- A frozen account is a standard institutional security measure to protect the assets, not a penalty or an accusation against the family.

- The type of ownership (sole, joint, or POD beneficiary) dictates how quickly and by what method the funds can be unlocked.

- Timelines require patience: expect a 5 to 10 business day review period even after you submit the perfect packet of court documents.

- Never attempt to bypass a freeze using the deceased person’s old login credentials, as this often triggers a fraud investigation that locks the estate down for months.

Discovering a Locked Account: Why It Happens and How to Breathe Through It

In my experience, one of the most jarring moments for a newly named executor happens at the checkout counter or the computer screen. I once worked with an executor who discovered the freeze while trying to buy sandwiches for a post-funeral reception. The card was declined, the bank app locked her out, and she was left feeling like the institution was questioning her intentions or intentionally withholding family money.

Finding a bank account frozen after death often causes immediate panic. As someone who helps executors navigate the physical paperwork and communication loops of estate administration, I want to offer you a different perspective. A freeze is simply the bank’s automated brakes kicking in. It is a control mechanism, not a verdict.

When an institution learns of a passing, their primary directive shifts instantly from providing fast, frictionless service to pure risk management. They freeze the account to preserve the exact financial snapshot that existed on the date of death. This protects the funds from unauthorized access, identity theft, or well-meaning family members accidentally paying the wrong bills. Let us walk through what the bank is actually waiting for and how you can organize your requests to move forward with far less frustration.

The Security Mechanics: Why a Bank Froze the Deceased’s Account

It is helpful to understand how institutions operate behind the scenes. Many executors wonder how the bank found out about the passing so quickly, especially if the family has not officially notified anyone yet. The banking system is deeply interconnected with federal and state databases, and a freeze can be triggered through multiple standard channels.

Common Triggers That Alert the Institution

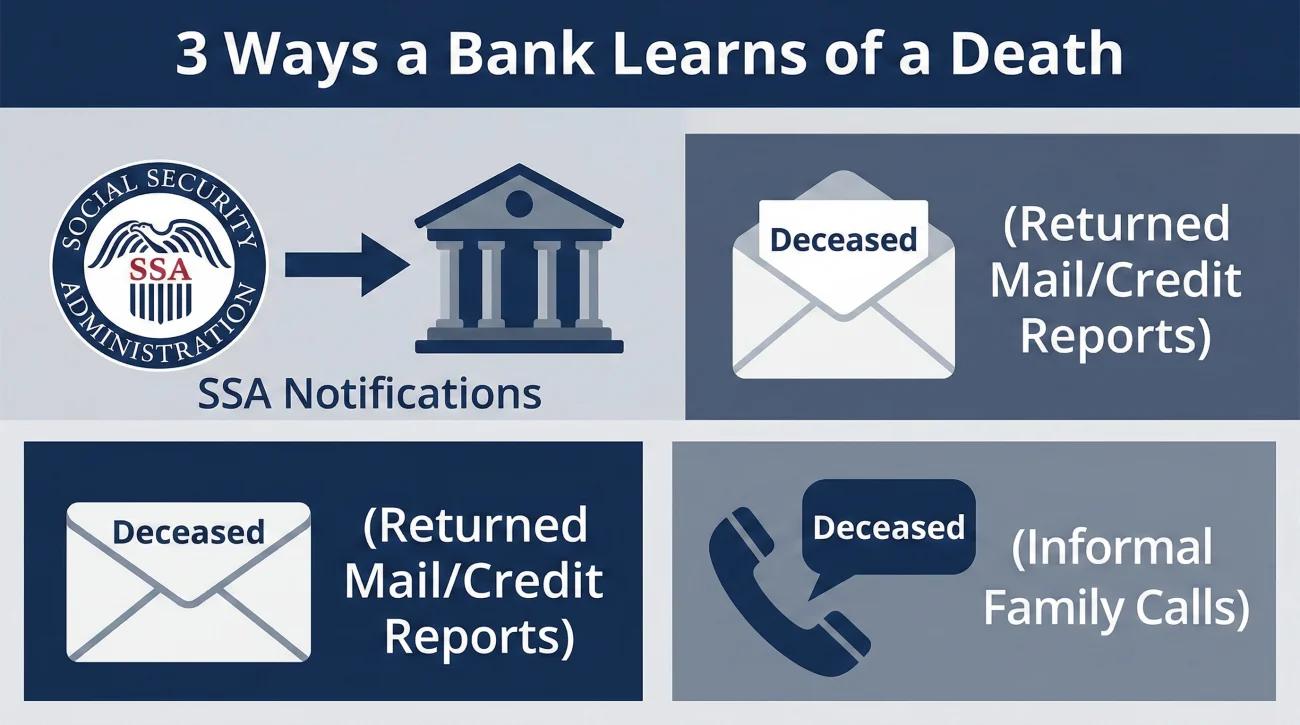

Banks do not rely solely on family members walking into a branch with a death certificate. In everyday practice, I often see accounts frozen automatically based on automated data feeds. Here are the most common ways an institution is alerted:

- ✅ Social Security Administration (SSA) Notifications: When a funeral home reports a death to the SSA, that information is pushed out to financial institutions. If the deceased was receiving direct deposits, the bank is often notified within days.

- ✅ Returned Mail or Credit Reporting: Activity on credit reports or mail returned by the postal service marked “deceased” can flag an account for review.

- ✅ Informal Family Calls: This is a pattern I see frequently. A relative might call the general customer service line just to ask a hypothetical question about the account. The moment the word “deceased” is recorded by the representative, protocol requires them to lock the profile.

💡 Pro Tip: If you are the executor, avoid calling the bank just to “chat” or explore options before you have your physical documents organized. A premature phone call will almost always result in an immediate freeze, cutting off access before you are fully prepared to handle the fallout.

The Shift From Speed to Risk Management

To understand why the bank acts the way it does, we have to look at their liability. Before a person passes away, the bank’s goal is customer convenience. After death, their goal is to avoid paying the wrong person, which could make the bank financially liable to the actual heirs or creditors.

The bank relies on passwords, PINs, and signatures to authorize fast transactions.

The bank relies entirely on certified paper documents, verified identity, and legal authority to authorize any movement of money.

Knowing this, your next step is determining exactly what kind of account you are dealing with, as that dictates how hard the freeze actually is.

How Ownership Structure Dictates the Freeze

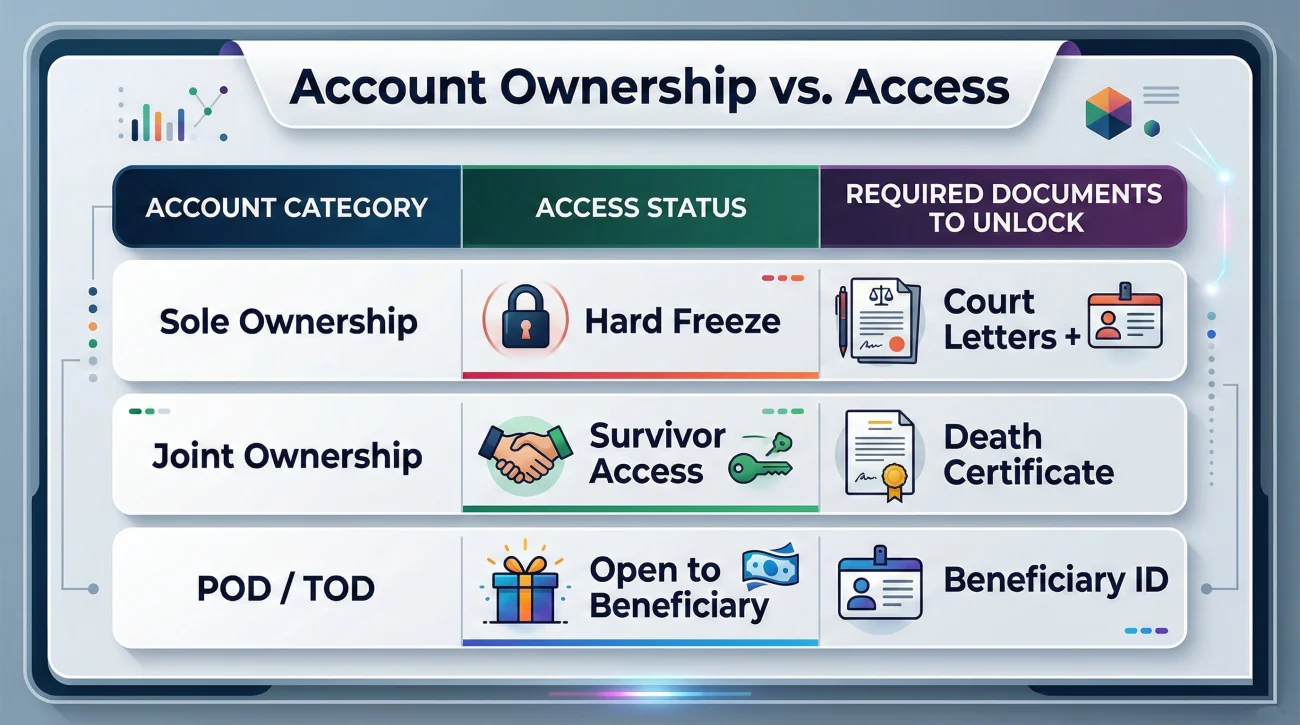

One of the most common misunderstandings in estate administration is the belief that all bank accounts are treated exactly the same way. In reality, the way the account was originally titled (who owned it and how) changes everything. A bank account frozen after death will require different unfreezing steps depending on its ownership category.

Solely Owned Accounts: The Hard Freeze

If the account was in the deceased person’s name only, with no joint owners and no named beneficiaries, it is considered a probate asset. This results in a hard freeze. The bank will not let anyone withdraw funds, write checks, or close the account until the court formally appoints an executor or administrator. Even if you hold the original will, the bank cannot act on it until a judge validates it.

Joint Accounts: The Continuous Access Exception

Joint accounts usually have a right of survivorship. In many cases, if one owner passes away, the surviving owner still has full access to the funds. The account may not experience a full freeze, but the bank will eventually require a certified death certificate to remove the deceased person’s name from the account. I often advise surviving spouses to verify with the institution whether a temporary hold will be placed while the name removal is processed.

Payable-on-Death (POD) Accounts: The Beneficiary Transition

If the account has a designated Payable-on-Death (POD) or Transfer-on-Death (TOD) beneficiary, the funds do not belong to the estate. The account is frozen to the general public and to the executor, but it unlocks directly for the named beneficiary. The beneficiary typically needs to present their own identification and a certified copy of the death certificate to claim the funds.

| Account Type | Immediate Status After Death | What Usually Unlocks It |

|---|---|---|

| Sole Ownership | Hard Freeze (No access) | Court-issued authority (Letters) + ID |

| Joint Ownership | Usually open for survivor | Death certificate to update account name |

| POD / TOD | Frozen to estate, open to beneficiary | Death certificate + Beneficiary ID |

Before you rush to the branch to solve this, you need to set up a system to track your progress. Unfreezing accounts is rarely a one-step process.

Recordkeeping: Building a Clear Trail From Day One

Dealing with a frozen account is almost never a single transaction. It is usually a process of submitting documents, waiting for review, answering questions, and waiting again. A common pattern I track in estate administration is the “missing document loop”, where a bank claims they never received a fax, or an agent tells you a file is incomplete weeks after you submitted it.

To protect your sanity, you must establish clear communication hygiene immediately. Treat your interactions with the bank as a formal project.

The Reference Number Rule

Every time you submit a packet of documents to unfreeze an account, or every time you speak to the estate department, you must log the interaction. Never hang up the phone without getting a reference number or an employee ID.

[Date of Action] + [Name/ID of Representative] + [Reference Number] + [Expected Turnaround Time]

If you mail physical documents, use certified mail with tracking. If you use a secure upload portal, take a screenshot of the confirmation screen. When you inevitably have to follow up, having this data completely changes the tone of the conversation.

📧 Email/Message Script: Following up on a submitted packet

Subject: Status Update Request – Estate of [Name] – Ref: [Number]

Hello,

I am following up on the document packet submitted on [Date] regarding the frozen account for [Name]. The submission reference number is [Number].

Please confirm that the documents have been received by the review team and advise if any additional information is needed at this time.

Thank you,

[Your Name]

With your tracking log ready, you can now focus on gathering the exact papers the bank wants to see.

The Paperwork and the Timeline Reality

When an executor is trying to figure out how to handle a frozen account, the conversation inevitably turns to paperwork. I constantly see people walk into a branch with a folder full of personal documents, only to be turned away because they lack the specific legal proof the bank’s compliance department requires.

It is important to understand that the bank teller you speak with does not have the power to bend the rules. They are following a strict checklist.

Why the Will Usually Is Not Enough

A frequent point of frustration for first-time executors is learning that holding the original Last Will and Testament does not automatically grant banking access. A will is essentially a list of wishes. It names who the deceased wanted to act as executor, but it does not prove that the document is the final, valid version, or that the probate court has actually granted you the power to act. Banks cannot legally interpret a will; they need a judge to do that for them.

The Documents Banks Actually Look For

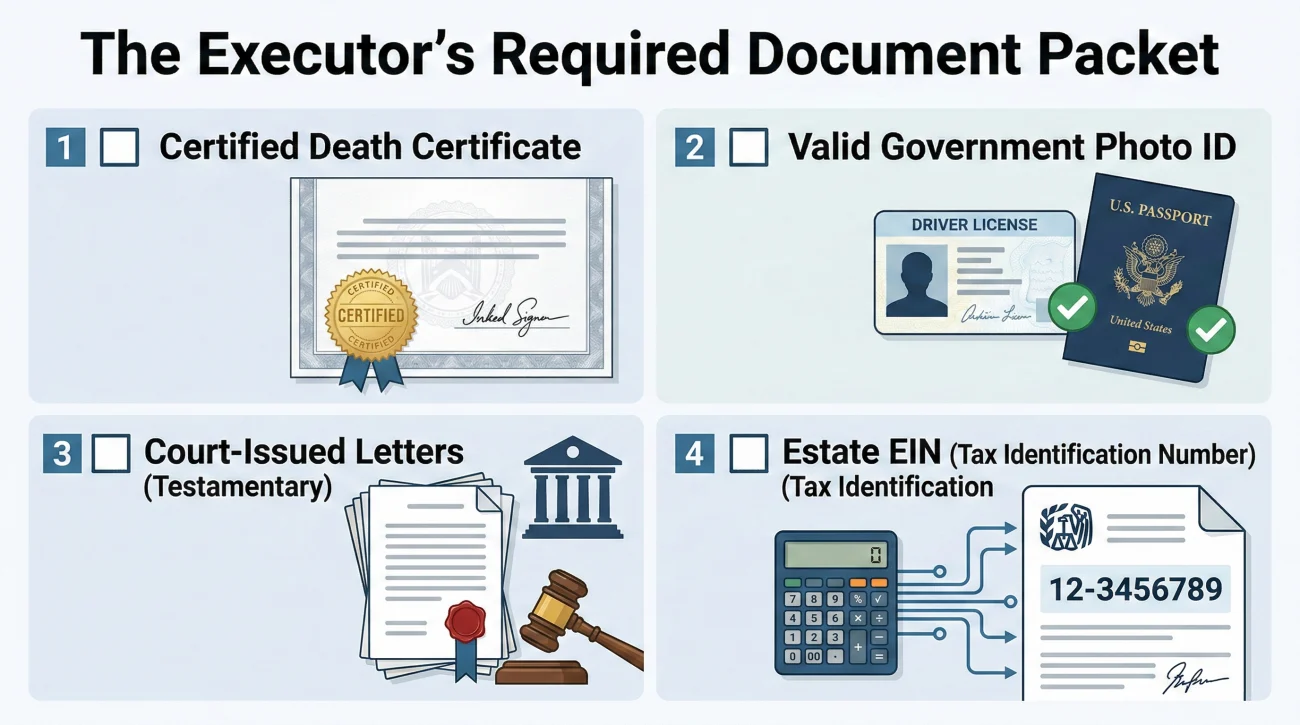

To lift a freeze on a solely owned account, banks typically require a combination of identity and authority verification. While every institution has slightly different packaging rules, the core requirements usually include:

- 📄 Certified Death Certificate: Proves the event of death.

- 📄 Proof of Identity: Your unexpired government-issued ID.

- 📄 Court-Issued Letters: Often called Letters Testamentary or Letters of Administration (these documents prove the court has officially appointed you to handle the estate).

- 📄 Tax Identification: In many cases, banks will eventually require an Estate EIN (Employer Identification Number) to transition the funds.

The Timeline Reality: What Takes the Longest

One of the biggest frustrations is assuming that handing over the right documents results in instant access. It rarely does. Once you submit your paperwork, the branch forwards it to a back-office legal team for review. In my experience, you should expect a review period of 5 to 10 business days before the bank acknowledges your authority and officially unlocks the funds. Knowing this timeline up front helps you manage expectations and avoid daily, stressful phone calls to the branch.

For a broader view of how to navigate these institutional requirements and map out your paperwork, I highly recommend reviewing our complete Executor Banking Checklist.

Internal Bank Disconnects: Why Different Departments Sound Inconsistent

One of the most common complaints I hear from people handling an estate is that the bank seems incredibly disorganized. You might call the 1-800 number and be told one thing, then walk into a local branch and be told something completely different. This inconsistency is normal, though highly frustrating.

The reason for this is structural. The front-line teller or the general phone support agent is trained to handle everyday consumer checking and savings tasks. They rarely handle deceased accounts. When an account is frozen, the authority to review documents and release funds is almost always shifted to a specialized back-office unit, often called the Estate Unit, Bereavement Department, or Deceased Accounts Team.

Key Point: Do not rely on verbal instructions from a general customer service representative regarding a frozen estate account. Always ask to be connected to the specialized estate department and request their requirements in writing.

How to Navigate Away From the General Hotline

When you are stuck in a communication loop, your goal is to bypass general support. I advise using a calm, direct script to request the correct department. You do not need to explain your entire situation to the first person who answers the phone.

Phone Script: Asking for the correct department

“Hello, I am calling regarding the account of [Name], who recently passed away. I need to speak with the Estate Processing Department or the Bereavement Unit to learn exactly what documents your institution requires to proceed. Can you please transfer me directly to that specific department?”

Operational Red Flags: What Not to Do While the Account is Locked

When bills are piling up and the bank is moving slowly, the pressure can feel immense. I have seen many executors try to find workarounds to keep things moving. Unfortunately, attempting to bypass a bank’s security controls often makes the situation much worse, leading to fraud investigations or personal liability.

The Danger of Using Old Passwords

If you have the deceased person’s usernames and passwords, it is highly tempting to log in and transfer funds or pay a few final bills before the bank officially finds out about the death. Do not do this. I once reviewed a case where an executor logged into the deceased’s portal three days after the date listed on the death certificate. The bank’s system flagged the login IP as suspicious, cross-referenced the newly reported date of death, and instantly triggered a fraud investigation. That single login attempt locked the family out of the account for an additional two months while the legal department investigated.

❌ Note: Using a deceased person’s credentials to access a bank account is generally considered a violation of the terms of service, and in many jurisdictions, it can be viewed as fraud.

Avoiding the Commingling Trap

Another common mistake is depositing checks made out to the deceased person into your own personal bank account, or paying estate bills directly from your personal checking account without rigorous tracking. This is called commingling. If you mix estate money with personal money, you lose the clean audit trail. You will eventually find that an estate bank account is needed to handle incoming funds safely.

While avoiding these traps keeps you out of legal trouble, it does not solve the immediate problem of bills piling up. Let us look at how to handle the cash flow safely while the bank holds the funds.

Managing Cash Flow When the Estate is Paralyzed

The single most stressful part of a frozen account is the cash flow gap. The estate has money, but you cannot touch it. Meanwhile, the funeral home wants to be paid, the mortgage on the deceased’s house is due, and the utilities are threatening a shut-off. How do you handle this without putting yourself at financial risk?

Step 1: Prioritize the Bills

Not all bills are equal after a death. You do not need to pay everything immediately out of pocket. In my operational work, I always recommend prioritizing expenses that preserve the estate’s value:

- ✅ Pay first: Secured debts (like a mortgage to prevent foreclosure), home insurance premiums, and essential utilities (to prevent burst pipes or property damage).

- ✅ Pause: Unsecured debts (like the deceased’s personal credit cards or medical bills). These can wait until the estate account is open and funded. Notify the creditors of the passing and instruct them to pause the accounts.

Step 2: Ask the Bank for a Direct Funeral Payment

Many institutions have a specific policy that allows certain critical bills to be paid directly from a frozen account, provided you submit the official invoice. The bank will not give you the money, but they may cut a cashier’s check directly to the funeral home. Always ask the bereavement department if this policy exists at their institution.

📧 Email Script: Requesting a direct payment

Subject: Written Requirements & Funeral Payment Policy – Estate of [Name]

Hello [Name of Representative/Department],

I am the named executor for the estate of [Name]. To ensure I provide exactly what your legal department needs to process this account, please reply with a complete, written list of required documents.

Additionally, please confirm your policy regarding the direct payment of funeral expenses from the currently frozen funds to the funeral home.

Thank you,

[Your Name]

Step 3: Creating a Bulletproof Reimbursement Log

If you must pay out of pocket to keep the lights on or secure a property, your primary defense is documentation. Do not use cash. The safest way to front expenses is to designate one of your own personal credit cards specifically for smaller estate expenses (like utilities or maintenance) and use a clearly tracked personal checking account for large ACH payments (like a mortgage) during the gap period.

This separation creates a clean, independent monthly statement. Save every receipt, note exactly what the expense was for, and log the date in a master spreadsheet. Later, when the estate is opened and the funds are unfrozen, you can present this log to reimburse yourself legally from the estate account without anyone accusing you of mishandling funds.

What to Do When the Bank Remains Unresponsive

Sometimes, despite doing everything right, you hit a wall. You submit the certified documents, you wait the required 10 days, and the account remains frozen with no update from the back office. If the bank is unresponsive, you need an escalation path.

Do not go back to the front-line teller. Your first escalation point is the local Branch Manager. Ask them to internally ping the Estate Department. If that fails, ask for the Estate Department Supervisor. If you are still stonewalled after several weeks, you have the right to file a formal complaint. In many cases, simply mentioning that you are prepared to file a complaint with the state banking regulator or the Consumer Financial Protection Bureau (CFPB) will suddenly expedite the legal review of your documents. Escaping this administrative gridlock is the final hurdle before you regain control.

Final Thoughts

Navigating a frozen bank account after death is undeniably stressful, but it helps to remember that it is a normal, temporary phase of the administration process. The freeze simply means the institution’s security protocols are working as intended to protect the assets until the proper legal authority is established.

By understanding what the bank is trying to verify, avoiding the temptation to bypass security controls, and maintaining a meticulous record of your communications, you can reduce the back-and-forth loops. Focus on gathering your certified court documents and communicating only with the specialized estate departments. Once the paperwork clears their compliance rules, the account will unlock. At that point, your typical next step will be to close the frozen account entirely and transfer the cleared funds into a newly established estate checking account, allowing you to finally begin paying creditors and settling the estate.

❓ FAQ

📱 What happens to auto-pay subscriptions (Netflix, gym) attached to a frozen account?

Once the account is officially frozen by the bank, all automated clearing house (ACH) pulls and debit card charges will bounce. You will need to contact the subscription services directly to inform them of the death and cancel the accounts to stop further billing attempts.

💳 Can I use my own credit card to pay estate bills and get paid back?

Yes. Many executors use a personal credit card to cover urgent estate expenses (like utilities or property maintenance) while the bank account is frozen. Keep rigorous receipts and logs so you can properly reimburse yourself from the estate account once it is opened.

🏦 Do credit unions handle frozen deceased accounts differently than big national banks?

While the legal requirements are similar, credit unions are often faster and more communicative. Because they are smaller, you can frequently speak directly to the person reviewing your documents, whereas large national banks rely on rigid, disconnected back-office processing centers.

⏱️ Is there a maximum legal time limit a bank can keep an account frozen?

There is no universal federal time limit. An account remains frozen until the bank receives the exact legal documentation required by their compliance department and state law. If you provide the correct documents and they still delay for months, you may need to escalate to a banking regulator.

📉 Will the bank still charge monthly maintenance fees while the account is frozen?

In most cases, yes. Unless the bank has a specific policy to waive them, standard monthly service fees will continue to be deducted from the frozen balance. You can formally request the estate department to waive these fees during the lock period, but it is granted at their discretion.

📈 Will the frozen account still earn interest while I wait for court documents?

Yes. If the frozen account is an interest-bearing account (like a savings account or CD), it will generally continue to accrue interest at its standard rate during the freeze until the account is formally closed and distributed.

💸 Are outstanding checks written before death going to clear or bounce?

In many states, banks are legally permitted to honor checks written by the deceased for a short period (often up to 10 days) after the date of death, provided the bank has not been ordered to stop payment. After that window, outstanding checks will typically bounce.

🏠 How do I stop auto-drafted mortgage payments from failing during the freeze?

You cannot unfreeze the account just for the mortgage. You must call the mortgage servicer immediately, notify them of the passing, and arrange an alternative payment method (often using your tracked personal funds) to prevent the home from going into default.

🏧 Can the bank legally freeze a joint account if I am the surviving spouse?

Generally, joint accounts with rights of survivorship should remain accessible to the surviving owner. If the bank places a hard freeze on a true joint account, it is often an administrative error. Contact the branch manager to clarify your survivor rights immediately.

✉️ Do I need to physically mail original death certificates, or will they take a scan?

Most banks require you to either present the physical, certified copy of the death certificate in person at a branch or mail a physical certified copy to their estate department. Scans or photocopies are rarely accepted for the initial unfreezing process.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.