- Institutions often reject perfectly valid court documents simply because the certification date is considered “too old” by their internal compliance rules.

- Courts do not always set expiration dates, but banks, insurers, and title companies frequently demand a recent letters testamentary reissue based on their own risk policies.

- When requesting updated letters from the court, always check for an online portal first, provide your exact case number, and state a clear reason for the request.

- Do not order fresh copies in massive bulk; a “just-in-time” ordering approach keeps your documents valid for immediate tasks and saves estate funds.

The Frustration of Stale Documents

You have done everything right. You navigated the initial court process, received your official appointment, and started organizing the estate. You have been paying bills, securing property, and cataloging assets for months. Then, you finally locate a forgotten bank account and mail in your official paperwork to claim the funds. A week later, you get a rejection letter. The bank claims your documents are invalid.

I see this exact scenario play out constantly in my day-to-day estate administration support work. The executor panics, thinking they have lost their legal authority or done something wrong. In reality, the legal authority is usually completely intact. The problem is simply the date stamped on the paper. You have hit the “stale document” wall, and you need a letters testamentary reissue.

When you are managing an estate over a long period, the initial certified copies you received from the court age out in the eyes of corporate compliance departments. They do not want to risk handing over money if your status as executor changed last week. In this guide, I will walk you through exactly why this happens, how to identify when you need updated letters, and the exact scripts to use to keep the process moving.

Why Institutions Ask for Recent Letters

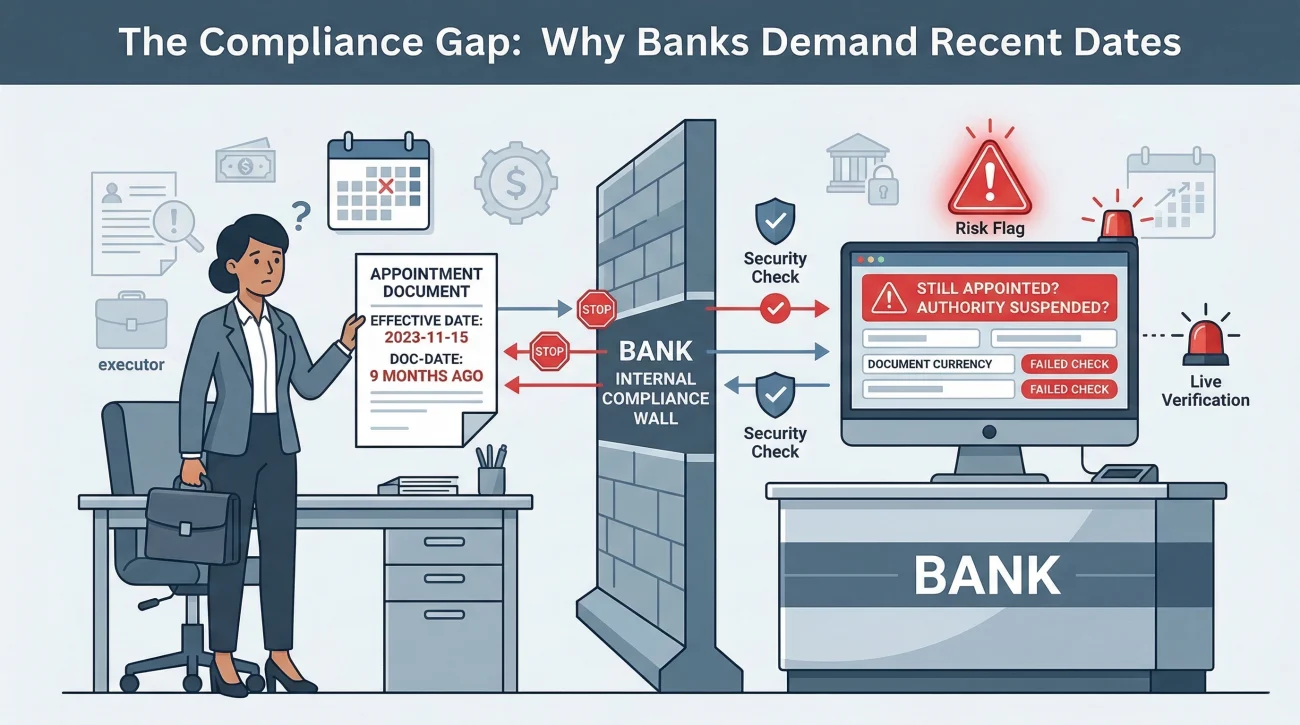

To understand why a bank teller or a corporate back-office rejects your documents, we have to look at it from their perspective. When a court appoints you as an executor or administrator, that authority generally lasts until the estate is officially closed or you are explicitly removed by a judge.

However, third parties (like banks, brokerages, and life insurance companies) have no direct pipeline to the court’s daily records. If you hand them a document that was stamped nine months ago, their compliance software flags a risk. The bank’s legal department worries: What if this person was removed as executor two months ago? What if a later will was found? What if the court suspended their authority?

Key Point: Banks are not questioning whether you were *ever* appointed. They are questioning whether you are *still* appointed today. A freshly dated certification seal is the only proof they will accept.

In many cases, the pushback is not a matter of state law, but rather an internal corporate policy. I always tell executors not to take this rejection personally. The front-line customer service representative is just following a checklist on their screen.

🔆 Tip: Before you spend hours on hold arguing with a bank manager about the validity of your old document, realize that it is almost always faster, cheaper, and less stressful to simply request a reissued letters testamentary from the court clerk.

Common Triggers for Reissue or Renewal

When I am helping someone map out an estate timeline, we try to predict exactly when they will need a letters of administration reissue or updated testamentary letters. By anticipating the bottlenecks, you can order fresh documents a few weeks before you actually need them. Here are the most common scenarios that force an update.

Corporate Compliance Aging Rules

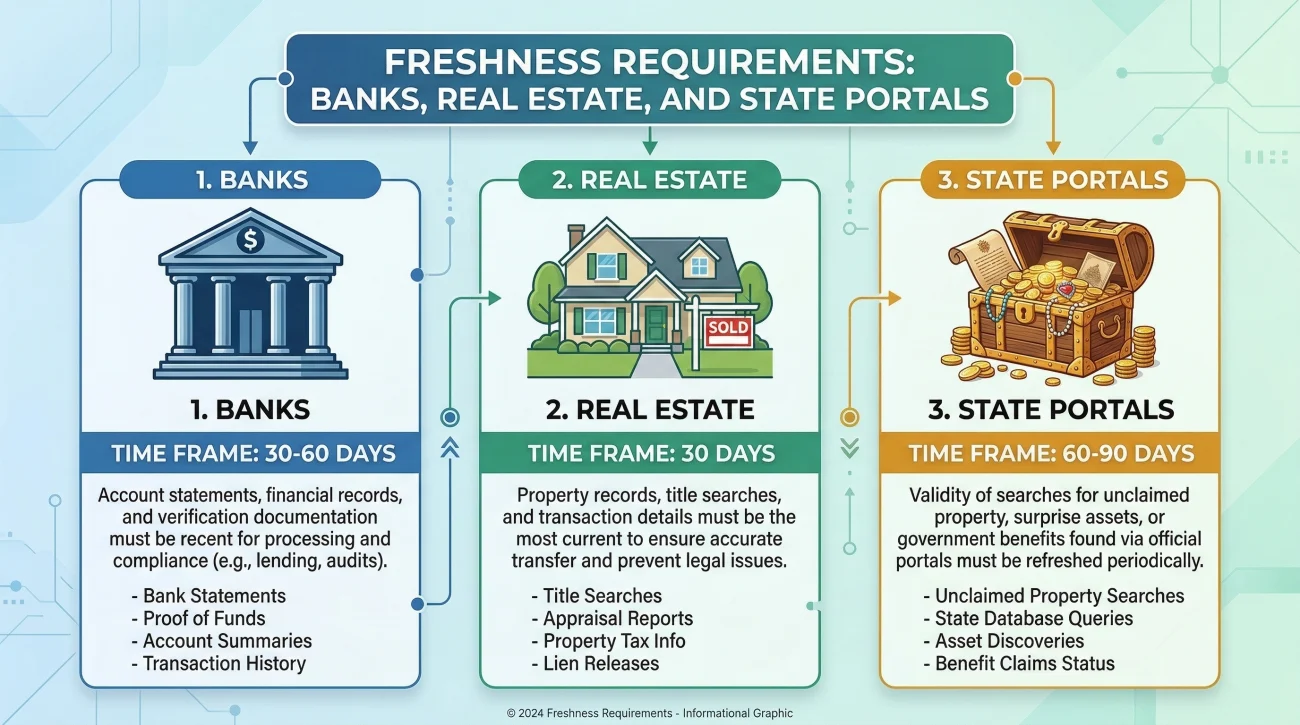

If an estate takes longer than a few months to settle, your original documents will eventually age past the acceptable window for major banks and brokerages. If you attempt to transfer a stock portfolio a year after the estate was opened, expect to provide freshly certified copies.

Real Estate Transactions and Title Companies

Selling the deceased person’s home is a massive undertaking, and title companies are incredibly strict about risk. If you are signing a deed to transfer property, the title underwriter will almost always demand a very recent certification date on your letters. Relying on old documents at a real estate closing is a common recipe for a delayed settlement.

Discovering Surprise Assets Late in the Process

Even the most organized executor cannot control when a piece of mail arrives regarding an unknown life insurance policy or an old uncashed check. By the time you reach out to claim a newly discovered asset two years into the process, your original packet of certified copies is long expired in the eyes of that company.

| Institution Type | Typical “Freshness” Requirement | Common Friction Point |

|---|---|---|

| Major National Banks | Usually within 30 to 60 days | Call center reps cannot override the system if the date is too old. |

| Title Companies (Real Estate) | Usually within 30 days | Underwriters will halt a home closing without a recent court seal. |

| Life Insurance Companies | Varies, often up to 6 months | Delays in processing claim checks if they require an updated copy. |

| State Unclaimed Property | Usually within 60 to 90 days | Government portals auto-reject old document uploads. |

When to Push Back on Institutions

While ordering a reissued copy is often the easiest path, there are times when an institution is being unreasonable. If you just received your letters from the court two weeks ago, and a customer service agent tells you they are “expired,” the agent is likely confused.

In these cases, before you spend time and money going back to the court, try escalating the issue politely but firmly within the institution. Often, a front-line worker may misread the date the will was signed as the date the letters were issued.

Here is a professional, copy-paste script you can use to request a review of your document before giving up:

Subject: Escalation Request: Validity of Letters Testamentary for [Account/Claim Number]

Hello,

I was recently informed by a representative that the Letters Testamentary I submitted for the Estate of [Deceased Name] were rejected due to the date.

Please review the document again. The court certification seal is clearly dated [Insert Date], which is only [Number] days old. This is a newly issued, valid document that demonstrates my current authority.

Could you please escalate this to your legal or compliance department for a secondary review? If there is a specific, written company policy stating that documents must be newer than [Number] days, please provide that policy to me in writing so I can include it in the estate’s expense log when I purchase another copy from the court.

Thank you for your prompt assistance with this review.

If this escalation works, you save the estate time and money. If they still refuse (and you are dealing with a large national bank), you technically have the option to file a complaint with the Office of the Comptroller of the Currency (OCC) or your state banking authority. However, you have to weigh this option against your timeline. If you have months to spare and want to hold the bank accountable, a formal complaint is a valid path. But if you need to access those funds immediately to pay pressing estate bills, your most pragmatic operational move is usually to swallow the frustration and order the updated copies.

What to Ask For: Request Language and Preparation

When you decide it is time to get updated letters, the process is generally straightforward, but clarity is essential. Court clerks manage thousands of cases, and vague requests lead to delays. You want to make it incredibly easy for them to locate your file, verify your identity, and stamp a new copy.

💡 Pro Tip: Court processes are highly localized. A large metropolitan probate court might have a slick online portal, while a small rural county might still require mailed physical letters. Always verify your specific county’s preferred method before sending anything.

Before you draft a request, gather this information:

- 📄 The exact case number or docket number.

- 👤 The full legal name of the deceased person.

- 📅 The approximate date you were originally appointed.

- 💳 A method of payment for the certification fees.

The Script for the Court Clerk

If your county does not have an online portal and requires an email or mailed request, keep your communication brief. You do not need to explain the entire backstory of the bank frustrating you. Just state what you need.

Subject: Request for Reissued Certified Copies – Estate of [Deceased Name], Case #[Number]

Dear Clerk of the Court,

I am the appointed executor for the Estate of [Deceased Name], under Case #[Number]. My original letters were issued on [Original Date].

I need to order [Number] new certified copies of the Letters Testamentary with a current date stamp, as a financial institution requires updated copies to release assets.

Please let me know the total fee for these copies and the preferred method of payment. Can these be mailed to my address on file, or do I need to send a self-addressed stamped envelope?

Thank you for your time and assistance,

[Your Name]

[Your Phone Number]

⚠️ Warning: Never send cash in the mail to a court unless explicitly instructed to do so. Always ask for their preferred payment method, which is commonly a cashier’s check, a firm check, or an online credit card portal.

Once you send this request off to the court, the very next step is to ensure you don’t lose track of it.

How to Document Requests to Avoid Repeats

One of the biggest mistakes I observe is executors treating document requests as random, one-off chores. They order a few copies, use them, forget about them, and then have to scramble and pay for more copies three weeks later when another bank asks for one. This creates a stressful, disjointed workflow.

To avoid this, you need a tracking system. When you build out your probate court checklist for executors, you should dedicate a specific section to document management. Treat your certified copies like valuable inventory.

Building a Document Inventory Log

Every time you request a letters testamentary renewal, log it. I recommend keeping a simple spreadsheet or a written ledger that tracks the lifecycle of your certified copies. This stops the endless cycle of guessing whether you have enough valid copies left for your upcoming tasks.

| Date Ordered | Method | Copies Received | Freshness Date | Where Sent |

|---|---|---|---|---|

| Oct 1, 2023 | Online Portal | 3 | Oct 5, 2023 | Chase Bank (Oct 10), Title Co. (Oct 12) |

| Jan 15, 2024 | Mailed Check | 2 | Jan 25, 2024 | State Unclaimed Property (Feb 2) |

You keep a pile of papers on your desk. When an insurer asks for a copy, you grab one, mail it, and cross your fingers. Two months later, you realize all the remaining copies are too old to use for the house sale.

You check your log. You see your current batch is 45 days old. Knowing the real estate closing is next month, you proactively order three fresh copies from the court today, ensuring no delays at the closing table.

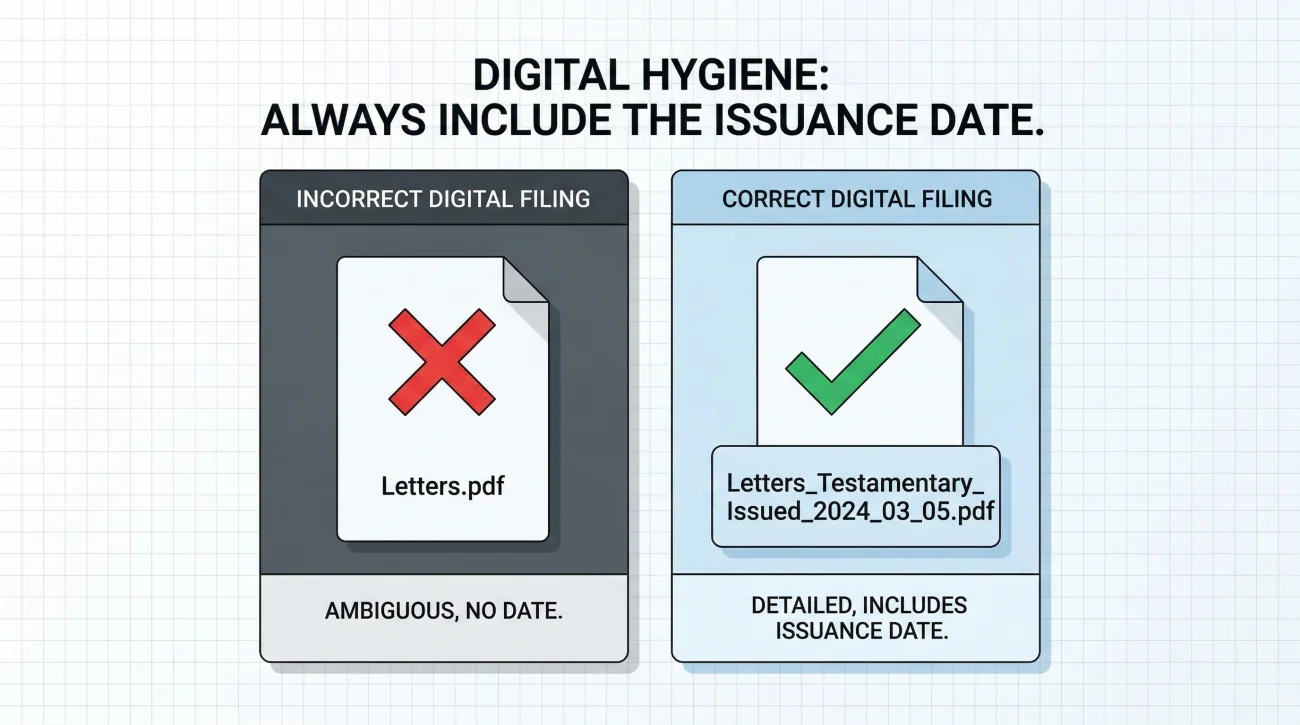

Digital File Naming for Scans

If an institution allows you to upload a scanned PDF of your updated letters testamentary rather than mailing a hard copy, your digital file naming hygiene becomes crucial. If you just name the file “Letters.pdf”, you will eventually confuse the original letters with the reissued ones.

Always include the issuance date in the file name so you know exactly which version you are sending. For example:

| ❌ Bad | ✅ Good |

|---|---|

| Letters_Final_Scan.pdf | Letters_Testamentary_Issued_2023_11_15.pdf |

| Court_Paperwork_Updated.pdf | LOA_Certified_Reissue_2023_11_15.pdf |

Managing Costs and Avoiding Over-Ordering

When executors first encounter the “stale document” problem, their instinct is to overcompensate. They think, “Fine, if they want fresh copies, I will just order 20 copies right now so I never run out.” This is a mistake that wastes estate funds.

Courts charge a fee for the physical labor and the official seal, typically ranging from $5 to $25 per certified copy, depending entirely on your county. Ordering 20 copies could easily cost hundreds of dollars.

Because those 20 copies will all have the exact same date stamp, any copies you don’t use within the next 30 to 60 days will age out together, becoming just as useless as the original batch. Instead of ordering in massive bulk, adopt a “just-in-time” inventory mindset. Map out your next 30 days of estate administration. How many institutions are you planning to contact or close out this month? Order only enough to cover those specific tasks, plus maybe one extra as a backup.

❌ Note: Never give away your last freshly certified copy unless you absolutely have to. If a bank asks for it in person, politely ask the branch manager if they can inspect the original, make a photocopy for their internal files, and hand the certified original back to you. Many banks will do this, saving you the cost of ordering a replacement.

Final Thoughts on Maintaining Authority

Navigating document expiration rules does not have to be a constant source of friction if you build a tracking system early on. Anticipating this pushback is a hallmark of a well-organized estate administration.

By understanding that banks and insurers operate on strict compliance timelines, you can stop fighting the system and start working within it. Track the age of your documents, order updated letters in small batches right before major transactions, and keep a clean log of where every document goes. This simple discipline will dramatically reduce your stress and keep the estate moving forward without sudden, unexpected roadblocks.

❓ FAQ

🕰️ Do letters testamentary expire?

Legally, the court appointment usually remains valid until the estate is closed or you are removed. However, financial institutions often treat them as “expired” for their internal compliance purposes if the certification date is older than 30 to 60 days.

🏛️ What if the court clerk is unresponsive to my request?

If a mailed or emailed request goes unanswered for weeks, try calling the clerk’s office directly. If that fails, look up the Court Administrator for that county; they oversee court operations and can usually help locate a stuck document request.

🔄 How do I get an updated copy of letters of administration?

You must contact the clerk of the probate court where the estate was opened. Many modern courts have online portals for this. Otherwise, you must mail or email a request with the case number and pay a small fee per copy.

📅 Is there a standard time limit for executor letters?

There is no universal legal time limit. Requirements vary entirely by the institution you are dealing with. A major bank might require a date within 60 days, while a local utility company might accept a copy that is a year old.

💸 Do I have to pay again for reissued letters?

Yes, in most cases. Courts charge a fee (often $5 to $25 per document) for the physical labor of finding the file, stamping the seal, and certifying the copy. This should be logged as a legitimate administrative expense of the estate.

🖨️ Can I just make a photocopy of the old letters?

No. Institutions requesting recent letters are specifically looking for a fresh, raised, or colored court seal with a recent date stamp. A standard black-and-white photocopy of an old document will generally be rejected.

📬 How long does it take the court to send renewed letters?

It depends on the specific county court’s backlog. Some courts process requests via an online portal in a few days, while others require mailed requests that can take several weeks to turn around. Always ask the clerk for current processing times.

🗺️ Do I need different letters if the estate has property in another state?

If you are dealing with out-of-state real estate, you often need to open an “ancillary probate” in that state. The title company there will require certified letters issued by that specific out-of-state court, subject to their own freshness rules.

📝 What do I say to the court clerk to get an update?

Simply say: “I am the executor for Case Number [X]. A financial institution is requiring a recently dated copy of my Letters Testamentary. I would like to order [Number] new certified copies. What is the fee and process?”

🛑 Can a bank freeze the estate account if my letters are outdated?

Once an estate checking account is successfully opened, banks rarely ask for updated letters just to keep it running for everyday bills. However, if you are in the middle of a major transaction (like transferring a large brokerage portfolio or wiring funds for a real estate closing) and your letters cross their “expiration” threshold mid-process, the institution can and will put a hard hold on the transfer until you provide a freshly dated copy.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.