- The financial obligations left behind belong entirely to the estate. Your risk as an administrator does not come from the debt itself, but from making procedural errors while handling it.

- Never guess who gets paid first. Paying a lower-priority bill while ignoring a major claim, or distributing money to beneficiaries too early, are the primary ways executors create personal liability.

- Implement a strict “pause and verify” workflow. Demand written proof for every claim and respect the local statutory waiting periods before issuing any payments.

- Stop the digital bleed by identifying and pausing auto-renewing subscriptions, and seek immediate local counsel if the estate’s total debts outweigh its assets.

The Operational Reality of Estate Obligations

In day-to-day administrative support work, the most urgent calls I receive from new executors are driven by mail anxiety. They open a stack of envelopes, see a mountain of credit card balances and utility notices, and immediately fear that these companies are going to target their personal savings. When auditing estate files, I consistently see that final medical expenses and lingering credit card balances form the bulk of complex claims in an average estate. The sheer volume of these invoices often panics people into making rushed decisions.

Let us establish the most important boundary right now. The debt belongs to the estate. Think of the estate as a contained bucket. Everything the person owned goes into that bucket, and every bill they owed must be paid out of it. Your job is to carry the bucket, organize the paperwork inside, and distribute the contents according to a highly specific, legally mandated order.

You are not expected to fill the bucket with your own money. However, carrying it is a serious responsibility. When executors find themselves facing personal legal trouble, it is almost never because the deceased person owed money. Liability arises because the executor made a structural mistake in how they managed, communicated, or paid those claims. Your protection comes from establishing a disciplined, highly auditable workflow from day one.

To see exactly where this fits into your broader administrative duties, I highly recommend mapping out your overall executor creditor and debt checklist so you have a complete picture of the landscape before you begin.

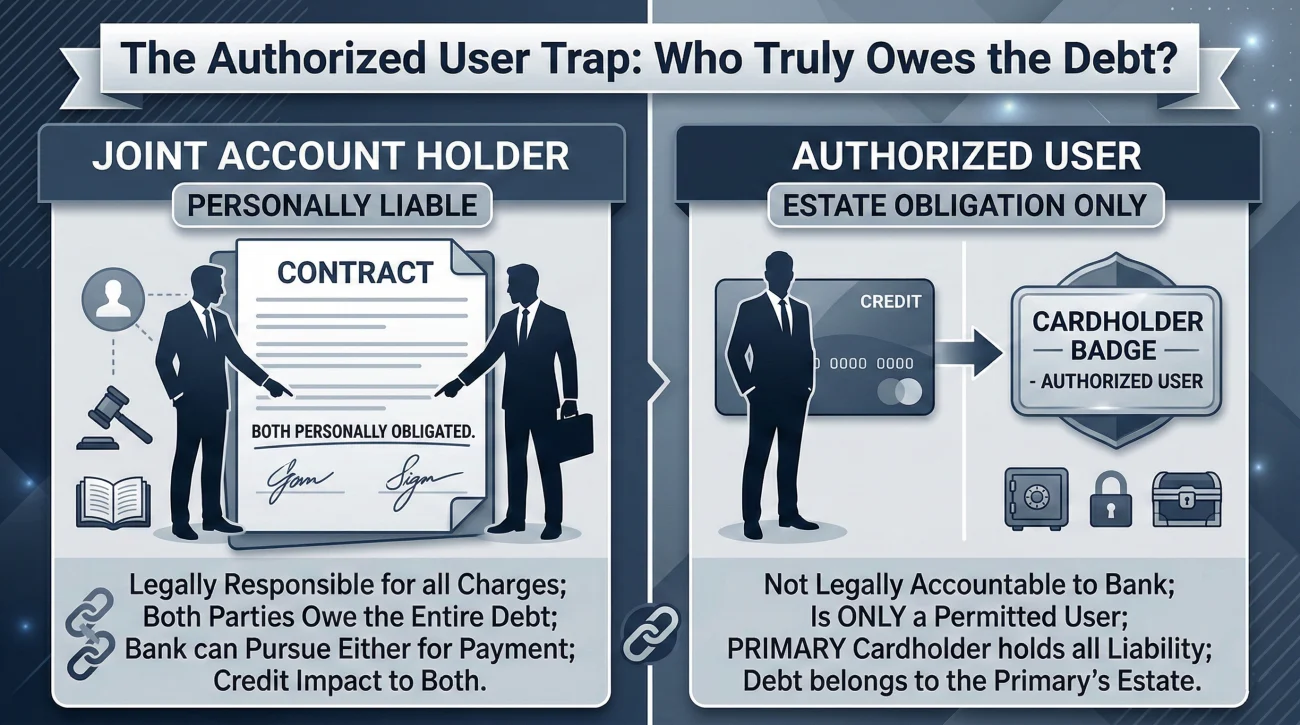

The “Authorized User” Trap: Clarifying Who Actually Owes What

Before looking at how executors make mistakes, we need to address a specific scenario that causes immense confusion. Often, a surviving child or relative discovers they had a credit card with their name on it, tied to the deceased parent’s account. They assume they are now personally on the hook for a $15,000 balance.

In reviewing estate files, I frequently have to point out the massive administrative difference between a joint account holder and an authorized user.

If you are a joint account holder, you applied for the credit alongside the deceased. In that specific case, the debt is typically yours. But if you were simply an authorized user, meaning the deceased allowed you to have a card on their primary account for convenience, you are rarely responsible for the primary cardholder’s debt. The debt remains an estate issue.

Collectors will not always clarify this distinction for you on a phone call. Finding out the exact legal status of the account by requesting the original agreement is step one in protecting yourself from paying a bill you do not personally owe.

The Three Procedural Mistakes That Create Personal Exposure

If the financial obligations belong to the bucket, how does an executor end up getting sued? In operations, we track patterns of liability, and they almost always stem from a desire to rush the process, appease family, or stop aggressive phone calls. Here are the three most common ways executors accidentally pierce the veil of their own protection.

Premature Distribution to Beneficiaries

Family members often expect their inheritance immediately. It is common to feel pressured at a memorial service or family gathering to hand out cash because everyone “knows” there are no debts. Giving in to this pressure is the single most dangerous thing you can do.

If you distribute funds to beneficiaries early, and four months later a massive, legitimate hospital bill arrives, the estate bucket is empty. The creditor will investigate and ask why you gave money to the family before clearing the estate’s legal obligations. If you cannot claw that money back from the beneficiaries, you, as the executor, may be held personally responsible for the shortfall. You are penalized for breaching your administrative duty to creditors, not for the debt itself.

Unequal Treatment and Priority Guessing

Estates are bound by strict rules of fairness. Imagine an estate has $10,000 left. An executor might decide to pay an $8,000 credit card bill just to stop the harassing phone calls, leaving $2,000 in the bank. The next week, a $25,000 hospital bill arrives for the deceased’s final week of care.

Because the executor exhausted the funds on a lower-priority unsecured debt, the hospital (which often holds a higher statutory priority for final illness expenses) can legally question those administrative choices. Guessing who to pay first creates severe imbalances if the funds eventually run dry.

Commingling Funds and Poor Documentation

Even if you are completely honest, messy paperwork looks suspicious to an outside auditor. If you pay a final utility bill from your personal checking account, or deposit an estate tax refund into your own bank, you are commingling funds. It becomes impossible to prove what money belongs to who.

⚠️ Warning: Never use cash to settle estate obligations. Cash leaves no auditable trail. Always use checks or traceable electronic transfers from the official estate account, and physically attach the corresponding invoice to the bank statement for your records.

A Practical Workflow for Handling Claims

Protecting yourself does not require a law degree. It requires extreme administrative discipline. Instead of reacting to every piece of mail, you need to build a system that slows the process down and shifts the burden of proof back to the companies demanding payment.

The “Pause and Verify” Rule

A common misconception is that you must write a check the moment an envelope is opened. In reality, the probate process builds in a statutory waiting period specifically so executors can gather the entire financial picture. Depending on your jurisdiction, this creditor claim window often ranges from three to nine months. (Please note that this window varies significantly by local laws and is used here simply as a general illustration).

Use this time. Implement an immediate payment freeze on all historical debts (things owed prior to the date of death). You cannot know if it is safe to pay a minor hardware store bill until you are absolutely certain there is not a massive tax lien waiting to be discovered. Let the mail arrive, open it, log it, and wait.

Demanding Proof of Debt

Not every invoice you receive is a legally valid claim. Sometimes, you will receive notices from third-party junk debt buyers for accounts that are years old and lack any supporting documentation. As a neutral administrator, your job is to demand proof.

Do not simply take a collection letter at face value. Require them to produce the original signed agreement or an itemized final statement showing the date of service. If they cannot produce the underlying paperwork, log their failure to do so in your records.

Building the Master Claim Log

Your best defense is a paper trail that proves you acted methodically. Every time a bill arrives or a collector calls, log the interaction immediately. Do not rely on memory.

| Date Received | Company Name | Stated Amount | Method (Mail/Call) | Action Taken |

|---|---|---|---|---|

| Oct 12 | National Card Services | $1,450.00 | Mail (Statement) | Logged. Sent request for itemized final statement. |

| Oct 15 | Regional Hospital Group | Unknown | Phone call | Refused verbal claim. Requested itemized bill via mail. |

This log demonstrates to any future auditor or judge that you were aware of the claims, actively managed them without bias, and waited for proper documentation before making any distribution decisions.

Stopping the Digital Bleed: Subscriptions and Auto-Drafts

Modern estates face a unique problem that older administrative guides rarely cover: the digital bleed. Today, monthly charges for streaming services, software licenses, gym memberships, and cloud storage will continue to automatically draft from the deceased’s checking account unless actively stopped.

While these are not traditional “debts” in the sense of a loan, allowing them to run unchecked for six to twelve months slowly drains the bucket. One of the highest-value administrative habits you can develop is scanning the last two months of the deceased’s bank and credit card statements specifically for recurring digital charges.

Because you may not have the passwords to cancel these services individually online, the most effective route is often to contact the bank holding the checking account or credit card. Provide your official executor appointment documents and request that the card be canceled and all auto-drafts be frozen to preserve the estate’s remaining assets.

Safe Creditor Communication Strategies

Debt collectors are highly trained to extract verbal commitments. If you use the wrong phrasing on a phone call, you can accidentally imply that you are personally taking on the obligation. Your language must be precise, boring, and relentlessly focused on documentation.

“I am so sorry about this balance. We are waiting on the house to sell, and then I will make sure you get paid next month.”

“I am the executor. The estate is currently in the inventory phase. Please submit your itemized claim in writing to the estate’s mailing address for review.”

The “Before” statement makes a personal promise and implies a timeline. The “After” statement establishes a strict administrative boundary and shifts the burden of proof back to the caller.

Scripts for Managing Contact

Keeping a standard script next to your phone is a massive stress reliever. Here are practical ways to handle common interactions.

Scenario 1: A collector calls your personal phone.

“Hello. I am the executor handling this estate. I cannot process verbal claims over the phone. Please send a complete, itemized statement showing the date of service and the balance owed to the estate’s formal mailing address. Once received, it will be added to the log for review.”

Scenario 2: Requesting a final balance in writing.

Subject: Estate of [Name] – Request for Final Statement (Acct: 1234)

To Whom It May Concern,

I am the executor for the estate of [Name], who passed away on [Date]. I am writing to request a final, itemized statement for account number [1234] as of the date of death.

Please freeze this account to prevent further fees and send the requested documentation to my attention at [Mailing Address]. A copy of my appointment document is enclosed for your records.

Regards,

[Your Name]

Executor

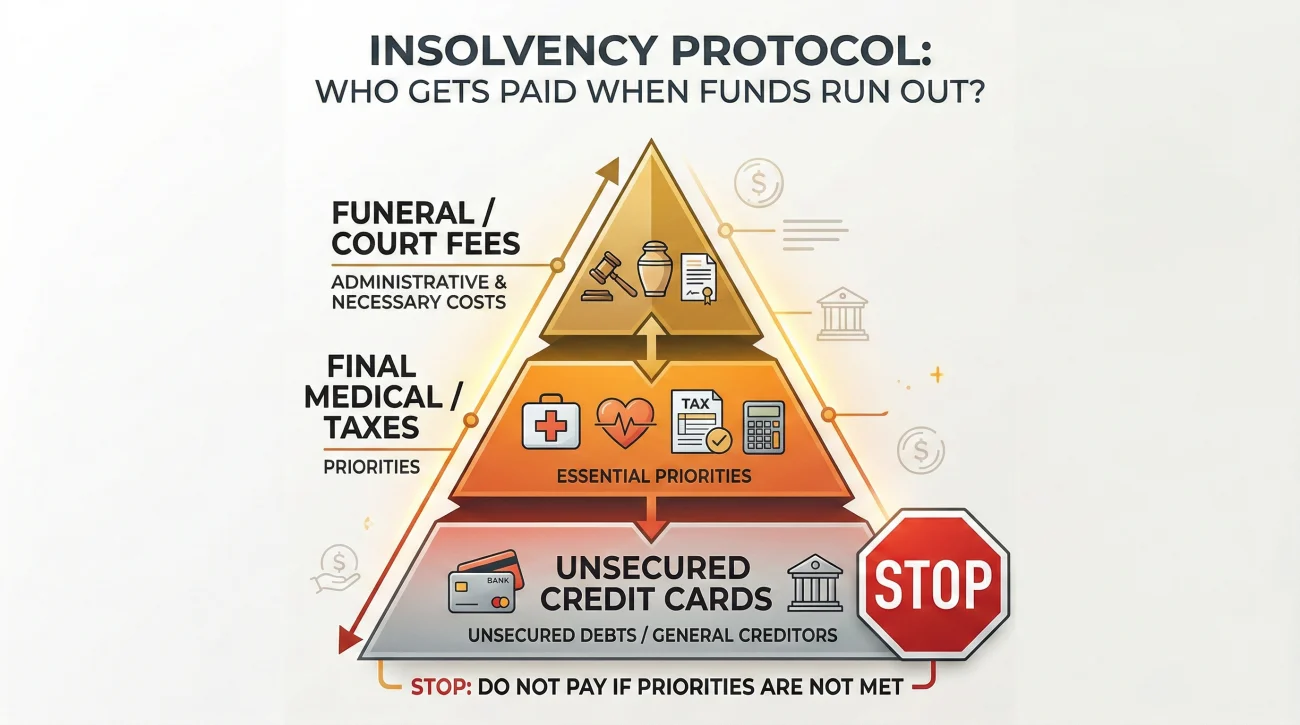

The Insolvent Estate Protocol: When the Math Fails

There is one specific scenario where personal risk skyrockets, and your workflow must change immediately. If you add up the value of the bank accounts, the house, and the car, and that total is smaller than the stack of medical bills and outstanding mortgages, the estate is insolvent.

When there is not enough money to pay everyone, the rules of administration flip. Your role shifts entirely from “paying” to “freezing.”

If you suspect insolvency, you must stop all outbound payments immediately. Do not pay the electric bill, do not pay the credit card, and absolutely do not reimburse family members for minor expenses. Every cent must be preserved. In an insolvent estate, state laws dictate a rigid hierarchy of who gets pennies on the dollar and who gets nothing.

Your job at this stage is to build a highly accurate snapshot of the remaining assets versus the total claims. Once that snapshot is built, you typically hand it to a local attorney who can guide the estate through the formal insolvency procedures required by the court, ensuring you are shielded from creditors angry about taking a loss.

Red Flags That Require Local Professional Help

While the daily logging of mail is a straightforward administrative task, certain complications push the job beyond DIY territory. I always advise executors to recognize the signals that require professional intervention. Paying for an hour of consultation out of estate funds is usually a legitimate administrative expense and the best way to buy peace of mind.

Seek local guidance immediately if you encounter any of the following:

- ✅ You discover pending lawsuits or active judgments against the deceased person.

- ✅ Beneficiaries are aggressively threatening to sue you for not distributing their inheritance fast enough.

- ✅ The deceased owned an active, complex business with its own payroll and commercial creditors.

- ✅ You receive formal demands or legal summons from state or federal tax agencies.

❓ FAQ

🏥 Can a hospital force me to pay a medical bill from my own pocket?

No. Assuming you did not personally sign a financial guarantee document upon their admission, the hospital’s claim is exclusively against the assets of the estate, not your personal bank account.

💳 What if a collection agency buys an old, written-off debt?

Treat it with extreme skepticism. Do not acknowledge the debt or make a small “good faith” payment, which can sometimes restart expired statutes of limitations. Demand they send original proof of the signed contract and the complete account history in writing.

⚰️ Can I safely pay for the funeral upfront with my own money?

While family members commonly front funeral costs, it carries risk if the estate is insolvent. Funeral costs are generally considered high-priority administration expenses for reimbursement, but if the estate has absolutely zero assets, you may not get that money back.

👨👩👧👦 How do I prove to family that I legally cannot distribute money yet?

Do not argue based on emotion. Point to the formal creditor claim window (the statutory notice period) required in your jurisdiction. Explain that distributing funds before that legal window closes exposes you to personal lawsuits, which you will not risk.

🏠 If the house is willed to me, do I inherit the mortgage?

Secured debt generally follows the asset. If you want to keep the house, the mortgage must continue to be paid. However, the distinction between the property having a lien and you taking on personal liability for the loan is complex and requires specific local guidance.

🚗 Should I keep making car payments to avoid repossession?

If the estate or a beneficiary intends to keep the vehicle and there are sufficient funds, maintaining payments prevents repossession. If the vehicle is underwater (owed more than it is worth) and will be surrendered, you should communicate your intent to the lender and pause payments.

📱 What if I can’t find the passwords to cancel digital subscriptions?

Do not waste weeks guessing passwords. The most efficient administrative move is to contact the bank or credit card company, provide your executor credentials, and have the specific cards canceled or frozen to stop future auto-drafts.

📬 Is it safe to just write “Return to Sender, Deceased” on bills?

No. Returning mail hides the claim from you, but it does not erase the debt. As the executor, you need total visibility into what is owed so you can build an accurate inventory. Always open, log, and file financial mail.

📝 A creditor missed the formal deadline, do I still pay them?

This is a strict legal issue because the law often treats “known” creditors (companies you were aware of but failed to properly notify) very differently from “unknown” creditors who suddenly appear late. Because missing a notice requirement could make a late claim legally valid, do not guess; present the late claim to a local professional for review before denying or paying it.

🕵️♂️ Can debt collectors repeatedly call my workplace?

Consumer protection laws generally restrict collectors from harassing you at work or using abusive tactics. If they call, calmly state you are the executor, provide the formal estate mailing address, state that phone calls at work are unacceptable, and hang up.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.