- Review and correct: Verify the spelling on your court document immediately and request a clerical amendment if you find any typos before ordering copies.

- Establish your tracking logs: Create a dedicated call log, document tracker, and decision log before you make a single phone call.

- Redirect the mail: Go to the post office in person to forward the deceased’s mail to your secure address to uncover unknown accounts.

- Obtain the estate EIN: Apply for the Employer Identification Number online via the IRS website so you are ready to open a bank account.

- Do not mix funds or sign personally: Keep personal money separate, log any out-of-pocket expenses as executor advances, and always sign documents with your official executor title.

The Reality of the Starting Line

In my experience supporting estate administration, getting the court letters feels like crossing the finish line, but it is actually the starting gun. For months, you have likely been told that you cannot move forward without official legal authority. Institutions have put you on hold, accounts have been locked, and the paperwork has piled up. Now that you hold the official document, your liability officially begins.

I often see executors rush to the bank or start making dozens of phone calls the very same day. This usually leads to lost notes, confusing email threads, and verbal agreements that institutions later deny. You have the power to act, which means you also have the responsibility to act systematically. In this guide, I will walk you through the first ten operational steps you should take after receiving letters testamentary to ensure your workflow stays clean and defensible from day one.

1. Confirm Details and Handle Document Typos

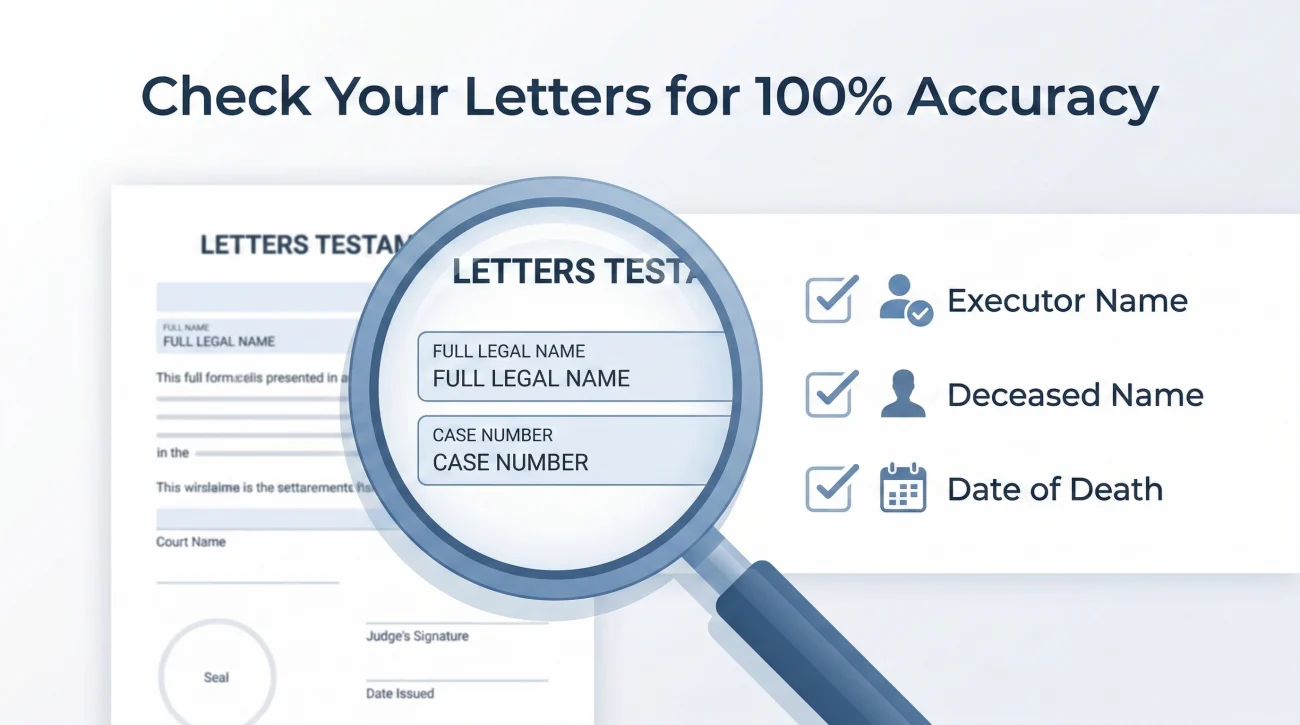

Before you use the document, you need to make sure the document itself is correct. Court clerks process thousands of forms, and simple typographical errors are incredibly common. If you send a document with a misspelled name to a strict financial institution, they will reject it, and you will have to start the process over.

Sit down with the original document and verify the exact spelling of your full legal name, the deceased person’s name, the date of death, and the case number. Every single letter must match your government-issued ID perfectly.

⚠️ Warning: Do not order your large batch of certified copies until you have verified that the master document is 100 percent accurate.

If you spot an error, do not panic. Call the probate clerk immediately and ask for a clerical amendment. This usually takes a few days to a week to process. While you wait for the corrected copy, you can safely proceed with steps two through six below. Once you know the document is perfect, order your certified copies. As a general rule of thumb, you will need one certified copy for every major financial institution, title company, and life insurance provider.

2. Set Up Your Tracking System First

This is arguably the most important operational step you will take. A common pattern I see is executors relying on their memory for the first few weeks. They call a utility company, make a mental note that the account is frozen, and move on. Three weeks later, they cannot remember who they spoke to or what was required next.

Before you pick up the phone, set up a dedicated tracking system in a binder or a digital spreadsheet. If you were appointed alongside a co-executor, decide today who will hold the physical records and how you will document joint agreement. You both carry liability, so you need a shared log.

The Three Core Logs You Need

- 📄 The Call Log: Track the date, time, institution name, phone number, representative name, and exact next steps.

- ✅ The Document Tracker: Keep a running list of what you mailed out, tracking numbers, and receipt confirmations.

- 📝 The Decision Log: Write down why you made specific administrative choices, such as why you hired a particular appraiser.

| Date & Time | Institution | Rep Name | Action Required | Status |

|---|---|---|---|---|

| Oct 12, 10:00 AM | Home Insurance Co. | Sarah M. | Send certified LOA and death cert | Pending Mail |

| Oct 12, 11:30 AM | Electric Utility | James T. | Account frozen. Wait for final bill. | Waiting |

3. Redirect the Mail In Person

Mail forwarding is your strongest tool for discovering unknown debts, final bank statements, and surprise assets. Do not rely on old tax returns alone to tell you where the deceased held accounts.

Take your certified letters, your own government ID, and a copy of the death certificate to your local post office. Fill out the formal change of address form in person to redirect the deceased person’s mail to your secure executor address. Doing this early ensures you catch automated billing notices before services are unexpectedly shut off.

4. Build the Institutions List and Prioritize

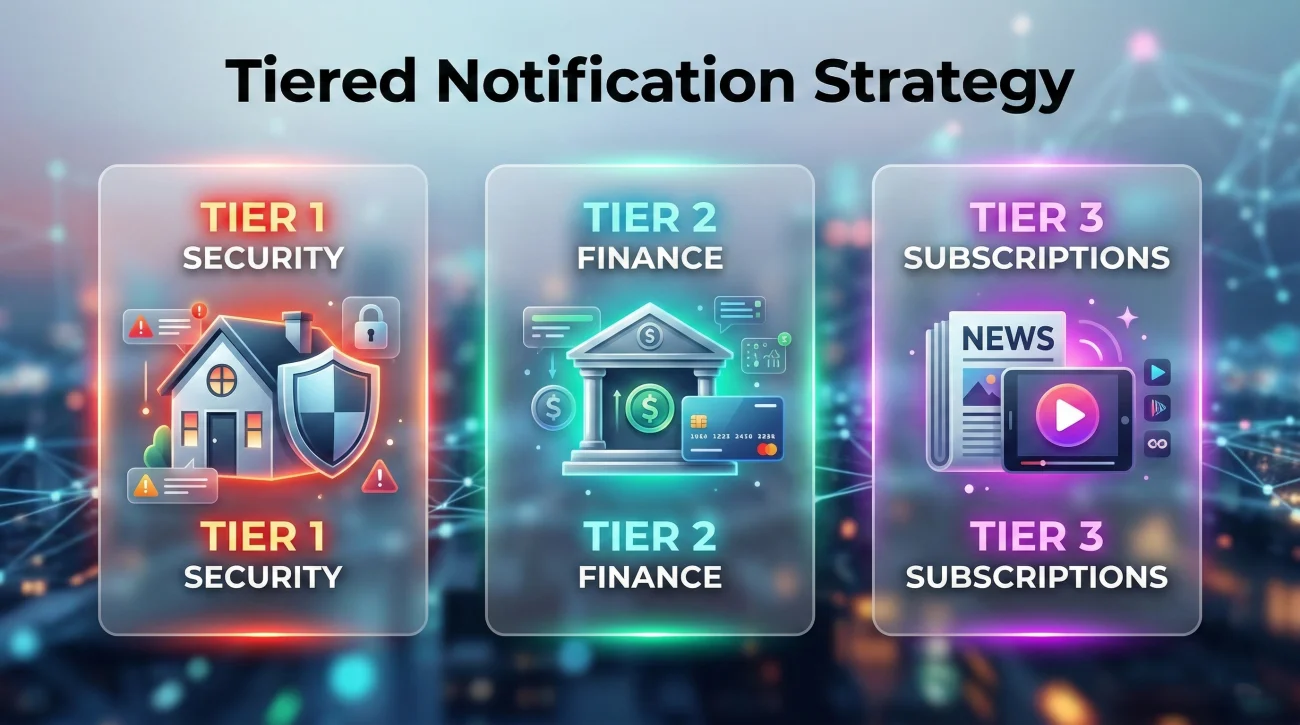

Knowing how to use letters testamentary effectively means understanding that not everything is a “day one” priority. In day-to-day admin work, the fastest wins come from securing physical property and halting automated payments. I always suggest organizing your list into three distinct tiers.

Tier 1: Property Security. Your immediate calls go to homeowners insurance, auto insurance, and local utility companies. If a house is vacant, insurance policies often change, and you need to inform them of your authority to keep coverage active.

Tier 2: Financial Holdings. Next, contact the primary banks, mortgage companies, and brokerage firms. Your goal is not to move money yet, but simply to notify them, provide your letters, and freeze the accounts to prevent fraud.

Tier 3: Subscriptions. Streaming services, magazines, and minor credit cards can wait until your second or third week.

5. Prepare Your First Call Packet

When you start making priority calls, having a reference packet sitting on your desk will lower your stress immensely. This packet should contain the deceased’s full legal name, past addresses, social security number, date of birth, date of death, and your court case number.

Key Point: Never rely on verbal instructions from a customer service representative regarding legal documents. Always ask them to email or mail you their exact requirements.

Here is a safe, polite script you can use when making these initial notification calls:

Verbal Request Script:

“Hello, I am calling to report the passing of [Name] and I am the appointed executor. I have my court letters ready. Before I send anything, could you please email me a written checklist of the exact documents your department requires to update the account, along with the secure mailing address?”

6. Obtain the Estate EIN (Tax ID)

You cannot simply walk into a bank with your letters and open an estate account. You must first obtain an Employer Identification Number (EIN) from the IRS, which acts as the social security number for the estate itself.

The fastest way to do this is to apply online via the official IRS website. If you have a valid Social Security Number yourself, the online process usually takes about fifteen minutes, and you will receive the EIN document immediately in PDF format. You can also file Form SS-4 by fax or mail, but that can take several weeks. Never pay a third-party service to acquire an EIN for you; the process is completely free through the government.

7. Prepare for the Estate Bank Account

With your EIN in hand, you are ready to separate the estate’s money from your personal money. Treat the estate bank account as the central hub for all financial activity. Every penny belonging to the deceased goes into this account, and every legitimate estate expense is paid out of it.

You also have a practical decision to make: choosing the right bank. In my experience, opening the estate account at the same bank where the deceased already held their primary checking account is often the smoothest route, as internal transfers between their old account and the new estate account require less paperwork. However, if their bank was a small local branch lacking a dedicated estate department, do not hesitate to open the account at a different, larger institution that truly understands the probate process.

Gather the death certificate, your certified letters, your ID, and your new EIN document. Call the bank ahead of time to make an appointment with the estate department, as regular tellers often cannot open these specialized accounts. For a detailed breakdown of this step, review our executor banking checklist.

8. Secure Digital and Online Assets

Modern estates consist of more than just physical bank accounts. Email accounts, social media profiles, digital subscriptions, and cryptocurrency wallets are often overlooked during the first week.

Focus on securing the primary email account first, as it serves as the password reset hub for almost everything else. Look for apps like PayPal or Venmo on the deceased’s devices to ensure funds are not sitting in digital limbo. Most tech platforms have dedicated memorialization or closure teams that require a copy of your letters and the death certificate to grant you official access.

9. Start Inventory and Valuation Tracking

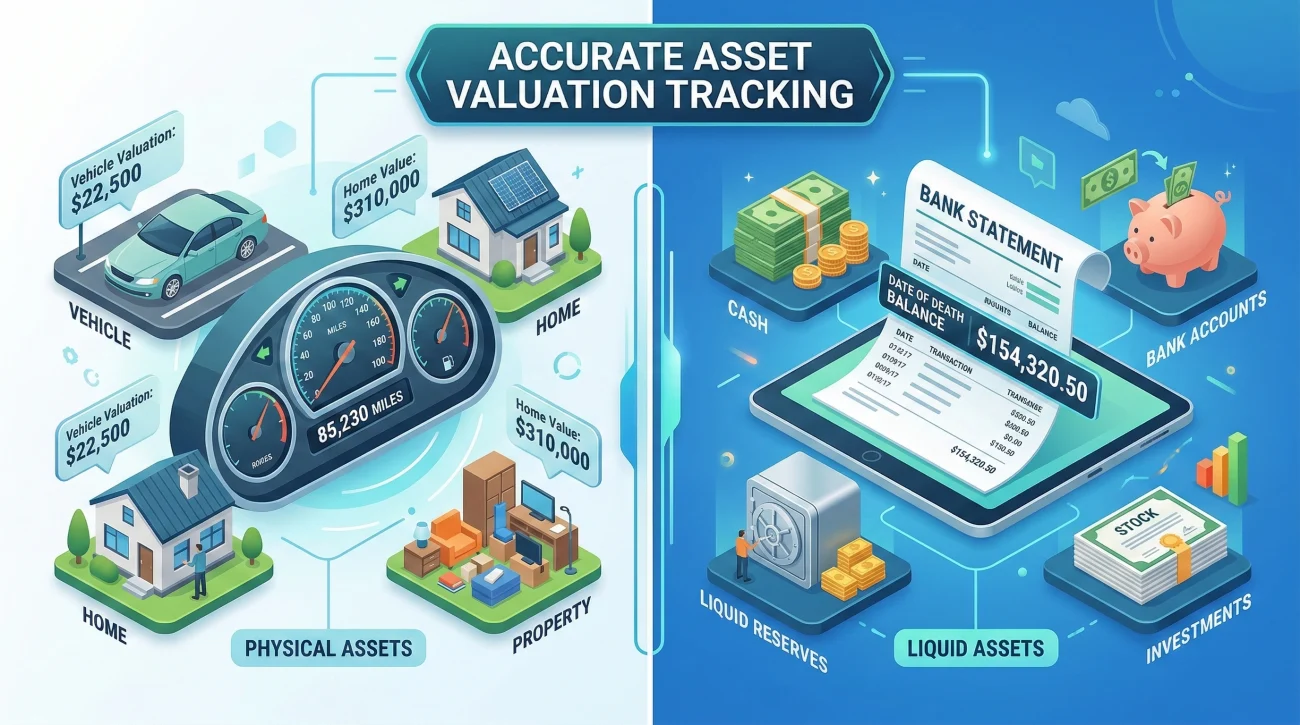

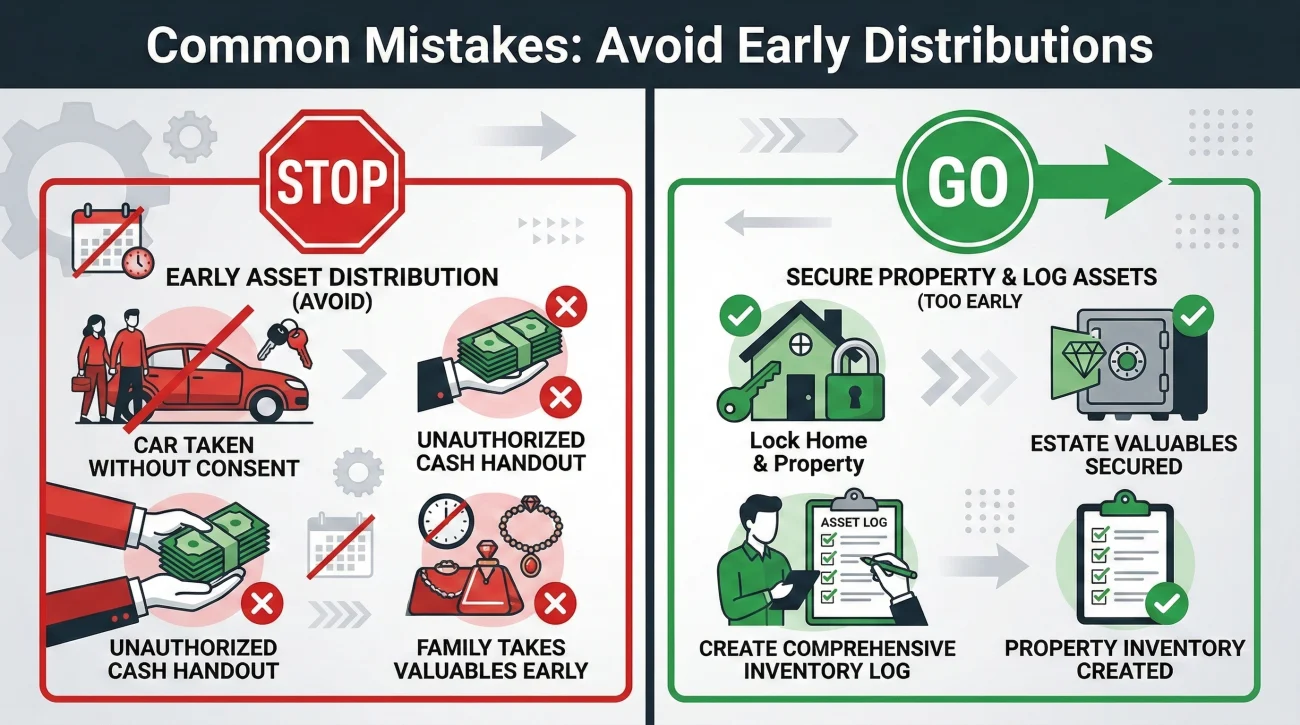

Once the banking and communication foundations are laid, you can safely begin mapping out the estate’s value. Secure the physical property and check usual hiding spots for cash or valuables. In my field notes, I often see families overlook items stashed inside hollowed books, hidden within old coat pockets, tucked behind picture frames, or locked in small fire safes in the basement.

You also need to log the exact mileage on any vehicles immediately. Do not just write down the make and model. You need the specific odometer reading because formal vehicle valuation tools require it to calculate the precise worth of the car on the day the person died. If you wait months to check the mileage, or if a family member drives the car in the meantime, your inventory valuation will be completely inaccurate.

Create a spreadsheet specifically for assets. When you send your letters to a bank or brokerage, your request must explicitly ask for the “Date of Death Balance.” This exact figure is required for your court inventory and tax filings. For a structured approach to cataloging these items, refer to our estate asset inventory checklist.

10. Track Expenses and Necessary Bills

As soon as you receive your letters, you might feel pressure to start paying off the deceased’s credit cards. Stop. Not all debts are paid immediately, and some may not be paid at all if the estate lacks funds.

Your immediate focus is on preservation expenses: the mortgage, property taxes, homeowners insurance, and essential utilities. If you must use your personal funds to keep the power on before the estate account is officially open, document it meticulously as an “executor advance.” You will reimburse yourself from the estate later.

Put credit card and medical bills in a folder labeled “Debts to Review.” To understand how to organize claims safely, read our executor creditor debt checklist.

When communicating with a creditor early on, keep it brief and entirely in writing:

Subject: Notification of Death – Account ending in [1234]

To Whom It May Concern,

I am writing to formally notify you of the passing of [Name]. I have been appointed as the executor. Please freeze this account to prevent further charges. Kindly send a final statement showing the date of death balance to my mailing address below. I will contact you regarding the claims process once the estate inventory is complete.

Sincerely,

[Your Name]

Executor for the Estate of [Name]

Common Mistakes Right After Receiving Letters

In the rush to get things done, new executors often make procedural errors that cost them weeks of delay later on. Being aware of these traps early on is half the battle.

Mistake: Signing documents as an individual. Always sign contracts or bank forms as “Your Name, Executor for the Estate of Their Name.” Signing just your name can make you personally liable for the agreement.

Mistake: Distributing assets too early. Family members often ask for an advance on their inheritance the moment they hear you have the letters. Do not hand out assets. Your current job is to secure and inventory. Distributions happen at the very end of the process.

Mistake: Mingling communication channels. Do not use your personal everyday email address for estate business. It is incredibly easy to lose an important tax document among personal newsletters. Set up a free email address dedicated entirely to executor duties.

Calling a bank, writing a generic phone number on a sticky note, losing the note, and having to call back to explain the entire situation to a new representative.

Calling the bank, logging the reference number and the representative’s ID in your master spreadsheet, and ending the call by asking them to email you the next steps.

Final Thoughts on Pacing Yourself

Holding the letters testamentary gives you the authority to manage the estate, but it does not mean you have to solve every problem in the first forty-eight hours. Estate administration is a marathon, not a sprint. By focusing your first few days purely on setting up a solid tracking system, ordering your certified copies, and making the most critical property security phone calls, you are building a defense against administrative delays.

Take it one checklist at a time and always ask for requirements in writing. For a broader view of how these initial steps fit into your overall legal authority, review our main probate court checklist for executors.

As you begin your work, you will likely encounter situations that fall outside the standard checklist. Below, I have answered a few unique scenarios I often discuss with new executors.

❓ FAQ

🚗 Can I drive the deceased’s vehicle to keep it running?

You should only drive the vehicle for necessary estate maintenance, such as taking it to a mechanic or preparing it for sale. Ensure the auto insurance policy is active and covers non-owner drivers before putting the key in the ignition.

✈️ Can I get reimbursed for travel expenses to the courthouse?

Yes, reasonable out-of-pocket expenses directly related to administering the estate, such as flights, gas, or hotel stays for court appearances, are typically reimbursable from estate funds if you keep meticulous receipts.

🗺️ What if I discover the deceased owned property in another state?

Your current letters likely only grant authority in the home state. You will usually need to open a secondary process, known as ancillary probate, in the other state to handle real estate located there.

🧾 Do I need to hire a CPA on the very first day?

While hiring a tax professional is highly recommended for filing the final personal returns and estate tax returns, you do not strictly need them on day one. Focus on getting your EIN and gathering financial statements first.

🐕 How do I legally handle the deceased’s pets?

Pets are legally considered property of the estate. Your immediate duty is to ensure they are physically cared for. You can use estate funds to pay for their food and veterinary care, provided you log the expenses.

📜 What happens if I find a newer will after receiving my letters?

Stop any major administrative actions immediately. You must notify the probate court clerk and your attorney about the newly discovered document, as it could revoke your current authority.

☂️ Do life insurance payouts go into the new estate bank account?

Typically, no. If the life insurance policy has a specific named beneficiary, the funds pass directly to that person outside of the probate process and should not be mingled with estate funds.

🏠 What if a family member refuses to leave the deceased’s house?

Do not attempt to change the locks on an occupant or forcefully remove them yourself. You will likely need to follow formal legal eviction procedures, and consulting an attorney is highly advised in this scenario.

🔍 How do I find financial accounts if there is no paper trail?

In addition to monitoring forwarded mail, review the deceased’s past tax returns for interest or dividend income sources, and search the state’s unclaimed property database under their name.

📉 Is my personal credit score affected by the estate’s debts?

No, the estate’s debts belong to the estate. Your personal credit will not be impacted unless you personally co-signed a loan with the deceased or inappropriately mingled your funds.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.