- The core purpose: Letters of administration are the official court document that proves you have the legal authority to manage an estate when there is no will.

- The main unlock: This single document shifts your status from “family member” to “legal administrator,” forcing banks, insurers, and utilities to speak with you.

- The exemptions: Not everything requires court authority. Joint accounts and accounts with named beneficiaries (like payable-on-death) bypass this process.

- The protection rule: Never mail your only original certified copy to an institution. Always ask if they can accept a clear photocopy or a digital scan first.

- The tracking habit: Keep a detailed log of every institution that requests a copy, who you sent it to, and when they confirmed receipt.

The Reality of Hitting the Document Wall

In my experience helping families navigate the paperwork left behind after a loss, one of the most stressful moments happens at the bank teller’s window. You bring the death certificate, your ID, and maybe some mail proving your relationship to the person who passed away. You explain the situation calmly. But the teller shakes their head and says they cannot access the account or even tell you the balance.

They inevitably tell you that the bank asks for letters of administration before they can do anything. For many first-time administrators, this is a highly frustrating roadblock. It feels like the institution is being unnecessarily difficult during an already painful time.

I always tell people to take a breath here. The bank is not actually trying to block you personally. They are following strict privacy and liability rules. Without a will to point to, nobody has default legal authority over those accounts. The institution needs an official, undeniable permission slip from the local court telling them exactly who is in charge. That permission slip is what we are going to cover in detail today.

My goal is to walk you through what are letters of administration, what they actually prove to the outside world, and how you will use them practically to unlock the estate’s assets.

Letters of Administration Meaning: The Court’s Permission Slip

When someone passes away without a valid will, the legal term is that they died “intestate.” Because there is no written document naming an executor, the local court has to step in and appoint someone to handle the business side of the estate. The person they appoint is called the administrator of estate.

The letters of administration is the physical document the court issues to you once you are officially appointed to that role. It is your ultimate proof of authority.

Key Point: Despite the name, this is not a traditional “letter” typed out like correspondence. It is a formal, standardized court order, usually bearing a raised or colored seal from the court clerk, validating your legal power to act on behalf of the deceased person’s estate.

I often see families assume that being the closest living relative automatically gives them control. Unfortunately, in the eyes of financial institutions, biological relationship does not equal legal authority. The letters bridge that gap. Once you have this document in your hand, you speak for the estate.

💡 Pro Tip: Keep in mind that probate processes are governed by state law. While many states follow similar frameworks like the Uniform Probate Code, your local jurisdiction might use slightly different terminology, such as “Letters of Representation” or offer simplified affidavits for very small estates. Always verify the exact document name with your local probate clerk.

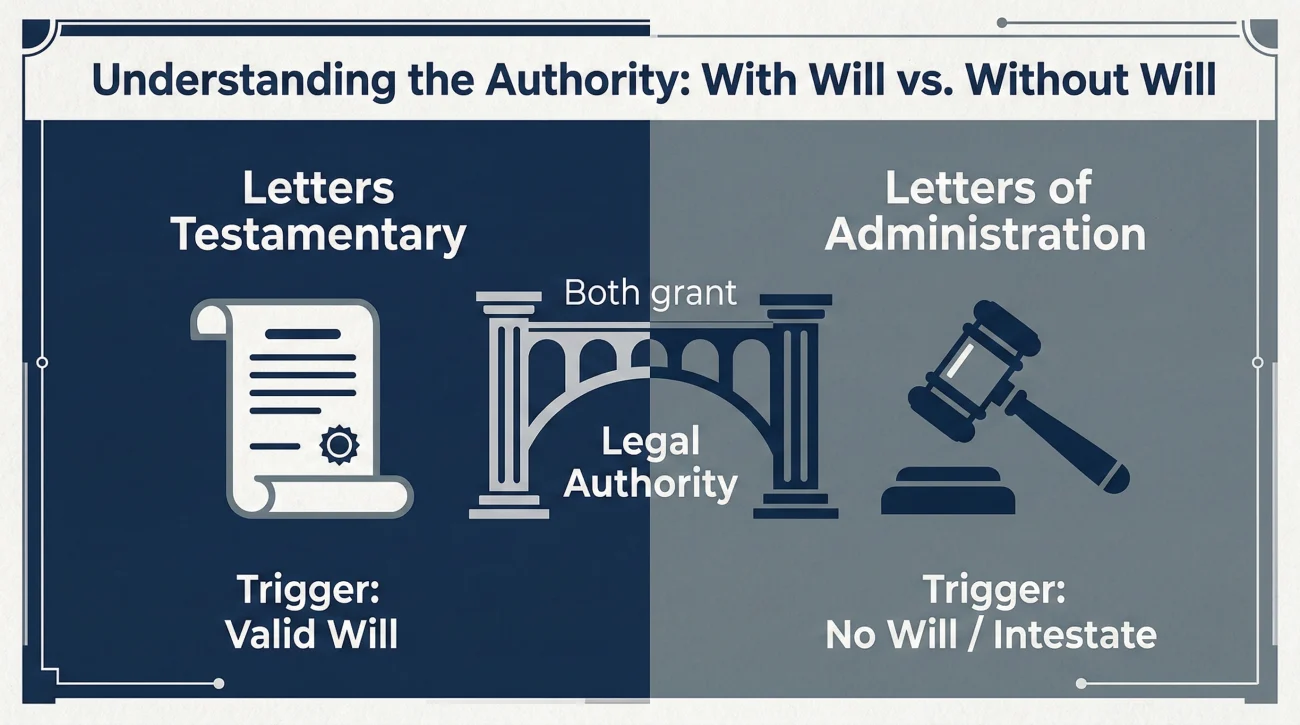

Letters of Administration vs Letters Testamentary

If you are researching this topic, you will frequently see two very similar terms grouped together. Understanding the difference between letters of administration vs letters testamentary is straightforward once you know the trigger for each.

Issued when there is a valid will, and the court is confirming the executor named in that will.

Issued when there is no will, or the named executor is unable to serve, and the court appoints an administrator.

In day-to-day admin work, the practical power of both documents is essentially identical. A bank or an insurance company will treat an administrator with letters of administration exactly the same way they treat an executor with letters testamentary. The difference only matters to the court during the initial appointment phase.

What This Document Authorizes in Practice

Having the title of administrator of estate sounds formal, but what does it actually allow you to do on a Tuesday morning when you are trying to sort out a messy desk full of bills?

At a high level, the letters prove to third parties that you have the right to gather information, consolidate money, and close accounts. I find it helpful to look at the exact operational changes this document creates.

| Without Letters of Administration | With Letters of Administration |

|---|---|

| Cannot view bank balances or transaction history. | Can request full statements and transfer funds to an estate account. |

| Cannot cancel or transfer vehicle titles. | Can sign title transfer paperwork at the local DMV equivalent. |

| Cannot claim life insurance without a named beneficiary. | Can claim policies that default to the estate. |

| Cannot access safe deposit boxes. | Can inventory and empty safe deposit boxes legally. |

It is important to remember that while the letters give you the power to gather assets, they also obligate you to handle the estate’s debts before distributing anything to heirs. You are stepping into the financial shoes of the person who passed away, with a duty to settle their affairs cleanly.

Assets That Do Not Require Letters

A frequent misconception is that you need court authority for every single asset. In reality, many assets bypass the probate process entirely. If a bank account is held in joint tenancy with another person, or if it has a Payable on Death (POD) beneficiary listed, the money transfers directly to the survivor outside of the estate. The same applies to IRAs or life insurance policies with living, named individuals. You will generally only need a death certificate and your personal ID for these accounts, saving you significant time.

The Big Misconception: Acting Before the Letters Arrive

A common trap I see is people trying to jump the gun. You might know you are going to be appointed as the administrator, so you start taking actions, like selling the deceased person’s car to a neighbor or writing checks from their account to pay funeral expenses, before the court has officially issued the letters.

You cannot legally act on behalf of the estate until the document is physically in your hands. Doing so can lead to massive personal liability and complicate the entire process. If you sign a legal document before you have authority, that signature is generally invalid.

However, this does not mean you have to sit idle while waiting for the court. There are entirely safe, organizational steps you can take during the waiting period. You can secure physical property, forward the mail, and start building a list of assets and bills based on the paperwork you find. You are simply organizing information, not moving money or changing ownership.

Where It Gets Used: Your Real-World Touchpoints

Once the court clerk hands you your certified copies, you will start deploying them across various institutions. Over the years, I have noticed distinct patterns in how different industries handle this document.

Banks and Financial Brokerages

Financial institutions are the strictest gatekeepers. When a bank asks for letters of administration, they are usually looking for a certified copy, not just a standard photocopy. They will use your letters to close the deceased person’s individual accounts and help you open a dedicated estate checking account. This new account becomes the central hub where you will deposit incoming checks and pay out legitimate final bills.

Insurance Companies

If a life insurance policy has a specific person listed as the beneficiary, the letters are rarely needed; the money goes directly to that person. However, if the estate itself is the beneficiary, or if the named beneficiary has also passed away, the insurance company will demand your letters before they release the payout.

Real Estate and Title Companies

If the deceased person owned a home solely in their name, you cannot list it for sale, sign a deed, or transfer ownership without proving your authority. Title companies will scrutinize your letters closely to ensure the chain of ownership is legally sound before closing a sale.

Retirement Accounts and Digital Assets

Modern estates often include 401(k) accounts, cryptocurrency platforms, and extensive digital footprints. If a retirement account lacks a living beneficiary, the administrator must step in to manage it. Furthermore, major tech companies now have dedicated legacy contact portals where your court document is strictly required to access, memorialize, or shut down online accounts.

Utility Companies

Closing out the electric bill, cell phone plan, or internet service used to be simple, but many companies have tightened their protocols. While some may only ask for a death certificate, many will ask for a copy of your letters to waive early termination fees or release account history. For these lower-risk accounts, a standard scanned copy of the document is often enough.

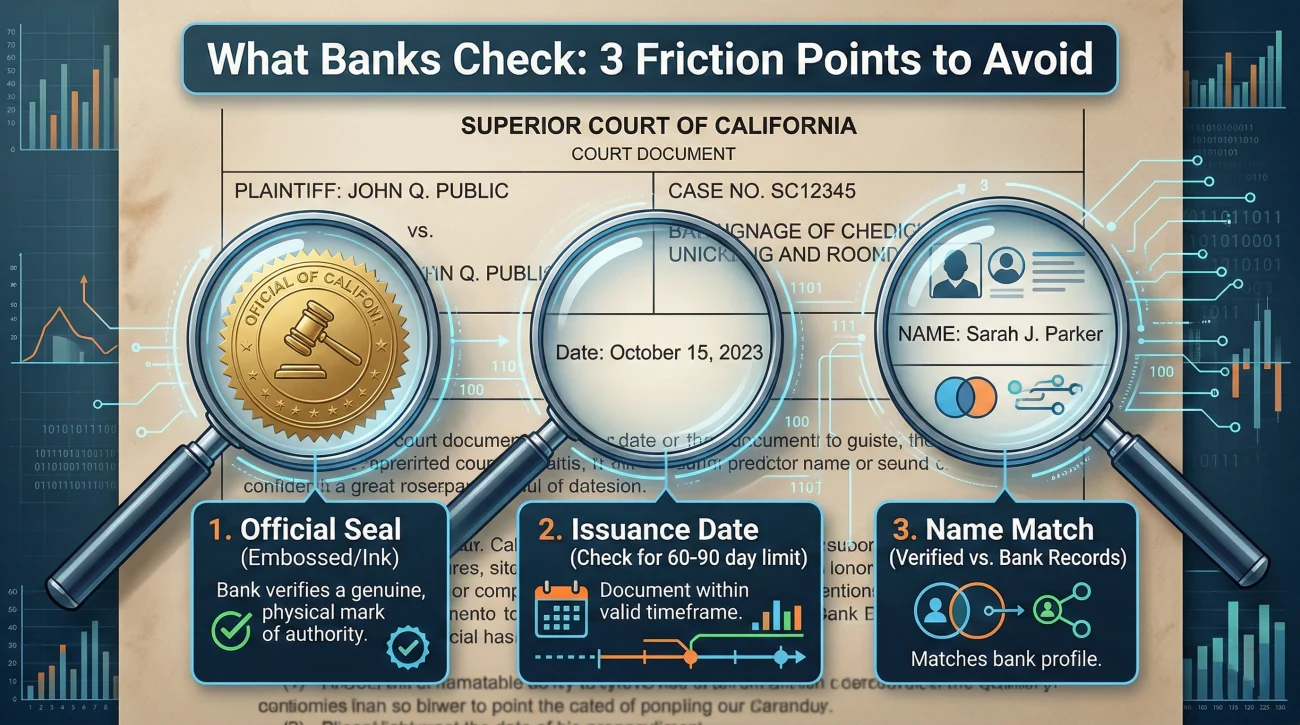

What Third Parties Actually Verify on the Document

When you slide your document across the desk or upload it to a secure portal, the clerk on the other side is looking for very specific details. Knowing what they check can save you hours of back-and-forth delays.

- 🔎 The Official Seal: Most institutions require a “certified” copy. This means the document has a raised, embossed seal or a colored ink stamp directly from the court clerk. A standard black-and-white photocopy from your home printer will usually be rejected by major banks.

- 🗓️ The Issuance Date: This is a massive friction point. Many financial institutions have internal policies stating they will only accept letters issued within the last 60 to 90 days. If your probate process drags on for a year, you may need to go back to the court to pay for freshly dated, updated copies.

- 📝 Name Matching: The name on the account must closely match the name of the deceased on your letters. If the bank account is under “William J. Smith” but your court document just says “Bill Smith,” the legal department might pause the process.

⚠️ Warning: Do not assume every institution needs an original certified copy to keep. Always ask if they can examine the certified copy and make their own photocopy for their records, returning your original. Certified copies cost money, and you want to conserve them.

How Many Certified Copies Should You Request?

When the court finally approves your appointment, they will ask how many certified copies you want to purchase. Based on real-world workflow, a practical rule of thumb is to request 10 to 15 copies upfront. While it costs a bit more on day one, it prevents the severe frustration of having to drive back to the courthouse, wait in line, and pay again when you inevitably discover hidden accounts or deal with stubborn corporate offices that refuse to return your originals.

Communication Hygiene When Submitting Your Letters

One of the most common ways timelines slip is during the submission of these documents. A family member mails a certified copy to a corporate processing center, and a month later, the institution claims they never received it. This creates a highly frustrating missing document loop.

To avoid this, I strongly recommend bringing a structured, tracking-first approach to all your communications. Never send a document into a black hole without a paper trail.

Script: Asking for Submission Requirements

Before mailing anything, send an email or make a call to clarify exactly what the institution needs and how they want it delivered.

Subject: Document submission requirements for the Estate of [Deceased Name] – Account ending in [1234]

Hello [Name/Department],

I am the appointed administrator for the estate of [Deceased Name]. I am prepared to submit the court-issued letters of administration to update your records.

Before I send the files, could you please confirm in writing:

1. Do you require a physical certified copy with a raised seal, or can you accept a clear digital PDF scan?

2. If a physical copy is required, what is the exact mailing address and attention line I should use?

Thank you for your guidance,

[Your Name]

Administrator for the Estate of [Deceased Name]

Script: Following Up on Submitted Documents

If you have mailed a physical copy, always use certified mail with a tracking number. Set a calendar reminder to follow up exactly 7 days after the tracking shows it was delivered.

Subject: Status check: Letters of administration submitted for Estate of [Deceased Name]

Hello [Name/Department],

I am writing to request a status update on the account for the late [Deceased Name].

Tracking records show that the certified letters of administration were delivered to your processing center on [Date] at [Time]. Could you please confirm that the documents have been attached to the file and advise on the next steps to access the account?

Thank you,

[Your Name]

Using polite, factual, and timeline-based language removes the emotion from the process and gently forces the institution to look up the tracking data rather than giving you a generic “we are still processing” response.

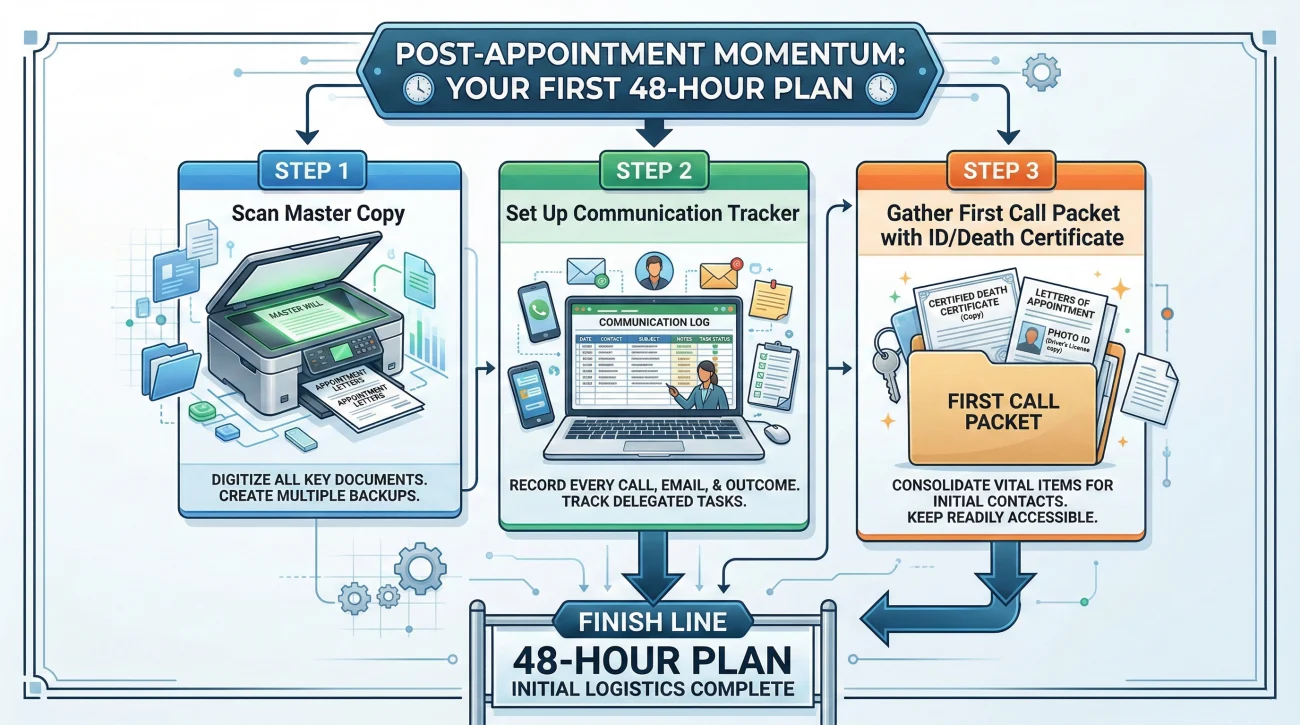

After the Letters Arrive: Your Next Actions Checklist

The day the court clerk hands you the physical documents is a major milestone. But it is also the starting line for the real administrative work. To prevent feeling overwhelmed, you need to channel that momentum into setting up a clean, organized workspace.

Here is what you should do in the first 48 hours after receiving your letters:

- 📄 Scan a master copy immediately. Before you mail anything out, scan the cleanest, flattest version of the certified copy into your computer. Name the file clearly, such as “2024-05-15_Letters_of_Administration_Estate_of_Smith.pdf”. This digital file will be used for 80% of your vendor communications.

- 📂 Set up your tracker. Start a simple spreadsheet or a dedicated notebook to log every single phone call and document mailed. If you send copy #3 to the life insurance company, note the date and the tracking number.

- 📞 Build the first call packet. Gather the letters, the death certificate, and the deceased’s social security number. Keep them in a single, accessible folder on your desk. You will be asked for information from these three items on nearly every phone call.

Once your desk is organized, you are ready to start dealing with the broader probate system. For a complete guide on how to interact with the court and manage your overarching responsibilities, I highly recommend reviewing our complete probate court checklist for executors. It will help you map out the entire road ahead, keeping you focused on one phase at a time.

Final Thoughts on Protecting Your Authority

Taking on the role of administrator is a heavy lift, often done while you are still actively grieving a personal loss. It is completely normal to feel overwhelmed by the sheer volume of paperwork and the bureaucratic walls that institutions seem to put up at every turn.

Remember that the letters of administration are your ultimate tool to tear down those walls. Treat these certified copies like high-value inventory, track every single piece of mail you send out, and build a paper trail for every conversation. Finally, if the estate becomes contested or feels too complex to handle alone, do not hesitate to consult a local probate attorney. You do not have to have all the answers on day one; you just need to protect your authority and take the process one organized step at a time.

❓ FAQ

🏦 What are letters of administration?

They are an official court document issued to an appointed individual, granting them the legal authority to manage and settle the estate of someone who passed away without a valid will.

📜 Why does the bank ask for letters of administration?

Banks are legally bound by privacy and liability laws. They require this document to prove that the court has authorized you specifically to access the deceased person’s funds and account history.

⚖️ Can I get letters of administration without a lawyer?

In many simple estates, you can apply for the document yourself through the local probate court clerk’s office. However, complex estates or family disputes often make professional guidance necessary.

💵 How much does a letter of administration cost?

There is no single flat price. Costs depend entirely on your local court’s filing fees and the fees they charge for generating certified copies. You can usually find the fee schedule on the county court website.

⏳ Do letters of administration expire?

While the actual court authority remains intact, many banks have internal rules requiring the document’s issuance date to be within the last 60 to 90 days. Check with the institution before submitting your paperwork.

🤝 What is the difference between an executor and an administrator?

An executor is chosen by the deceased person in their will. An administrator is appointed by the court when there is no will. Functionally, their daily administrative duties are nearly identical.

🏠 Can I sell a house with letters of administration?

Yes, typically this document provides the authority needed to sign real estate transfer paperwork on behalf of the estate, though title companies will review the court orders closely before allowing the sale to close.

📅 How long does it take to get letters of administration?

Timelines vary wildly by county, ranging from a few weeks to several months. Factors like court backlogs, mandatory waiting periods, and the complexity of locating heirs can heavily influence the speed.

✉️ Who can apply for letters of administration?

Courts generally follow a priority list defined by local rules, usually starting with the surviving spouse, followed by adult children, parents, and then siblings.

🚫 What if the bank refuses my letters of administration?

Ask for their refusal reason in writing. Often, the refusal is due to a technicality, such as a name mismatch, a missing raised seal, or an issuance date that is too old for their internal policies. Once you know the exact issue, you can correct it.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.