- An executor bond (or probate bond) is essentially an insurance policy that protects the estate and its heirs, not a penalty against you.

- Courts commonly ask for a bond if there is no will, if the will does not explicitly waive it, or if you live in a different state.

- The bond amount is set by the court, typically based on the estimated value of the estate assets. Do not guess this number on your own.

- You will need a specific set of documents to apply with a surety company, including an asset snapshot and your own basic background information.

- Always ask the court clerk for bond requirements in writing before you pay any premiums or sign contracts.

That Unexpected Courthouse Surprise

I still remember sitting at a table with a family who had just returned from their first trip to the courthouse. The clerk had told them they needed an “executor bond” before they could move forward. They were stressed, confused, and honestly, a little offended. They thought the court was penalizing them or implying they could not be trusted with the estate.

If you have just heard the word “bond” and are feeling that same anxiety, take a deep breath. In my experience helping families navigate estate administration, I often see this exact moment of panic. The reality is much less dramatic. An executor bond is a very common, routine requirement.

When I work with first-time executors, my goal is always to translate intimidating courthouse language into practical steps. You do not need a law degree to handle this. You just need to understand what the document actually does, what information the surety company will ask you for, and how to keep your records organized so the process does not drag on for months.

Let us walk through what an executor bond actually is, why it comes up, and exactly what you need to put together in your preparation checklist to get it handled smoothly.

What is an Executor Bond, Really?

When people hear the word bond, they often think of savings bonds you buy at a bank, or bail bonds from criminal TV shows. A probate bond, sometimes called an administration bond or an executor bond, is something entirely different.

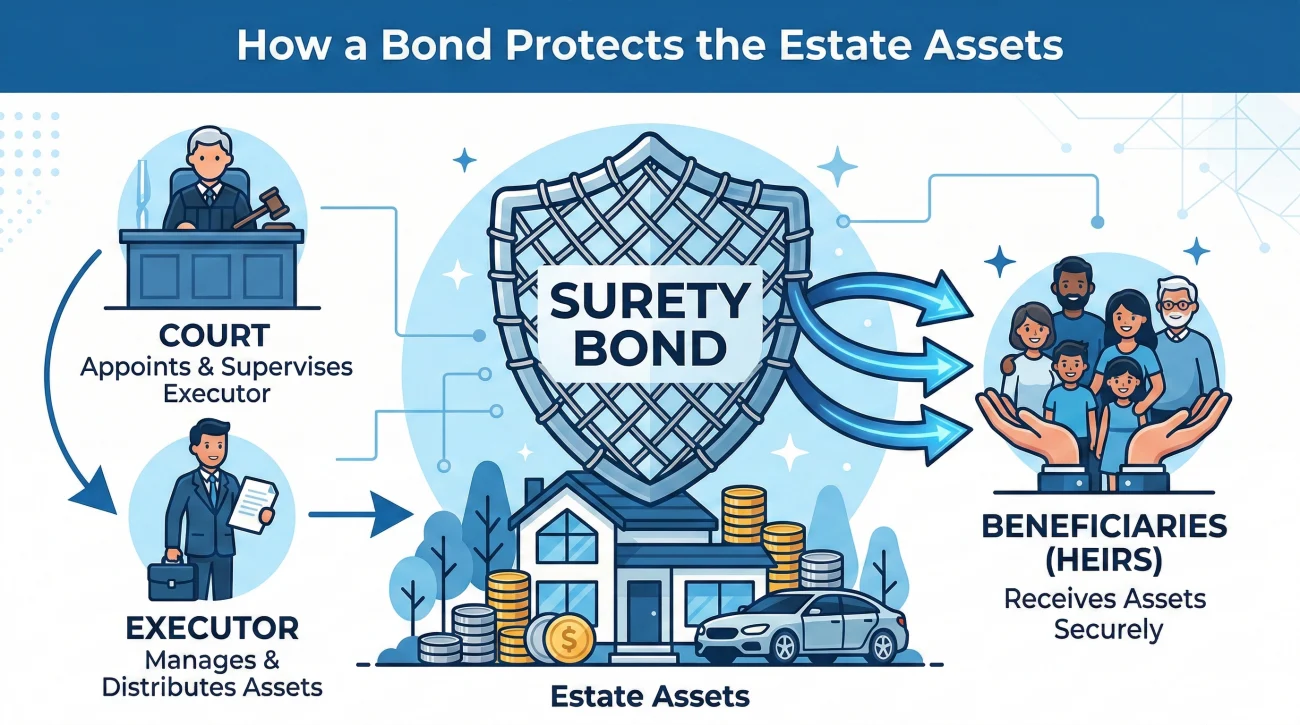

In simple terms, an executor bond is an insurance policy. But unlike car insurance that protects you if you make a mistake, this policy protects the beneficiaries and creditors of the estate. It guarantees that the person managing the assets will follow the rules and not mishandle the funds.

Key Point: Getting bonded does not mean the court thinks you are dishonest. It simply means the court is following a standardized procedure to put a safety net in place for the people who are supposed to inherit the assets.

I find it helpful to look at how this compares to what most people imagine when they hear the term.

A massive pile of cash you have to deposit with the court out of your own personal savings to prove you are wealthy enough to manage the estate.

A policy you purchase from a specialized insurance company (a surety company). You pay a premium, usually a small percentage of the total coverage amount, and the company provides a certificate to the court.

Once you understand that you are essentially just shopping for a specific type of insurance policy required by the court, the task feels much more manageable.

Common Situations Where a Probate Bond is Required

Why do some people have to get a bond while others skip this step entirely? In my daily work tracking these workflows, I commonly see a few specific procedural triggers that cause the court to ask for a bond.

Here are the most frequent reasons your checklist might include one:

| The Situation | Why it Triggers a Bond Requirement |

|---|---|

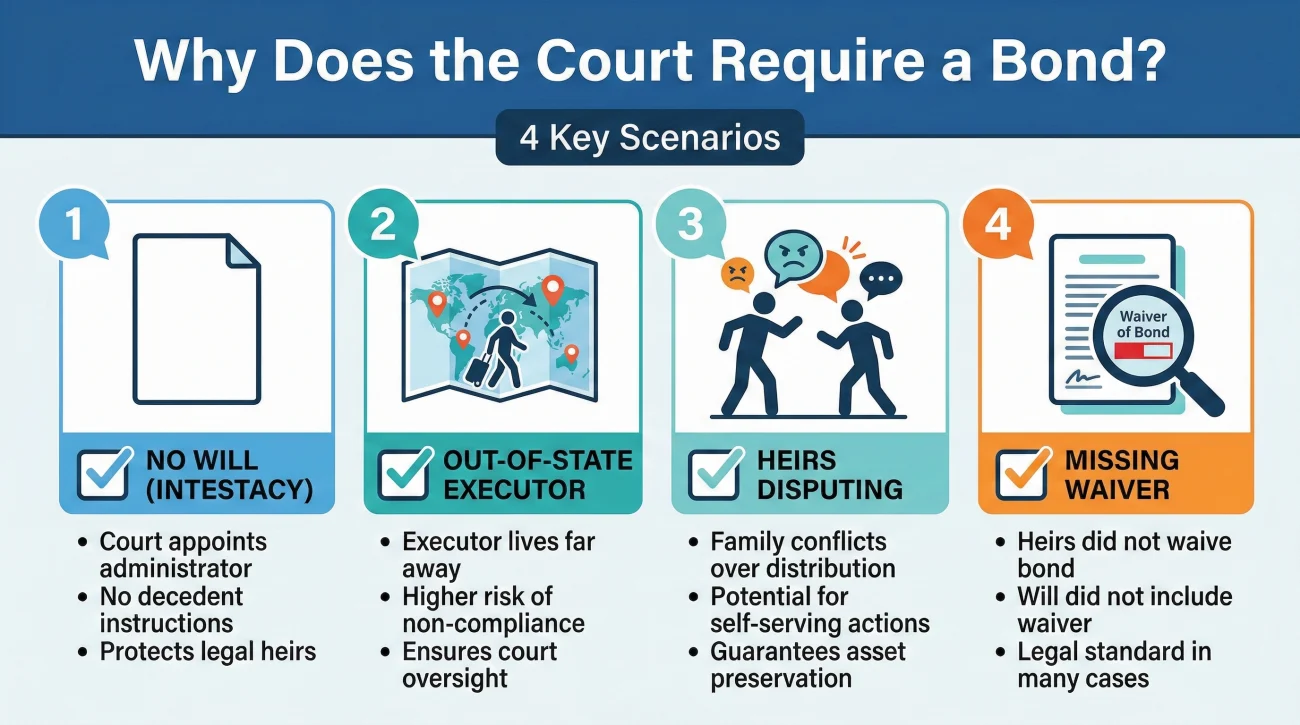

| There is no will | Without a will to guide the process, the court is appointing an administrator from scratch and often requires a safety net by default. |

| The will does not waive it | Many modern wills include a sentence explicitly saying “I direct that no bond be required.” If that sentence is missing, the court may ask for one. |

| You live far away | If you live out of state or out of the country, courts often ask for a bond because it is harder for them to oversee an out-of-state executor. |

| Disputes among heirs | If the family is arguing or someone officially requests a bond, the court will likely require it to protect everyone involved. |

A common mistake I see involves the second point. Sometimes, an executor reads the will, sees the phrase “no bond required,” and assumes they are completely exempt. But here is a field note from real operations: the court always has the final say. Even if the document waives it, a judge can override that if there are significant debts or minor children involved. Always wait for the court to confirm.

Now that you understand why the court is asking for this policy, let us look at how to actually get one without creating a paperwork nightmare for yourself.

The Executor Bond Preparation Checklist

When you find out you need an administration bond, your first instinct might be to just start Googling companies and filling out random forms. I highly advise against this. Taking an hour to get your paperwork organized first will save you days of back-and-forth emails with underwriters.

Surety companies need to assess risk. They want to know what the estate is worth and who is going to be holding the keys. Before you start gathering documents, you might be wondering about the cost. While it varies based on your credit and the estate size, the annual premium is usually a very small percentage of the total bond amount, often well under 1 percent.

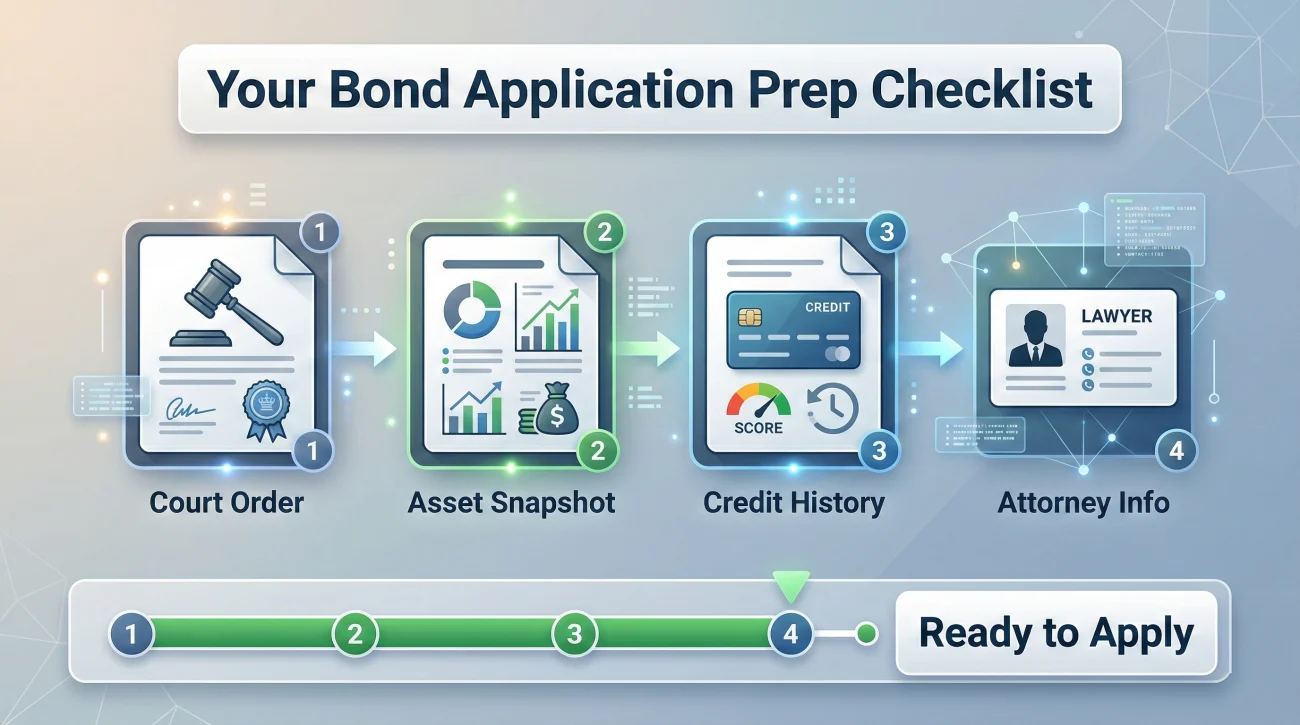

Here is the practical checklist of information you typically need to gather before you apply:

- A Specialized Surety Agency: Do not just pick the first generic insurance agent you find. Look for a surety agency that specifically advertises “probate bonds” or “fiduciary bonds” and is licensed in the state where the probate is taking place.

- The Court Order or Requirement Notice: You need the document from the court stating that a bond is required and specifying the exact amount. The bond amount is set by the court, not by you or the insurance company.

- An Asset Snapshot: You do not need a perfect, penny-exact inventory yet, but you need a reasonable estimate of the estate’s value. Group it into categories like real estate, bank accounts, and vehicles.

- Basic Background Information: The company will likely need your address, employment history, and sometimes a basic credit check to confirm you do not have a history of severe financial mismanagement or active bankruptcies.

- The Deceased’s Information: Full name, date of death, and the county where the probate case is taking place.

- Attorney Information: If you are working with an estate attorney, have their contact information ready. Many surety companies prefer communicating directly with legal counsel if one is involved.

⚠️ Warning: Never guess the bond amount. If you apply for a bond based on your own estimate of the estate, and the court later determines the amount should be higher, you will have to go back to the agency and pay for an adjustment, delaying your progress.

How Bonds Affect Your Timeline and Recordkeeping

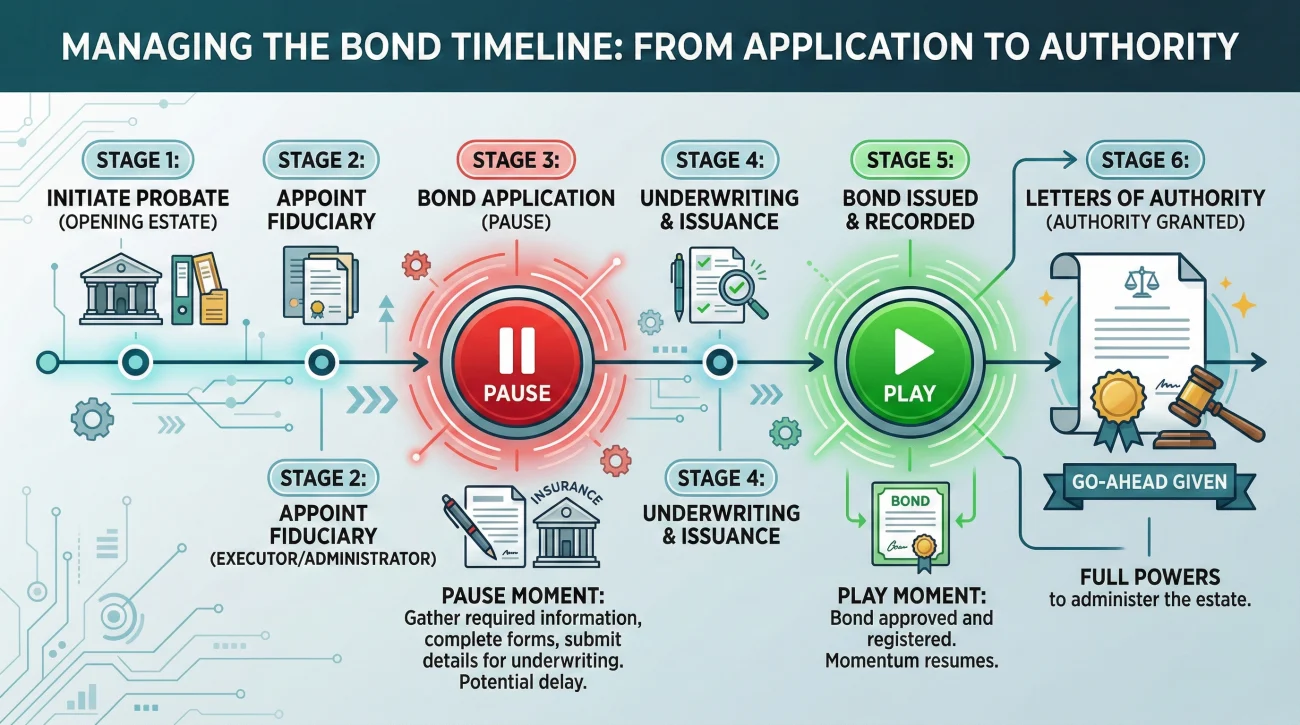

One of the biggest frustrations for executors is how a bond requirement affects the timeline. You cannot access bank accounts, you cannot sell the house, and you cannot pay estate debts until you have your legal authority. That sudden halt in progress is stressful. And if a bond is required, the court will not issue that authority until the bond is filed.

Because the bond essentially pauses your probate court checklist for executors, you need to be highly disciplined about your tracking system right now. In my workflow setups, this is the exact moment where disorganized executors start losing track of things. While you wait for the court to issue your official authority, you need to track three specific things carefully:

First, log every single phone call with the bond agency. Write down who you spoke to, what date it was, and what document they said they were waiting on. “Received but not logged” is a massive problem in this phase. The agency might receive your application but pause it because a signature is missing, and if you do not follow up, your application just sits there.

Second, track the premium payment receipt. You will likely have to pay this out of your own pocket initially because the estate accounts are frozen. Keep an immaculate record so you can handle the reimbursement later.

Third, set a calendar reminder for 11 months from now. Bonds usually have an annual premium. If the estate takes longer than a year to settle, which is very common, you will need to renew it. You should also note that if you discover a massive new asset later, you may need to update the bond coverage amount.

💡 Pro Tip: Create a dedicated physical folder (or digital folder) just for bond-related documents. Do not mix your bond application drafts in with funeral receipts or old tax returns.

Crucial Questions and Scripts

Clear communication is your best defense against endless administrative loops. When you are dealing with the court clerk and the surety company, vague questions get vague answers. You need written confirmation of what is expected.

Here is a script I often share with families when they need to ask the court clerk about the bond requirement. It is polite, neutral, and focuses on getting a paper trail.

Subject: Request for written bond requirements – Estate of [Name]

Hello Clerk’s Office,

I am currently preparing the initial documents for the Estate of [Name]. I understand a probate bond may be required before letters of authority are issued.

Could you please provide a written list of the court’s requirements for the bond, including the specific amount required and any preferred forms the court uses for submission?

I want to ensure I submit exactly what is needed to avoid any delays in your office. Thank you for your guidance.

Best regards,

[Your Name]

Notice the formula used in that script. It is a structure you should use often.

[Context of your request] + [Polite request for specific, written requirements] + [Focus on avoiding delays for them]

Once you are talking to a bond agency, you also need to ask the right questions before handing over any money. Always ask:

- “How long does your underwriting process typically take once you have all my documents?”

- “Do you file the final bond directly with the court, or do you mail it to me to submit?”

- “Is this an annual premium that needs to be renewed, or a one-time flat fee?”

That last question is critical. Many executors assume they are paying once, only to get a renewal bill a year later because the estate is still open. Knowing this in advance helps you plan your timeline and expenses.

What If You Cannot Get Approved?

This is a high-stress scenario I see occasionally. If your credit history has significant red flags, like an active bankruptcy or severe unpaid judgments, a surety company might deny your application.

If that happens, do not panic. It is not the end of the road, just a change in strategy. You have practical options. You can often ask the court to allow a co-executor with stronger credit to serve alongside you. Alternatively, you might choose to step down and let another family member or a professional administrator handle the estate. The key is to communicate openly with your attorney or the court clerk so you can pivot quickly without stalling the estate for months.

Final Thoughts on the Process

Finding out you need an executor bond can feel like an annoying detour right when you are trying to get started. It adds a layer of paperwork and a waiting period that nobody wants to deal with.

But when you break it down into manageable steps, it is just a routine administrative hurdle. Focus on gathering your basic asset snapshot, getting the exact required amount from the court in writing, and maintaining a clean, organized folder for your application materials. Once you submit that approved bond to the court, the waiting game shifts. The clerk will process the file, and shortly after, they will issue your official letters of authority. By keeping a calm, structured approach, you will secure the bond and move on to the actual work of settling the estate.

❓ FAQ

🤔 What exactly is a probate bond?

A probate bond is a specialized insurance policy required by the court. It guarantees that the person managing the estate will act ethically and distribute the assets correctly, protecting the heirs and creditors from mismanagement.

💸 Who pays for the executor bond?

The estate is ultimately responsible for this expense. Since you cannot access estate funds until the bond is officially filed, you generally advance the money yourself and log it as a formal administrative expense for reimbursement later.

⏳ How long does it take to get a probate bond approved?

If you have all your documents ready, underwriting can take anywhere from a few days to a couple of weeks. Delays usually happen when the surety company has to wait for missing signatures or an incomplete asset snapshot.

📉 Does my personal credit score affect the executor bond?

Yes, many surety companies run a soft credit check. They do not expect perfect credit, but they look for major red flags like recent bankruptcies, active judgments, or a severe history of unpaid debts.

🤷♂️ What happens if I cannot get an executor bond?

If you are denied due to credit issues, do not panic. You can often ask the court to allow a co-executor to apply with you, or you can step down and let another family member or professional take over.

📝 Is an administration bond the same as an executor bond?

Practically, yes. The term “administration bond” is usually used when there is no will, while “executor bond” is used when there is a will. Both serve the exact same purpose of protecting the estate.

⚖️ How is the bond amount set by the court?

The judge specifies this exact number in your court order, typically by calculating the estimated value of the estate’s liquid assets.

🚫 Can a probate bond be waived?

It can often be waived if the deceased person’s will explicitly stated that no bond is required, or if all the legal heirs agree in writing to waive it. However, the judge always has the final authority to demand one.

📅 When is a probate bond required during the process?

It is required at the very beginning. You typically must file the approved bond with the court before they will issue your letters of authority, meaning you cannot access accounts until it is done.

🏦 Do banks need to see the executor bond?

No, banks generally do not ask to see the bond itself. They want to see the court-issued letters of authority. The bond is just the requirement you must fulfill for the court to hand you those letters.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.