- An executor bank documents checklist is a highly specific, stripped-down packet designed solely for the bank’s bereavement or legal department.

- Banks typically look for three stacks of verification: Proof of Death, Proof of Identity, and Proof of Authority.

- Do not hand the teller your entire executor master file; only provide what they specifically ask for to avoid confusion and lost documents.

- Packaging matters. Using a cover sheet, avoiding staples on original documents, and keeping physical files organized often reduces processing delays.

The Reality of the Bank Visit

If you are stepping into the role of executor, one of your earliest hurdles will likely be dealing with financial institutions. In my day-to-day admin work supporting people through this process, I often see executors walk into a local branch carrying a heavy, overflowing accordion folder filled with everything from medical bills to family photos, hoping the bank manager can sort it out. Almost inevitably, this leads to a frustrating experience where the bank sends them home to get “just one more document.”

The truth is, bank tellers and branch managers are not probate experts. They are operating off strict internal compliance checklists. When you approach them, you need an executor bank documents checklist that translates your authority into a format their back-office legal department can easily process.

This guide is not about how to settle the entire estate. Instead, I want to walk you through how to build a highly targeted, bank-facing packet. We will look at what documents you actually need to pack, how to physically organize them, and how to avoid the common naming and dating mismatches that cause banks to freeze up.

Scope Boundaries: The Bank Packet vs The Master File

Before we start gathering papers, we need to separate your overall job as an executor from the specific job of unlocking a bank account. It is highly common for people to confuse the two.

Your master executor file will eventually contain tax returns, utility bills, house deeds, and personal notes. The bank does not need, and should not see, 90 percent of that. Handing a bank representative extra, unrequested information usually triggers confusion. If they see a document they do not understand, they may send your entire file to their legal department for an extended review, stalling your progress.

The bank bereavement paperwork packet should be lean, precise, and limited to exactly what the institution requires to prove who you are and what you have the right to do. If you have not yet organized your overall master file and need a broader view of your initial duties, you should pause and review your executor first steps checklist to build your foundation. Once your master file is stable, you can extract just the pieces needed for the bank.

⚠️ Warning: Never surrender your only original copy of a legal document to a bank unless you have confirmed in writing that they will return it immediately. Often, banks only need to inspect the original and scan a copy into their system.

The Two-Trip Strategy and the Pre-Visit Call

Before we build the packet, we need to adjust expectations. I frequently see executors stress themselves out trying to get everything done in a single branch visit. In reality, bank access is usually a two-trip process.

Trip one is often just for discovery—finding out exactly what their specific legal department requires. Trip two is for submission. You can often skip the frustrating first trip by making a targeted phone call before you ever step foot in a branch.

Instead of walking in cold, call the local branch and use this script:

“Good morning, I am the executor of an estate and I need to begin the account closure process. Could you connect me with your estate settlement or bereavement team so I can confirm exactly which documents to bring?”

This ensures you are speaking to the right department and stops you from guessing what their back office needs.

The Core Model: The 3-Stack Bank Packet

When you sit down with a bank representative, they are essentially trying to answer three specific questions to satisfy their fraud and compliance rules. I have found it incredibly helpful to mentally organize the documents bank needs after death into three distinct “stacks.” When you understand what each stack is trying to prove, it becomes much easier to anticipate what the bank will ask for.

Stack 1: Proof of Death

The bank must confirm that the account holder has actually passed away. This triggers them to lock the account to protect the funds from unauthorized withdrawals.

The primary document here is the death certificate. However, a simple photocopy you made at home is rarely sufficient. Banks typically require a certified copy of the death certificate. This means it must have the raised seal or colored ink stamp from the county or state vital records office.

In many cases, the branch manager will take your certified copy, look at the seal, make their own internal photocopy, and hand the certified original back to you. However, some smaller institutions or specialized departments may ask you to mail a certified copy that they will keep. Always ask for their specific policy before mailing anything.

Stack 2: Proof of Identity

Once the bank knows the account holder has passed, they need to know exactly who is sitting across the desk from them. Because of strict federal “Know Your Customer” (KYC) banking regulations, institutions have very little flexibility here.

You must provide unexpired, government-issued photo identification. Acceptable forms typically include:

- ✅ A valid state driver’s license

- ✅ A current passport

- ✅ A state-issued non-driver ID card

Here is a common pattern where things go wrong: The court documents name the executor as “William T. Harris,” but your driver’s license just says “Bill Harris.” To a strict bank compliance officer, those are two different people.

If your identification does not perfectly match the name listed on the court documents, you may face delays. It is often wise to bring secondary forms of identification or a marriage certificate if your name has changed.

⚠️ Warning for Co-Executors: If the court appointed two of you to act together, banks will often require both of you to be present in the branch with your IDs to initially set up the estate account, unless your court documents explicitly grant independent authority.

Stack 3: Proof of Authority

This is the most critical stack. Just because you are the deceased person’s child, or even if you are holding their original Last Will and Testament, does not automatically give you the authority to withdraw their money. The bank needs legal proof that you are the authorized decision-maker.

Typically, this means providing executor proof of authority issued by the probate court. Depending on your local jurisdiction, this document is commonly known as Letters Testamentary or Letters of Administration.

While specific administrative requirements can vary slightly by state, financial institutions are ultimately guided by federal and FDIC regulations regarding the protection of insured deposits. They cannot legally release funds to you until your authority is verified to the satisfaction of their internal compliance requirements. Banks look closely at these court documents for two things: the scope of your power and the date the document was issued.

Many banks have internal rules requiring that the Letters be “fresh” (often dated or recertified within the last 60 to 90 days). If your court documents are older than that, the bank may refuse them. If you need a deeper understanding of how these court documents function in the broader probate process, you can refer to your general probate court checklist.

The Tax Identity Add-On: When the EIN Appears

While the three stacks above cover the basics of access, you will commonly encounter a fourth requirement: tax documentation. Once a person passes away, their Social Security Number can generally no longer be used. However, I frequently see executors apply for an Employer Identification Number (EIN) before they even know if the bank requires one.

Here is a safer decision tree to follow for bank visits:

- 📄 You likely DO need an EIN if: You are opening a new “Estate of” checking account, or you need to deposit checks made payable directly to the estate.

- ✅ You likely DO NOT need an EIN if: You are simply closing an existing account and the bank is issuing a cashier’s check for you to distribute, or if you are claiming a POD account as a direct beneficiary.

If you have determined you need an estate EIN, bring the official confirmation letter you received from the IRS. Additionally, the bank may ask you to fill out a W-9 form to formally certify the estate’s tax ID number in their system.

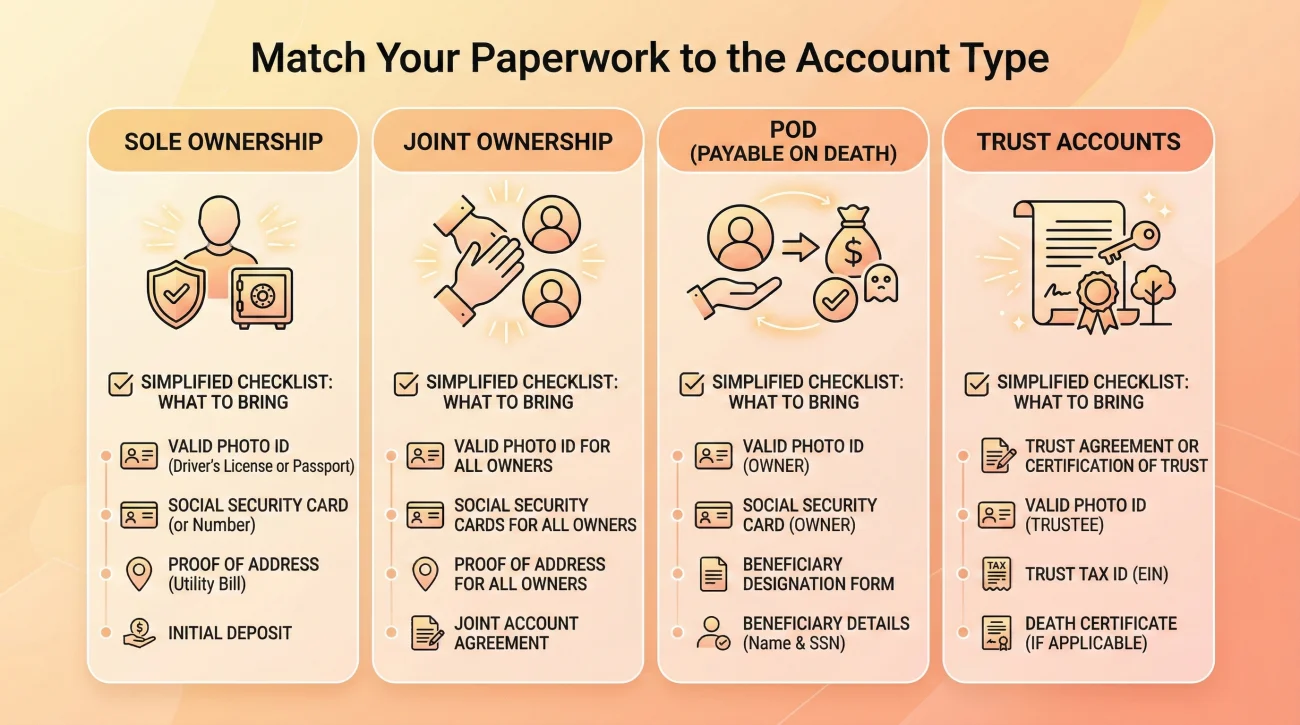

Specific Triggers: How Account Types Change the Packet

One of the most frequent points of confusion for executors is why a bank might ask for court documents on one account, but hand over a check for another account just by seeing a death certificate. The required executor bank documents checklist changes based entirely on how the account was owned.

| Account Ownership Type | What Banks Commonly Request | Why They Ask For It |

|---|---|---|

| Sole Ownership (No Beneficiaries) | Death Certificate + ID + Court Letters | The estate is the only entity that can claim the funds, requiring court-appointed authority. |

| Joint Ownership (With Right of Survivorship) | Death Certificate + ID of Surviving Owner | The account generally passes directly to the surviving owner, bypassing the probate estate. |

| Payable on Death (POD / TOD) | Death Certificate + ID of Named Beneficiary | The funds belong directly to the named beneficiary upon death, not the executor. |

| Trust Owned Account | Death Certificate + ID + Certificate of Trust | The successor trustee has authority, not the executor (unless they are the same person). |

As you can see, if you are dealing with a POD account where you are the named beneficiary, bringing your court-issued Letters Testamentary is often unnecessary and might only confuse the teller. Always try to determine the account type before finalizing your paperwork packet.

A note on online-only banks: If you are dealing with a digital-only institution that has no physical branches, this entire process shifts to secure online portals or certified mail. The rules of the packet remain the same, but the delivery changes. Never mail your only original documents unless they explicitly guarantee their return in writing.

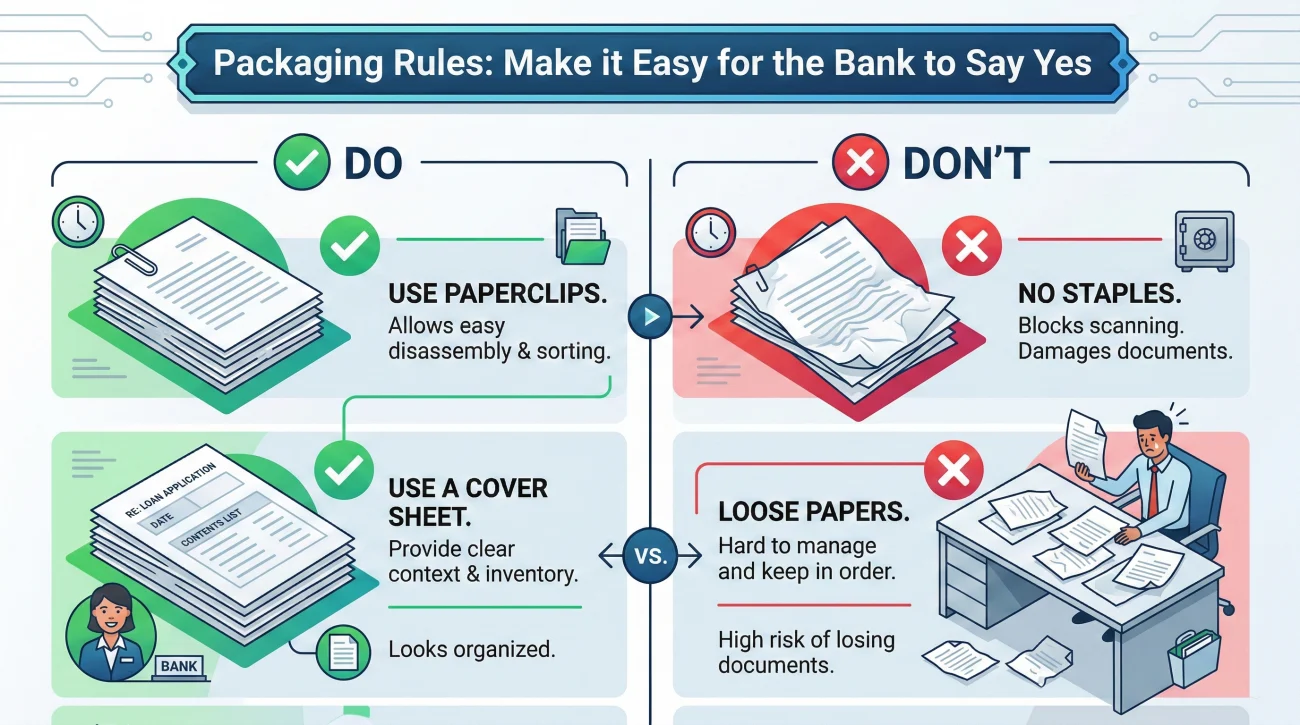

Packaging Rules That Reduce Back-and-Forth

In my experience, having the right documents is only half the battle. How you present those documents heavily influences how smoothly the bank processes your request. If you hand over a crumpled, stapled stack of mixed papers, the bank associate has to sift through it, increasing the chance they overlook something and delay your access.

Here are operational habits that create a professional, bank-ready packet:

- 📄 Use paperclips, never staples: Bank back-offices need to scan documents. If you staple your original Letters Testamentary, they will have to rip the staple out, potentially tearing the official seal.

- ✅ Create a dedicated folder: Do not carry your bank documents in the same folder as the funeral receipts. Use a clean, distinct envelope or folder labeled clearly with “Bank Documentation: Estate of [Name].”

- 📑 Use a cover sheet: A simple printed cover sheet acts as a map for the bank associate. It shows them exactly what you have brought.

Here is an example of a simple, effective cover sheet you can clip to the front of your packet:

Estate of: [Deceased Name]

Date: [Current Date]Documents Included in this Packet:

1. Certified Copy of Death Certificate (For inspection and copy)

2. Original Letters Testamentary (For inspection and copy)

3. Copy of Executor’s Driver’s License

4. IRS Confirmation Letter for Estate EIN

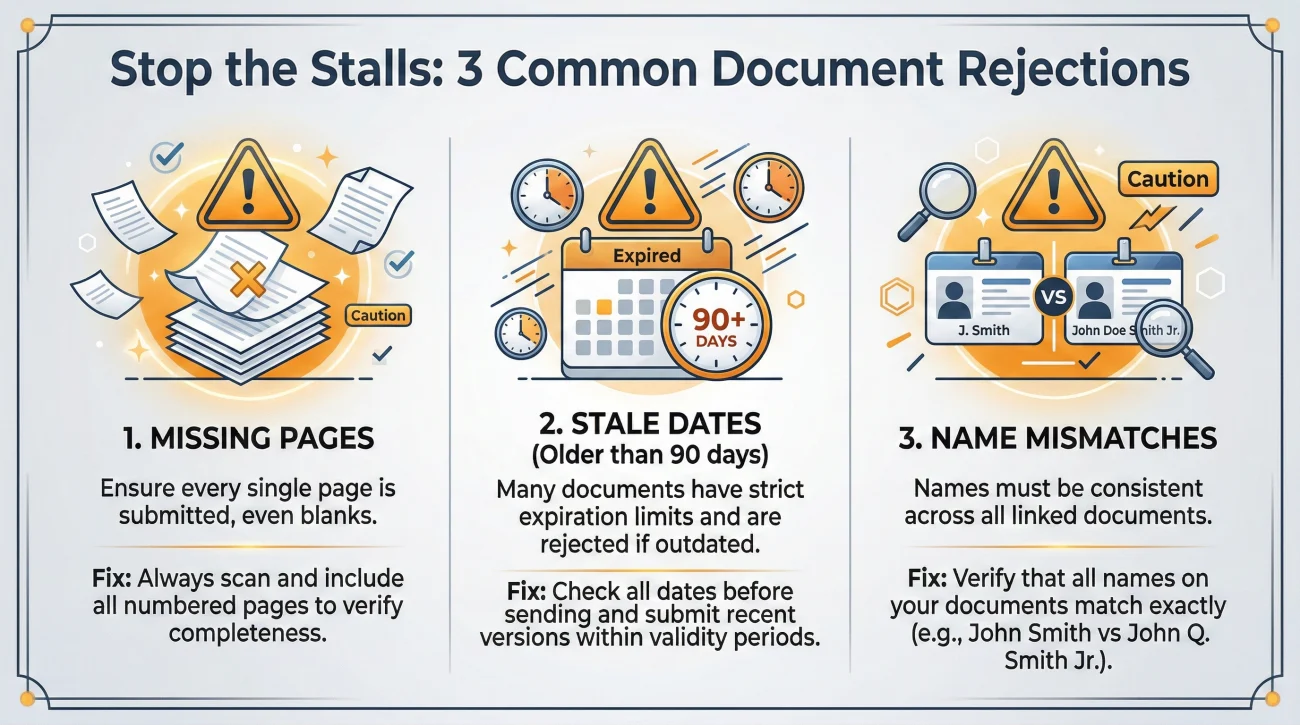

Common Packet Failures (And How to Prevent Them)

Even when your packet is perfectly assembled, the bank itself can introduce friction. Knowing where other executors commonly stumble can save you a frustrating return trip.

Missing Pages: In my operational experience, I often see perfectly organized packets get rejected because of a single missing page. Sometimes court documents or trust certificates are several pages long. If you accidentally leave the last page containing the judge’s signature at home, the bank’s legal team will reject the entire submission. Always count your pages.

Stale Paperwork: As mentioned earlier, banks hate old court documents. If your Letters were issued in January and you go to the bank in October, they may reject them. Always check the date on your court documents before a bank visit. If they are older than 60 days, you may need to ask the court clerk for a freshly stamped copy.

Name Mismatches: If the deceased used a nickname at the bank (“Bob”) but their legal name on the death certificate is “Robert,” the bank’s system may flag a mismatch. Be prepared to provide additional proof linking the names, or ask the bank what specific document they need to bridge that gap.

Walking into the bank with a grocery bag of loose mail, old tax returns, a photocopy of the death certificate, and asking the teller “what do I do?”

Walking into the bank with a slim folder containing your ID, one certified death certificate, fresh court Letters, and a cover sheet mapping exactly what you brought.

Responding to the “One More Document” Request

No matter how perfectly you pack your folder, there is always a chance the bank’s internal legal department will request something extra. Every institution has its own quirks. Some require a proprietary “Affidavit of Domicile,” while others have their own internal beneficiary claim forms.

When a bank representative tells you that your packet is incomplete, the worst thing you can do is argue legalities at the window. Instead, pivot to clear, written communication.

I always recommend using this formula when dealing with a stalled request:

[Acknowledge the requirement] + [Ask for the exact name of the document] + [Request the requirement in writing]

For example, if the teller says the back office rejected your letters, you can say:

“I understand the legal department needs more information to release the funds. Could you please print out their exact internal requirement or the specific form they need, so I can make sure I bring back exactly what they are asking for?”

Getting their requirements in writing prevents the awful loop of returning three different times for three different forms. It forces the bank to give you a definitive checklist. For a broader overview of how to navigate these institutional roadblocks, reviewing the executor banking checklist map is highly recommended.

Final Thoughts on Building Your Packet

Preparing the documents a bank needs after a death is an exercise in restraint. The goal is not to prove everything about the estate, but to prove just enough to unlock the next step of the banking process. Keep your packets small, keep your original documents safe, and always document who you spoke with and what you handed over.

Whether you are walking into a physical branch alongside a co-executor, or uploading scanned files to a digital-only bank portal, the principle remains the same. Protect your original certifications, prove exactly what is required for that specific account type, and always get their requirements in writing to stop the frustrating back-and-forth loop.

❓ FAQ

🏦 Do I need to bring original death certificates to the bank?

Banks usually need to inspect a certified copy of the death certificate (the one with the raised seal or stamp). Many will make a photocopy for their records and hand the certified copy back to you, but some may require you to mail one in. Always ask before leaving an original behind.

⏳ How old can my Letters Testamentary be for the bank?

Many financial institutions have internal policies requiring court letters to be dated within the last 60 to 90 days. If your letters are older than their threshold, you may need to visit the court clerk to get a newly certified, updated copy.

🪪 What happens if my name on my ID doesn’t exactly match the will?

A mismatch (like missing a middle initial or a maiden name change) can cause delays. You may be asked to provide secondary identification, a marriage certificate, or an affidavit explaining the name variation to satisfy the bank’s compliance team.

📑 Can I just email the documents bank needs after death?

Usually not initially. Because of fraud concerns, most banks require you to present original or certified documents in person at a branch, or mail them via certified mail to a specific bereavement department. Ask for their exact secure submission process.

📋 Does the bank need a copy of the will or just the court letters?

In most standard probate cases, the bank only needs the court-issued Letters Testamentary, as that proves the court has authorized you. However, some banks may ask for a copy of the will for their records. It is best to bring it but only offer it if explicitly requested.

🗣️ What if the bank refuses my paperwork but won’t put the reason in writing?

If a teller refuses your documents verbally, calmly ask to speak with the branch manager. Explain that you need their specific denial policy or missing document request in writing so you can present it to your probate attorney or the court for the official record.

📞 Who at the bank actually reviews my bereavement paperwork?

The teller or branch manager usually only collects the documents. The actual review and approval is almost always done by a back-office legal or estate settlement department. This is why having clean, easy-to-read paperwork is critical.

🛑 What if the bank loses the paperwork I dropped off?

This happens. To protect yourself, always use a cover sheet, keep a personal log of exactly what you handed over and to whom, and never give away your only original certified copy of a document without a receipt.

🤝 Do I need these documents if I was a joint owner on the account?

Typically, joint accounts with rights of survivorship only require a certified death certificate and the surviving owner’s ID to remove the deceased person’s name. You usually do not need court letters for this specific type of account.

📝 Why is the bank asking me for an EIN to access the funds?

If you need to open an “Estate of” checking account to deposit checks made out to the deceased, you cannot use their old Social Security Number. The bank needs an Employer Identification Number (EIN) to properly report tax information for the estate entity.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.