- A check payable to “Estate of” belongs to a distinct legal entity, not the deceased person and not you personally.

- Personal accounts and joint accounts will reject these checks because the payee names do not match the account holder perfectly.

- To process these funds, you typically need to establish a dedicated estate bank account to act as the central landing pad.

- Banks require a specific document packet, usually including court-issued letters, to prove your authority before accepting the deposit.

- Always ask the specific bank for their required endorsement format in writing before signing the back of any check.

The Payee Line Changes The Entire Process

You open the mail and find an unexpected envelope. Maybe it is a refund from the utility company, an insurance premium return, or a final paycheck. You look at the payee line, and instead of the deceased person’s normal name, it reads “Estate of [Name].” If you are like many people stepping into this role for the first time, your initial thought might be to just sign the back and deposit it into your own account to help cover upcoming expenses. Then, the mobile deposit bounces, or the bank teller politely but firmly slides the check back across the counter and says they cannot accept it.

In my experience tracking administrative workflows and helping people organize their paperwork, trying to deposit an estate check is one of the most common early friction points. It catches people off guard because the amount might be very small, yet the banking system treats it with the exact same rigidity as a massive settlement. The reason for this strictness comes down to how financial institutions view those two words: “Estate of.”

Once a person passes away, their individual financial identity essentially stops. A new, temporary legal entity takes its place, which is the estate. The bank does not know who the rightful heirs are, what the will says, or if creditors need to be paid first. All the bank sees is that the check belongs to a separate entity. Because personal accounts and joint accounts are owned by living individuals, depositing an estate check into them creates an immediate name mismatch that banking software is programmed to reject.

Understanding this shift in perspective is the first step to reducing your frustration. You are no longer dealing with personal banking logic; you are dealing with fiduciary banking logic. In this guide, I will walk you through why banks treat these checks differently, what it actually takes to get them deposited, and how a clear workflow prevents repeat trips to the branch.

Why Banks Treat These Checks With Extreme Caution

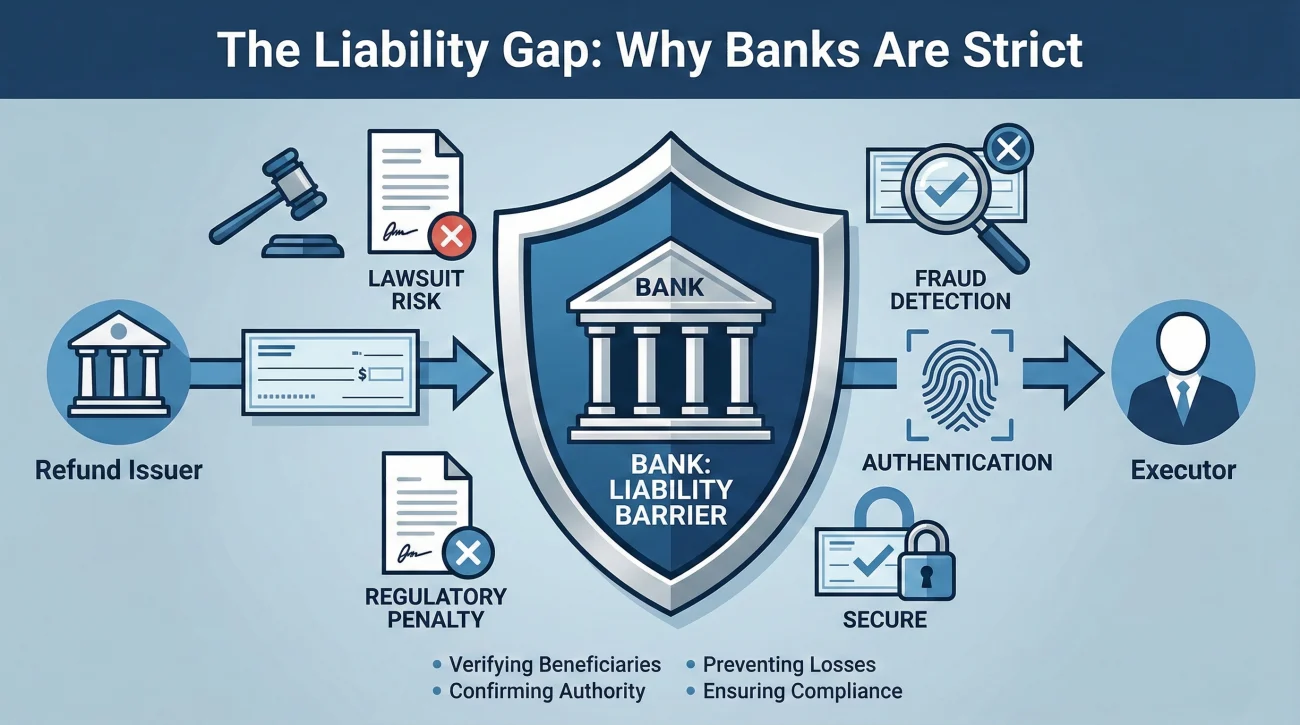

To navigate this hurdle smoothly, it helps to understand what is happening behind the teller counter. When you present an estate check, the bank is looking at a massive liability risk. If they allow you to deposit that money into an unverified account, and it turns out someone else was actually supposed to inherit those funds, the bank can be held legally responsible for the misdirected money.

The check issuer wrote “Estate of” specifically to wash their hands of the responsibility of figuring out who gets the money. By doing so, they passed that responsibility onto the estate’s representative and the bank that accepts the deposit. Think of this as a liability gap. The bank closes that gap by demanding absolute proof that you are the authorized person and that the money is going into an audited space.

This strictness is a protective measure. While it feels like a roadblock when you are just trying to deposit a fifty-dollar refund, the exact same system prevents an estranged relative from cashing a fifty-thousand-dollar asset check that belongs to the rightful beneficiaries. The tellers are trained to stop these transactions at the front line until the back office has verified your paper trail.

The Estate Account is the Required Landing Pad

Because you cannot force these funds into a personal or joint account, the money needs a dedicated landing pad. Conceptually and practically, this is where an estate checking account comes into the picture. It acts as the central hub for gathering the deceased person’s assets and paying their final bills in a transparent way.

⚠️ Warning: Avoid the temptation to take cash if a teller mistakenly offers it. Walking away with cash breaks the auditable timeline and creates a high risk of commingling funds, which can lead to disputes with beneficiaries or the court later on.

Setting up this account is not just a matter of walking up to a window with a check. It requires a formal onboarding process. You are asking the bank to recognize a brand new entity. To do this, you typically must present a specific packet of documents, sign new signature cards in your capacity as the fiduciary, and make an initial deposit. Once the bank’s compliance team approves the account (a review process that can take anywhere from a few days to a few weeks depending on the institution’s backlog), the system recognizes you as the authorized signer for the “Estate of” entity.

From that moment on, processing an estate check shifts from being an exception to a standard transaction. If you have not yet set up this hub, holding onto the check in a secure folder is almost always the safest move. Forcing a deposit prematurely usually creates administrative messes that take weeks to unravel.

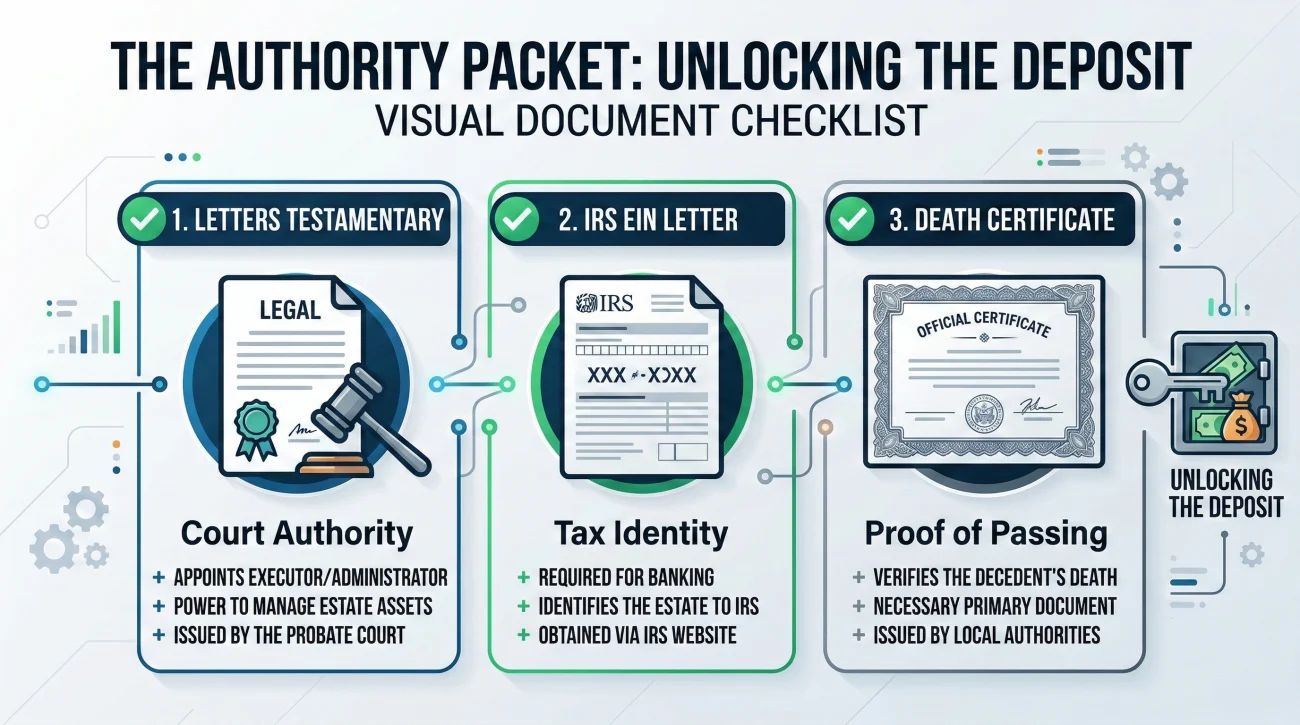

The Documents That Unlock the Process

To open that estate account and successfully deposit the check, you have to prove your legal right to touch the assets. A will is almost never enough on its own. A will simply states wishes; a bank needs proof of authorized reality.

The core document for proving this authority is usually the court-issued appointment, often called letters testamentary or letters of administration. This piece of paper proves that a judge has officially authorized you to act. In addition to this, the bank will almost always ask for an Employer Identification Number (EIN) for the estate. Because the estate is a new entity, it cannot use the deceased person’s Social Security Number for new financial accounts. The bank uses the EIN to report the new account to the IRS.

Small Estate Alternatives

There is a common scenario where going through full probate for a single small check seems unreasonable. In many jurisdictions, if the total value of the estate is under a certain dollar threshold, you might be able to use a Small Estate Affidavit instead of formal court letters. This affidavit serves as a streamlined proof of authority. However, not all banks understand or easily process these affidavits at the local branch level, so you must confirm their specific policy beforehand.

Getting these documents right the first time is crucial because it transforms you from a stranger holding a check into a legally recognized fiduciary in the bank’s eyes. To ensure you walk in with the right items in the right format, I highly recommend reviewing our core executor banking checklist. Once you provide this complete packet and the bank scans it into their system, your profile becomes active and ready to receive funds.

What Can Vary by Bank Policy

One of the most frustrating aspects of this process is hearing conflicting advice. A friend might tell you exactly how they deposited an estate check last year, only for your bank to reject that exact same method today. While the core rules of banking liability are universal, the internal risk tolerance varies wildly from one institution to the next.

Check Size Triggers: The dollar amount changes the scrutiny. A $40 utility refund check might be accepted for deposit into a surviving spouse’s joint account with just a death certificate and an internal indemnity form at a very forgiving community branch. However, a $15,000 home insurance claim check will almost universally trigger a hard stop, requiring full court letters and a formal estate account without exception.

Bank Relationships: Where you do business matters. If you are dealing with a local credit union manager who knew the deceased for thirty years, they might have the administrative override power to guide you through a simplified process. Conversely, a teller at a massive national bank branch has zero override power and must follow the screen prompts rigidly.

Endorsement Phrasing: The exact wording required on the back of the check is entirely up to the receiving bank’s compliance department. Some want simply “Estate of [Name].” Others want your signature followed by the word “Executor.” Guessing this phrasing is a major source of delays.

Handling Name Mismatches and Stale Checks

Even if you have the account open and the court letters in hand, the check itself can still cause problems. In my routine reviews of stalled files, a surprisingly high percentage of delays stem from two specific physical issues with the paper check.

The Name Mismatch

What happens when the issuer writes “Estate of Bob Smith” but your legal court documents say “Estate of Robert James Smith”? Banks look for perfect matches. Some strict banks will pause the transaction over a missing middle initial. If the bank refuses the check due to a naming discrepancy, you usually have to contact the company that issued the check, explain the legal name mismatch, send them a copy of your authority document, and ask them to reissue a new check with the exact legal phrasing. You can control your internal paperwork, so always ensure your EIN application and account setup perfectly match your court letters.

The Stale Check Problem

It can take months to receive court authority. Meanwhile, that refund check has been sitting in your folder. Standard checks typically become “stale” or void after 90 to 180 days. If you finally get your estate account open in month seven, the bank’s system might automatically reject the old check. If you notice a check is approaching its expiration date before you have the power to deposit it, contact the issuer early. Let them know the estate is in progress and ask about their policy for reissuing expired checks. This proactive step saves a lot of panic later.

The Safe Start-to-Finish Workflow

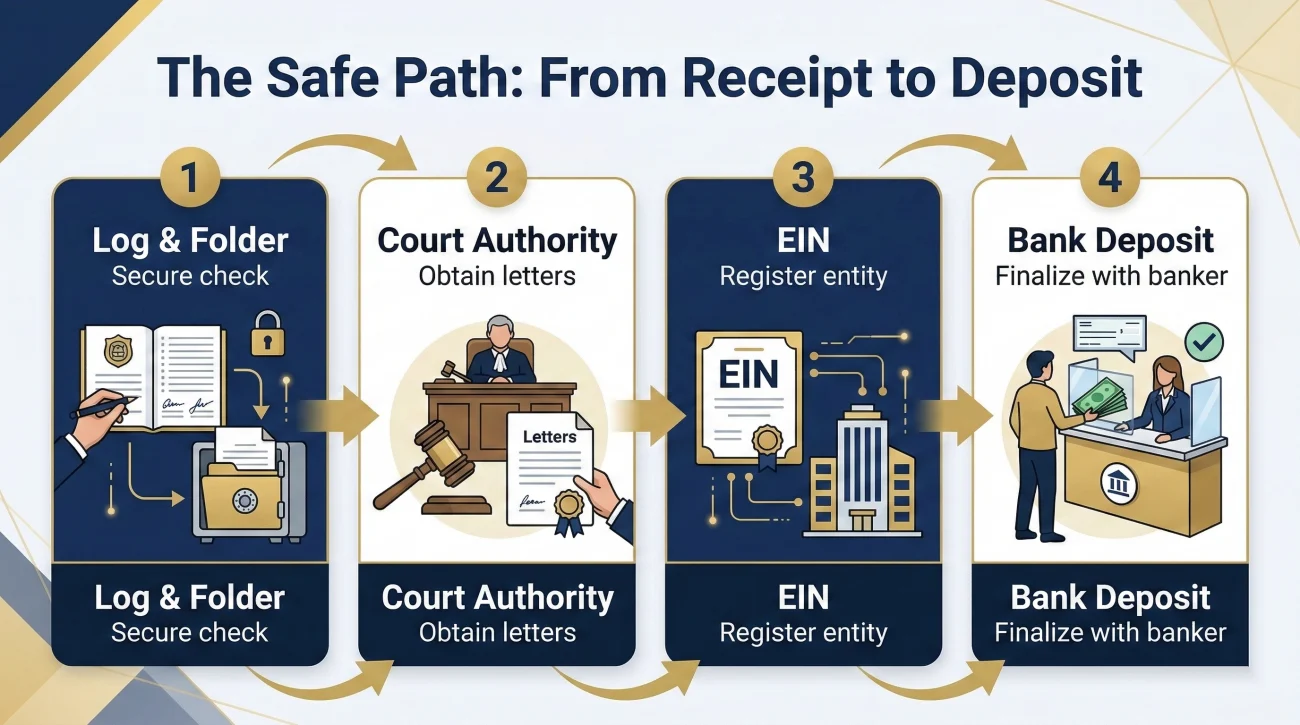

To see how this all connects, let us look at a typical, dispute-free workflow for handling an unexpected estate check. This sequence prevents you from taking backward steps.

First, when the check arrives, you log it in your administrative tracker (date, amount, issuer) and place it in a physical folder. You do not sign it. Second, you focus entirely on obtaining your proof of authority, whether that is court letters or a small estate affidavit. Third, you apply for the estate EIN online.

Fourth, you schedule an appointment with the bank to open the estate account, bringing your clean document packet. Once the account is open and active, you present the check to the banker. You ask them exactly how they want it endorsed. You sign it right there at the desk in front of them, receive your deposit receipt, and file the receipt next to your original log entry. This linear approach eliminates the messy workarounds that trigger fraud alerts.

Common Mistakes That Create Friction

Most errors happen because someone is trying to save time or solve an urgent cash flow problem quickly. In estate banking, skipping steps almost always results in a longer delay.

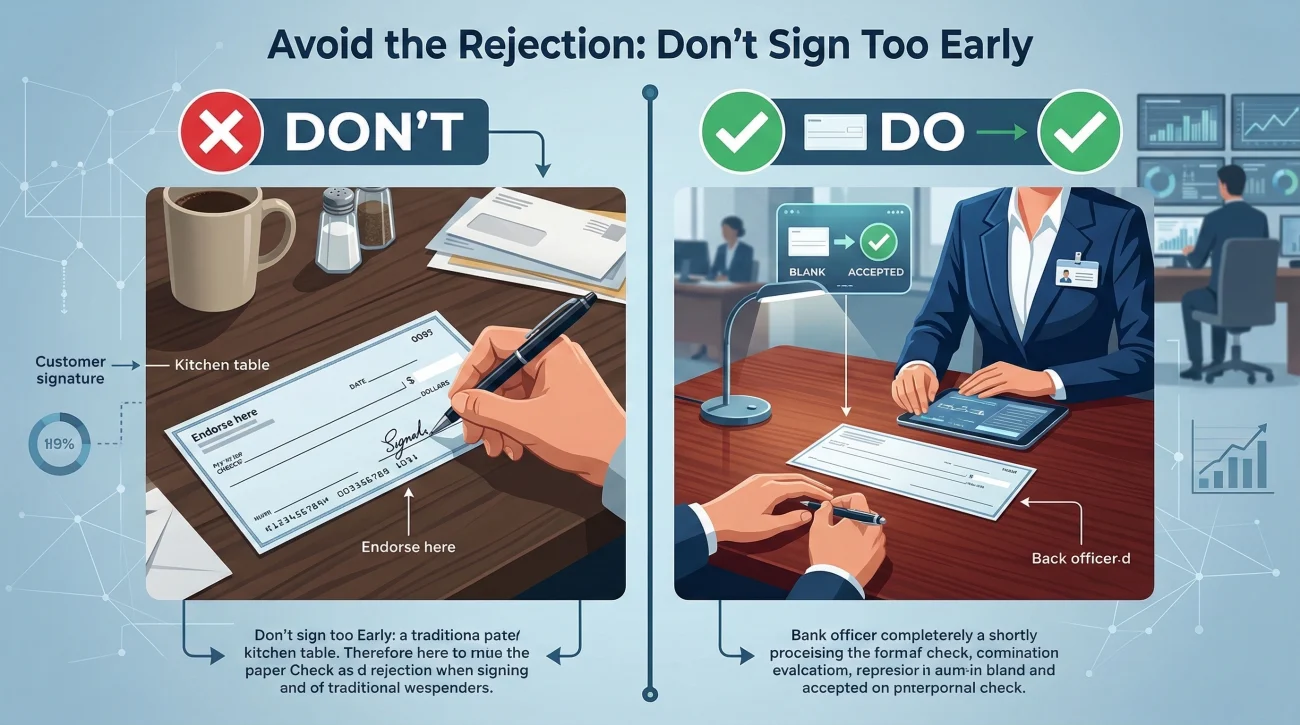

Signing Before Receiving Instructions

The most frequent error is endorsing the check incorrectly before speaking to the bank. If you endorse the check in a way the bank’s fraud department does not accept, you might render the paper void. You would then have to go back to the issuer, explain your mistake, and wait weeks for a replacement.

Signing the back of the check at your kitchen table, hoping the mobile deposit app accepts your signature.

Leaving the back of the check completely blank until you are sitting in front of a banker who tells you exactly what their system requires.

Arguing Logic Instead of Policy

Many executors get understandably frustrated and try to argue logic with the teller: “I am his only son, the money is going to me anyway, just deposit it.” However, the front-line teller simply does not have the administrative power to override compliance software with logic. If you hit a wall, do not escalate an argument about fairness or common sense. Instead, pivot to asking for their written policy. A practical script is to say calmly, “I understand your system will not accept this right now. Can you please print out the specific written requirements your compliance team needs from me to process this deposit?” This shifts the conversation from a personal rejection to a clear, actionable checklist.

Getting Clear Instructions in Writing

Once you know what not to do, the next step is controlling how the conversation actually goes. The goal is to stop reacting to the bank and start guiding the interaction. If you need to ask a bank how to handle a specific check, try to get their answer in writing before you visit the branch. If a phone representative tells you one thing, and a local teller rejects it, you are stuck. Here is a safe, polite way to request clarity if you are communicating via a secure message portal or email:

Subject: Request for deposit instructions: Check payable to Estate

Hello [Name],

I recently received a check made payable to the “Estate of [Deceased Name].” Before I bring this to the branch, could you please provide your institution’s specific requirements for depositing this check?

Specifically, I would like to know:

1. If this must be deposited into the formal estate account.

2. The exact phrasing required for the endorsement on the back of the check.

Please let me know what documents you need from me to process this smoothly.

Thank you,

[Your Name]

If you must ask in person, take clear notes. Write down the name of the banker you spoke with, the date, and the exact steps they gave you. If another employee later contradicts those instructions, you can calmly reference your log. This simple habit of tracking your interactions is one of the most powerful tools you have to maintain control of the workflow.

Final Thoughts on Estate Checks

Receiving a check payable to the estate can feel like a sudden roadblock, especially if you were hoping for a quick resolution to a final bill. It is entirely normal to feel exhausted when the system forces you to slow down. However, remembering that the bank is operating out of strict liability protection can help you approach the counter with more patience.

By securing your authority documents, establishing the proper account infrastructure, and asking for specific endorsement rules before you sign anything, you protect the estate from lost funds and protect yourself from endless administrative loops. Treat each check as a formal transfer of assets, follow the linear workflow, and you will navigate this process safely.

❓ FAQ

🏦 Can I deposit a check made out to the estate into my personal account?

In almost all cases, no. Because the check is payable to the “Estate,” depositing it into a personal account creates an immediate name mismatch. The banking system is programmed to reject these mismatches automatically as a strict fraud prevention measure.

📱 Will mobile deposit work for an estate check?

Usually not, unless you are using the mobile app specifically tied to an officially opened estate checking account. If you attempt a mobile deposit into any other type of account, the back-office audit will likely flag and reverse the transaction.

✍️ How do I endorse a check made out to an estate?

Endorsement rules vary heavily by institution. You should ask the specific bank where you hold the estate account for their exact required endorsement phrasing before writing anything on the back of the check.

⏳ Does an estate check expire if I cannot deposit it right away?

Yes, standard checks typically become stale after 90 to 180 days. If you are waiting on court documents and notice the check is nearing expiration, contact the issuer to explain the delay and ask about their reissue policy.

📝 Do I need letters testamentary to deposit an estate check?

Often, yes. Banks generally require court-issued letters (or a valid small estate affidavit, depending on the rules) to prove you have the legal authority to open an estate account and process those funds.

🏛️ What if the bank refuses to deposit the estate check?

Ask them politely for a written list of exactly what documents or conditions they need to accept the deposit. A refusal usually means they are missing a specific piece of paperwork, like an EIN or certified court letters.

💵 Can a joint account holder deposit a check made out to the estate?

Typically no. Many surviving spouses or children assume that because their name was already on a joint account with the deceased, they can simply deposit the estate check there. However, the bank cannot bridge that gap; it must treat the “Estate” as a completely separate legal entity that requires its own distinct account.

📄 Is a death certificate enough to deposit an estate check?

Rarely. A death certificate proves the person has passed, but it does not prove who has the authority to handle their money. Banks usually need additional proof of authority before allowing a deposit.

💼 Do I have to open an estate account just for one small check?

Often, yes, though some banks have internal exceptions for very small amounts if you provide specific paperwork. You should contact the branch manager, explain the amount, and ask if their policy requires a formal account for that specific size.

🛑 Why did the bank freeze the account after I tried to deposit an estate check?

If you tried to force an estate check into an existing personal account, the bank’s fraud system likely detected the payee mismatch. They freeze the account to stop the flow of funds until they can verify who the money actually belongs to.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.