- The goal is safety: Distributing estate assets too early is the most common way executors accidentally take on personal financial risk. You need a structured readiness checklist.

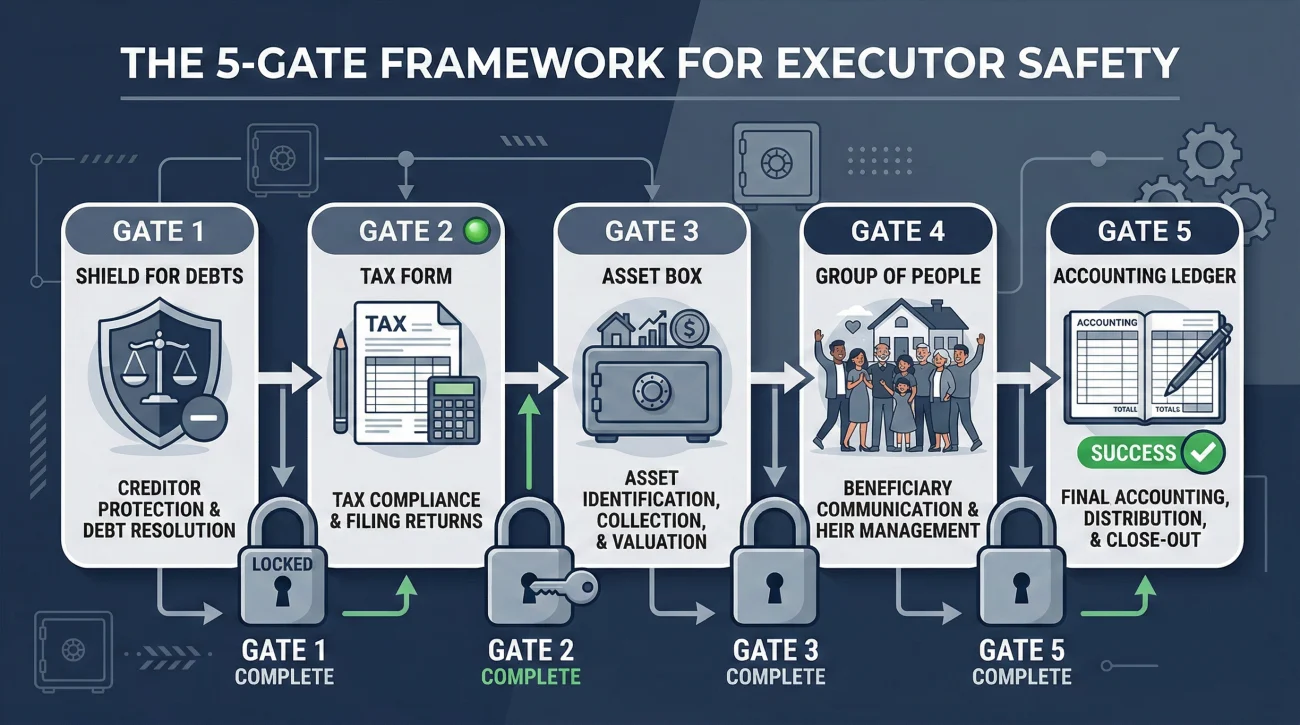

- Verify the core gates: Before money moves, debts must be stable, tax lanes identified, assets fully pooled, beneficiary disputes addressed, and a readable accounting draft must exist.

- Holdbacks are standard: Most experienced executors do not distribute 100% of the funds at once. They keep a documented reserve buffer for unexpected trailing costs.

The Pressure to Pay vs. The Need for Safety

If you are managing an estate, you are likely feeling a very specific type of pressure right now. The house might be sold, the bank accounts are pooled, and your inbox is filling up with polite, but persistent, emails from family members asking exactly when can executor distribute the funds. It is completely natural for beneficiaries to want closure, and honestly, as an executor, you just want this project off your desk.

In my day-to-day work organizing estate files, this exact moment at the finish line is where I see the most stress. Why? Because writing the checks feels like the end, but if you distribute estate funds before final accounting and debts are truly settled, you risk having to ask beneficiaries to give the money back.

Key Point: A distribution readiness checklist is not a delay tactic. It is your personal shield. It provides a logical, documented sequence to ensure you are legally and financially safe to proceed.

Gate 0: The Pre-Distribution Mindset Check

Before we look at the paperwork, I always ask executors to check their own mindset. Often, the executor is also a beneficiary. This creates a natural conflict of interest.

When you are tired and want your own inheritance share to buy a car or pay off a personal loan, it is incredibly tempting to rush the process. You might think, “I am sure there are no more bills, I will just send the money now.” To clear Gate 0, you must separate your role as a project manager from your role as an heir. The estate’s safety must come before your personal timeline.

Why We Treat Readiness as a Series of Gates

Once your mindset is focused strictly on the estate’s safety, you need a framework to enforce it. I advise treating distribution as a series of operational “gates.” You cannot pass through the next gate until the current one is securely closed. This framework removes the emotion from the timeline.

When a beneficiary asks for an early payout, you do not have to say a flat “no.” Instead, you can point to the process. You can honestly say, “We are currently clearing Gate 2 for tax clearance, and we cannot move forward until the CPA gives us the green light in writing.” This transforms you into a diligent project manager following the rules.

The Typical Distribution Timeline

To give you a realistic picture, here is how a standard sequence usually flows in my files. Keep in mind your local jurisdiction will dictate exact legal dates, so always consult your estate attorney for specific deadlines.

| Milestone | Typical Operational Timeline |

|---|---|

| Estate Opened | Month 1: Authority granted, accounts pooled. |

| Creditor Window Closes | Month 5: The local 4 to 6 month statutory window ends. |

| Tax Clearance | Month 7: CPA files final tax returns and confirms clearance. |

| Distribution | Month 8: Final accounting is approved and payouts begin. |

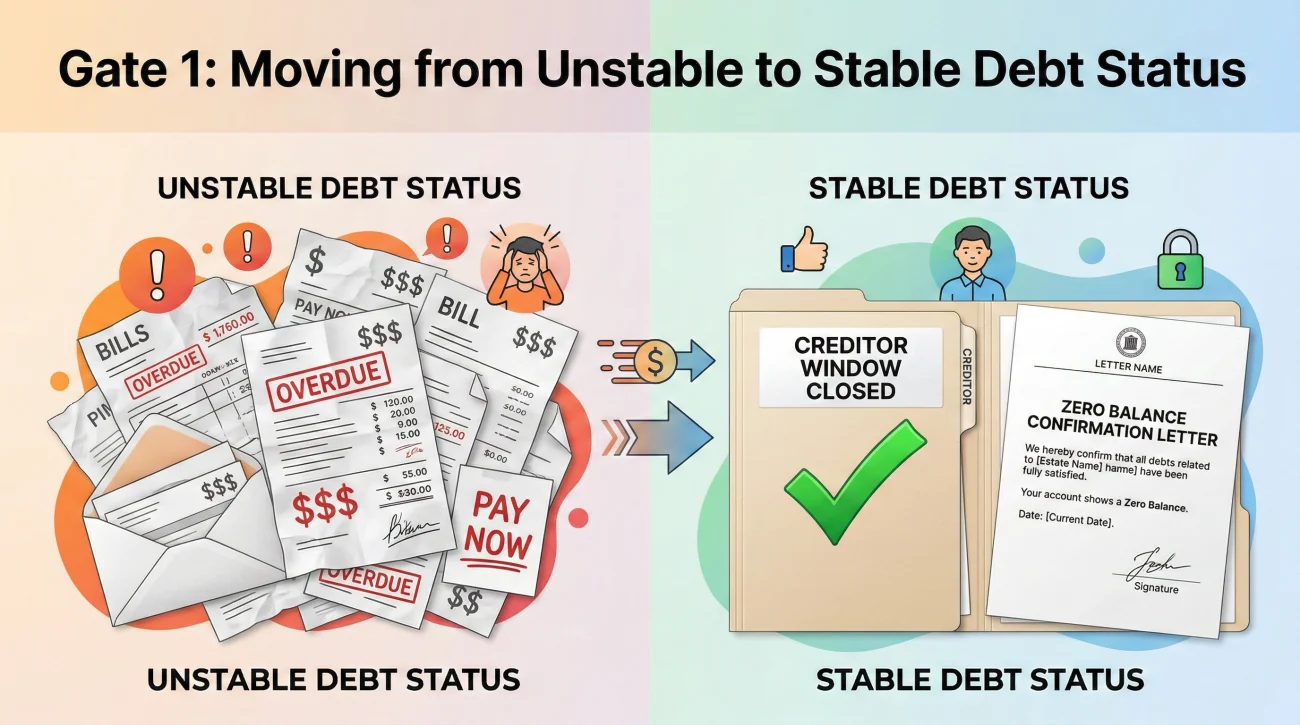

Gate 1: The Debts and Claims Snapshot is Stable

The first and most critical gate in any estate distribution checklist before paying taxes or heirs is ensuring your debt landscape is completely stable. You cannot distribute what you do not truly own, and until all valid creditors are satisfied, the estate’s money technically belongs to them first.

What does “stable” mean operationally? In most jurisdictions, there is a strict 4 to 6 month statutory creditor claim window. I strongly advise consulting your estate attorney to confirm exactly when this window officially closes in your local area. Stability means this specific window has officially passed, you have documented every known debt, you have formally responded to claims, and you have verified with legal counsel that no surprise lawsuits are pending.

A common pattern I see is an executor who successfully pays off the major credit cards, but forgets about trailing administrative costs. For example, did the estate pay for the final utility bill on the house that was sold last month? Is there an outstanding invoice from the probate attorney?

“I haven’t received any new bills in the mail for a few weeks, so I think we are good to go.”

“The creditor claim period ended on October 1st. I have written confirmation of a zero balance from all known accounts, and the attorney submitted their final invoice.”

If you need to verify a balance with a vendor before marking this gate clear, use a simple, polite script like this:

Subject: Request for final statement, Estate of [Name]

Hello Customer Service,

I am the executor for the Estate of [Name]. I am preparing to close the estate’s administrative files.

Can you please provide a final, updated statement showing a $0.00 balance for account ending in [1234], and confirm in writing that this account is officially closed?

Thank you for your help in finalizing these records,

[Your Name]

Executor

Gate 2: Tax Lanes are Identified and Buffered

Taxes are the ultimate wildcard. I am not a CPA, and I do not give tax advice, but from an operational standpoint, assuming “there are no taxes because the estate is small” is incredibly dangerous. The government will always look to the executor to make them whole.

You need a professional to confirm in writing that these three common tax lanes are either clear or adequately buffered with reserve funds:

- 📄 The Deceased’s Final Personal Return: Did they owe taxes for the year they passed away?

- 🏦 Estate Income Tax: Did the estate itself generate income, like rent or dividends, while you were managing it?

- 🏛️ Estate/Inheritance Taxes: Does the estate trigger any federal or local threshold taxes?

⚠️ Warning: Never clear Gate 2 based on a verbal phone conversation with an accountant. Always get a clear “ready to distribute” instruction in writing.

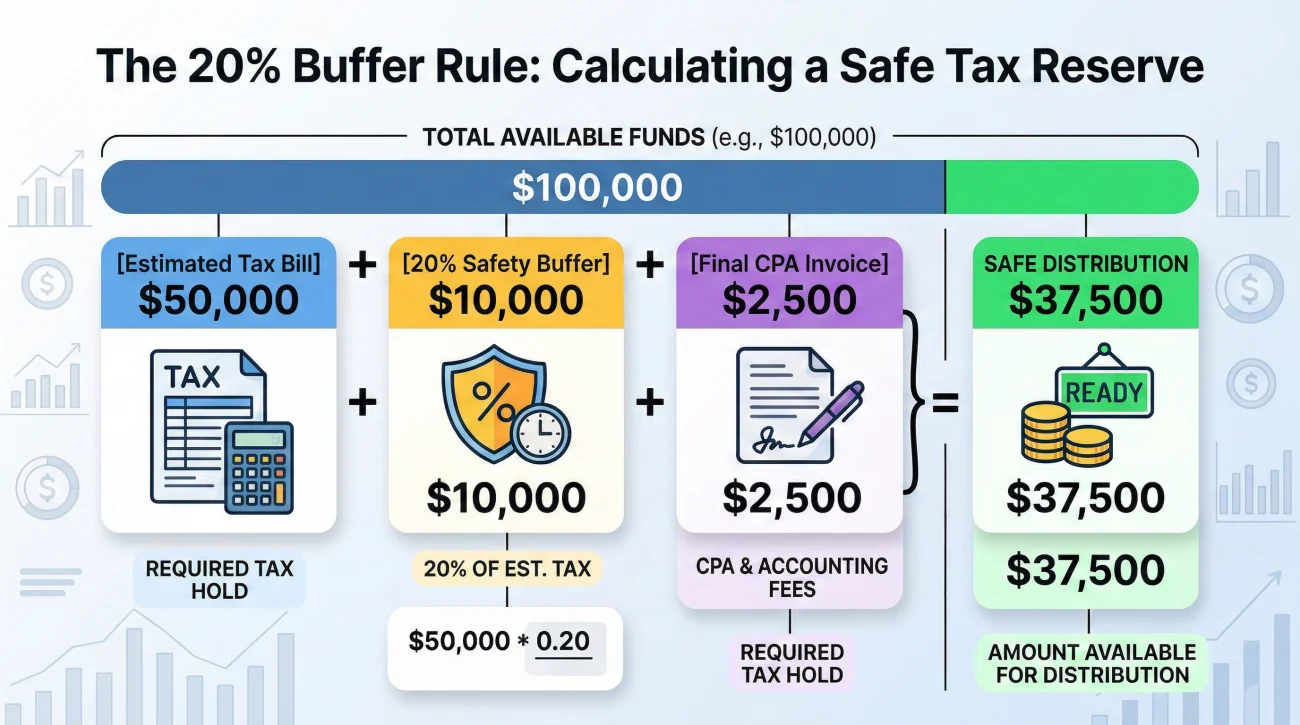

How to Calculate a Tax Reserve

Often, a CPA will tell you that they cannot finish the final return until early next year. If that happens, you do not have to freeze the entire estate. You establish a “tax reserve.”

Let’s look at a practical example. If the estate has $100,000 remaining and the CPA estimates a $4,000 final tax bill, do not just hold $4,000. In my files, we always use a 20 percent buffer for safety. We hold $4,800 for taxes, plus another $1,500 for the CPA’s final invoice. The remaining $93,700 is what safely moves to the distribution pool.

Gate 3: The Assets List is Complete Enough for Fairness

Gate 3 is about ensuring your asset pool is fully gathered. Over the years, I have seen too many executors rush to distribute the main checking account, only to receive a surprise refund check from a nursing home three months later.

If you have already done the complex math to divide the estate among five siblings, finding a random $400 check means you have to recalculate everything or figure out how to split a tiny amount of money fairly. Ask your attorney if it is safe to consider the asset pool finalized.

When the dust has settled and the estate bank account balance has sat unchanged for a few weeks, aside from normal monthly bank fees, you have likely achieved the stability needed to clear Gate 3.

To formally clear this gate, I typically have executors review their initial inventory and run through this basic checklist:

| Asset Category | Checklist for Gate 3 Readiness |

|---|---|

| Real Estate | Is the property sold and escrow funds fully deposited? Or, if transferring in-kind, is the deed fully prepped? |

| Bank Accounts | Are all known accounts fully consolidated into the single estate checking account? |

| Refunds & Deposits | Have you received the prorated refunds for canceled insurance, utilities, and facility deposits? |

| Personal Property | Have all physical items been accounted for, appraised, or assigned a documented disposition plan? |

Pooling the money and confirming the assets is only half the battle. Now you face the human element of making sure the right people receive it, which brings us directly to Gate 4.

Gate 4: Missing People and Disputes are Addressed or Buffered

You cannot distribute an estate if you do not know who is supposed to get the money, or if the people receiving the money are actively fighting.

I frequently handle files where one beneficiary has moved, changed their phone number, and stopped answering emails. As an executor, you cannot simply ignore the missing person or divide their share among the others just to close the estate.

If you face a missing heir, Gate 4 requires you to document your search efforts heavily. Before setting up a blocked reserve account with your attorney’s help, you should send a formal letter to their last known address via certified mail. Here is a generic template:

To: [Beneficiary Name]

Last Known Address: [Address]Subject: Final Notice Regarding the Estate of [Name]

Dear [Beneficiary Name],

I am writing to you in my capacity as Executor for the Estate of [Name]. We are nearing the final distribution phase of the estate.

I have attempted to reach you via email and phone on [Dates] without success. Please contact me at [Your Phone/Email] by [Date, usually 30 days out] so we can process your distribution share.

If I do not hear from you by this date, I will proceed with holding your share in a reserve account under the guidance of the estate’s legal counsel.

Sincerely,

[Your Name]

Executor

For active disputes, such as two siblings fighting over a house valuation, you must rely on legal help to create a structural buffer. Do not attempt to force a settlement yourself.

Gate 5: The Accounting Draft Exists and is Readable

I often hear executors groan when I mention “accounting,” but please do not think of this as a corporate audit. The final accounting is simply the financial story of the estate, translated into a readable format.

It shows what the estate started with, every penny that came in, every penny that went out, and exactly what is left to distribute. At this stage, you must have the draft complete. If a beneficiary looks at your spreadsheet and cannot understand why the bank balance dropped by $5,000 in March, your draft is not ready.

💡 Pro Tip: I always advise executors to have an organized PDF packet ready. If you list a $5,000 roofer expense, you should have a file named 2024-03-15_Invoice_SmithRoofing_Paid.pdf ready to back it up.

In my experience reviewing hundreds of estate files, a clean, readable accounting draft is the single best tool to stop beneficiary arguments before they even start. Once you are confident the math ties out perfectly to your bank statements, you have cleared Gate 5.

What If You Missed a Gate and Distributed Early?

But what happens if you did not wait for Gate 5 to fully clear before writing checks? In the real world, mistakes happen. What do you do if you sent out the inheritance checks, and two weeks later, a valid $2,000 medical bill arrives in the mail?

First, do not hide it. Transparency is your best tool. You will need to contact the beneficiaries immediately, explain the oversight, and request a prorated return of funds. Provide a copy of the bill so they see exactly where the money is going. If they refuse or have already spent the money, you will likely need to cover the bill out of pocket and consult your attorney regarding your recovery options.

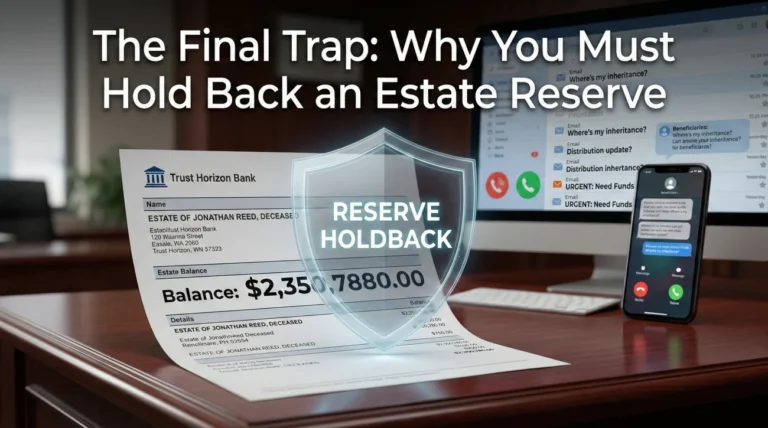

The Final Decision: Why You Should Not Empty the Account

Even after clearing all five operational gates, there is one final habit you should adopt: the holdback.

To avoid the stressful remediation scenario mentioned above, most estates utilize an estate reserve holdback. This is a buffer amount left in the checking account to cover late bank fees, final postage, or unexpected trailing taxes.

Document this decision clearly in your accounting draft so beneficiaries see the math. Transparency here prevents accusations of hidden money.

The Final Step: Moving from Readiness to Action

Reaching the distribution phase is a massive accomplishment. By enforcing these five gates, you ensure the beneficiaries receive an organized handover.

Remember, your job as an executor is to be accurate, not fast. Take the time to build your documentation, confirm your balances in writing, and always lean on your local professionals when a gate seems stuck.

Once you are completely confident in your readiness, the next phase is executing the actual paperwork. These five gates form the core of a safe estate distribution checklist, ensuring you can close the accounts and finalize the handover without carrying any lingering personal risk.

❓ FAQ

🕒 When can I distribute estate assets?

You can typically distribute assets only after all known debts are resolved, the statutory 4 to 6 month creditor claim period has expired, tax obligations are cleared, and a final accounting draft is prepared. Timing depends on these operational gates, not an arbitrary calendar date.

📄 Can an executor distribute property before final accounting?

It is highly risky. Final accounting is the proof that the estate can afford the distribution. Distributing property before the math is finalized can lead to major accounting errors if an unexpected debt surfaces later.

🏦 Do I have to pay taxes before distributing an estate?

In most cases, yes. Tax agencies generally have top priority. Always get written clearance or specific reserve instructions from a CPA before moving money to beneficiaries.

📉 What happens if I distribute money and a bill comes later?

If the estate account is empty, the executor must usually try to recall the funds from the beneficiaries. If the beneficiaries refuse, the executor is often held responsible for paying the valid bill, which is why a reserve holdback is crucial.

✅ Is there a checklist for distributing estate funds?

Yes, a safe checklist includes five main gates: 1) Verify all debts are paid or denied. 2) Clear or buffer all tax liabilities. 3) Gather all trailing assets. 4) Resolve any beneficiary disputes. 5) Complete a transparent final accounting draft.

🛡️ How long does an executor have to hold money before distribution?

There is no universal single timeframe. The holding period is dictated by local laws, such as a mandatory creditor claim window, and the time it takes to finalize tax returns. Executors hold the money until all legal risks are definitively resolved.

⚖️ Can I do a partial distribution early?

Partial distributions are commonly done if the estate is very large, debts are clearly minimal, and a massive safety reserve is kept. However, it requires careful documentation to ensure fairness if the remaining balance drops unexpectedly.

💬 What if a beneficiary demands their share right now?

A beneficiary’s demand does not override the executor’s legal duty to pay creditors and taxes first. Respond politely but firmly, explaining the exact readiness gate the estate is currently in and provide a date for your next status update.

🔍 How do I know if the estate is ready to close?

The estate is ready when the bank balance is completely stable, no new mail or bills are arriving, the CPA has signed off, the final accounting is drafted, and you are simply waiting for beneficiaries to sign their receipts and releases.

🛑 Do I need court approval to distribute funds?

It depends entirely on your local jurisdiction and whether you are navigating formal or informal probate. In many areas, if all beneficiaries sign a waiver and approve your final accounting, formal court hearings can be bypassed.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.