- Your primary job is gathering documents and organizing records, not calculating tax liabilities or memorizing the tax code.

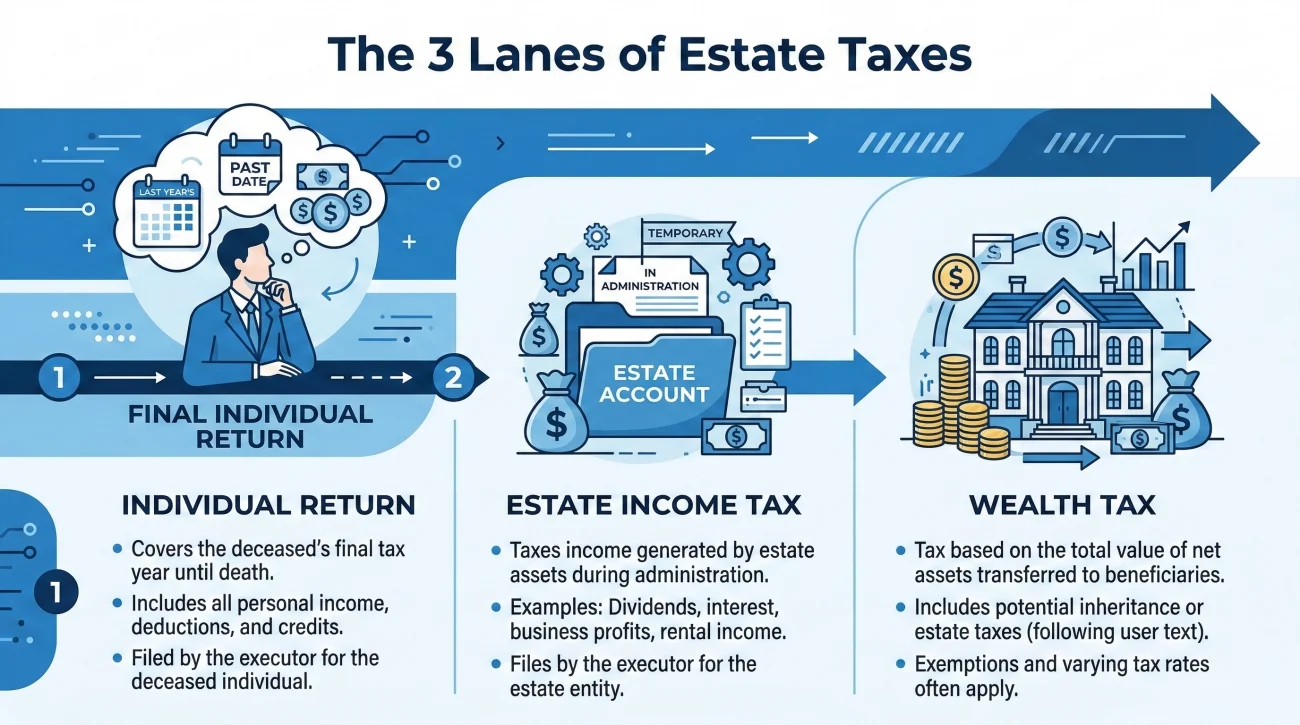

- Estate taxes generally fall into three distinct conceptual lanes: the person’s final individual return, the estate’s own income return, and the rarely applied wealth tax.

- Building a clean, well-documented paper trail is the safest way to hand off the workload to a tax professional and protect yourself from personal liability.

Making Sense of the Tax Paperwork (Without the Panic)

Whenever I sit down with someone who has just stepped into the executor role, there is usually one specific moment when their posture completely changes. It is the moment the conversation turns to taxes. Managing a deceased loved one’s property is stressful enough, but the phrase “executor tax responsibilities” often triggers a deep, immediate sense of dread. People picture themselves sitting at a kitchen table surrounded by receipts, trying to interpret complex federal codes they have never seen before.

I want to take a step back and let you take a deep breath. In my experience helping families organize estate administration workflows, the panic comes from a misunderstanding of what the job actually requires. You do not need to become a certified accountant overnight. You do not need to calculate depreciation or understand the nuances of capital gains law. Your role, quite simply, is to be the ultimate gatherer and organizer of information.

When you view your responsibilities through the lens of organization rather than calculation, the entire process becomes manageable. You are building a bridge of paperwork. On one side is the messy reality of a person’s financial life, and on the other side is the tax professional who will actually file the forms. Your job is to make sure nothing falls off that bridge.

In this guide, I am going to walk you through a plain-English map of the tax landscape you might encounter. We will look at the three common “lanes” of estate taxes, discuss a practical timeline for when things happen, and cover the communication habits that keep beneficiaries calm while you wait for clearance.

A Concept Map, Not a Filing Guide

Before we look at the different categories of tax, we need to establish a firm boundary around what you should and should not attempt to do on your own. It is incredibly common for an executor to try and save the estate money by downloading forms and trying to fill them out themselves. This is usually where the biggest, most expensive mistakes happen.

⚠️ Warning: I am an estate administration support writer, not a CPA or a tax attorney. This guide is designed to help you organize your files, understand the concepts, and prepare for a professional handoff. It is not tax advice, and it does not contain state-specific filing deadlines or tax thresholds.

When you hire a professional to handle the technical filing, you are essentially transferring the risk of making a mistake off your own shoulders. When you understand the concepts below, you know what mail to keep. When you know what mail to keep, you hand your accountant a complete file. A complete file means fewer billable hours from the accountant and a faster resolution for the estate.

Lane 1: The Final Individual Return (Looking Backward)

The first lane is usually the easiest to understand because it is the one we all participate in every year. When a person passes away, their personal tax clock stops on that exact date. However, the government still requires a final accounting of the income they earned from January 1st up until the day they died.

This is commonly referred to as the decedent final tax return. It looks backward at the life they lived during their final calendar year.

What This Lane Typically Covers:

- ✅ Wages or salary earned before their passing.

- ✅ Retirement distributions, pensions, or Social Security received while they were alive.

- ✅ Interest or dividends paid out into their personal accounts prior to the date of death.

In my day-to-day tracking, this is the lane where the “shoebox method” usually fails. Family members often go to the deceased person’s house, grab a stack of mail from the desk, and hand it to the accountant. But tax documents do not usually arrive until early the following year. If you stop checking the mail in November, you will miss the vital paperwork that arrives in February.

Guessing what the person earned by looking at a few random bank statements and hoping it is correct.

Setting up mail forwarding for a full year and dedicating one specific physical folder purely for incoming tax documents clearly marked with the current tax year.

Lane 2: The Estate’s Own Income (Looking Forward)

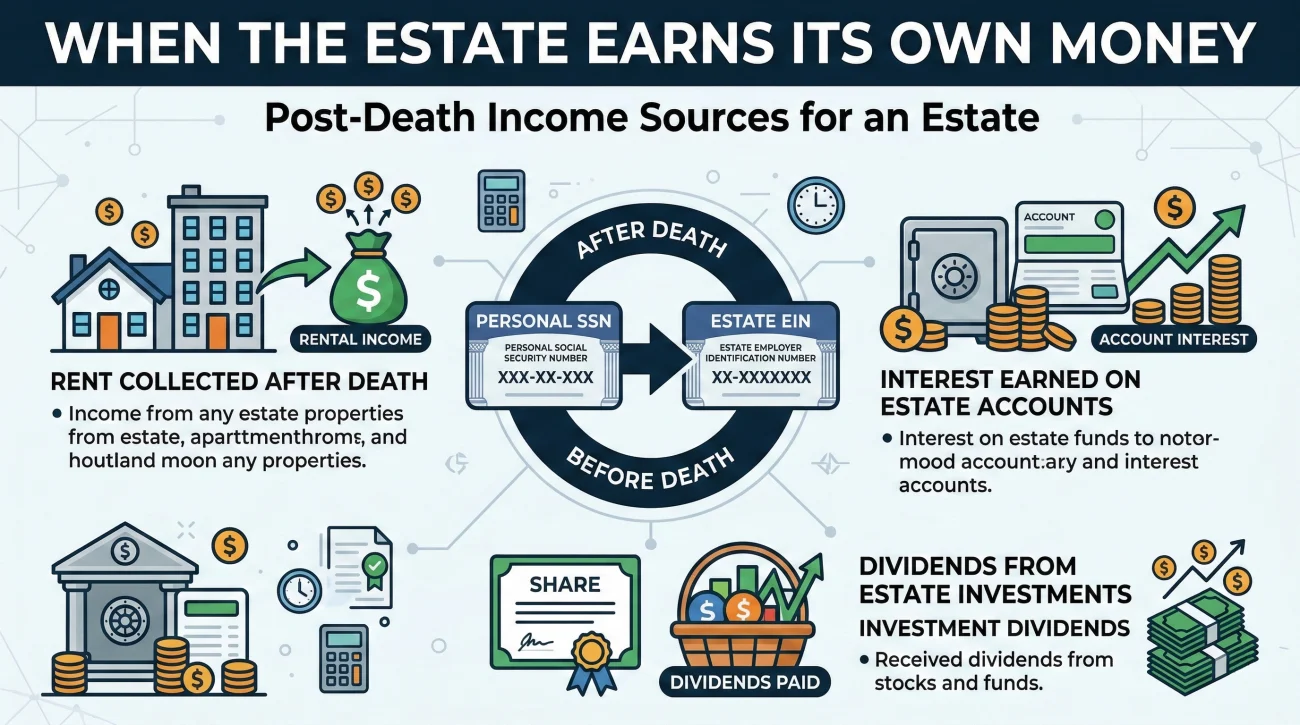

This is where many new executors get confused, assuming that once the final personal return is filed, the tax journey is over. Instead, think of the estate as a temporary business that has been set up to close down a life. If that temporary business makes a profit, it has to report it.

An estate often continues to exist for months or even years while properties are sold and debts are settled. During this transition phase, the assets inside the estate might generate their own money. If the estate holds onto a rental property, rent is still coming in. If the estate has a large bank account, that account is generating interest. Because the original person is gone, this new money belongs to the estate itself as a separate entity.

When an estate generates its own money, it may need to file an estate income tax return (often part of a form 1041 overview conversation you might have with your CPA).

What Triggers This Lane:

- ✅ Rent collected from tenants after the date of death.

- ✅ Interest earned on the estate’s official bank account.

- ✅ Dividends produced by investments held by the estate before they are sold or transferred.

Field note: I commonly see a breakdown here when an executor fails to separate the money. If you leave money in the deceased person’s old, frozen account and try to calculate the post-death interest, the paperwork becomes a nightmare. This is why opening a proper estate account and getting an official tax ID number is so crucial. It creates a clean, clear dividing line for your accountant.

Lane 3: The “Wealth” Tax (Often Feared, Rarely Applied)

If you search the internet for an estate tax return overview, you will likely find terrifying articles about the government taking half of an inheritance. This is the third lane. It is the one that causes the most lost sleep, even though it applies to the fewest people.

An estate tax is fundamentally different from an income tax. Income tax is a tax on money that comes in. The estate tax is a tax on the total, overall value of everything the person owned when they died (houses, cars, accounts, businesses) simply because they are transferring it to someone else.

So why is it so rarely applied? Because federal exemptions are incredibly high. For most everyday families, the federal threshold sits in the multi-millions, meaning standard household estates never come close to triggering it. It is essentially a tax on accumulated, generational wealth.

However, you cannot ignore this lane entirely. The trap here is that while the federal limit is high, many individual states have their own estate taxes, and those state thresholds can be drastically lower. If the estate includes multiple real estate properties, a small business, or large retirement accounts, you must have a local professional review the total value. Once a CPA confirms your total falls below the local threshold, you can stop worrying about this lane.

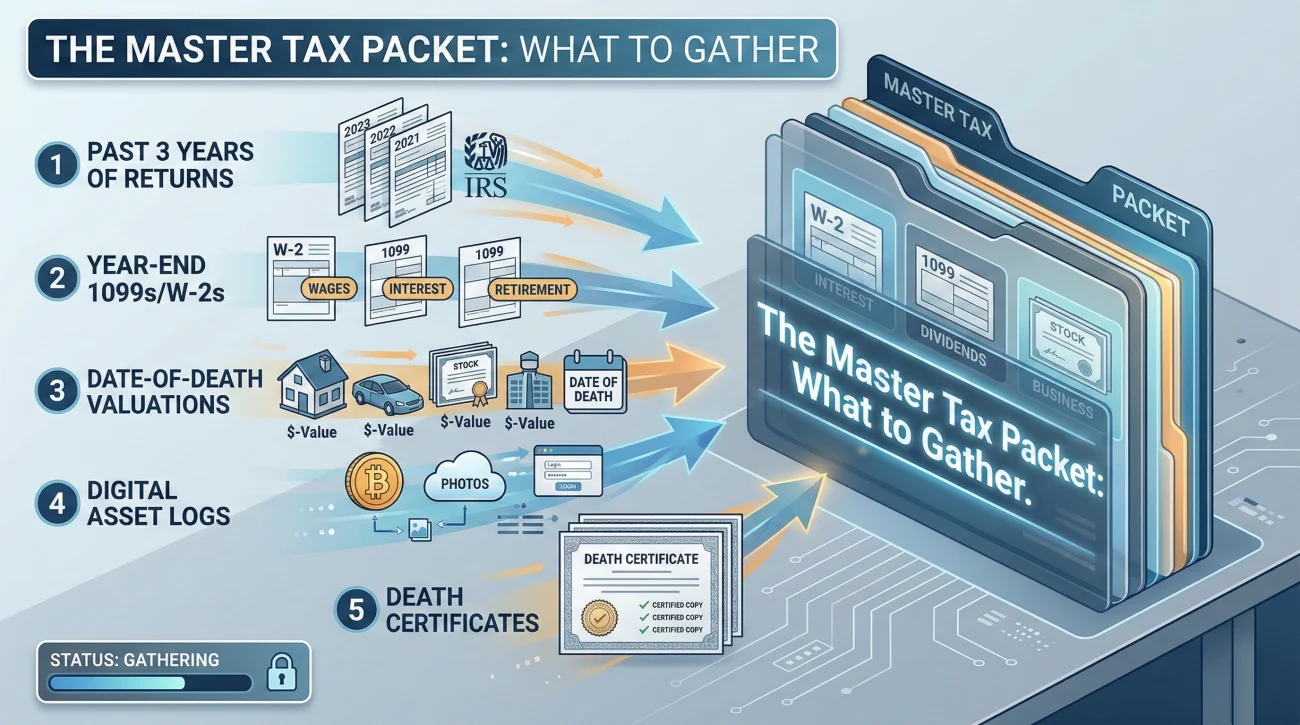

The Master Document Gathering File

Now that we have separated the anxiety into three manageable concepts, we need to talk about execution. Building a reliable taxes executor checklist is about creating a central hub for data. You cannot hand your CPA a garbage bag full of unsorted mail and expect a quick, cheap turnaround.

I always recommend creating a “Master Tax Packet.” This should be both a physical binder for paper mail and a secure digital folder for electronic statements. As you go through the house, check the mail, and contact institutions, you drop the relevant items into this packet.

| Document Type | Where It Usually Hides | Why Your CPA Needs It |

|---|---|---|

| Previous 2 to 3 years of filed tax returns | Home office filing cabinets, digital hard drives, or their previous accountant. | Establishes baselines, uncovers hidden assets, and shows historical carryovers. |

| Year-end income statements (W-2s, 1099s) | Mail arriving January through March of the year following the death. | Required for Lane 1 (the final individual return). |

| Date-of-death asset valuations | Bank statements spanning the exact date of passing, formal appraisals for property. | Determines the starting line for the estate’s value. This is critical for the “step-up in basis”, a rule that resets the value of assets like houses to what they were worth on the day of passing, potentially saving beneficiaries massive capital gains taxes later. |

| Digital asset logs and online accounts | Email histories, crypto wallets, or 1099-K forms from platforms like PayPal or eBay. | Increasingly targeted by tax authorities. Missing these can cause surprise audits for the estate down the road. |

| Death certificates and appointment letters | The executor’s main legal binder. | Proof the CPA needs to legally file on behalf of the deceased. |

Often, you will know a document exists but you will not be able to find it in the house. When this happens, you have to request it in writing from the financial institution or the former employer. Keep your requests simple, polite, and heavily documented.

Here is a neutral, professional script you can use to request duplicate tax documents without overcomplicating the situation:

Subject: Request for duplicate tax documents – Estate of [Name]

Hello,

I am the appointed executor for the estate of [Name], who passed away on [Date]. For our required tax filings, our accountant has requested duplicate copies of all end-of-year tax statements (such as 1099s or W-2s) issued to [Name] for the [Year] tax year.

I have attached my letter of authority and a copy of the death certificate for your records. Please provide a written list of any additional forms you require to process this request, and let me know the expected timeline for receiving the duplicate statements.

Thank you for your assistance in keeping our records complete.

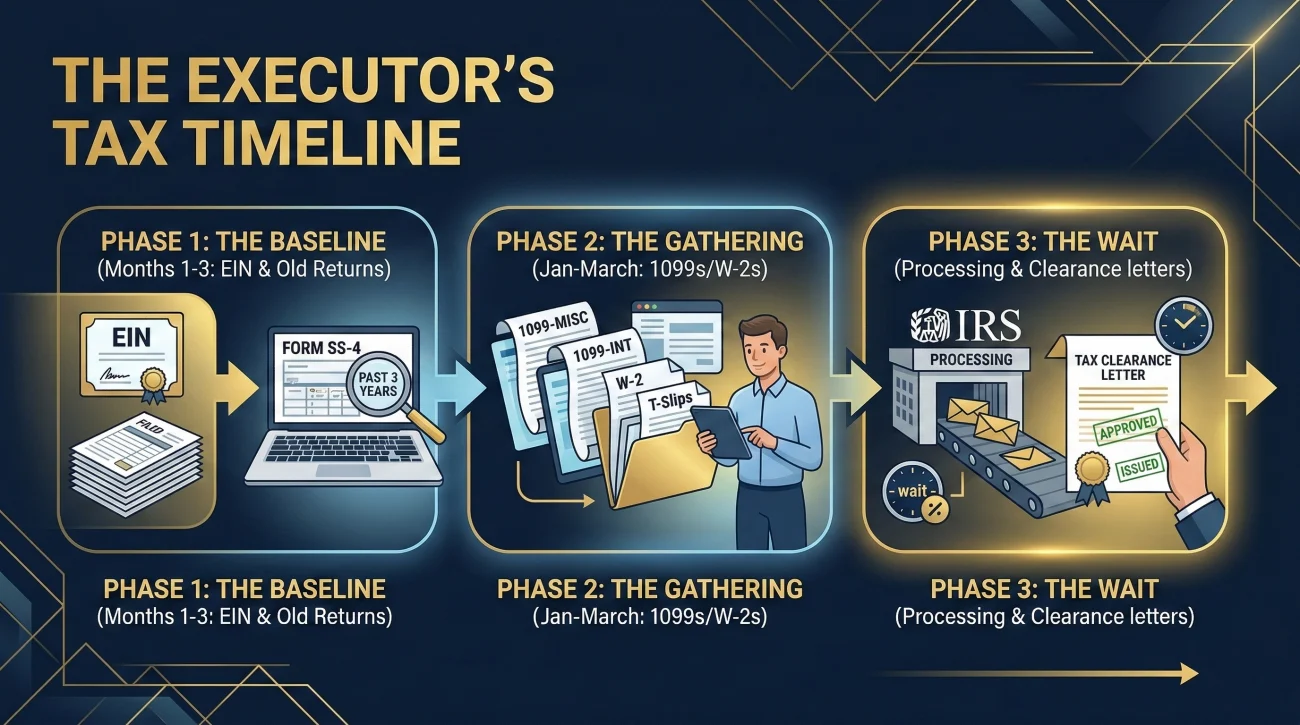

The General Tax Timeline (What to Expect)

One of the hardest parts of the executor role is feeling like you are always behind schedule. Because tax documents rely on external companies mailing things out, you will often experience periods of intense work followed by months of waiting.

While exact filing deadlines depend on the date of death and your specific state, an executor’s workflow usually follows a predictable rhythm.

- ✅ Months 1 to 3: The Baseline. You request old tax returns, locate the deceased person’s previous CPA, set up mail forwarding, and obtain the estate’s official tax ID (EIN).

- ✅ Early the Following Year: The Gathering. Between January and March, you collect all the W-2s and 1099s that arrive in the mail and hand your completed Master Tax Packet to your accountant to file Lane 1.

- ✅ The Closing Phase: The Wait. After everything is filed, you wait for the IRS and state authorities to process the returns and issue formal closing letters or tax clearance certificates.

The Distribution Trap: Holding the Reserve

That final waiting phase is usually the most stressful part of the entire process. While you are waiting for those official clearances to arrive in the mail, you will face intense pressure from beneficiaries who want their money. Family members often do not understand why the estate is taking so long, and they view the executor as an unnecessary bottleneck.

This pressure leads to the most dangerous mistake in estate administration: distributing funds before tax liabilities are fully cleared. If you give all the money to the beneficiaries and six months later the IRS or the state tax authority sends a bill, you may find yourself personally responsible for recovering that money. If the beneficiaries have already spent it, you are in a terrible position.

Key Point: Taxes are usually considered a high-priority obligation. They almost always sit near the very top of the list when you look at a safe executor creditor and debt checklist. You cannot safely distribute the bottom of the barrel until the top obligations are absolutely satisfied.

This is why the concept of an “estate reserve” is so vital. In many cases, executors will work with their professionals to hold back a significant buffer of money in the estate account specifically to cover potential, unfiled taxes. Only after the tax professional confirms that all returns have been accepted and all clearances have been issued is the final reserve distributed.

If you realize early on that the estate simply does not have enough money to pay the taxes and the regular creditors, you are dealing with what is called an insolvent estate. Stop paying everything immediately and seek local legal guidance, as taxes often have strict priority rules over credit cards and medical bills.

Communicating a delay to the family requires a steady hand. Do not get defensive, and do not make promises about timelines that are out of your control.

Hi everyone,

I want to provide a quick update on the estate timeline. We have successfully gathered the necessary financial documents and have handed the file over to the accountant.

Right now, we are in a holding pattern while the final tax returns are prepared and processed. Because the estate is responsible for any pending tax obligations, we cannot safely release the remaining funds until the accountant gives us formal clearance that no further taxes are owed. I will provide another status update once we hear back from the tax office. Thank you for your continued patience.

Red Flags That Mean It is Time to Stop and Ask for Help

There is a persistent myth that hiring a CPA is an unnecessary luxury for an estate. In reality, there are certain scenarios where trying to navigate the system without a guide is virtually guaranteed to create a disaster.

If you encounter any of the following situations during your document-gathering phase, you should immediately pause your efforts and secure a local tax professional:

- 🛑 Missing History: You discover that the deceased person had not filed their personal tax returns for several years prior to their death.

- 🛑 Business Ownership: The person owned a small business, held partnership shares, or had complex commercial real estate investments.

- 🛑 Messy Records: There are multiple bank accounts with large, unexplained cash transfers, or you cannot reliably reconstruct their financial footprint.

- 🛑 Beneficiary Disputes: The family dynamics are hostile, meaning every penny spent or held back for taxes will be scrutinized and challenged.

When you hire a professional, you are not just paying for them to fill out boxes on a form. You are paying for their liability coverage and their ability to interface directly with tax authorities. Knowing when to hand over the reins is the ultimate form of protecting yourself and the estate.

Final Thoughts: Building the Bridge to the Finish Line

Stepping into the executor role can feel like being asked to fly a plane having never taken a lesson. The dials and gauges of tax terminology, such as final individual returns, estate income, and basis step-ups, are confusing and intimidating. But remember, you do not have to fly the plane. You just have to make sure the pilot has the right map.

Focus entirely on your administrative hygiene. Open the mail, log the statements, request duplicate records in writing, and keep a clean, separated estate bank account. If you build a pristine master tax packet, you will protect the estate’s assets, you will protect your own personal liability, and you will eventually bring the process to a quiet, predictable close.

❓ FAQ

🗓️ Do I have to file taxes for a deceased person?

In many cases, yes. If the person earned income between January 1st and the date they passed away, a final individual return is usually required to close out their tax history.

✉️ What if I cannot find their old tax returns?

Do not guess. You or your accountant can request historical tax transcripts directly from the tax authorities to reconstruct their filing history and see what was previously reported.

🏦 Does the estate need its own tax ID number?

Typically, yes. Once the person passes, their Social Security Number can no longer be used for new estate business. An Employer Identification Number (EIN) is usually obtained to open the estate bank account and track the estate’s own income.

🛑 Can I distribute money before taxes are filed?

Doing so creates severe personal risk. If a tax bill arrives after you have distributed all the funds, you may be held personally responsible for paying that debt out of your own pocket.

⚖️ What happens if the estate runs out of money before taxes are paid?

This is known as an insolvent estate. Federal and state taxes typically hold a very high priority over standard credit card debts or medical bills. If money is running out, you must pause all payments and get professional guidance on the strict legal order of who gets paid first.

🧾 Who pays the accountant to do the estate taxes?

Professional tax preparation is generally considered a standard, legitimate administration expense. These fees are typically paid directly out of the estate’s funds, not from the executor’s personal pocket.

🏠 Does selling the house trigger estate taxes?

Selling a house often involves capital gains considerations or estate income tax, but it does not necessarily trigger the federal wealth tax. A CPA will look at the date-of-death value versus the sale price to determine what needs to be reported.

🤷♂️ What if the person had not filed taxes in years?

This is a major red flag that requires immediate professional help. A CPA can help reconstruct the missing years, negotiate with tax authorities if necessary, and prevent the estate from being frozen due to penalties.

💸 Are inheritances considered taxable income for beneficiaries?

A straight cash inheritance usually is not, but retirement accounts like Traditional IRAs are a massive exception. Because the deceased had not paid income tax on that money yet, the beneficiary usually has to pay it. A professional must advise on the ’10-year rule’ to avoid a massive tax bomb.

📝 How long should I keep the tax records after closing?

Most CPAs recommend keeping the full tax packet, bank statements, and the IRS closing letter for at least three to seven years after the estate is formally closed, depending on the complexity of the returns.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.