- Preparation is protection: Gathering the right open estate bank account documents before you visit the branch reduces the chances of being turned away or stuck in endless legal reviews.

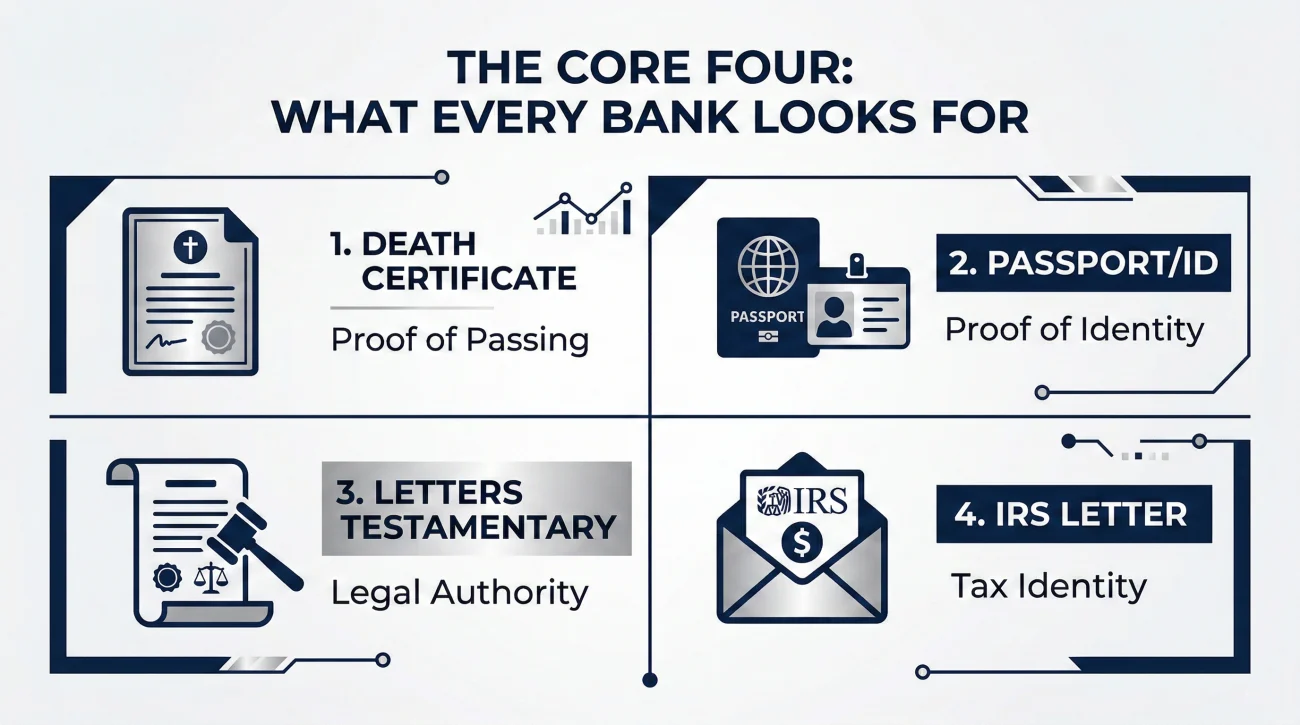

- The core four: Banks generally look for proof of death, proof of your identity, proof of your authority, and a new tax identity for the estate.

- The photocopy rule: Bank compliance teams require certified copies with raised seals or official stamps for legal documents, not home printouts.

- Perfect matching matters: Discrepancies between the name on the death certificate and the name on your court documents commonly cause unexpected account freezes.

The Preparation Gap: Why the First Bank Visit Often Fails

In my time helping people organize estate administration tasks, I often see the initial bank visit become an unexpected bottleneck. Just recently, an executor spent an hour carefully gathering documents and took time off work, only to be turned away at the branch desk. The reason? A middle initial on the court order did not perfectly match the spelling on the death certificate. The bank associate typed into their system, apologized, and said they could not open the account that day.

This is an incredibly common scenario. It happens because executors often bring what they logically think the bank needs, rather than what the bank’s back-office compliance team actually requires. When an institution is notified of a death, their primary goal is to lock down liability.

If you are trying to figure out the exact estate account requirements, the secret is shifting your mindset. You are not just walking in to open a checking account. You are walking in to prove a chain of facts. In this guide, I will walk you through what banks commonly ask for, where the hidden operational traps are, and how you can organize your paperwork to make that branch visit successful.

Key Point before We Start: Remember that an estate account is not a continuation of the deceased person’s old checking account. It is an entirely new, separate financial bucket that operates under a new tax identification number, managed solely by you.

The Common Requirement Categories: What the Bank Evaluates

When you sit down at the banker’s desk, they are simply collecting evidence to satisfy four main categories of verification. While every institution has its own specific internal manual, I commonly see them look for proof of the passing, proof of your identity, proof of your legal authority, and a tax identity for the new account.

⚠️ The Golden Rule of Bank Packets: Bank compliance teams almost universally reject home photocopies of legal documents. You must bring the freshly issued, certified copies with raised seals, watermarks, or official colored ink. The bank will inspect the original seal, make their own internal copy, and usually hand your certified version back to you.

Let us break down exactly what goes into each of these four categories.

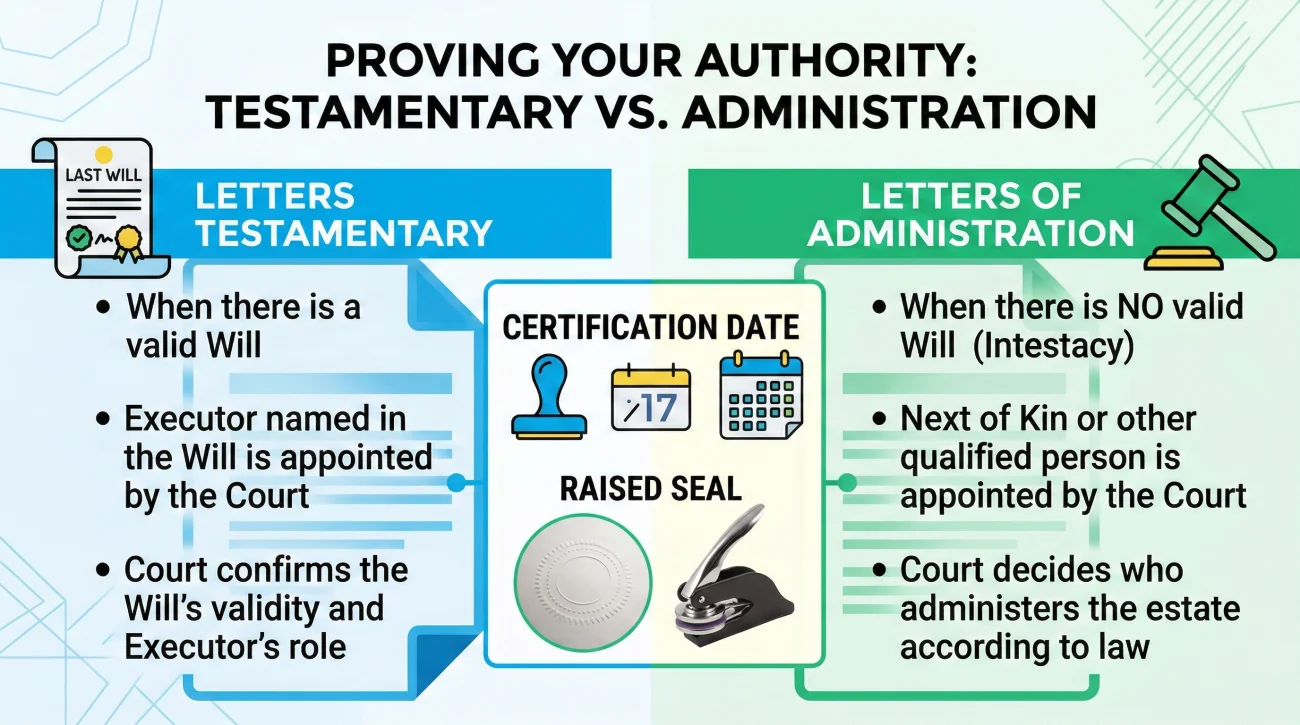

Category 1: Proving the Passing

The first document the bank will ask for is the official death certificate. This serves as the foundational proof that the original account owner is deceased and that their personal accounts should be formally transitioned or closed.

In practice, I always suggest keeping at least three certified copies in your master folder when you go to the bank. While the associate will only scan one, having backups prevents panic if you accidentally drop or damage a copy. More importantly, take five minutes to review the certificate line by line before your appointment. If you spot a typo, such as a missing suffix or an incorrect digit in the Social Security Number, do not expect the teller to overlook it. You will generally need to request a formal amendment through the funeral home or vital records office before the bank’s compliance team will clear the document.

Category 2: Proving Your Identity

You might be opening the account for the estate, but the bank needs to verify exactly who is operating it. They will run your personal name through their standard security and identity verification protocols.

You will typically need to bring your unexpired, government-issued photo ID, such as a driver’s license or a passport. A frequent point of friction I see is when an executor’s current home address does not match the address listed on their driver’s license. If you recently moved, the bank might ask for a secondary form of proof, like a recent utility bill in your name. It is always a smart habit to bring a secondary form of ID just in case.

Category 4: The Tax Identity Switch (Estate EIN)

When someone passes away, their Social Security Number essentially stops being active for new financial reporting. You cannot open a new estate bank account using the deceased person’s SSN, and you definitely should not use your own personal SSN.

You need an Employer Identification Number (EIN) for the estate. Despite the word “employer,” this is simply a tax ID format used by the IRS for businesses, trusts, and estates. When you sit down with the banker, they will universally ask for the official IRS confirmation letter showing the estate’s new EIN.

The bank uses this number to set up the account’s tax profile, ensuring that any interest earned is correctly reported to the estate. Some banks may also ask you to fill out an IRS Form W-9 at the desk to formally certify that the EIN you are providing is accurate.

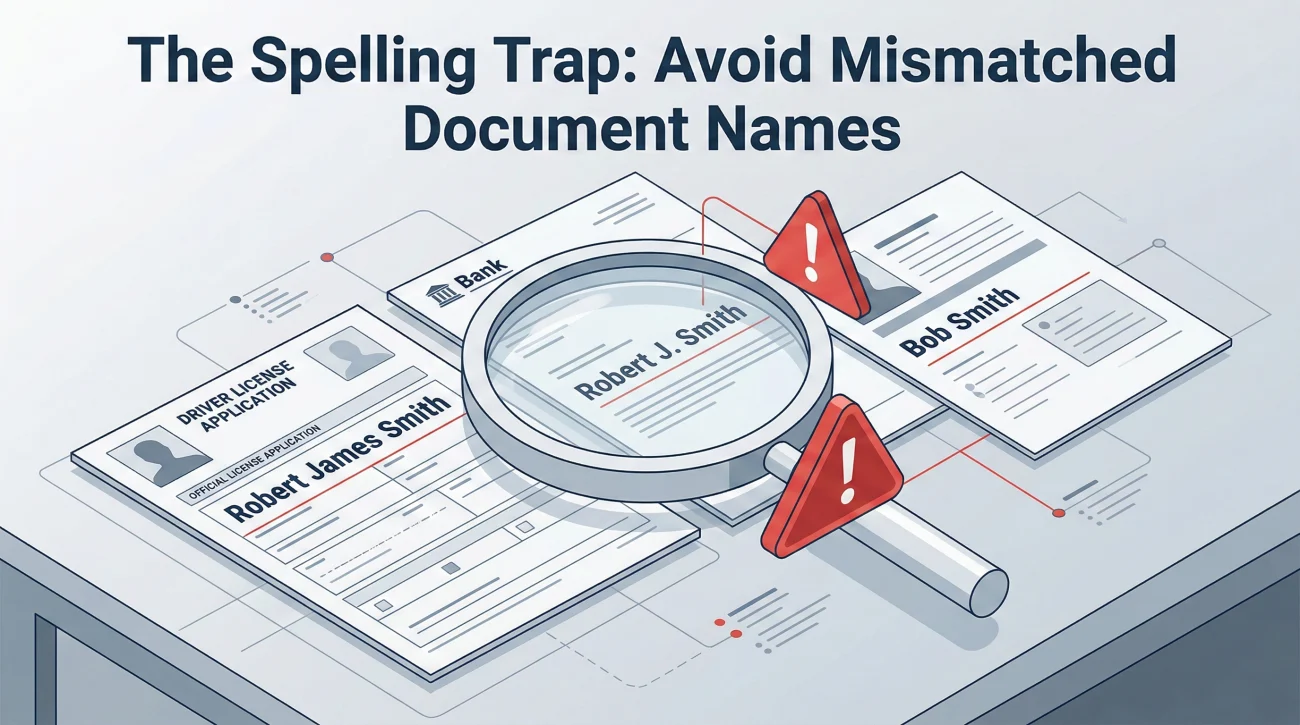

The Spelling Trap: Why Exact Name Matching Matters

If there is one hidden operational hazard I want you to be aware of, it is name matching. When you hand over your stack of documents, the bank associate will cross-reference all of them to make sure the names align perfectly.

I frequently see account openings stall because of minor discrepancies. If the death certificate says “Robert James Smith,” the court letters say “Robert J. Smith,” and the EIN confirmation says “Bob Smith Estate,” the bank’s legal department might flag the file and refuse to open the account until the documents are formally amended.

Before you go to the bank, lay your death certificate, your court letters, and your EIN paperwork on a table. Look at how the deceased person’s name is spelled. If there is a discrepancy, be prepared for the bank to ask questions, or proactively bring secondary documentation that ties the names together.

The Co-Executor Complication

When a judge appoints two people to serve as co-executors, the administrative workload does not get cut in half; at the bank, it usually doubles. Banks treat co-executor situations with extreme caution because they must ensure neither person is acting unilaterally against the court’s exact orders.

Many banks have strict policies requiring all named co-executors to be physically present at the branch to sign the initial signature cards. If one executor lives out of state, the local branch might refuse to open the account with only one signature. In these cases, you often have to work with the bank’s national estate department to facilitate mailing signature cards or arranging for the out-of-state executor to visit a branch local to them.

Furthermore, you will need to establish how checks are signed. Banks will ask if the account should be set up as “Executor A OR Executor B” (either can sign alone) or “Executor A AND Executor B” (both signatures required on every check). The “AND” setup is safer for preventing disputes, but it creates a massive logistical headache when trying to pay routine bills.

The Communication Habit That Saves Trips

Because bank policies vary widely, the best operational habit you can build happens before you ever leave your house. Never assume that the general requirements listed on a bank’s public marketing website are the exact rules the local branch manager will enforce on the ground.

Before you drive to the branch, use this simple communication hygiene practice: call the specific location you plan to visit and ask them to email you their exact checklist. It is also highly recommended to schedule an appointment rather than just walking in, as estate account openings often take an hour to process.

Sample script for calling the bank:

Hello, I have been appointed as the executor for [Name]’s estate and I need to open an estate checking account. Before I schedule an appointment, could you please provide a written list of the exact documents your branch requires to open the account? I want to make sure I have the correct certifications so we do not waste anyone’s time.

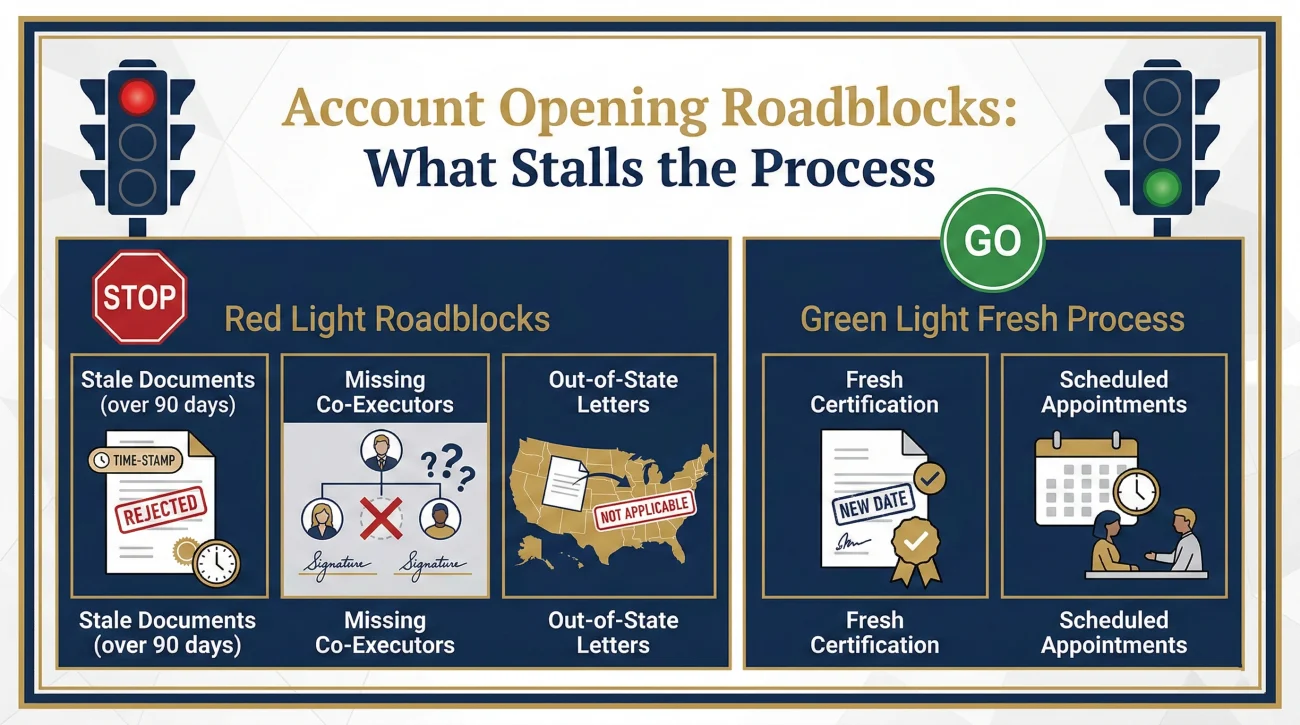

Common Reasons the Account Opening Stalls

Even if you bring what you think is a perfect packet, delays can happen. Often, the person at the desk cannot make the final decision. They scan your documents and send them to an internal back-office legal department for review.

| The Roadblock | What It Usually Means |

|---|---|

| “We need to schedule this with a manager.” | Standard branch tellers usually cannot open estate accounts. If you walk in without an appointment, the specific relationship banker authorized to review legal documents might not be scheduled that day. |

| “This has to go to legal review.” | This is standard practice at many large national banks. Do not panic. They are simply having a specialist verify the court seal and the authority clauses. |

| “You cannot open this across state lines.” | If you live in one state but the estate is in another, a local branch might struggle to process out-of-state court documents. You often have to ask for a manager or a dedicated estate department. |

Operating the Account Safely After Opening

Once the account is finally open, the way you use it is just as important as how you opened it. The primary rule of estate administration is to never mix money.

Never deposit estate funds into your personal checking account, and never pay personal bills out of the estate account. Even a harmless mistake, like accidentally using the estate debit card to buy your own groceries, can trigger disputes from beneficiaries or look like fraud during an audit.

Make it a habit to log every single transaction that goes in and out of that account. Keep the receipts for every expense you pay, and save all monthly statements in a dedicated folder. This level of discipline ensures that when it is time to close the estate, your financial map is crystal clear. If you want to see how this ongoing tracking fits into the broader picture, review our comprehensive executor banking checklist to understand how different account types change your workflow.

The Step That Establishes Your Control

Opening an estate account is often your first major administrative hurdle, and it is completely normal if the process feels rigid. The friction at the banker’s desk is not a personal judgment on your capability; it is simply institutional risk management functioning as designed.

By treating this visit as a formal presentation of evidence rather than a casual errand, you set yourself up for success. Once that account is successfully funded and active, you transition from scrambling to gather information into a position of true administrative control. You finally have a secure hub to manage the estate’s obligations with total transparency.

❓ FAQ

⏳ How long does it take a bank to open an estate account?

If all documents are perfectly matched, it may be opened during your appointment. However, it is very common for banks to send the paperwork to a back-office legal department for review, which can take anywhere from 24 hours to over a week.

📝 Can I open an estate bank account with just a death certificate?

Usually, no. A death certificate only proves someone passed away; it does not prove you have the legal right to manage their money. You typically need court authority documents or a specific state affidavit as well.

💻 Should I use an online bank or a traditional bank for an estate account?

Many executors prefer traditional brick-and-mortar banks because you can sit down with a person to review complex court documents. While some online banks offer estate accounts, their document verification process is often slower and done entirely through uploaded scans.

🤝 What happens if there are two co-executors?

Most banks require both co-executors to be heavily involved. You will typically both need to present your IDs and sign the initial account signature cards, often at the exact same time inside the branch.

📄 What if the estate is too small for formal probate?

If the estate qualifies under your state’s limits, you may be able to use a Small Estate Affidavit instead of formal court letters. You must present the notarized affidavit to the bank alongside the death certificate and EIN.

✍️ Can I write checks immediately after opening the account?

Not always. When you make the initial deposit to fund the estate account, banks often place a standard hold on the funds (sometimes 5 to 7 days) to ensure the initial check clears before allowing you to pay out estate bills.

💳 Does an estate bank account come with a debit card?

Often, yes. Many banks will issue a debit card tied to the estate account to help you pay routine estate expenses. However, you should strictly use it only for legitimate estate bills, never for personal purchases.

💵 How much money do you need to open an estate account?

This varies by bank. Some institutions require no minimum deposit, while others may ask for $25 to $100 to initially fund the account. You can usually fund it with a check made payable to the estate.

📍 Do I have to open the estate account at the deceased person’s bank?

No, you are generally free to open the estate account at any bank you prefer, assuming you have the proper authority documents. Many executors choose a bank that is geographically convenient for them.

🛑 What happens if the bank refuses to open the estate account?

If refused, calmly ask for a written explanation of exactly what is missing or incorrect. Usually, the issue is a stale date on a court document or a mismatched name, which can be fixed by obtaining updated paperwork.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.