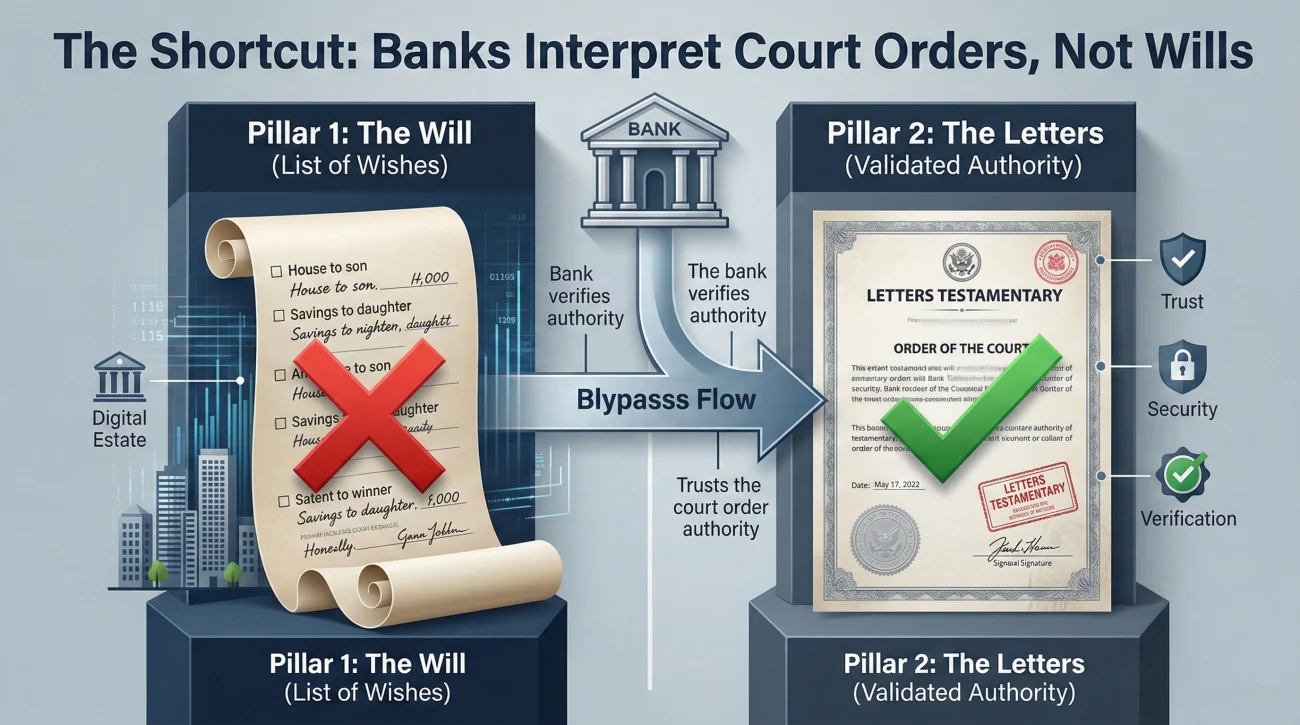

- The core purpose: Banks use your letters (testamentary or of administration) as a legal shortcut to verify you have the authority to access accounts and information, not just a will showing you were chosen.

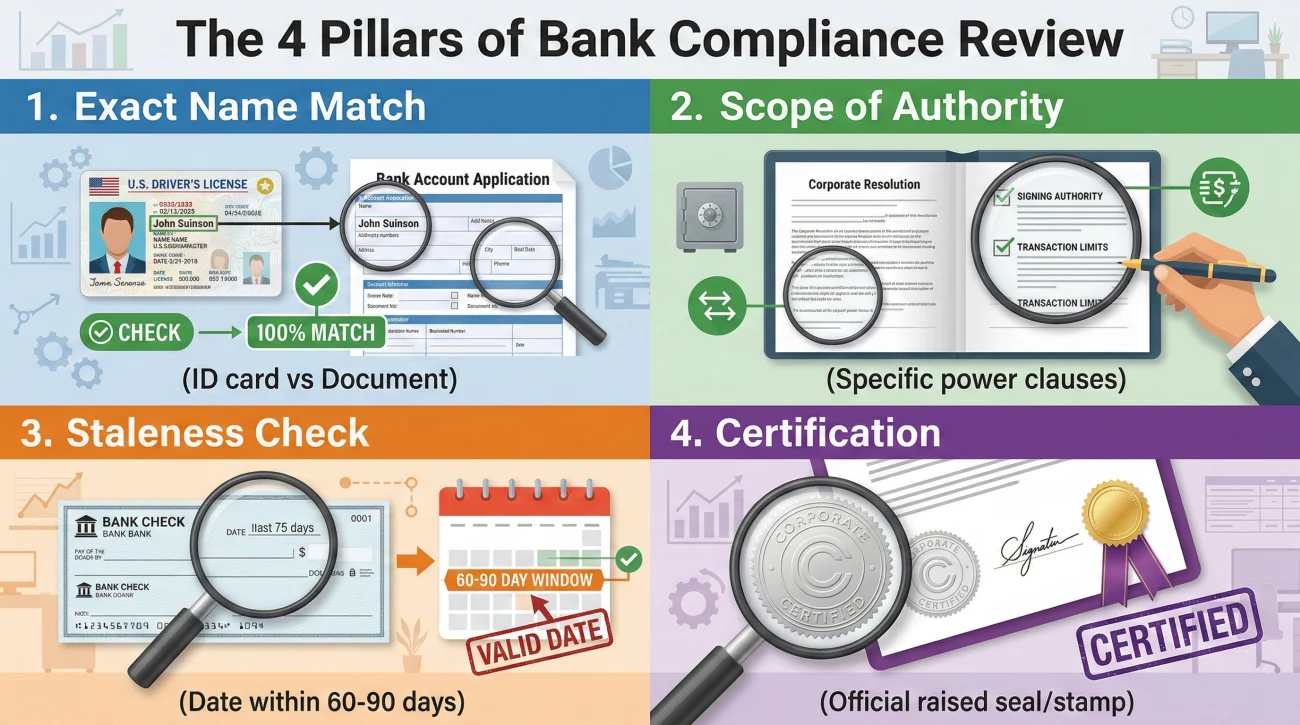

- What banks actually check: Back-office risk departments look for an exact name match, an official court seal (certification), the scope of your authority, and the issuance date to ensure the document is not stale.

- Account types matter: Letters typically unlock solely owned accounts. They rarely override the existing instructions on joint accounts or accounts with specific Payable on Death (POD) beneficiaries.

- The golden rule of submission: Always provide a physical certified copy if requested, get a written receipt that the bank accepted it, and keep a clean communication log of who you spoke with.

The “We Need Your Letters” Roadblock

If you are reading this, you have probably already walked into a bank branch, death certificate and will in hand, only to be politely but firmly turned away. The teller or branch manager likely told you that they cannot share account balances, stop automatic payments, or transfer funds until you bring them your “letters.”

In my daily work writing estate administration guides and helping executors build clean document packets, I review hundreds of communication logs where people hit this exact wall. It feels incredibly counterintuitive. You have a legally drafted will that clearly names you as the executor. You have the official death certificate. Why is the bank acting like you are a stranger?

The short answer is risk. The bank is not trying to be difficult. They are operating under strict federal and internal compliance rules. They cannot rely on a will because a will is just a list of wishes until a court validates it. To a bank, letters for bank access are the ultimate proof that the court has officially handed you the keys.

I want to walk you through exactly what happens when you hand those letters across the desk. We are going to look at what the bank’s back office is actually verifying, why they reject perfectly good documents, and how to keep the process moving when communication stalls.

💡 Boundary Note: This guide is strictly focused on the bank-facing side of the process. If you are still waiting on the court and do not actually have your document yet, you will want to step back and start with our full probate court checklist for executors to understand how the appointment phase works.

Why Banks Lean on Letters as a Verification Shortcut

To understand why the bank is so stubborn about this one document, it helps to look at the situation through the eyes of a branch manager. When an account holder passes away, the bank’s primary legal obligation is to freeze the assets and prevent unauthorized withdrawals. This protects the estate, the beneficiaries, and the bank itself from fraud liability.

Key Point: Banks do not interpret wills. They interpret court orders. Your letters are a direct order from a judge confirming your current authority.

When you present letters testamentary or letters of administration, the bank uses them as a massive verification shortcut. Instead of their legal department having to read a 20-page will, verify witnesses, and check for later amendments, the bank simply relies on the fact that the local court has already done that heavy lifting.

Bank staff are trained to look for specific “green lights” on this document. Once they see those markers, it shifts the liability off their shoulders and allows them to open the doors for you. But if any of those elements are missing, the process stops completely.

What Banks Typically Check on Your Letters

When your paperwork crosses the desk, it usually goes straight to a specialized back-office team (often called a bereavement, risk, or estate settlement department). This team does not know you, and they are not interested in the backstory. They are simply running down a compliance checklist.

Instead of a generic review, here is exactly what the risk department is scrutinizing on the page.

Exact Name Matches

The name of the deceased person on the letters must match the name on the bank account. If the bank account is held under “James Robert Smith” and the letters say “Jim Smith,” the back office will often flag this as a mismatch. They will also verify your identity against the document. The ID you present must perfectly match the executor name appointed by the court.

Scope of Authority

Not all letters grant the same power. Some documents provide broad, independent authority to close accounts and write checks. Others might be restricted, perhaps only allowing you to gather information but not move funds without another court order. The legal team will read the specific clauses to see exactly what you are allowed to do.

Currency, Expiration, and the “Staleness Rule”

Banks want to know that your authority is current. If a court appointed you three years ago, the bank has no way of knowing if you were subsequently removed from that role. Because of this, they look very closely at the date the document was issued or certified.

⚠️ Warning: Many banks enforce an internal “staleness rule,” meaning they will reject letters certified more than 60 to 90 days ago. If your document is older than their specific threshold, you will usually need to go back to the courthouse and purchase newly certified copies before the bank will talk to you.

The Certification Stamp or Seal

A plain photocopy is rarely enough to initiate major account changes. The bank wants to see that the court clerk has physically or digitally certified that this copy is a true and accurate reflection of the current court record.

Certified vs. Copy: Why the Bank Insists on Certification

I often see executors make a very logical mistake. They get one beautiful, official copy of their letters from the court. They go home, put it on their scanner, print out five copies, and drive to five different banks. Almost inevitably, they get rejected.

A home-printed copy proves that you had the document at the moment you scanned it. It does not prove that the document is still valid today, and it lacks the anti-fraud markers banks require.

When a bank asks for certified copies, they are asking for a document that the court itself has stamped, sealed, or watermarked. Often, this involves a raised seal that you can feel with your fingers, or an ink stamp on the back of the page with the clerk’s signature.

In many cases, the bank will ask to see the physical certified copy. They will make their own internal scan of it and then hand the physical original back to you.

💡 Pro Tip: Before leaving the teller window, always say: “Could you please confirm that you have scanned all pages, including the back of the page with the certification stamp, and return the original to me?”

Operational Roadblocks: Where Packets Usually Fail

Even with certified paperwork in hand, things do not always go smoothly. When an executor gets stuck in a loop with the back office, it usually comes down to a minor logistical mismatch rather than a legal dispute.

Here are three common friction points you should prepare for.

The Alias Issue

If the deceased person opened their bank account 40 years ago under a nickname, but their court paperwork uses their formal legal name, the bank’s system will hit a wall. In my experience, if the names do not align, do not try to force it or argue. Calmly ask the bank for their standard procedure for resolving name variations. They often have a specific internal affidavit they use for this exact scenario.

The Missing Page Pattern

Court letters are sometimes printed on legal-sized paper, or they span multiple pages. If the local teller scans the document and accidentally misses page two, the back office will reject the entire packet a week later. When you submit your documents, verbally confirm the page count. “I am handing you a three-page document, plus the certification page.”

Navigating Online-Only Banks (Neobanks)

If you are dealing with a neobank that has no physical branches, the process changes entirely. You cannot simply show a manager your raised seal. Often, these institutions will require you to mail the physical certified copy to their legal department, or they will provide a highly secure, specialized upload portal. Always ask for their exact intake procedure in writing before putting your only official copy in the mail.

How Letters Interact with Different Account Types

One of the most surprising things for a new executor to learn is that court letters do not magically unlock every single account. Your authority is heavily dictated by how the account was structured before the person passed away.

| Account Ownership Type | Do Letters Usually Provide Access? | What Typically Happens |

|---|---|---|

| Sole Ownership (Individual) | Yes | The account is usually frozen upon notification of death. Your letters are required to gain information, close the account, or transfer funds to an estate checking account. |

| Joint Account with Rights of Survivorship | Rarely | The surviving joint owner typically assumes full control immediately. Even with letters, the bank often will not let the executor interfere with the surviving owner’s access. |

| POD / TOD (Payable on Death) | No | The funds belong directly to the named beneficiary. The executor usually has no authority over these funds, and the bank will deal directly with the beneficiary. |

Understanding this distinction saves a massive amount of stress. If a bank refuses to give you statements for a joint account, they are not ignoring your letters; the letters simply do not apply to that specific bucket of money.

The Autopay and Direct Deposit Hazard

When you present your letters and the bank freezes a solely owned account, that freeze usually stops everything. Automatic bill payments (like utilities or mortgages) will bounce, and direct deposits (like pensions or social security) may be returned. You must be prepared to contact those external billing companies immediately once you initiate the freeze, as the bank will not do this for you.

Review Timelines, Denials, and How to Escalate

Let’s say your document is perfectly certified, freshly dated, and the names match exactly. You hand it over, the teller scans it, and then… nothing happens. The account is still restricted, and no one is calling you back.

This is the most common anxiety point. It helps to know that estate reviews are rarely instant. A typical review window for a major bank’s back office is anywhere from 3 to 10 business days. During this time, the file might be escalated to a senior legal review team if the estate involves significant funds or complex business accounts.

If you find yourself stuck in a prolonged holding pattern, do not rely on phone calls that leave no trail. Use a calm, process-oriented written approach to force an update.

Here is a polite, highly effective script you can use to gain clarity when a bank stalls your access:

Subject: Request for written requirements regarding account access – Estate of [Deceased Name]

Hello [Name or Department],

I am writing to follow up on the certified letters and death certificate I submitted on [Date] regarding the accounts for [Deceased Name].

I understand the file is currently under review with your risk department. To ensure I am not delaying the process on my end, could you please provide a written list of any additional documents, forms, or specific information your team requires from me to complete this review?

Please confirm receipt of this message and let me know the standard timeline for these reviews to be finalized. Thank you.

Best regards,

[Your Name]

Executor for the Estate of [Deceased Name]

How to escalate: If another 3 to 5 business days pass without a coherent reply, it is time to escalate. Call the specific branch manager you originally worked with. If they cannot resolve it, ask them for the direct phone number to the institution’s “estate settlement hotline” or “bereavement support team.” Most large banks have a dedicated phone line for executors, but they rarely advertise it on their main website.

The Bank-Facing Checklist: What to Bring Alongside Your Letters

Your letters are the anchor of your authority, but they rarely travel alone. If you want to reduce the chances of being sent home to find one more piece of paper, you need to bring a complete packet.

While every institution has its own quirks, a standard bank-facing packet usually includes:

- ✅ The original certified letters (dated recently).

- ✅ Multiple certified copies of the death certificate.

- ✅ Your personal, unexpired government-issued ID.

- ✅ The deceased person’s account numbers, debit cards, or recent statements (if you have them).

- ✅ The Estate EIN paperwork (if you are opening a new estate account).

In practice, most estates involve three to five different financial institutions. Do not try to memorize who needs what. Build one standard master packet and replicate it for every bank.

Walking into the branch with a messy folder, handing over a home-printed copy of the letters, and leaving without a receipt.

Bringing a neatly labeled packet with freshly certified documents, handing them to the manager, and asking for an email confirmation that the risk department has received the file.

Final Thoughts on Banking Authority

Navigating bank risk departments is often a test of patience, not a test of logic. When you understand that the back-office staff are simply checking boxes on a liability form, you can stop taking their rejections personally.

Treat every bank interaction as a formal business handover. Provide exactly what they ask for, confirm their receipt in writing, and keep a clean timeline of your communications. The executors who experience the least friction are not the ones who argue the loudest; they are the ones who present a clean, auditable paper trail that makes it easy for the bank to say yes.

❓ FAQ

🏦 Do I need letters to close a solely owned bank account?

In most cases, yes. Unless the estate qualifies for a small estate process based on local thresholds, banks typically require official court appointment documents to release funds from a solely owned account.

⛔ Why won’t the bank accept my letters?

Common reasons for rejection include the document being too old (stale), lacking a proper certification seal, having name mismatches, or not granting the specific authority required to move funds.

📅 How old can my letters be for the bank to accept them?

Many institutions have internal policies requiring the certification date on the document to be within the last 60 to 90 days. If yours are older, you may need to request newly certified copies from the court.

📂 Does the bank keep my original certified letters?

Typically, no. The bank should scan the certified document for their internal records and return the physical original back to you. Always ask for it back before you leave.

📱 Can I just email the bank a PDF of my letters?

Often, a PDF is not enough for the initial verification step. While some back offices may accept secure uploads, many local branches require you to present the physical document with the raised seal or ink stamp first.

⚖️ What if the bank says my letters do not give me enough authority?

If your appointment was limited or restricted by the judge, the bank cannot override that. You should ask the bank for a written explanation of what specific authority is missing, and you may need to consult the court to expand your powers.

⏳ How long does the bank take to review my letters?

Once submitted, the back-office risk or estate settlement team usually takes anywhere from 3 to 10 business days to complete their legal review and unlock the accounts, depending on the complexity of the estate.

📞 How do I get the back office to talk to me directly?

Often, you cannot. Estate settlement departments are usually internal and only communicate through the local branch. Ask the branch manager to act as your liaison and request all updates in writing.

💳 What happens to automatic bill payments when the account is frozen?

When the bank freezes the account after verifying death, all outgoing automatic payments (utilities, mortgages) will typically bounce. The bank will not notify the billers; as executor, you must contact them directly.

📋 What else does the bank need besides my letters?

Alongside the court document, banks typically require a certified death certificate, your valid government-issued ID, and sometimes an Estate EIN if you are opening a new estate checking account.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.