- The goal is a structured search, not perfection: You do not need to be a private investigator to identify creditors; you need a methodical, documented process using available records.

- Use the two-pass method: Start with a quick physical scan of mail and workspaces, then do a deep scan of bank statements to catch hidden auto-pays and loans.

- Never guess or promise payment: When a potential debt surfaces, log it and request written proof. Do not make verbal commitments to callers.

- Document everything you find: Build a clean, readable creditor list that tracks the entity, the claimed amount, and the date you discovered it.

The Overwhelming Fear of Missing a Hidden Debt

When I speak with people who have just taken on the role of executor, one of their most common anxieties sounds like this: “What if I miss a debt, and they come after me later?” It is a highly stressful position to be in. You are looking at a house full of paperwork, a mailbox that keeps filling up, and you have no idea who the deceased person actually owed money to.

In my experience supporting estate administration workflows, I find that executors often freeze during this discovery phase. They worry they need to pull credit reports or hire professionals just to figure out the baseline. While complex estates might require professional tracing, the vast majority of creditor discovery comes down to a calm, methodical review of household routines and financial statements.

You do not need to uncover every secret overnight. You just need a practical search map to find the creditors of the deceased, verify their claims, and document your findings safely. Let us walk through how to build that map without over-collecting unnecessary data or accidentally taking on personal liability.

What Actually Counts as a “Creditor” in Estate Administration?

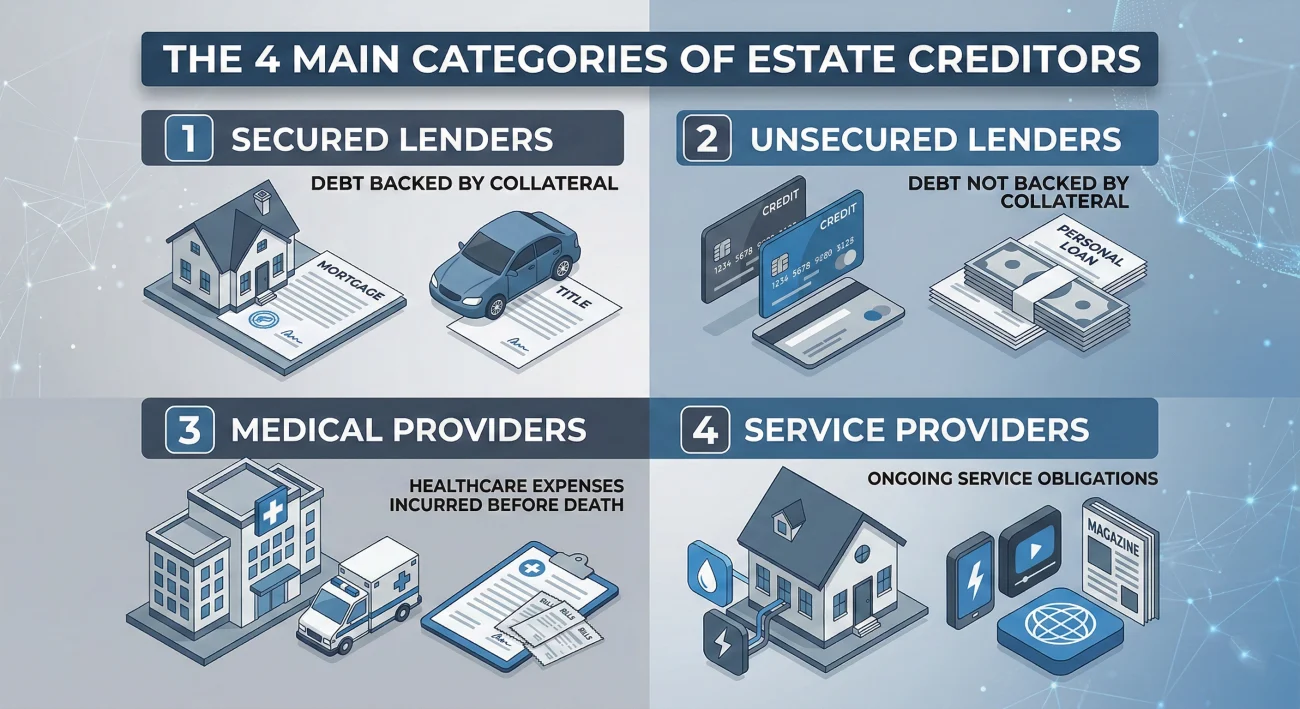

Before we start looking for debts, it helps to define exactly what we are looking for. In the context of an estate, a creditor is simply any person, company, or government agency that has a valid legal claim against the deceased person’s assets.

We typically see creditors fall into a few predictable categories during the discovery phase. First, there are secured lenders, such as the mortgage company, the car loan provider, or anyone holding a lien against physical property. Because these debts are tied to a specific asset, they often require immediate organizational attention to prevent foreclosure or repossession.

Next are unsecured lenders, which include credit card companies, personal loan issuers, and payday lenders. These claims rely solely on the deceased person’s general promise to pay, making them incredibly common but entirely separate from the physical property.

You will also encounter medical providers. This category frequently includes hospitals, ambulance services, nursing facilities, and individual specialists connected to final illness care. Finally, there are standard service providers, such as utility companies, cell phone carriers, and subscription services that are owed a final balance for household operations.

Key Point: Just because someone claims to be a creditor does not automatically mean the estate owes them money. Your job in this phase is to identify the claims and log them, not to instantly validate or pay them.

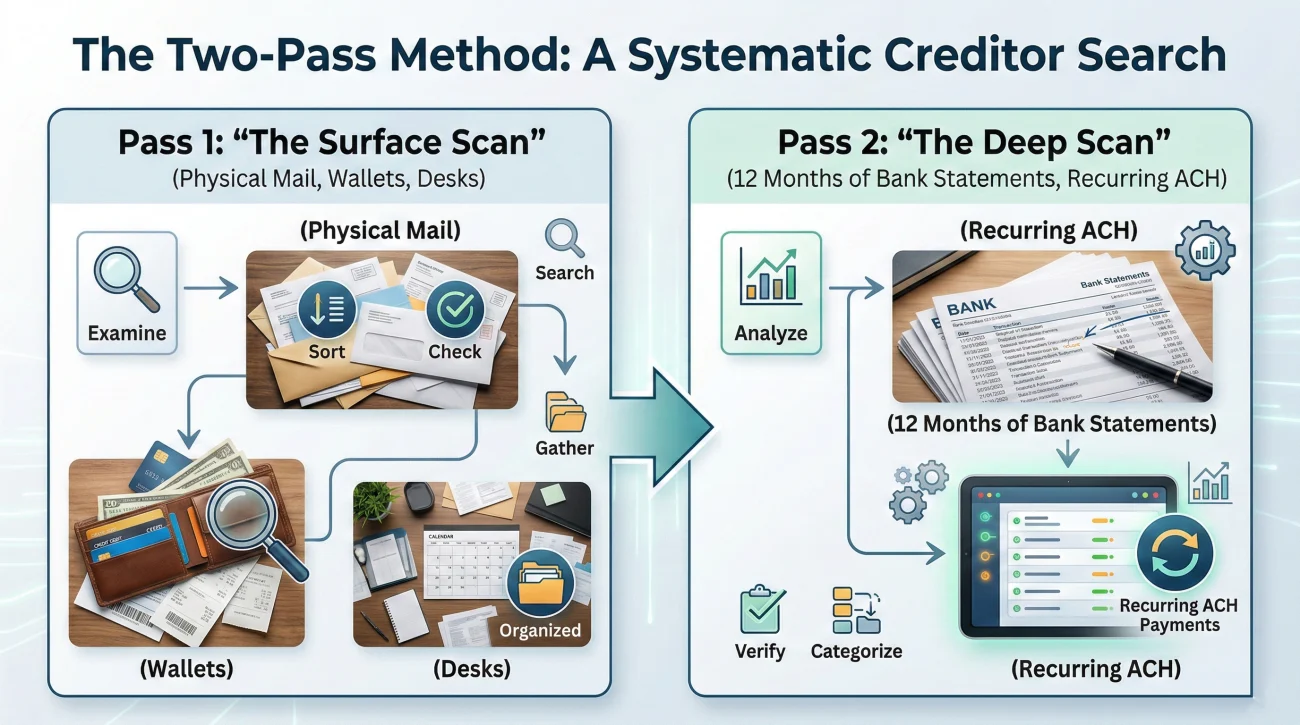

The Two-Pass Search Method: A Practical Workflow

When you are staring at a lifetime of paperwork, you need a system. I always suggest using a “two-pass” method. This keeps you moving forward without getting bogged down in reading every single receipt from ten years ago.

Pass 1: The Quick Surface Scan

Your first pass is purely physical. You are looking for the obvious, glaring debts. Set up a dedicated folder labeled “Potential Creditors” and start gathering.

During this phase, check the physical mailbox daily. Watch the mail for at least four to six weeks. Creditors operate on monthly billing cycles, so if a credit card has an outstanding balance, a physical statement or a past-due notice will usually show up within a month.

Next, check the usual physical drop zones in the home: the kitchen counter, the home office desk, and the deceased’s wallet. You are looking for recent utility bills, collection letters, mortgage statements, and medical invoices.

Pass 2: The Deep Financial Scan

Physical mail will only show you half the picture. In today’s digital world, many people opt out of paper statements entirely. To find the rest of the creditors, you have to follow the money.

Once you have the legal authority to request records from the deceased’s bank, ask for the last 12 months of checking account statements. You are not looking at what they bought at the grocery store; you are scanning for regular, recurring outbound payments.

Look for these common indicators on the bank statements:

- Recurring monthly ACH transfers to entities with “Bank,” “Credit,” or “Financial” in the name.

- Payments made every three or six months (commonly insurance premiums or property taxes).

- Payments to unfamiliar individuals that might indicate a private loan.

💡 Pro Tip: If you see a payment for a storage unit, treat the storage company as a potential creditor and contact them immediately. Unpaid storage units can be quickly auctioned off, potentially losing valuable estate assets.

Where Unknown Creditors Typically Hide

Even with a solid two-pass search, some debts are stubborn and hard to find. As you build your deceased debts checklist, be aware of these common hiding spots that might delay your final tally.

Medical Billing Lag

Medical debts are notorious for arriving late. A hospital might take 60 to 90 days after the date of service to process insurance and send the final patient balance. Do not assume that a quiet mailbox in month two means there are no medical creditors.

Annual Subscriptions and Memberships

Some debts do not show up on a monthly bank statement because they only bill once a year. Think about annual HOA dues, software subscriptions, or country club memberships. This is exactly why your deep financial scan needs to look back a full year, as shorter windows easily miss these infrequent charges.

Digital Portals

If the deceased managed everything on their smartphone, you might face a challenge. I heavily caution against trying to guess passwords or access digital accounts without authorization, as this can violate terms of service and create legal headaches. Instead, monitor the email inbox if you have lawful access to it, looking for subject lines like “Your payment is due” or “Action required on your account.”

How to Build a Readable Creditor List

Finding a bill is only step one. Step two is getting it out of a messy pile and into a structured log. A scattered approach leads to missed communications and angry collectors. You need a centralized list.

Whenever you identify a potential debt, log it immediately. I recommend keeping a simple spreadsheet or a dedicated notebook with clearly defined columns. You want to capture just enough data to track the debt without writing a novel.

| Creditor Name | Account / Reference # | Claimed Amount | Source of Discovery | Status / Next Step |

|---|---|---|---|---|

| Capital One Credit | Ending in -4452 | $1,240.00 | Mail (Statement dated 10/14) | Send death cert, request final balance |

| Dr. Smith Cardiology | Patient ID #8890 | Unknown | Bank statement (past payments) | Call billing, request final invoice |

| State Auto Finance | Loan #77654 | $12,500.00 | Physical file cabinet | Request payoff amount in writing |

By using a format like this, you create a clear snapshot of the estate’s liabilities. If a beneficiary asks why a house sale is delayed, you can point to the pending status of known creditors on this list.

What NOT to Do During the Discovery Phase

When executors feel pressured, they sometimes make quick decisions that complicate the estate later. The discovery phase is strictly about information gathering. It is not the time to open your checkbook.

⚠️ Warning: The most common mistake I see is an executor writing a check from their personal account just to “make a collection agent go away.” This can muddy the waters and make it incredibly difficult to get reimbursed by the estate later.

As you contact potential creditors to gather information, stick to these boundaries:

- Do not promise payment: You do not yet know if the estate is solvent (has enough money to pay everyone). Promising payment to one creditor might unfairly prioritize them over another.

- Do not share unnecessary personal data: If a creditor calls you, do not provide your own Social Security Number or personal banking details. You are acting in an official capacity for the estate.

- Do not guess on amounts: If you find an old statement, do not assume that is the final balance. Fees and interest accrue. Always ask for the claim in writing as of the date of death.

If you find yourself on the phone with a collector who is pushing you for immediate action before you have finished gathering your list, use a neutral, boundary-setting script.

Phone Script: Setting Boundaries with a Collector

“Hello, I am the executor for the estate of [Name]. I am currently in the process of identifying all estate obligations. Please place a hold on this account and mail a formal, written statement of the final balance to [Estate Mailing Address]. I cannot process or discuss any payments until I receive the written claim and complete my review of the estate.”

When to Stop Searching and Start Tracking

A common question is, “How do I know when I have found everyone?” The reality is that you can never be absolutely, 100% certain that an unknown creditor will not surface. However, you cannot keep the estate open forever waiting for a phantom bill.

Generally, the intensive search phase slows down after the first two to three months. By this time, the monthly billing cycles have rolled over, you have reviewed the bank statements, and the bulk of medical and utility bills have arrived in the mail. This is the moment when your focus naturally shifts from searching for debts to tracking the ones you have successfully identified.

Keep in mind that if your local jurisdiction utilizes a formal “notice to creditors” process, often involving a newspaper publication to set a legal time limit for unknown creditors to come forward, this is typically the time that process runs in the background. Always check with local professionals on how to safely close the window for unknown claims in your specific area. Once you have built your baseline list and verified those local timelines, you are ready to transition out of the discovery phase.

Final Thoughts on Building Your Creditor Map

Identifying creditors as an executor is an exercise in organization, not detective work. Your goal is simply to build a clean, accurate inventory of who believes they are owed money.

Rely on the paper trail you have gathered and keep a meticulous log of every entity that steps forward. By keeping your boundaries firm and requiring all creditors to submit their claims in writing, you protect yourself from personal liability and ensure that the estate is handled with absolute transparency.

Remember, taking your time during the discovery phase is a sign of a responsible executor. Do not let collection calls rush your process. As you move from gathering these claims to actively managing them, I suggest keeping our Executor Creditor and Debt Checklist handy as a guide for what to pay, what to pause, and how to maintain clean records moving forward.

❓ FAQ

🎙️ How do I find out who a deceased person owes money to?

Start by monitoring their physical mail for at least 30 to 60 days to catch billing cycles. Next, review their most recent 12 months of bank statements to look for recurring electronic payments or checks written to lenders and service providers.

📬 Will creditors automatically notify the executor?

Not always. Creditors do not automatically know someone has passed away until they are notified. They will continue sending bills to the deceased person’s address on file, which is why monitoring the mail is so critical.

💳 What if I find a credit card bill but no statement?

Log the name of the credit card company and the partial account number (usually found on the card itself). Contact them via their estate handling department, notify them of the death, and request a final written statement.

🏥 How long do hospitals take to send a final bill?

It can often take anywhere from 30 to 90 days for hospitals to finalize bills. They usually must process claims through Medicare or private insurance first before sending the final balance due to the estate.

📱 Do I need to check the deceased person’s email for bills?

If you have legal access and the passwords were provided to you, checking email is a great way to find paperless billing. However, avoid trying to bypass security or guess passwords, as this can violate provider terms of service.

🕵️♂️ Should I hire a private investigator to find debts?

In most standard estates, this is not necessary. A thorough review of mail, bank statements, and household files is usually sufficient to identify the vast majority of valid creditors.

🛑 What if a debt collector calls before I’ve found their bill?

Do not panic and do not promise payment. Log their name, company, and phone number. Ask them to mail a formal, written statement of the claim to the estate’s mailing address for your review.

💸 Can I just pay the bills as I find them?

No, this is a common mistake. If the estate runs out of money, you may have unfairly prioritized one creditor over another. Always build your complete list first and understand the total financial picture before making payments.

📄 Do I have to pay unknown creditors if they show up later?

This depends on local procedures. Many places have a formal “notice to creditors” process that creates a strict deadline. If a creditor misses that legal deadline, their claim is often barred, but you should verify this timeline with a local professional.

🏦 Will the bank give me a list of the deceased’s debts?

A bank will only give you information regarding debts held directly with that specific bank (like their mortgage or credit card). They do not have a master list of debts owed to other outside companies.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.