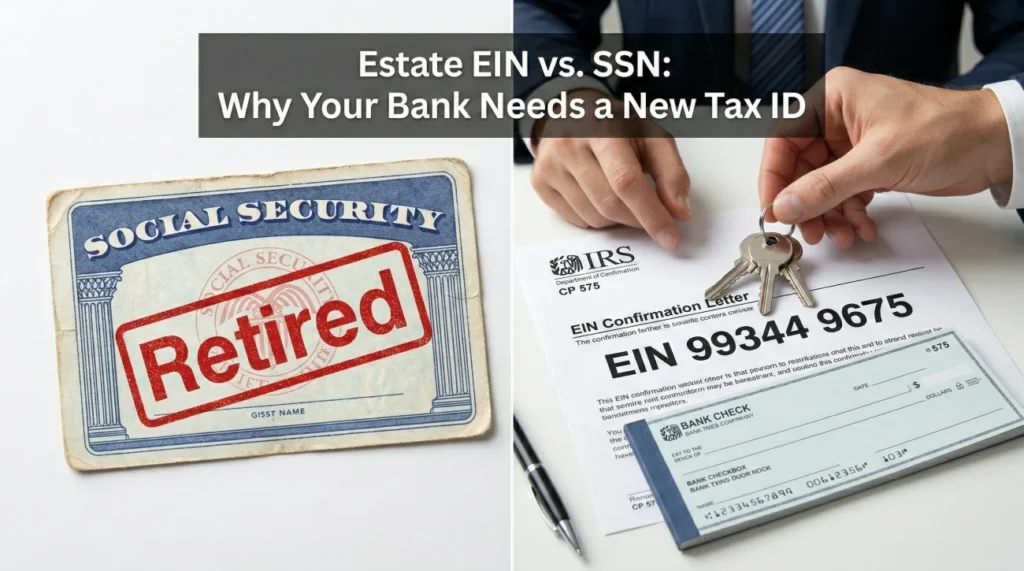

- The bank asks for an EIN because a deceased person’s Social Security Number (SSN) can no longer be used to report new financial activity.

- You only need one EIN for the entire estate. This single number will be used across all banks, brokerages, and title companies you deal with.

- If you are settling a very small estate using a state-specific Small Estate Affidavit, you may not need an EIN at all.

- Never use your own personal SSN to open an estate account, as this merges the estate’s tax liabilities with your personal finances.

The Sudden Tax ID Roadblock

Last month, I was on a conference call with an executor and a brokerage firm. The executor had the death certificate and the court appointment letters in hand. She was fully prepared to move the funds. But when she asked to liquidate the account, the broker stopped her and asked for the estate EIN. She had not applied for one because she assumed her mother’s SSN was sufficient.

If you are experiencing a similar roadblock, it can feel incredibly frustrating. You might wonder why the bank is suddenly treating a family situation like a corporate entity. Understanding the difference between an estate EIN vs SSN is one of the most important conceptual shifts you will make in this role.

The bank is not trying to make things difficult. They are simply following strict reporting rules. The moment a person passes away, their financial identity changes in the eyes of the banking system. Your job is to provide the paperwork that matches that new identity.

The Line in the Sand: Why the SSN Stops Working

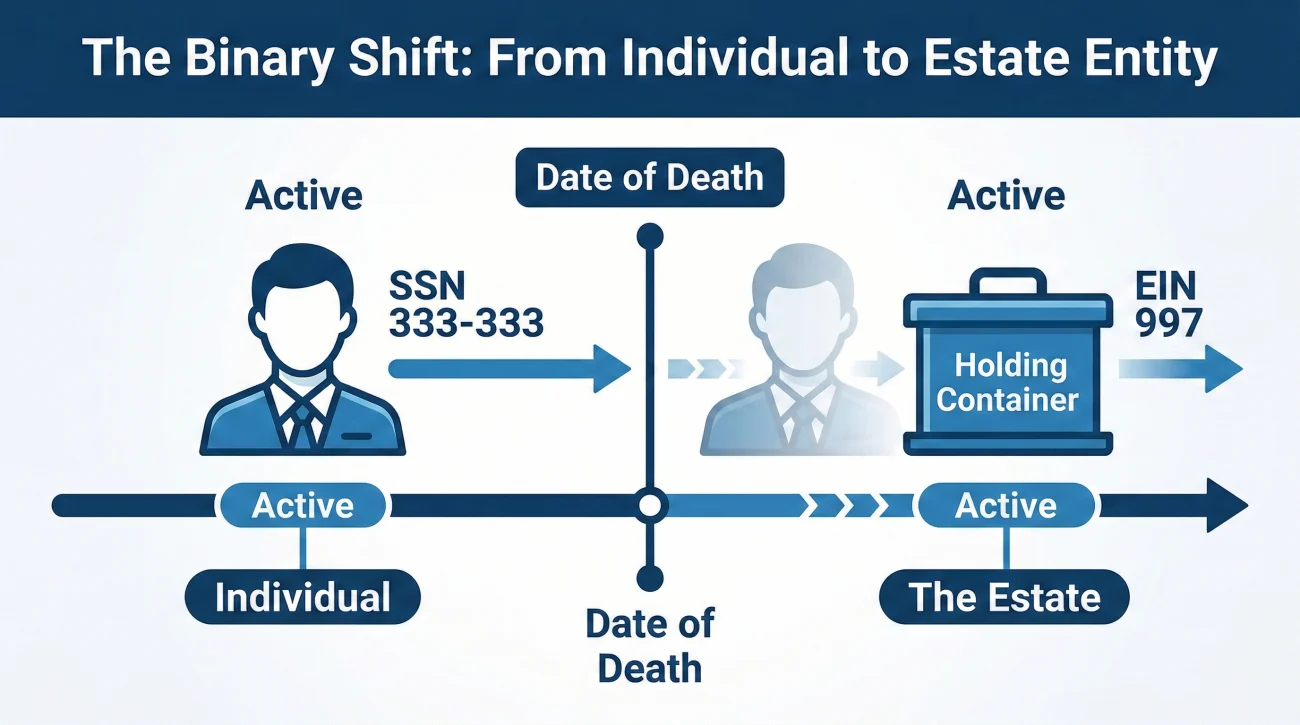

Every bank account must be tied to a taxpayer identification number. For most of our lives, that number is our SSN. However, an SSN is tied strictly to a living individual. When someone passes away, federal agencies lock that SSN down to prevent identity theft. From an administrative standpoint, the individual can no longer earn income, open new accounts, or report new tax events.

But the assets they left behind still exist. Those assets might still generate interest, receive refunds, or need to be moved.

Key Point: Think of the “estate” as a temporary, invisible holding container that springs into existence the moment someone passes away. Because this container holds money and assets, it needs its own identification number.

Banking systems are binary. Once the system registers a date of death, the SSN is retired for new business. The bank reports all new financial activity to the “Estate of” the individual, using the newly assigned Employer Identification Number (EIN).

Clarifying the “Employer” and “Trust” Confusion

One of the biggest sources of confusion is the name itself. The government uses the term “Employer Identification Number” for almost all entities that are not living individuals. When an executor needs an EIN, it does not mean they are suddenly responsible for payroll or corporate taxes. It is simply a nine-digit tracking number assigned to the estate.

💡 Pro Tip: In the context of estate administration, you can mentally replace “Employer Identification Number” with “Estate Identification Number.” The bank understands exactly what it is for.

The “Employer” label is not the only naming trap. A second major hurdle catches executors who are also dealing with a living trust.

Estate EIN vs Living Trust EIN

I recently worked with a family where the father had a Living Trust (which had its own EIN) and a few leftover assets in his personal name that required probate.

The executor tried to use the Trust’s EIN to open the probate estate bank account. The bank rejected it. If the deceased had both a trust and a probate estate, these are two separate invisible containers. They each need their own unique ID number. You cannot mix them.

When You Actually Need One (and When You Don’t)

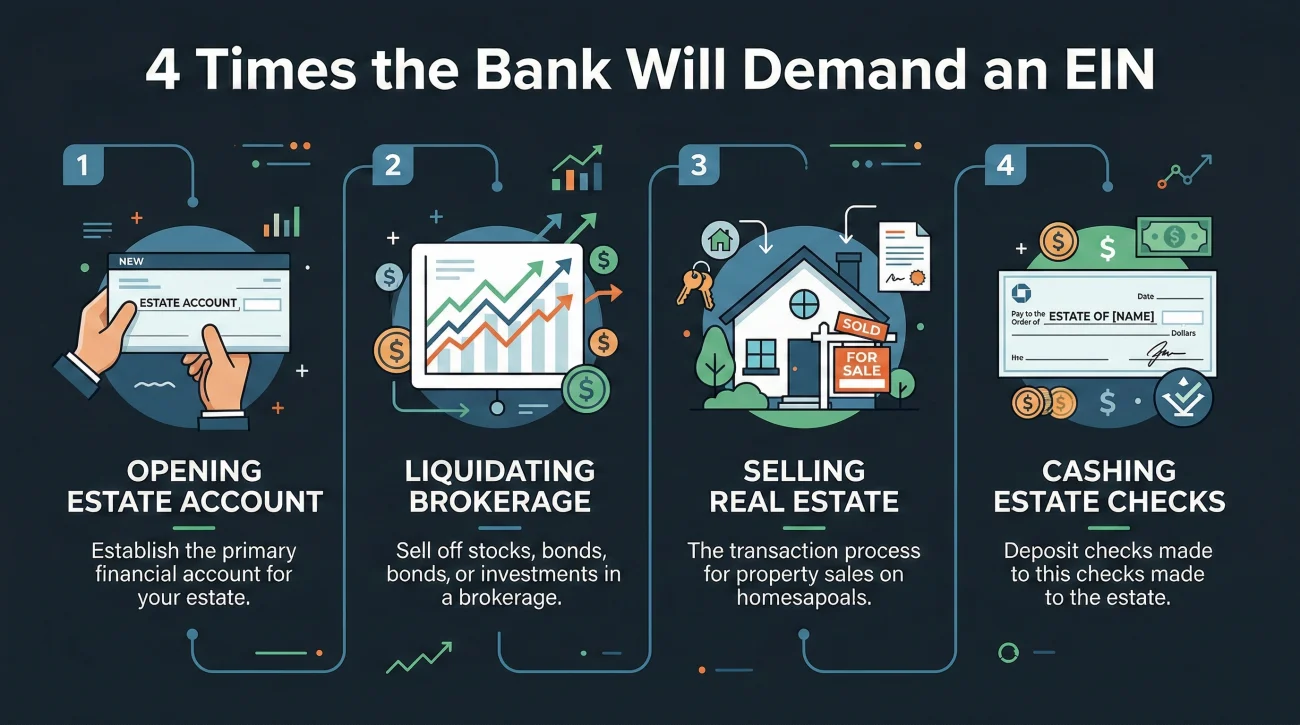

You might not need an EIN on day one. You will usually submit a form to move an asset, and the response will be a request for the tax ID. Here are the most common scenarios where the SSN is rejected and the EIN is required:

| The Executor Action | Why the Bank Asks for an EIN |

|---|---|

| Opening an Estate Checking Account | The new account belongs to the estate entity, not the deceased. |

| Cashing a check made to “Estate of” | A check written to the estate cannot be deposited into an account bearing an individual’s SSN. |

| Liquidating brokerage accounts | Selling stocks often generates capital gains or losses, which must be reported under the estate’s tax ID. |

| Selling real estate | Title companies require an EIN to report the proceeds of the property sale. |

The Small Estate Exception

Before you rush to apply for an EIN, confirm your authority path. If you are settling a very small estate using a state-specific Small Estate Affidavit, you are generally bypassing formal probate. In many of these cases, you do not need an EIN at all. The bank often allows you to collect the funds using your own SSN because the money is passing directly to you as the affiant, rather than flowing through a formal estate container.

How the EIN Connects to an Estate Bank Account

The most frequent reason executors run into this requirement is when they attempt to open an account to hold estate funds. Establishing an EIN for estate checking is a non-negotiable step for almost every major financial institution.

When you walk into a branch, the bank is essentially building a new customer profile. They need the legal name of the entity, the authorized signer (you, proven by your court letters), and the entity’s identification number. Without the EIN, the bank’s software physically will not allow the representative to proceed to the next screen.

If you are preparing for this step, I highly recommend reviewing the broader Executor Banking Checklist to understand how this tax ID fits into the larger picture of securing assets.

Asking the Bank About Their Sequence

Because every bank has a slightly different workflow, it is wise to clarify their exact sequence before you schedule a long appointment. Here is a safe, polite way to ask:

Subject: Requirements for opening an estate account

Hello [Bank Representative],

I am preparing the paperwork to open the estate checking account. Before we finalize an appointment time, could you please confirm in writing if the bank requires me to have the physical EIN confirmation letter from the IRS present at the initial meeting, or if the court appointment documents are sufficient to begin the process?

Thank you,

[Your Name]

Filling Out the W-9 Form for an Estate

Here is a situation I see constantly: An executor successfully obtains the EIN. They call the bank’s bereavement department and say they have the tax number. The bank replies, “Great, please fill out a W-9 estate form and send it back to us.”

The executor freezes because a W-9 is usually associated with freelance work. But in the banking world, a W-9 is simply a standardized delivery vehicle. Banks cannot just take your word for it over the phone. They need a formal, signed document where you certify the tax identification number is correct.

When you fill out a W-9 for an estate, you are not putting your personal tax profile on the line. Here is exactly how this usually looks in practice:

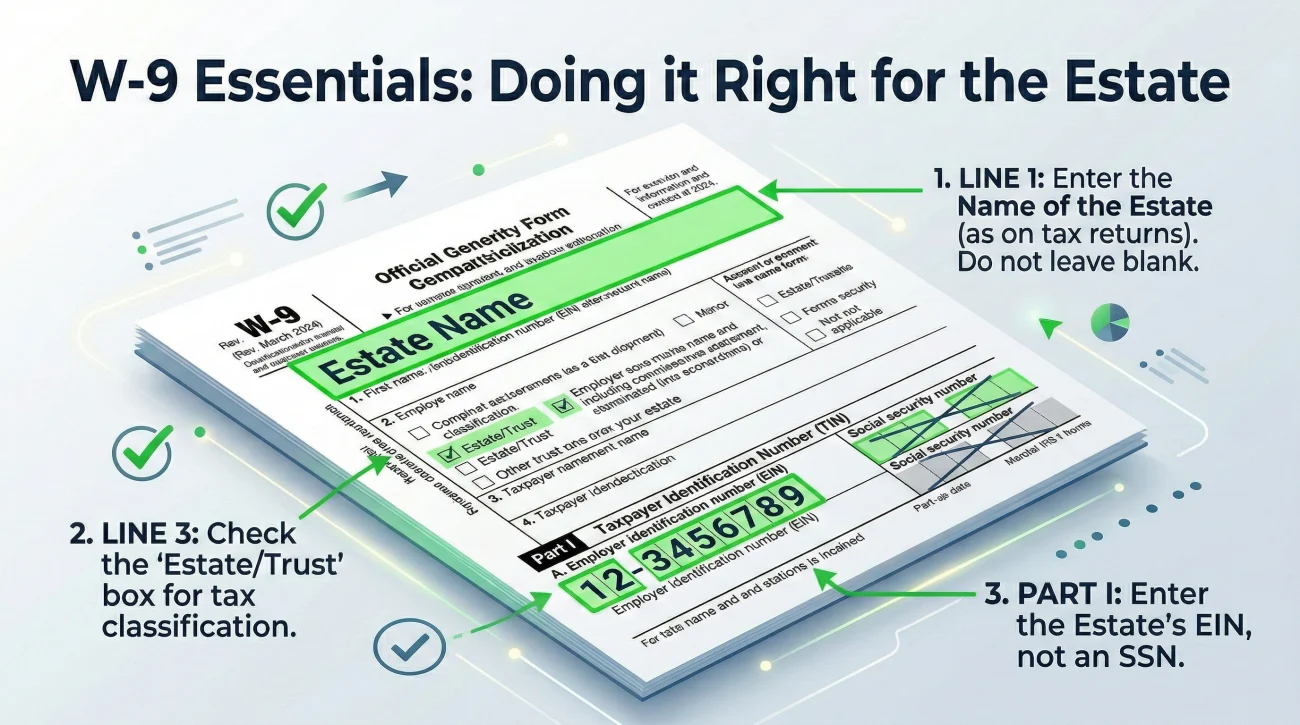

- ✅ Line 1 (Name): You write the exact legal name of the estate as it appears on your court documents (e.g., Estate of John Doe).

- ✅ Line 2 (Business name): You generally leave this blank.

- ✅ Line 3 (Tax Classification): You check the box specifically designated for “Estate or Trust.”

- ✅ Part I (TIN): You enter the 9-digit EIN you received from the IRS. Do not enter the deceased’s SSN here.

Filling out the W-9 correctly is only half the battle. Even with the right form, a small inconsistency in how you present your information can cause the bank’s compliance department to reject it. Let’s look at the most frequent paperwork stalls.

Common Misunderstandings That Cause Paperwork Delays

In administrative work, precision is everything. Here are the traps executors fall into when dealing with tax IDs.

The Personal SSN Trap

The most dangerous mistake is giving the bank your own personal Social Security Number when opening the estate account. Sometimes a well-meaning teller will suggest it just to get the account open quickly.

⚠️ Warning: Never use your personal SSN for an estate bank account. If you do, any interest earned on that account may be reported to the IRS under your personal name. This creates a massive headache during tax season and blurs the line between estate funds and your own money.

The Name Mismatch Loop

Banks are incredibly strict about name matching. I once saw an account opening delayed by three weeks simply because the EIN paperwork omitted a “Jr.” suffix that was present on the court documents. When you apply for the EIN, ensure that the name of the estate is typed exactly the same way it appears on your court appointment papers.

Recordkeeping: Building Your Identity Packet

Because the tax ID for estate account setup is so critical, a scattered approach to saving these files guarantees frustration. You will be asked for this number multiple times by different institutions. You only need to apply for one EIN, but you need to share it efficiently.

Instead of maintaining a dozen separate folders, the most effective executors I work with build a single “Identity Packet.” This packet contains the court-issued Letters, the death certificate, and the official IRS CP-575 EIN confirmation letter merged into a single PDF or permanently stapled together in a physical file.

Banks almost never ask for the EIN in isolation. They need to verify your authority alongside it. By pairing these documents permanently, you prevent yourself from sending incomplete files. When a title company or a second bank asks for your tax ID, you do not need to hunt for the IRS letter or worry if you attached the right things. You simply send the complete Identity Packet. This small habit drastically reduces back-and-forth emails.

Final Thoughts on the Tax ID Transition

Securing and managing the estate’s tax ID is your first real act of boundary-setting as an executor. By keeping the estate’s tax identity strictly separated from your own, and treating the official IRS confirmation letter as a core piece of your authority packet, you protect yourself from messy tax entanglements down the line. Verify exactly how the bank wants to receive the new number, refuse to use your personal SSN, and handle the paperwork step by step.

❓ FAQ

💳 How do I apply for an estate EIN?

The fastest way is to apply directly on the official IRS website. The online application is free, and in most cases, it generates the EIN immediately upon completion so you can download the confirmation letter right away.

🏦 Can I just keep using the SSN if the account is already open?

Usually, no. Once a bank is notified of a death, they will generally freeze or restrict the account. To move the funds or establish a functional account for estate use, they require the new estate EIN.

⏳ How long does it take for the bank to verify an estate EIN?

If you have the official confirmation letter, the bank can usually update their system during your appointment. However, it can sometimes take a couple of weeks for a newly issued EIN to register in all external banking verification databases.

📄 What if I lose the EIN confirmation letter?

If you lose the letter, you can contact the IRS directly to request a replacement confirmation letter. The bank will likely pause any account openings until you have the official replacement document in hand.

📉 Does getting an EIN mean I have to file extra tax returns?

Having an EIN often means an estate tax return (Form 1041) may need to be filed if the estate generates income. However, obtaining the number itself is simply a banking and administrative requirement. You should consult a tax professional regarding actual filing duties.

🏛️ Can the bank apply for the estate EIN for me?

No, the bank cannot generate an EIN for you. The appointed executor, administrator, or their hired professional (like an attorney or CPA) must request the EIN from the IRS.

🏠 Why is the mortgage company asking for an EIN?

If the estate is selling real property, the title company’s reporting of the sale proceeds must be tied to the estate’s tax ID, not the deceased individual’s SSN.

🔒 What happens to the EIN when the estate is closed?

The EIN is never truly deleted or reused by the IRS, but once the final estate tax returns are filed and the estate is officially closed, the number simply becomes dormant and inactive.

🔍 Is a tax ID for an estate account the same thing as an EIN?

Yes. In the context of estate administration, when a bank asks for the estate’s Tax ID, Taxpayer Identification Number (TIN), or EIN, they are all referring to the same nine-digit number assigned by the IRS.

🤝 Do joint accounts need an estate EIN?

Typically, no. If an account is jointly owned with rights of survivorship, the surviving owner usually assumes full ownership, and the account reporting shifts entirely to the surviving owner’s personal SSN.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.