- Closing an estate account is usually the final administrative step, but it often requires all pending transactions to be fully cleared and the balance to hit exactly zero.

- Banks view “settlement” differently than families do; the bank simply needs clear authorization and a zero balance to officially shut down the ledger.

- Uncashed distribution checks and phantom interest (a few cents posting overnight) are the most common roadblocks that prevent an executor from closing the account.

- Keeping a clean paper trail of the final bank statement and the closing confirmation is critical for your own recordkeeping and protection.

Approaching the Finish Line: The Reality of the Final Step

By the time you are ready to close an estate bank account, you have likely been acting as an executor for months, if not longer. You have gathered documents, tracked down assets, paid final bills, and navigated a maze of paperwork. You just want to distribute the remaining funds, close the estate bank account, and finally step away from the administrative burden.

In my experience helping executors organize their workflows, this final step is often where patience is tested the most. Because the finish line is in sight, there is a natural temptation to rush. However, closing an estate checking account is rarely as simple as clicking a button or making a quick phone call. It requires precision.

One of the most frustrating cases I have seen involved an executor who spent three weeks trying to close an account, only to be blocked repeatedly because of a twenty-cent discrepancy and a slightly misnamed internal form. If you leave a few cents behind, the bank will keep the account open. If you close the account too early and a final tax bill arrives, you may find yourself in a difficult position without an estate ledger to pay from.

The goal of this guide is to walk you through what to expect after the estate is settled, how to prepare the bank-facing paperwork, and how to avoid the common logistical traps that cause the finish line to slip further away.

What “Settlement” Actually Means in Banking Terms

When families talk about settlement, they usually mean that everyone has agreed on who gets what, the house is sold, and the major debts are paid. But banks do not see the family dynamics. To a bank, settlement is purely mathematical and procedural.

Banks are primarily concerned with liability. They want to ensure that whoever is asking to close the account still has the active authority to do so, and they want to make sure the ledger is perfectly balanced at zero. If the bank closes an account while an automated payment is still pending, or while a check is floating around uncashed, it creates a reconciliation problem for them.

Key Point: To a bank, “settlement” simply means the account has a zero balance, there are no pending holds or incoming transactions, and the authorized executor has provided a formal instruction to close the file.

Depending on how the account was originally opened and what rules the bank operates under, the closing process can range from a simple withdrawal request to a requirement for a final court document showing the estate is formally closed. This is why I always recommend treating the final account closure as its own distinct administrative project, rather than an afterthought.

The Timing Squeeze: When Do You Actually Close It?

One of the most common questions executors ask is regarding the exact order of operations. Do you empty the account first and then close it? Do you close it and have the bank hand you a final cashier’s check?

Often, the safest order of operations is to request the closure first, and let the bank issue the final remaining funds directly to you as the executor on that specific day. Trying to manually zero out the account beforehand with personal calculations usually backfires, as banking systems process fees and interest on their own hidden schedules.

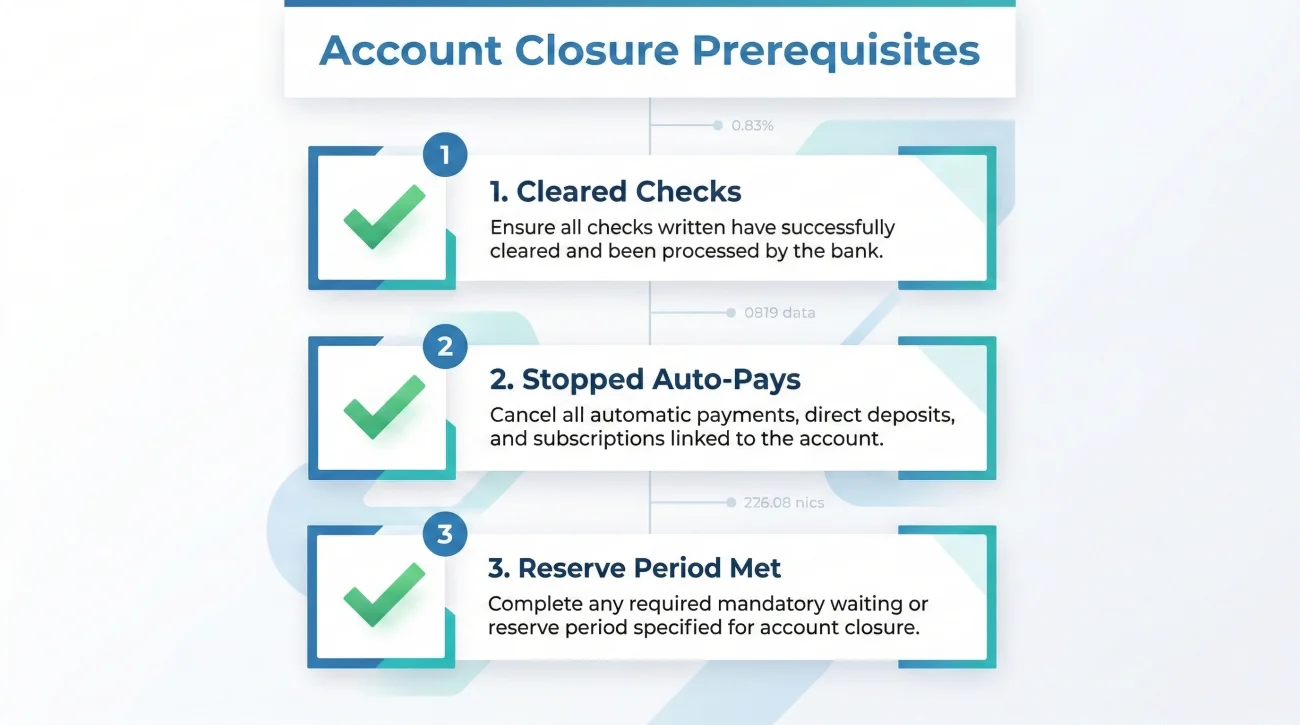

Common Prerequisites Before You Request Closure

Before you walk into a branch or send a final closure letter, you need to ensure the account is truly ready to be shut down. Attempting to close an account prematurely is a common pattern that leads to unnecessary back-and-forth phone calls with bank representatives.

When reviewing post-settlement files, the cleanest closures always share the same baseline. You should verify these three conditions first:

- ✅ All outgoing checks have fully cleared: If you wrote checks to creditors or initial distributions to beneficiaries, you must wait until those checks actually post to the account. An uncashed check is a hard stop for the bank.

- ✅ All automatic deposits and withdrawals are stopped: Check the last three months of statements. Are there any residual refunds expected? Are there any automatic bill pays still hooked up to this routing number? Everything must be manually disconnected.

- ✅ The “Reserve” period has passed: Many executors choose to hold a small reserve of funds in the estate account just in case a surprise final tax bill or late administrative expense appears. Typically, this reserve period lasts 3 to 6 months after the main distributions. The exact length depends heavily on whether you are waiting for a final tax return to process or expecting a delayed property tax refund. Once you have cleared the tax deadlines and are confident no more expenses are coming, the account is ready.

Meeting these conditions sounds simple, but the reality of banking systems often gets in the way. When these prerequisites are not perfectly met, you hit administrative roadblocks.

Common Finish-Line Roadblocks (And How to Handle Them)

Even with careful planning and a completed checklist, the final days of an estate account can get messy. The banking systems are automated, and they look for exact matches. Here is how to handle the situations where the prerequisites fail.

The Phantom Interest Problem

This issue specifically applies to interest-bearing accounts. If the estate account earns any interest at all, even a tiny fraction of a percent, it accrues daily and posts at the end of the statement cycle. You might look at the balance on a Tuesday, see exactly $5,000, and write distribution checks totaling $5,000. By the time those checks clear on Thursday, the account might have generated $0.12 in interest. The balance is now twelve cents, not zero. The bank will not close it.

The practical workaround is to let the bank do the final math. When you are ready for the final distributions, you ask the bank to close the account and issue the entire remaining balance (including the exact interest up to that very second) in the form of a cashier’s check. You then use that cashier’s check for the final distribution.

The Uncashed Distribution Check

I have watched executors get caught by this exact problem three times in one quarter. You mail a final check to a family member. Two months pass, and they have not deposited it. Because the funds are still sitting in the estate account, the bank considers the account active. You cannot close it until that money moves.

| The Problem | The Practical Fix |

|---|---|

| Beneficiary is slow to deposit the check. | Set a polite but firm deadline. Remind them that the estate cannot be finalized until all checks clear the banking system. |

| The check was lost in the mail. | Place a stop payment on the original check, verify the address, and issue a replacement immediately. Document the stop payment fee. |

| Beneficiary’s name was misspelled on the check. | Do not ask them to “just try depositing it anyway.” Void the check in your records and write a new one with the exact legal name matching their ID. |

Stale Authority Documents

Some banks have policies regarding the “freshness” of your authority documents. Even though you opened the account a year ago using your certified court papers, the bank might ask to see a newly certified copy (often dated within the last 60 to 90 days) to prove that your authority was never revoked before they allow you to withdraw the final funds. If the bank requests this, it is usually faster to simply obtain the updated copy rather than arguing with the branch manager about policy.

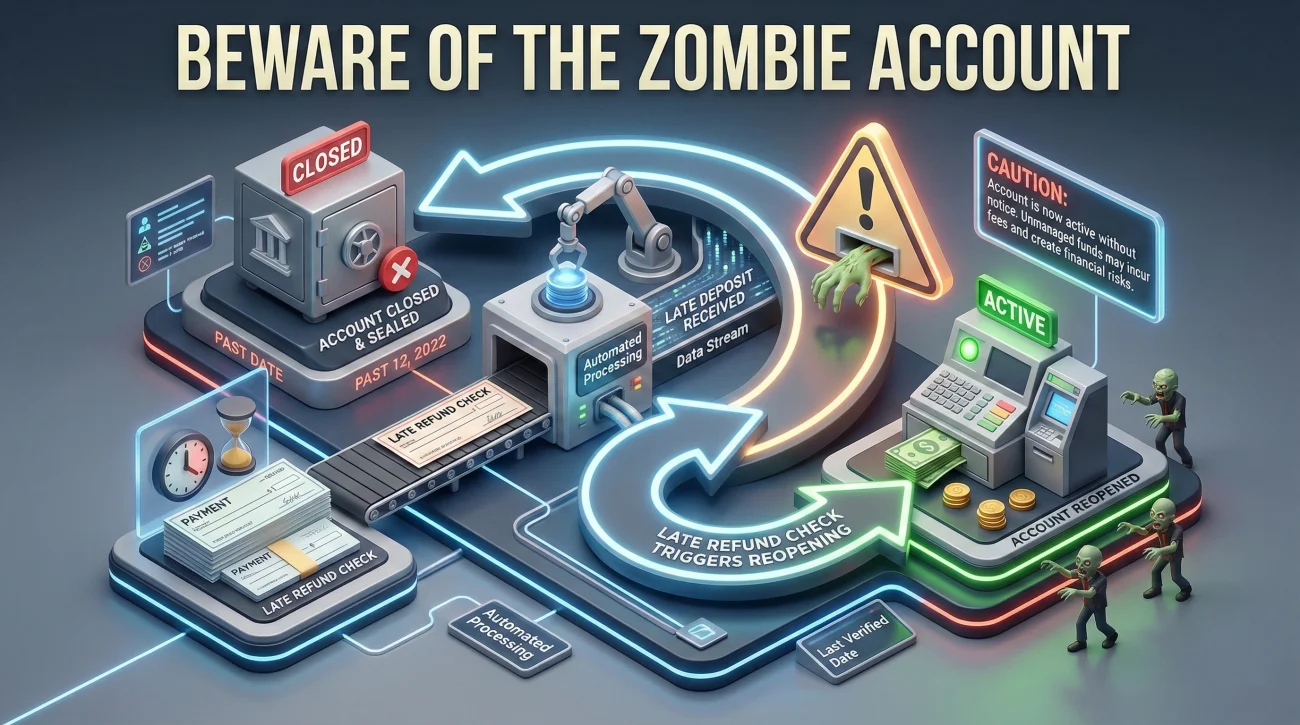

Handling the “Zombie” Account: When a Closed Account Reopens

You successfully close the account, the balance is zero, and you have the confirmation receipt. Three weeks later, an unexpected utility refund check arrives made out to the “Estate of [Name]”. Or worse, an automated deposit tries to hit the old routing number.

Many banking systems are programmed to automatically reopen a recently closed account if a valid deposit arrives within a certain window (often 30 to 60 days). Suddenly, your closed estate account is a “zombie” account, back from the dead with a small positive balance, and usually incurring monthly maintenance fees because it no longer meets minimum balance requirements.

⚠️ Warning: Do not ignore late-arriving checks. If you try to endorse an “Estate of” check over to your personal account, it will likely be rejected for commingling risks. You usually have two choices: go back to the bank to formally reopen the account, deposit the check, and repeat the closure process; or contact the issuer of the check and request they reissue it directly to the beneficiaries (which is often very difficult). This is why the 3 to 6 month reserve period is so critical.

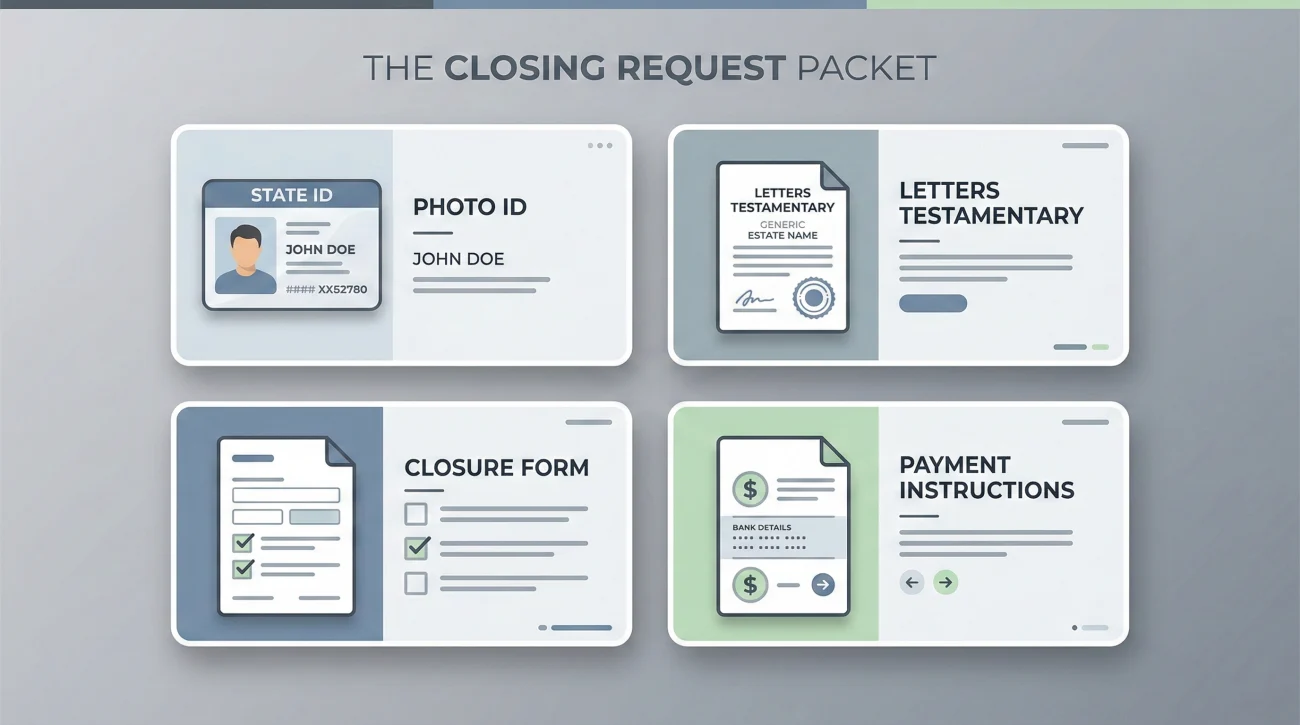

What Banks Usually Need to See for Closure

When you are ready to make the final request, you should treat it like a mini-packet, similar to the documentation you provided when opening the account. Having everything organized reduces the chance of the bank asking you to come back another day.

A typical closing request packet might include:

- 📄 Your personal identification: Always carry your unexpired, government-issued ID. If there are multiple co-executors on the account, some banks require all of you to be present or to sign a notarized release.

- 📄 Proof of authority: Have a recent copy of your appointment documents on hand. Some banks scan this into their system; others need a physical copy for their compliance file.

- 📄 The closing instruction: The format matters. Some banks require you to sign a specific internal “Account Closure Authorization” form directly at the branch. Others may accept a formal letter of instruction, but might require a medallion signature guarantee if you are doing it by mail.

- 📄 Payment instructions: Clear directions on where the remaining balance should go (e.g., “Please issue a cashier’s check payable to the Estate of [Name]”).

Closing Channels: In-Person vs. By Mail

If you live in the same town as the branch, closing in-person is almost always the safest and fastest route. You can walk out with the zero-balance receipt in hand.

However, if you are an out-of-state executor dealing with a regional bank, you may be forced to close the account by mail. Mail closures require much stricter documentation. The bank will typically not accept a simple letter. They will often require you to mail a formalized closure request with a notarized signature, or sometimes a medallion signature guarantee, along with your updated certified court documents. Always call the specific institution first to ask for their exact mail-in closure procedures.

💡 Pro Tip: Before you drive to a branch or mail a packet, call ahead. Ask the representative: “I am the executor for an estate account ending in 1234. I am preparing to close the account next week. Can you provide a written list of the documents your specific branch requires to process a closure?”

Keeping the Final Distribution Readable for Beneficiaries

Closing the account at the branch is only half the job; the other half is communicating that finality clearly to the heirs. If beneficiaries receive a random check in the mail with no context, they may have questions, which leads to more phone calls for you. A sudden, unexplained payout can trigger anxiety about whether the numbers were calculated correctly.

The goal is to provide a highly readable, transparent trail. When you send the final funds, you should also send a clear explanation of what the check represents and confirm that the bank account is officially closing. This is part of maintaining good communication hygiene.

Mailing a check with a sticky note that just says, “Here is the rest of the money, the bank is closed now.”

Sending a brief, formal cover letter that explains the final accounting, states the bank account is now at zero, and provides the final statement for their records.

Here is a neutral, safe script you can use to communicate this final step. It keeps expectations clear and creates a written record that you have completed the banking portion of your duties.

Subject: Final Estate Distribution and Account Closure – Estate of [Name]

Hello [Name],

I am writing to provide you with the final distribution from the Estate of [Name]. Enclosed is a check for [Amount].

This check represents your final portion of the remaining estate funds. With this distribution, the estate bank account has reached a zero balance and has been officially closed with [Name of Bank].

I have also attached a copy of the final bank statement showing the closure for your records. Please deposit this check at your earliest convenience so that we can conclude the final administrative tracking.

Thank you for your patience throughout this process.

Best regards,

[Your Name]

Executor, Estate of [Name]

What to Keep for Your Own Records (The Post-Closure Archive)

Once the teller hands you the receipt showing a zero balance and confirms the account is closed, your job is mostly done. However, you must not throw away the banking files. Questions can arise months or even years later, and your only defense is a well-organized archive.

If you have been maintaining clear recordkeeping for bank requests, you already have a logical folder structure. Now, you just need to add the final pieces to the archive. Treat this as your final-day mandatory checklist.

You should permanently retain these three items:

- 📄 The zero-balance confirmation: This might be a final receipt from the teller or a formal letter generated by the bank confirming the account status is “Closed.”

- 📄 The final statement: Banks usually generate one last statement at the end of the month showing the balance going from something to zero. Make sure you log in and download this, or confirm it will be mailed to you, before you lose online access.

- 📄 Copies of final distribution checks: If you wrote checks to beneficiaries or received a cashier’s check from the bank to distribute, keep scanned copies of the front and back of those checks (once cleared, if possible) to prove the money went where it was supposed to go.

❌ Note: Do not rely on the bank’s online portal to store your records. The moment an account is closed, many banks immediately revoke your online login access. Download every PDF statement to your personal executor folder before you request the closure.

Final Thoughts on Closing the Loop

Closing the estate bank account is a major milestone. It represents the physical end of the financial administration. While the process can feel overly bureaucratic, remembering that the bank is simply trying to zero out their liability will help you navigate the final paperwork with less frustration.

By ensuring all pending transactions are clear, accounting for every cent of interest, and keeping a meticulous paper trail of the final statements, you protect yourself from future questions and close out your duties cleanly. If you need to review the broader picture of how banking fits into the entire process, you can revisit our main executor banking checklist.

❓ FAQ

⏱️ How long does it take to close an estate account?

If there are no pending transactions and you have the correct authority documents, the actual bank process usually takes less than an hour at a branch. However, waiting for final checks to clear before you can request the closure often takes several weeks.

⚖️ Can I close the estate account before probate is officially over?

This largely depends on the specific instructions of the local court or the type of administration you are handling. Many executors keep the account open until the court formally approves the final accounting and releases them from their duties.

📬 What happens if a check arrives after I close the estate account?

This often causes the banking system to automatically reopen the account, creating a “zombie” account that may start incurring fees. You generally cannot deposit an estate check into your personal account due to commingling rules. For the full decision map on how to resolve this safely, see the Handling the “Zombie” Account section above.

💸 Do banks charge a fee to close an estate account?

Typically, banks do not charge a specific “closure fee.” However, they may charge fees for issuing multiple cashier’s checks for final distributions, or standard monthly maintenance fees if the balance dropped below a minimum threshold right before closing.

🏦 How should I distribute the money before closing the account?

Many executors find it safer to have the bank issue cashier’s checks for the final distribution amounts at the exact moment of closing, rather than writing personal estate checks and waiting weeks for them to clear the ledger.

🏛️ Do I need court permission to close the executor account?

The bank itself usually does not require a new court order just to close the account (unless it was a highly restricted account). However, your local legal guidelines may require you to file a final accounting with the court before you are permitted to distribute funds and close the bank file.

📄 What do I do with the final bank statement?

Save it permanently in your digital and physical executor files. You may need to provide copies to the beneficiaries to prove the final balance was distributed, or file it with your final reporting documents.

❌ Can I just transfer the remaining estate funds to my personal account?

Transferring estate funds into your personal checking account is generally considered commingling, which creates severe accounting risks and disputes. Funds should be distributed directly from the estate account to the proper beneficiaries.

🔔 Will the bank notify beneficiaries when the account is closed?

No. The bank only communicates with the authorized executor. It is your responsibility to inform the beneficiaries that the final distributions have been made and the banking matters are concluded.

🪙 What if there is only a few dollars left in the estate account?

The bank will not close an account with a positive balance, even if it is just $2.00. You must withdraw or distribute every single cent to bring the ledger to exactly $0.00 before the closure can be finalized.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.