The Final Tax Buffer

This is usually the largest and most unpredictable category. A reserve for taxes estate buffer is mandatory because tax agencies operate on timelines that you cannot control. A major blind spot here is the difference between personal and fiduciary taxes. Many executors remember to hold back funds for the deceased’s final personal income tax return (money earned while alive). However, they frequently forget the fiduciary income tax return, which covers income the estate itself earned after the date of death, such as interest on the bank account or capital gains from selling the house. Because processing times can be lengthy (as noted by official IRS guidelines regarding estate obligations), this buffer must remain intact until you hold a physical clearance letter.

2. Final Professional Fees

Closing an estate requires professional help right up to the very end. Even if the attorney and the accountant have been paid for their work over the past year, they will still need to bill the estate for the final administrative steps. Drafting the final accounting, filing the last tax returns, and preparing beneficiary release documents all require unbilled future hours. The holdback secures the funds to pay them.

3. Executor Compensation and Administrative Costs

If the estate is still maintaining a storage unit while final distributions are being arranged, the reserve covers those carrying costs. Crucially, this is also the bucket that covers your own compensation. Many executors forget that if they intend to claim an authorized executor fee or request final out-of-pocket reimbursements for travel or postage, those funds must be explicitly calculated and safely held back from the beneficiaries.

4. The Contingency Padding

Even the most organized executor cannot predict everything. A standard practice is to add a percentage-based contingency padding to the calculated reserve. This padding, usually twenty to thirty percent, is typically calculated against the combined total of your estimated tax and professional fees, rather than the entire estate balance. Why add this extra padding? Because estimates are rarely perfect. Attorneys and CPAs bill hourly, and if beneficiaries start asking complex questions about the final accounting, your attorney will have to spend unbilled hours answering them, driving up the final cost. The contingency padding absorbs these fluctuations.

💡 Pro Tip: A complication I frequently see involves a beneficiary who is also a creditor (for example, a sibling who loaned the deceased money for home repairs). If their creditor claim is still being validated, the holdback must be large enough to cover that potential debt payout, keeping it entirely separate from their inheritance share.

How to Document the Holdback Decision Neutrally

Documentation is your best defense against beneficiary impatience. If someone asks why you are keeping funds back, you want to be able to point to a logical, written breakdown rather than relying on a defensive explanation.

You do not need a complex legal document for your internal tracking. A simple spreadsheet or a tracked list is highly effective. The goal is to show your math and demonstrate that the reserve is not an arbitrary stockpile.

Building the Internal Reserve Log

Here is an example of the high-level fields I commonly see in a well-organized executor’s reserve tracking file.

| Holdback Category | Estimated Amount Needed | Source of Estimate | Expected Resolution Event |

|---|---|---|---|

| Final Tax Preparation | [Base Estimate] | Quote from Tax Advisor | Filing of Final Return |

| Tax Liability Buffer | [Generous Padding] | Advice from Tax Advisor | Clearance Letter Received |

| Final Legal & Closing Fees | [Base Estimate + Padding] | Discussion with Attorney | Final Accounting Approved |

| General Contingency (20%) | [Calculated Buffer] | Executor Discretion | Estate Officially Closed |

Holding back a random chunk of money because you feel nervous about unknown bills, leaving beneficiaries to guess your motives.

Holding back a documented amount based on professional estimates and contingency padding, with an internal log justifying every category.

This organized approach seamlessly sets the stage for moments when you want to release some funds early to keep the peace, which brings us to the concept of partial distribution.

The Partial Distribution Pressure Valve

Often, executors find themselves caught between a rock and a hard place. The estate has a large amount of cash sitting idle, but the final tax clearance will not arrive for several months. Beneficiaries are frustrated, and the executor is stressed. In these scenarios, a partial distribution holdback strategy is commonly used to safely distribute a portion of the inheritance early.

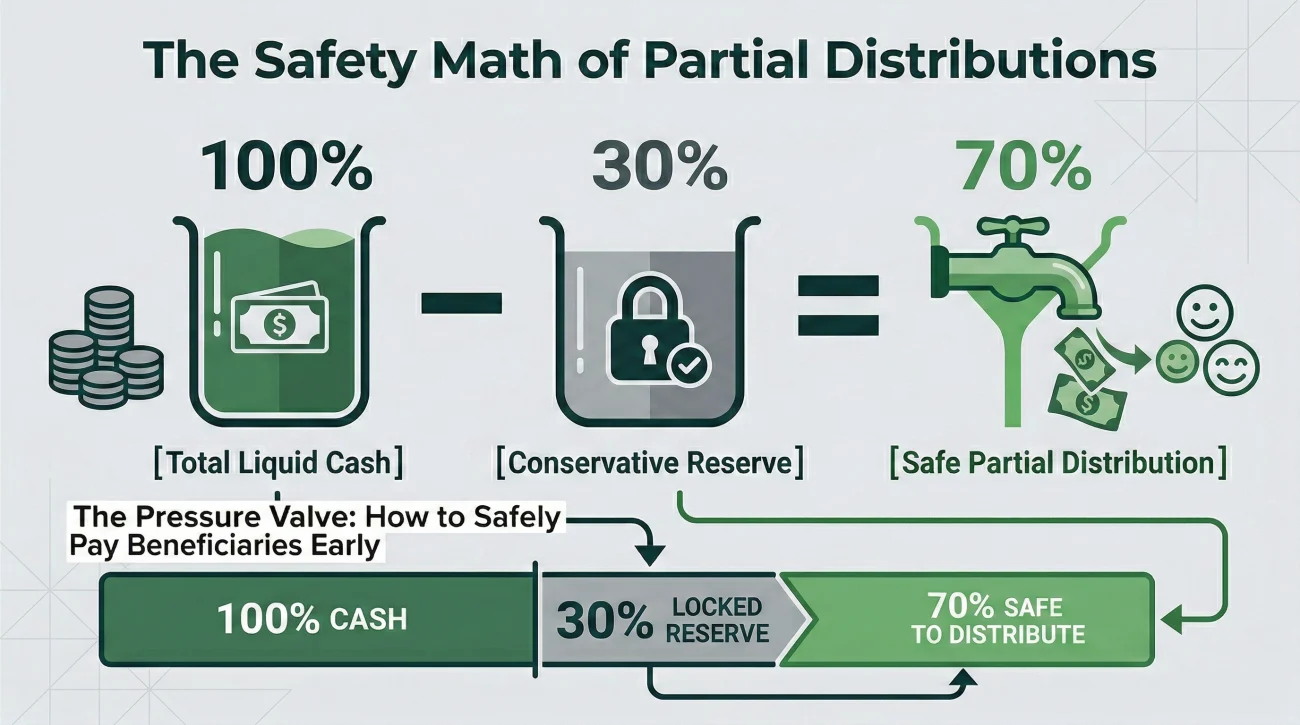

The Safety Math of Partial Distributions

If you decide to pursue a partial distribution, the math works backwards. You must calculate the rock-solid reserve amount first, lock that down, and only use the leftover surplus for the early payout:

[Total Liquid Estate Cash] - [Highly Conservative Reserve Holdback] = [Safe Amount for Partial Distribution]

👉 Hypothetical Math Example: Let us say the total liquid estate cash represents 100 percent of your available funds. The CPA estimates final taxes will consume 15 percent, and the attorney estimates closing costs at 5 percent. A safe holdback does not just retain that exact 20 percent. A seasoned executor will retain the 20 percent for known bills, plus an additional 10 percent for contingency padding. That means 30 percent is locked safely in the reserve, leaving 70 percent available to safely distribute as a partial payment to beneficiaries.

When to Avoid Partial Distributions

While partial distributions are a fantastic tool, there are specific times when making one is highly reckless. You should generally avoid partial distributions if the estate is facing pending litigation, if there are unresolved Medicaid recovery claims, or if the deceased had a highly complex business tax situation that has not been audited. In these volatile situations, keeping 100 percent of the funds in the reserve is the only safe move.

Communication Hygiene: Explaining the Reserve

Once you have calculated that safe partial amount, the next hurdle is explaining it to the family. How you communicate the reserve to beneficiaries will largely determine whether they accept it peacefully or fight you on it.

The best approach is early, neutral, and process-focused communication. You want to frame the holdback not as your personal choice, but as a standard administrative requirement.

Scripts for Holdback Communication

Here are a few copy-paste safe scripts you can adapt when you need to explain why funds are not being fully distributed immediately.

Scenario 1: Announcing a partial distribution while retaining a reserve

Subject: Estate Update: Initial Distribution and Final Reserve

Hello [Everyone / Beneficiaries],

I am writing to provide an update on the estate administration. We are preparing to make an initial, partial distribution of the estate funds in the coming weeks.

As is standard practice, the estate will be retaining a final reserve holdback. This buffer is kept in the estate account to cover the final tax filings, the concluding professional fees (CPA and legal), and any remaining administrative closing costs.

Once the final tax clearances are received and all closing expenses are definitively paid, I will provide a final accounting, and the remaining reserve balance will be distributed in full to close the estate.

I will send a separate email shortly detailing the next steps and the documents required for this initial distribution.

Best regards,

[Your Name]

Scenario 2: Responding to a beneficiary asking “Why aren’t we getting everything now?”

Subject: Re: Question regarding final distribution timelines

Hello [Beneficiary Name],

I completely understand the desire to wrap things up quickly.

To ensure the estate is closed safely, I am required to hold back a reserve to cover the upcoming final tax returns and closing administrative costs. Distributing all the funds before these final liabilities are formally cleared would place the estate at significant risk if a final bill comes in higher than estimated.

My goal is to protect the estate’s assets and ensure we close cleanly without any unexpected issues later. I will keep you updated as we cross the final administrative milestones.

Thank you for your patience,

[Your Name]

These templates are designed to remove emotion from the conversation. By leaning on the administrative process, you help beneficiaries understand that the delay is standard procedure.

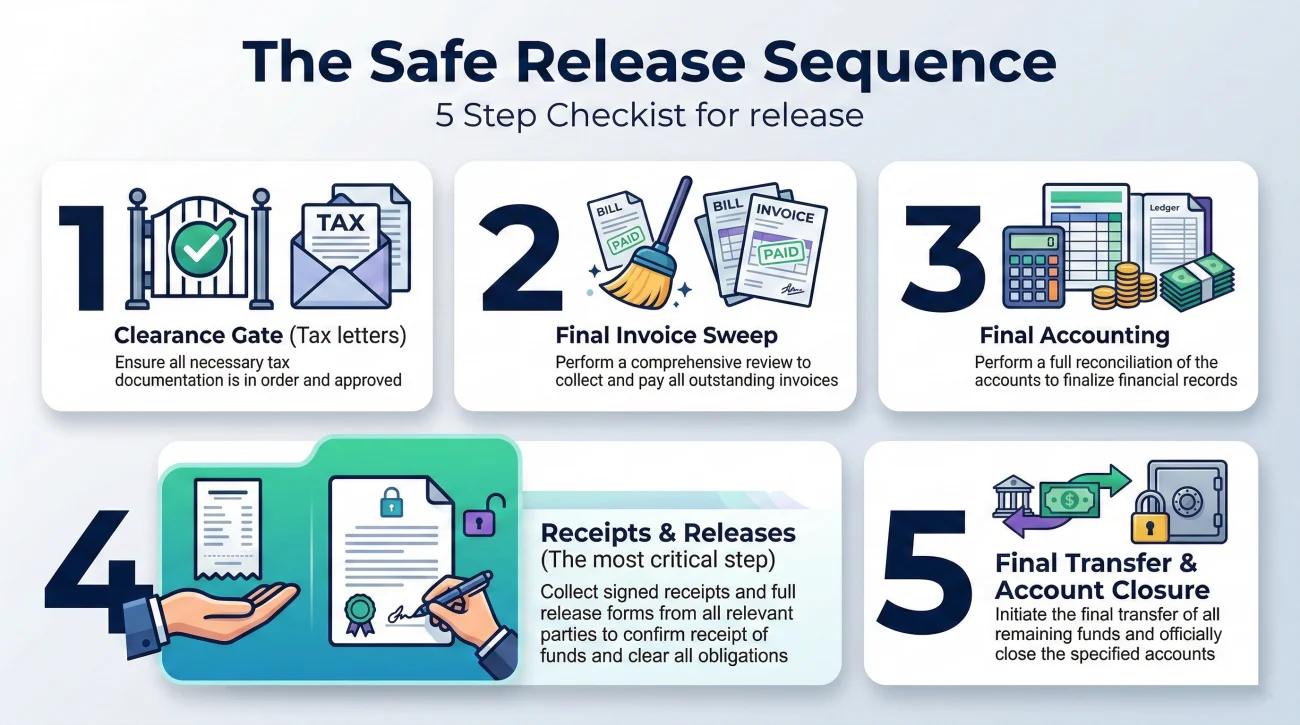

The Release Sequence: How the Holdback Finally Leaves

One of the biggest questions I get from executors is: “Okay, I held the money back. Now how do I safely let it go?” You do not just wake up one morning and decide to write the checks. Releasing the holdback is a sequenced process.

While every estate has its own rhythm, the safe release sequence generally looks like this:

- ✅ Step 1: The Clearance Gate. You receive written confirmation that the final tax returns are accepted and no further taxes are due.

- ✅ Step 2: The Final Invoice Sweep. You request and pay the absolute final invoices from your attorney, your CPA, and yourself (if claiming compensation).

- ✅ Step 3: The Final Accounting. You prepare the final accounting document, showing exactly what is left in the reserve after those final bills were paid.

- ✅ Step 4: The Receipts and Releases. Beneficiaries review the accounting and sign a formal release, acknowledging the final numbers and releasing you from liability.

- ✅ Step 5: The Final Transfer. Only after the releases are signed do you write the final checks, zeroing out the reserve and closing the bank account.

Skipping straight to Step 5 without securing the documents in Step 4 is a recipe for post-closure disputes.

Common Holdback Mistakes and How to Avoid Them

Even with the release sequence in hand, there are recurring patterns that derail executors at the last moment. Based on real-world operational patterns, here are the most common points where the reserve process goes wrong.

Mistake 1: The Silent Holdback

If you keep a reserve but never tell the beneficiaries, they will assume the math on your final accounting is broken. They will see a bank balance of one amount, and a distribution of a smaller amount, and immediately suspect foul play. Transparency from day one prevents this missing document loop. State clearly that a reserve exists and why.

Mistake 2: Failing the Digital Estate Audit

Executors are usually very good at holding back money for taxes and lawyers, but they often forget that modern estates bleed cash through subscriptions. I highly recommend running a quick “digital audit” on the deceased’s credit card statements before finalizing the holdback amount. Look specifically for auto-renewals on web domain hosting, premium cloud storage (like Apple or Google Drive), streaming services, subscription boxes, and software licenses. If you have not fully shut these down, they will quietly eat away at your reserve over the next six months.

Mistake 3: The Insolvent Reserve

Sometimes, despite your best planning, the reserve is simply not enough. A massive tax bill arrives that wipes out the contingency and the base estimate. If you have already made a partial distribution and the remaining holdback cannot cover the new bill, the estate is functionally insolvent regarding that debt. At this point, you must pause everything and consult your attorney immediately, as there are strict legal protocols for handling debts that exceed available cash. You cannot simply ignore the bill, nor should you panic and pay it yourself without legal guidance.

Final Thoughts on Protecting the Estate

The period right before final closure is often the most exhausting phase of your role. You are tired, the paperwork feels endless, and the beneficiaries are eager to move on. The pressure to cross the finish line quickly is intense.

But before you write those final checks, remember the executor from the beginning of this guide who had to pay a delayed medical transport bill from his personal checking account. That entire financial nightmare could have been completely avoided if he had stayed disciplined and maintained his executor hold back funds until the very end.

Your job is to close the estate safely, not just quickly. By documenting your reasoning, communicating the categories clearly, and refusing to release the reserve until you hold the final clearance letters, you protect both the estate and yourself.

Once your reserve is securely in place and you understand what it covers, you are ready to look at the broader picture of how to finalize the estate. For a comprehensive look at the steps required to cleanly finish your duties, including accounting, obtaining releases, and finalizing records, I highly recommend reviewing our complete Estate Distribution Checklist. It will help you map out the final leg of the journey with confidence.

❓ FAQ

⏳ What is the realistic timeline for holding back estate funds?

While every estate varies, executors commonly hold the final reserve for 6 to 18 months. This timeline is heavily dictated by how long it takes to process the deceased’s final tax returns and receive official clearance from tax authorities.

✍️ What if a beneficiary wants to sign a waiver instead of me holding back funds?

A beneficiary signing a piece of paper saying they will pay future bills does not usually protect you from creditors or the IRS. Authorities generally pursue the executor who released the funds prematurely, not the beneficiary holding a DIY waiver.

🏛️ Do I need a judge’s permission to finally release the holdback?

This depends heavily on whether the estate is under formal court supervision. In independent or unsupervised administration, executors often release the reserve once beneficiaries sign off on the final accounting, without needing a final court hearing.

🌍 How do out-of-state properties affect the reserve amount?

Properties in multiple states usually trigger “ancillary probate,” meaning you are dealing with multiple local jurisdictions, multiple filing fees, and potentially multiple tax systems. This drastically increases the chance of surprise costs, requiring a much larger contingency reserve.

📦 What happens if I discover a new asset while holding the reserve?

If a new asset (like a forgotten stock account) is liquidated, those funds are typically deposited into the estate account, increasing your liquid cash. You would simply update your accounting, ensure the reserve is still sufficient, and distribute the surplus accordingly.

🧾 How do I prove to beneficiaries that the holdback was spent correctly?

This is the exact purpose of the Final Accounting document. The accounting will list the starting reserve balance, itemize every final bill and tax payment made from it, and show the remaining balance available for the final closing distribution.

🛑 Can a creditor force me to distribute the holdback to them immediately?

Valid creditors must be paid according to a strict legal priority order (taxes usually come first). If the estate is solvent, legitimate bills are paid from the reserve as they are verified. You do not distribute to beneficiaries until those creditors are cleared.

📉 Should I keep the holdback in a separate savings account?

You can, but it is rarely necessary unless the estate is highly complex. Most executors simply keep the reserve in the main estate checking account and track the restricted amount on their internal spreadsheet to avoid accidentally spending it.

🔍 What happens to the final holdback if a beneficiary cannot be located?

If a beneficiary goes missing at the end, their specific share of the remaining holdback is usually deposited with the state’s unclaimed property division or held by the court, allowing you to finalize the accounting and step down as executor.

💼 Can the attorney hold the reserve in their trust account instead of me?

Yes, in many jurisdictions, the estate attorney can hold the reserve funds in their firm’s formal trust account (IOLTA). This transfers the burden of managing the final payout sequence from you to the attorney, which many executors prefer.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.