- The permission slip: Letters Testamentary are the official court documents proving a judge has validated the will and granted you legal authority.

- Why a will is not enough: Financial institutions require court documents to shield themselves from liability before releasing account access or funds.

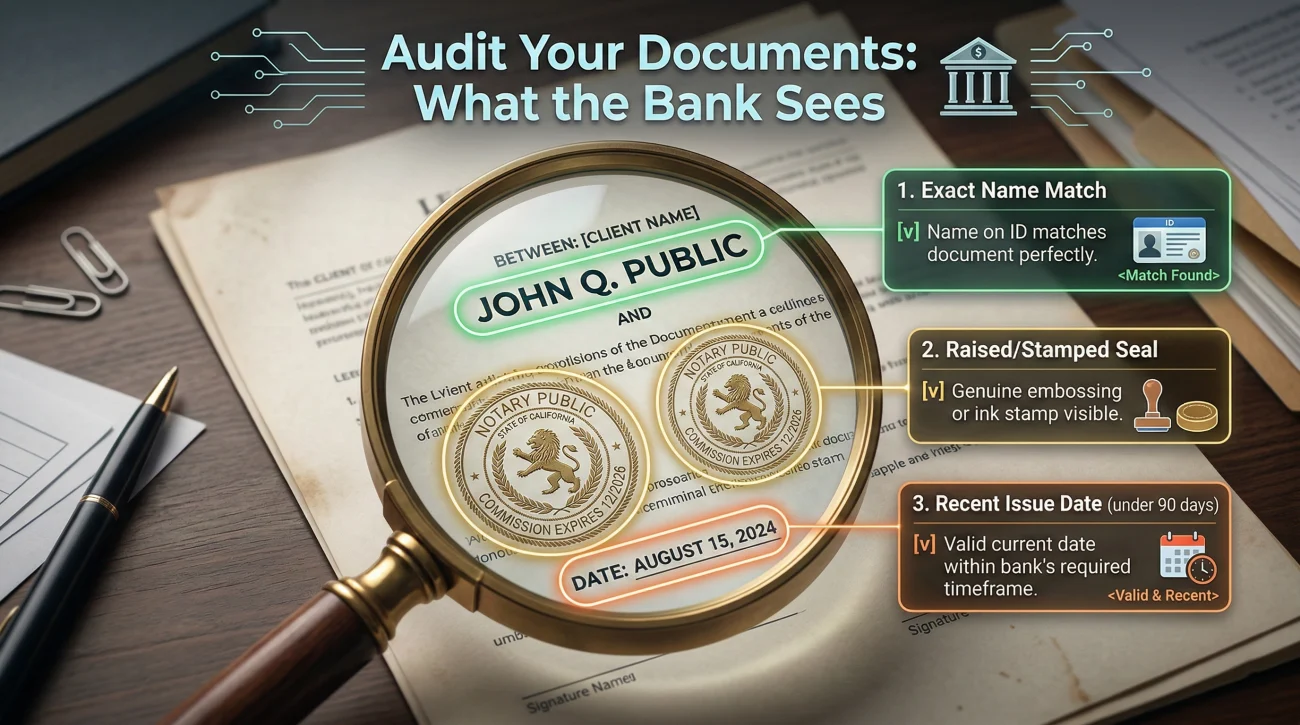

- What desk workers verify: Third parties typically check for your exact name, the raised or colored court seal, and an issue date within the last 60 to 90 days.

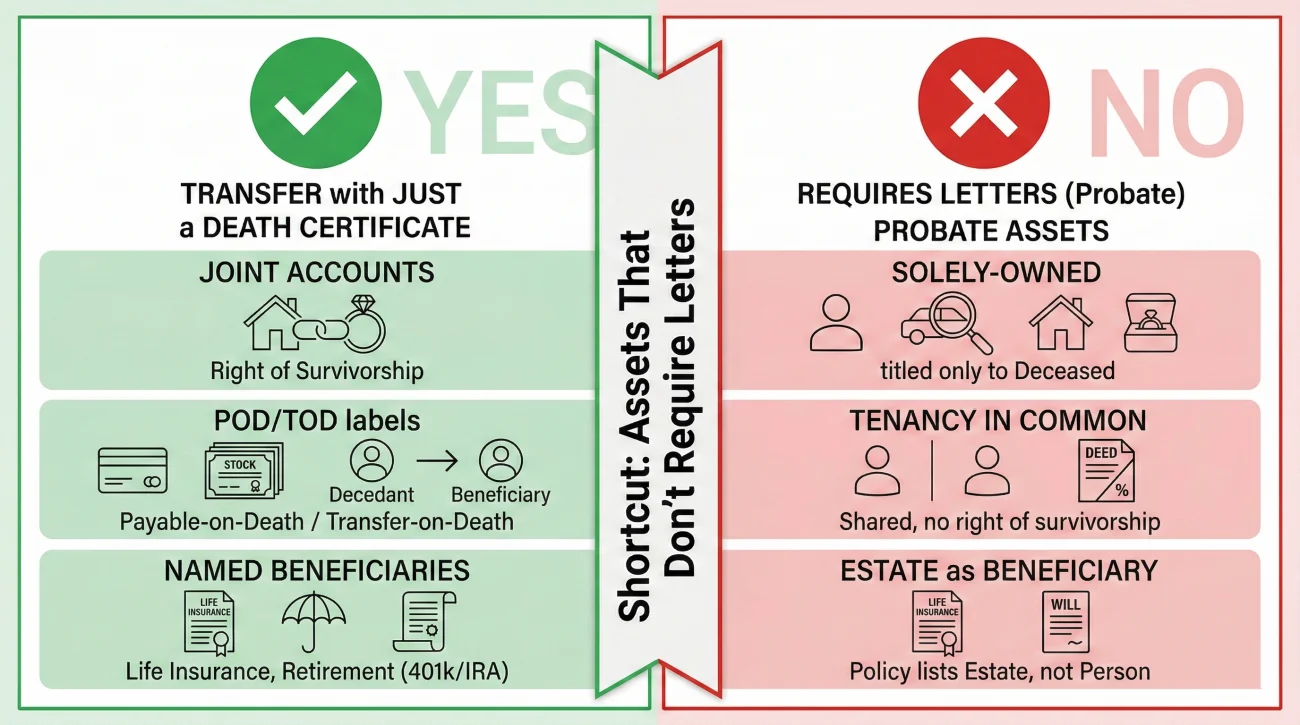

- Not all assets require them: Accounts with designated beneficiaries, payable-on-death (POD) labels, or joint owners usually bypass the need for these letters entirely.

- Keep a tracking log: Certified copies cost money. Treat them like numbered keys, log exactly where you send them, and never mail your final physical copy.

The Moment The Will Is Not Enough

In my experience helping families organize estate files, there is a very common scenario that plays out at bank branches every single day. You walk up to the desk with a neat folder. Inside, you have the original will, an original death certificate, and your identification. You are ready to close out an account or set up an estate checking account. You hand over the paperwork, expecting to move forward.

The desk worker looks at the will, hands it back to you, and politely says, “I am sorry, but we cannot do anything until you bring us the Letters Testamentary.”

If this is your first time managing an estate, this moment can feel incredibly frustrating. You are explicitly named in the document. The intent of the deceased is clear. Why is the institution putting up a roadblock?

I frequently see executors get stuck in a loop of confusion here because they believe the will itself grants them immediate power. In reality, a will is simply a blueprint. It tells everyone what the deceased person wanted, but it does not actually hand you the tools to build the house. To unlock accounts, speak to insurers, and manage physical assets, you need court-issued proof that you are the person legally approved for the job.

My goal here is to help you understand exactly what this document does, how to get it, what the person across the desk is actually looking for, and how to organize your files so you can clear these institutional hurdles smoothly.

How You Actually Obtain the Letters

A common misconception is that you can simply walk into a courthouse, show the clerk a will, and walk out with your letters five minutes later. The reality requires a formal legal process.

Before any document is issued, you must file a petition with the local probate court requesting to open the estate. The court then schedules a hearing or a review period. During this time, the judge validates the will, ensures no immediate red flags exist, and confirms you are fit to serve. Only after the judge signs the official order approving your appointment will the clerk’s office generate your Letters Testamentary.

Depending on your local jurisdiction, the exact terminology might vary. While many courts use the term “Letters Testamentary”, some states refer to this exact same document as “Letters of Authority” or “Letters of Personal Representative”. Regardless of the specific title printed at the top, the function remains identical.

What The Document Actually Proves

Despite the slightly confusing name, Letters Testamentary are not actually letters written by you, nor are they letters written by the deceased person. They are an official decree issued by a probate court.

When an institution asks for this document, they are asking for a specific, standardized proof of authority. Handing this document to a representative proves three distinct facts immediately.

First, it proves that the court has formally recognized the death and accepted the will as the valid, final version. Second, it proves that you are the specific individual the court has appointed to serve. Third, it proves that your authority is currently active.

Key Point: You can think of the will as the map and the Letters Testamentary as the keys to the vehicle. The map tells you where to go, but you cannot actually start driving until the court hands you the keys.

In daily administration work, I often advise people to treat this document like a corporate ID badge. If you do not have your badge, security will not let you into the building no matter how much you insist you work there. Once you clip the badge on, doors open for you automatically.

Why Institutions Reject the Will Alone

It is very common to wonder why financial institutions are so stubborn about this requirement. From the outside, it feels like unnecessary bureaucracy. From the inside of a financial institution, it is entirely about liability and risk management.

Imagine a scenario where a bank accepts a will that a family member found in a desk drawer. The bank releases the funds. Two weeks later, another family member shows up with a newer will signed five years later, naming a completely different executor. If the bank gave the money to the first person, the bank could be held financially responsible for that error.

Institutions are not in the business of interpreting legal documents or deciding which version of a will is the final one. They rely entirely on the court system to do that verification. They require Letters Testamentary because it completely removes their liability. The document tells them the court has made the final decision, and they are safe to release information and funds to you.

Institutions view you as a well-meaning relative, but legally, you are a third party with no rights to access private financial data.

Institutions view you as the legal continuation of the deceased person for financial purposes.

Understanding this mindset shift helps reduce the friction when you make your calls. You are not fighting the bank. You are simply waiting to provide them with the liability shield they are required to have.

When You Do Not Need Letters Testamentary

It is important to note that not every asset requires a court document to transfer. In fact, a significant portion of modern wealth bypasses the probate process entirely.

If the deceased person set up accounts with clear beneficiary designations, those assets usually transfer automatically outside of probate. Common examples include life insurance policies with a named living beneficiary, retirement accounts, or bank accounts labeled Payable on Death (POD) or Transfer on Death (TOD). Similarly, property held in joint tenancy with the right of survivorship typically transfers to the surviving owner with just a death certificate.

Additionally, if the total value of the estate is very small, many jurisdictions offer a “small estate affidavit” process. This allows families to claim basic assets without ever opening a formal probate case or requesting Letters Testamentary. Always check your local court guidelines before assuming full probate is required.

Where You Will Use This Document

For the assets that do not bypass probate, this document becomes the centerpiece of almost every administrative task you perform. You will pull it out of your folder frequently. Here is a high-level look at where this document gets used in practical workflows.

| Institution Type | What The Letters Unlock |

|---|---|

| Banks and Credit Unions | Accessing account balances, freezing automatic payments, and transferring funds into an estate account. |

| Life Insurance Companies | Filing claims if the estate itself is named as the beneficiary, or gathering policy values for your inventory. |

| Title Companies | Clearing the title so you can legally list or sell real estate owned by the deceased person. |

| Investment Brokerages | Accessing stock portfolios, mutual funds, and managing the transfer or liquidation of those assets. |

| Government Agencies | Processing final tax filings or resolving queries with federal and state revenue departments. |

Knowing where you will use them is only half the battle. The other half is knowing exactly what the person processing your request is looking for when you hand the document over.

What The Desk Worker Is Actually Verifying

When you hand your paperwork to a clerk, a teller, or mail it to a back-office processing center, they do not read the document like a book. Instead, they are trained to scan for specific visual cues and data points.

I have seen many document packets get rejected simply because the executor did not know what the reviewer was verifying. Knowing their checklist helps you audit your own documents before you send them.

💡 Pro Tip: Before you leave the courthouse or close the envelope to mail your documents, verify these three elements yourself.

Exact Name Matches

The reviewer will check your government-issued ID against the name printed on the letters. If your legal name is “Jonathan Edward Smith” but the letters say “John E. Smith,” you may encounter friction. Consistency in your document packet is critical. The name on the court document must perfectly align with the person presenting it.

The Raised or Stamped Seal

A standard photocopy of the document is rarely accepted for opening or closing accounts. The institution is looking for a “certified copy.” This usually means the document has a physical, raised seal embossed into the paper, or a specific colored stamp from the court clerk. If the document feels perfectly flat and looks like it came from a standard home printer, a major financial institution will likely reject it.

The Issue Date

Reviewers always check the date the document was certified. They want assurance that the court’s decision is recent and that you are still the active executor. An older date is the most common trigger for a paperwork rejection.

Common Friction Points and How to Handle Them

Even with perfect preparation, estate administration involves humans, and humans follow rigid corporate rules. You will likely hit a wall at least once during your phone calls or branch visits.

A frequent pattern I notice is the “stale document” rejection. You might mail a certified copy to an investment firm, wait three weeks for a reply, and then receive a letter stating your documents are too old to process. This happens because many institutions have strict internal policies requiring the certification date to be within the last 60 to 90 days.

When this happens, the best approach is calm, written confirmation. You want to avoid guessing what the institution wants.

Subject: Clarification on document requirements for Estate of [Name]

Hello [Representative Name],

I received the notice that the document packet was not accepted. I want to ensure my next submission is exactly what your legal team requires.

Could you please confirm in writing if you require a newly certified copy of the Letters Testamentary with a date issued within the last 60 days? Also, please confirm if this needs to be mailed physically, or if a secure digital upload is acceptable.

Thank you for your guidance.

Using a script like this removes the emotion from the delay. It forces the institution to give you a clear, written requirement. Once you have their exact rule in writing, you can confidently request a freshly dated copy from the court without worrying that it will be rejected again.

Organizing, Tracking, and Digital Submissions

Because you must purchase certified copies directly from the court clerk, they are essentially an estate expense. Courts typically charge between $5 and $25 per copy depending on the state. You should save the receipt, as this is a valid administrative expense that the estate will reimburse.

Organization is your best defense against administrative fatigue. If you purchase five copies to start, treat them like numbered keys. When you mail one to a life insurance provider, log the date, the company, and the tracking number of the envelope. I frequently see executors lose track of which institution is holding their documents, leading to unnecessary panic and duplicate court fees.

⚠️ Warning: You should always assume that any physical certified copy you mail to a processing center will not be returned to you. Never mail your absolute last physical copy. If you are down to your final document, keep it safely in your own files and order more from the court before proceeding.

Today, many banks and brokerages allow you to bypass the mail entirely by uploading documents to a secure legal portal. If you take this route, file hygiene is critical. Make sure your scanner is set to at least 300 DPI, as blurry court seals or unreadable certification dates are immediately rejected by compliance software.

Do not leave your scan named “document001.pdf”. Rename it immediately to something clear, such as: Smith_Estate_LettersTestamentary_Certified_Nov2023.pdf. This small habit prevents you from attaching the wrong file when navigating multiple vendor portals.

What Happens If The Executor Changes

It is important to understand that your authority is tied to your specific identity. In some complex estates, an executor may need to step down due to health reasons, or a co-executor might pass away before the estate is closed.

If an executor resigns or is removed by the court, their original Letters Testamentary become instantly invalid. The court must formally appoint the successor executor named in the will, or an administrator if no backup was named. The new representative will then receive their own freshly issued letters with their name printed on them. Institutions will freeze estate accounts if they discover the active executor has changed until the new, valid documents are presented.

Final Thoughts on Managing Your Letters

Receiving your Letters Testamentary is usually the exact moment when the abstract idea of being an executor becomes a very real operational job. Your name is officially on the court record, and the responsibility is now active.

While the overall probate process can feel overwhelming, having a clear understanding of what this document proves gives you immense confidence. When an institution pushes back, you now know they are not doubting you personally; they are simply checking their corporate liability boxes. Keep your documents clean, keep your communication in writing, track exactly where you send your copies, and you will navigate the institutional friction much more smoothly. Take it one task, and one document packet, at a time.

❓ FAQ

📝 What exactly are letters testamentary?

They are an official court-issued document that legally proves a judge has validated the deceased person’s will and appointed you to act as the executor of their estate.

🏦 Why is the bank asking for letters testamentary when I have the will?

Banks cannot rely on a will alone because they have no way to prove it is the final, legally valid version. They require the court document to shield themselves from liability before releasing any funds.

🏛️ How do I actually get my letters testamentary?

You cannot simply ask for them. You must file a petition with the probate court, attend a hearing or wait for a review period, and have a judge officially approve your appointment before the clerk will issue the document.

⚖️ What is the difference between letters testamentary and letters of administration?

Letters Testamentary are issued when there is a valid will naming an executor. Letters of Administration are issued when there is no will, or the named executor cannot serve, and the court appoints an administrator instead. Both grant similar administrative authority.

⏳ Do letters testamentary expire after a certain amount of time?

While your legal authority usually does not expire until the estate is closed, financial institutions frequently require the physical document to have a certification date within the last 60 to 90 days. If your copies are older, you may need to order fresh ones.

📂 How many certified copies should I ask the court for?

A common rule of thumb is to estimate the number of major financial institutions, insurers, and real estate properties you need to deal with. Most executors order between 5 to 10 copies initially to cover the main accounts.

💻 Can I just show a picture of the letters on my phone?

In most cases, no. When dealing with significant assets or closing accounts, institutions usually require a physical certified copy with a raised seal, or a high-quality, high-resolution scan uploaded directly into their secure legal portal.

🤝 Can a joint account holder skip the letters testamentary?

Often, yes. If a bank account is held jointly with right of survivorship, the surviving owner can usually take full control by simply presenting a death certificate. Letters are typically needed for accounts owned solely by the deceased.

💵 How much do certified copies of letters testamentary cost?

The cost varies heavily depending on the state and county courthouse, but you can typically expect to pay between $5 and $25 per certified copy. Keep your receipt, as this is a reimbursable estate expense.

❌ What do I do if my name is spelled wrong on the letters?

You must contact the court clerk immediately to have the error corrected. Institutions verify your ID against the document, and even a small typo can cause a bank’s legal department to reject your paperwork.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.