- A notice to creditors is not about inviting bills; it is a formal way to establish a clear timeline and protect the estate from surprise claims years down the road.

- Executors must differentiate between “known” creditors (who usually get direct communication) and “unknown” creditors (who are addressed by public publication).

- The most critical part of this process is tracking: saving the newspaper’s proof of publication, logging the exact dates, and organizing incoming claims without automatically paying them.

The Invisible Clock: Why We Talk About Creditor Notices

When you step into the role of managing an estate, you are immediately hit with a wave of unfamiliar terminology. One phrase you will hear repeatedly from court clerks, attorneys, and guides is the “notice to creditors.” For many people I support in my daily administration work, this phrase causes instant anxiety. It sounds like you are standing on a rooftop with a megaphone, inviting anyone and everyone to come take money out of the estate.

I want to shift how you view this step. In my experience organizing estate workflows, the notice to creditors probate process is actually your best friend. It is not an invitation for chaos; it is a boundary line. It is the mechanism that starts an invisible clock.

Without this notice, an executor is forced to constantly look over their shoulder. You might organize all the finances, pay the obvious bills, and prepare to distribute the remaining funds to the family. But in the back of your mind, you would always wonder: what if a random medical bill or an old private loan surfaces two years from now? The notice process exists specifically to eliminate that exact fear. It forces any outstanding debts to come out of the woodwork within a defined timeframe, or risk being barred permanently.

My goal here is to explain what this notice actually means in plain English, why it matters so much for your own peace of mind, and exactly what documents you need to track when this phase begins. We will not be diving into state-specific timelines or legal statutes, because those vary wildly. Instead, we are going to focus on the operational reality: how to organize the paperwork so you stay in total control.

Why Notice Exists: Creating a Clean Finish Line

To understand the paperwork, you first have to understand the logic behind the system. The legal system recognizes that a person’s financial life is complicated. When someone passes away, they take their memory of their debts with them. Even the most organized person with a perfectly labeled filing cabinet might have a debt that nobody else knows about.

As the person managing the estate, you cannot be expected to magically know every single financial transaction the deceased person ever made. However, you also cannot just ignore the possibility that legitimate debts exist. The notice system is the compromise between these two realities.

I always explain it to families like this: the estate process is like closing down a business. You cannot just lock the doors and walk away. You have to put a sign on the window saying, “We are closing soon. If we owe you money, speak up now.”

By publishing a notice to creditors, you are fulfilling your duty to be transparent. You are giving the public a fair chance to present their bills. In return for doing this properly, the system eventually gives you a clean finish line. Once the formal waiting period expires, you can generally move forward with distributing the assets, knowing that latecomers have lost their right to disrupt the estate. It transforms an open-ended risk into a manageable, time-limited task.

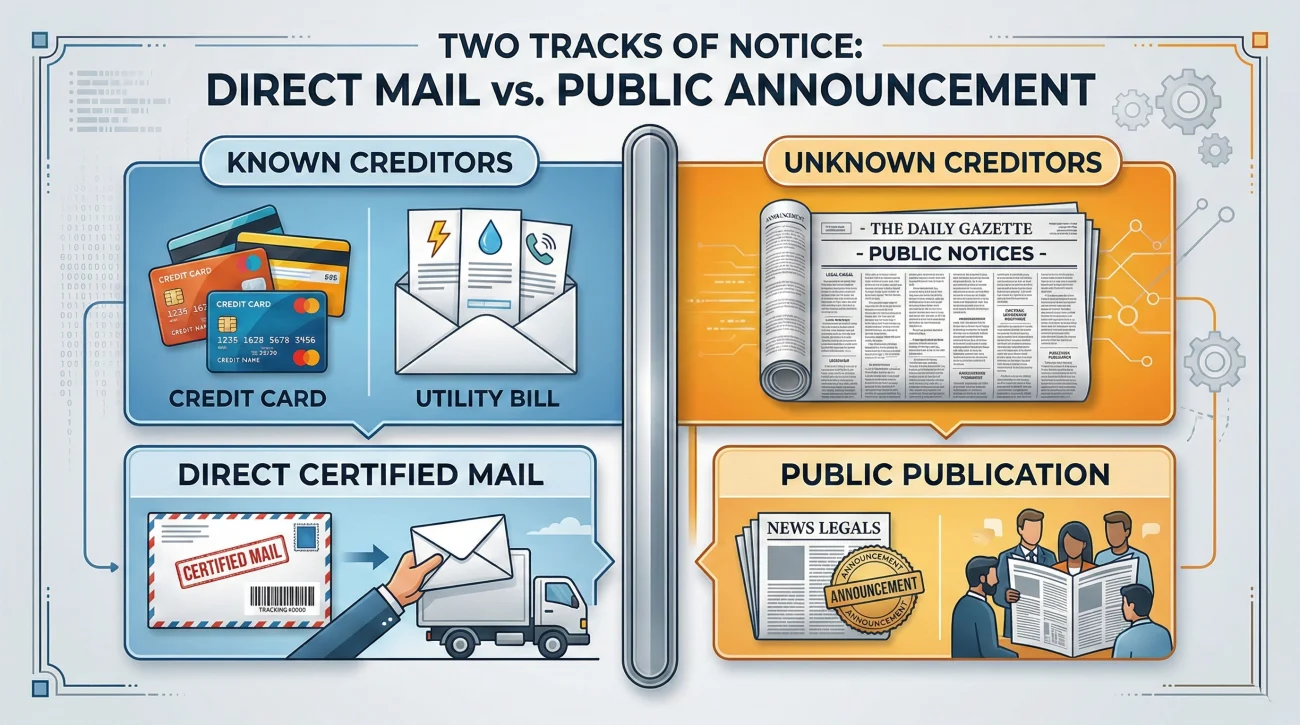

Known vs. Unknown Creditors: The Digital Sweep

One of the most common points of confusion I see involves the difference between known and unknown creditors. The administrative steps you take will depend heavily on which bucket a creditor falls into.

A “known” creditor is a debt that you are reasonably aware of. In the past, this meant finding a recent credit card statement on the kitchen counter or an active mortgage bill in the mail. Today, it also requires a basic digital sweep. I recently worked with an estate where the deceased had zero paper bills in the house, but a quick check of their email and bank autopay history revealed three active online loans and a “buy-now-pay-later” balance. Because these were discoverable in normal records, they are treated as known creditors.

An “unknown” creditor is someone you have absolutely no reasonable way of finding. Perhaps the deceased co-signed a lease for a friend years ago, or they had a minor fender-bender just before they passed away and the other driver has not filed an insurance claim yet. There is no paperwork, physical or digital, to follow.

Typically requires direct, written notification. Because you know they exist and have their address, you mail them a letter stating the person has passed and telling them where to send their formal claim.

Handled through public publication. Since you do not know who they are, you publish the notice to creditors newspaper announcement. This serves as a blanket, public notification.

From a tracking perspective, this means you will have two distinct paper trails: a log of letters you mailed directly, and a formal newspaper publication proof for the unknown entities.

The Tracking Method: What to Log When Notice Begins

This is where the theoretical concept of the notice becomes a practical desk job. The actual act of publishing or mailing a notice is usually simple. The place where executors get into trouble is failing to maintain a pristine paper trail of what happened and when.

I cannot stress this enough: your memory is not a reliable filing system. When you are managing dozens of administrative tasks, you will not remember exactly which date the newspaper ad ran, or which day you mailed the letter to the hospital.

<strong⚠️ Warning: The most frequent operational failure I see is a lost Affidavit of Publication. When a newspaper runs your notice, they will mail you a sworn document proving the ad ran on specific dates. Because it often comes in a generic envelope that looks like an advertising invoice, executors frequently throw it away. Treat this document like a legal receipt; you will likely need to file it with the court.

Building Your Creditor Tracking Log

Once you understand the stakes of securing that publication proof, the next step is building a central place to record every other interaction. I always start families with a simple spreadsheet or a dedicated notebook before they send out any letters. Here are the columns I recommend:

| Creditor Name | Notice Sent/Pub Date | Method of Notice | Claim Received Date | Stated Amount | Status (Review/Hold) |

|---|---|---|---|---|---|

| Local Daily Newspaper | Oct 12, Oct 19, Oct 26 | Publication | N/A (Affidavit received Nov 2) | N/A | Affidavit Filed |

| Major Credit Card | Oct 15 | Certified Mail | Pending | Unknown | Waiting on Claim |

| City Hospital | Oct 15 | Certified Mail | Nov 10 | Check invoice | Logged, Under Review |

Notice that the final column is “Status (Review/Hold)” and not “Paid.” Receiving a claim does not mean you write a check that same afternoon. Before you start paying anything, you need to map out your overall strategy. I always advise families to establish a safe order of operations for handling estate debts so they know exactly what to pay first and what to pause.

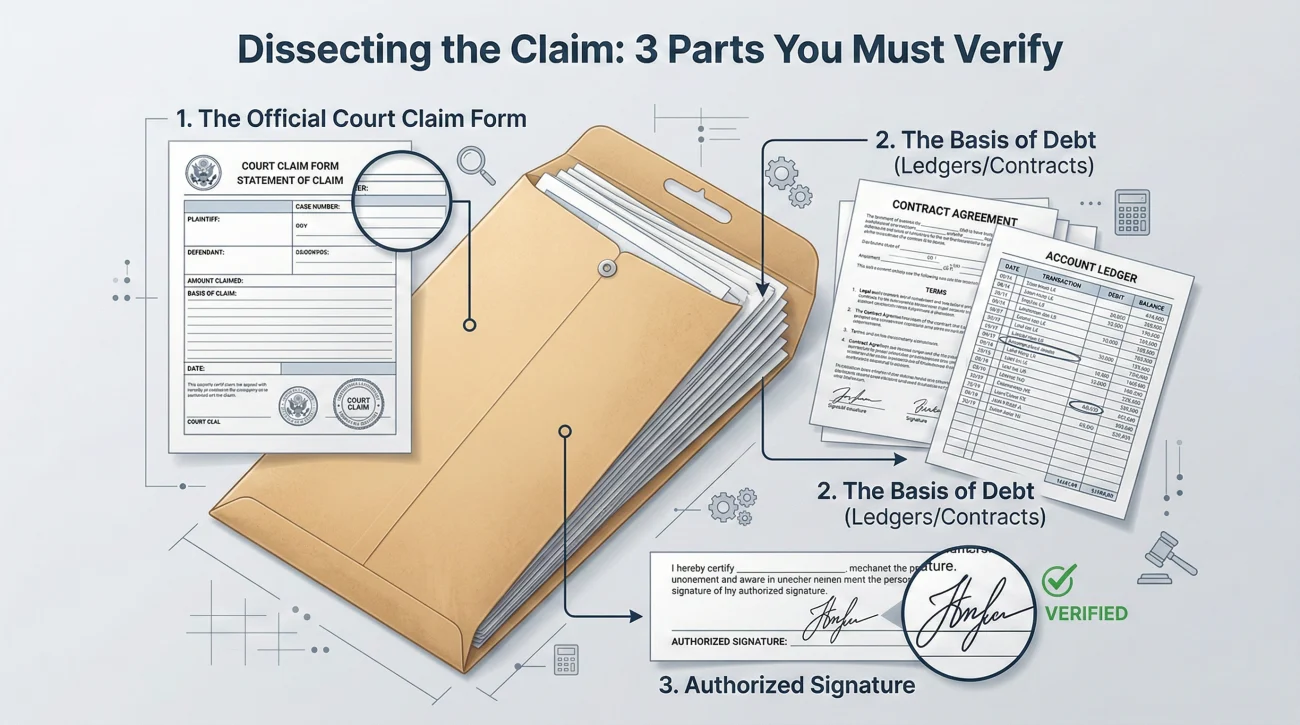

Anatomy of a Creditor Claim: What Usually Arrives

So, you have published the notice and mailed your letters. Often, the mail starts changing. Instead of standard monthly statements, you will start receiving formal creditor claims.

A formal claim is usually not just a casual letter saying “please pay us.” For example, a standard hospital claim usually arrives as a thick envelope containing the court’s official cover form on top, followed by a sworn statement from the billing department, and a multipage printout of the patient’s itemized ledger showing specific billing codes and dates of service.

- 📄 The Claim Form: States the name of the estate, the creditor’s contact info, and the exact dollar amount owed.

- 📄 The Basis of the Debt: Attachments proving why the money is owed, like a signed contract or medical ledger.

- 📄 Signature: Typically signed by an authorized representative stating the debt is valid and unpaid.

Handling Disputed Claims

When a packet arrives, your first job is purely administrative: open it, date-stamp it, scan a copy into your folder, and log it into your spreadsheet. But what happens if you receive a claim that looks completely wrong? Perhaps a contractor files a claim for home repairs, but you already found a cashed check from the deceased paying that exact bill.

If you suspect a claim is invalid, exaggerated, or already paid, log it anyway. Write “Disputed – duplicate payment” in your spreadsheet notes and set the file aside for professional review. Do not ignore the claim, but do not call the creditor to argue with them either. Your legal advisor will guide you on the formal process for rejecting or challenging a claim safely.

When Collectors Call the Family Directly

While we are discussing incoming claims, I want to address a very common and stressful scenario. Before formal claims are filed, collection agencies will often bypass the mail and call the deceased person’s children or spouse directly, demanding immediate payment over the phone.

I have seen grieving families panic and pay out of their own personal checking accounts just to make the phone calls stop. Remember this fundamental rule: family members do not personally inherit debt. The estate owes the money, not the children.

If a collector calls your personal phone, do not negotiate or explain the estate’s finances. Politely state, “This account is being handled through the estate. Please submit a formal written claim.” Then hang up, block the number if necessary, and log the call in your records.

The Insolvent Estate: When There Isn’t Enough Money

As claims roll in and you log them in your spreadsheet, you must keep an eye on the total. What happens if the claims add up to $50,000, but the estate bank account only holds $10,000? This is known as an insolvent estate.

If you suspect the money will run out, you must pause all payments immediately. You cannot simply pay the creditors who asked first. The law dictates a strict priority order for who gets paid when funds are short. Usually, administration costs and funeral expenses take priority over standard credit card debts or personal loans.

If you guess the priority order and pay a credit card bill first, leaving no money for the final tax return, you could be held personally liable for that mistake. If the math looks tight, freeze the checkbook and get local legal guidance before a single dollar leaves the account.

The “Nobody Reads the Newspaper” Misconception

If I had a dollar for every time an executor asked me, “Why am I paying to publish this in a newspaper? Literally no one reads print media anymore,” I could retire early. I completely understand the frustration. It feels like an outdated practice in a digital world.

Field Note: I once saw an estate preparing to close when a major national bank suddenly filed a $15,000 claim on the final allowable day. The bank did not receive a direct letter; instead, their automated software had scraped the local newspaper’s legal notices, flagged the deceased’s name, and generated the claim. The system absolutely works, even if your neighbors aren’t reading the paper.

Do not try to outsmart this step. Do not skip the publication because you think the deceased had no debt. You are publishing the notice to satisfy a procedural requirement that starts the legal countdown clock. If the local process requires it to close the estate safely, you treat it as a mandatory administrative chore.

How to Verify Local Requirements Safely

Because the rules regarding how long a notice must run, which newspapers are acceptable, and how many days creditors have to respond are intensely local, I will never give you a generalized timeline. Assuming that your county follows the same rules as a neighboring county is a massive mistake that can force you to restart the entire process.

Your responsibility is to verify the exact requirements in writing. Do not rely on a quick phone call where you might mishear a deadline. Go straight to the source.

💡 Pro Tip: Many local court websites maintain an “Approved Publications List.” This is a specific roster of local newspapers legally authorized to run estate notices. Using a paper that is not on this list, even if it is cheaper, can invalidate your notice.

If you are working with an attorney, they will usually handle the mechanics of this for you. But if you are managing the administration and need to request guidance from the court clerk, keep your communication brief, polite, and focused entirely on the procedural steps. Here is a safe way to ask:

Subject: Request for creditor notice publication requirements – Estate of [Deceased Name]

Hello,

I am currently organizing the administrative steps for the Estate of [Deceased Name]. Could you please provide the written guidelines regarding the notice to creditors?

Specifically, I am looking to confirm:

1. The list of approved publications/newspapers for this jurisdiction.

2. The required frequency for running the notice.

3. Which specific form or template must be submitted to the publisher.

I want to ensure my records are fully compliant before proceeding. Thank you for your guidance.

Best regards,

[Your Name]

Your Notice to Creditors Action Checklist

Handling the notice to creditors is largely an exercise in patience and precise filing. To keep yourself organized, follow this summary checklist as you move through this phase of the estate administration:

- ✅ Step 1: Identify known creditors via paper mail and a basic digital sweep of emails and autopay records.

- ✅ Step 2: Request the approved publication list and notice rules from your local court clerk in writing.

- ✅ Step 3: Set up your creditor tracking spreadsheet before sending any communication.

- ✅ Step 4: Mail formal written notices directly to the known creditors you identified.

- ✅ Step 5: Submit the required publication request to the approved local newspaper.

- ✅ Step 6: Secure and safely file the Affidavit of Publication when the newspaper mails it back to you.

- ✅ Step 7: Direct family members to tell calling collection agencies to “submit a formal written claim” and hang up.

- ✅ Step 8: Log all incoming physical claims immediately, without paying them.

- ✅ Step 9: Flag any disputed or suspicious claims for professional review.

- ✅ Step 10: Pause all payments and seek help if the total claims start exceeding the estate’s available funds.

The effort you put into tracking the notice process today is exactly what will protect you and the family from surprises a year from now.

❓ FAQ

🧭 What is a notice to creditors in probate?

It is a formal, public announcement that a person has passed away and their estate is being settled. It serves as an official call for anyone who is owed money by the deceased to submit their bills within a specific timeframe.

📰 Do I have to publish a notice to creditors in the newspaper?

In most jurisdictions, yes. Even if you know of no debts, publishing in an approved local newspaper is typically a mandatory administrative step to formally start the deadline clock for unknown claims.

✉️ Do I use the same form for known and unknown creditors?

Usually, no. Known creditors typically receive a direct, physical letter in the mail, while unknown creditors are addressed broadly through the public newspaper publication. The documentation you track for each method is different.

⏳ How long do creditors have to submit a claim after the notice?

This timeline is strictly determined by local rules. It commonly ranges anywhere from a few months to nearly a year after the notice is first published. You must verify the exact duration with your local court or legal advisor.

🛑 What happens if I do not publish the notice to creditors?

If you skip this step, the legal clock for creditors to submit claims often never starts. This means a creditor might legally demand payment years later, long after the estate’s money has been distributed, creating severe complications.

📧 Can I just email the notice to creditors instead of mailing it?

Direct mail is much safer. For known creditors, courts usually expect formal written letters, often sent via certified mail, to generate a verifiable paper trail that proves the entity actually received the warning.

🗂️ What should I do with the Affidavit of Publication?

Treat it as an essential legal receipt. You or your attorney will eventually need to file this original sworn document with the probate court to prove that the public clock was started legally.

🚫 If a creditor misses the deadline, do I still have to pay them?

If you followed all notice procedures correctly and a claim arrives after the formal deadline has passed, the claim is often legally barred, meaning the estate may no longer be required to pay it. However, always have a professional confirm a claim is truly barred before rejecting it.

🏛️ Does the court automatically publish the notice for me?

You should assume this is your responsibility. While the court provides the initial authorization, the executor usually has to handle the administrative task of contacting the newspaper, paying the fee, and securing the paperwork.

📍 How do I know which newspaper to use for the notice?

You cannot use just any paper. Most courts maintain a specific list of “approved legal publications” for the county where the deceased lived. You should ask the court clerk for this specific list to ensure your notice is valid.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.