- A last will and testament is a document of wishes, but it does not automatically grant you legal access to bank accounts.

- Banks are heavily regulated and typically require proof of court appointment, not just a nomination in a will, to release funds.

- The type of account ownership (like joint or POD) often overrides the will entirely.

- Some smaller estates may qualify for a simplified process, bypassing the need for formal court documents.

- Arguing with branch staff rarely works; instead, ask for their exact documentation requirements in writing.

The Frustration of Holding the Right Document at the Wrong Time

In my time helping families navigate the administrative side of estate closures, I see one specific scenario play out almost weekly. A family member walks into a local bank branch, holding a pristine, legally signed last will and testament. They point to the page where they are clearly named as the executor and expect the bank to hand over the account balances.

Instead, the teller politely slides the will back across the counter with a firm no. When a bank won’t accept will executor paperwork as proof of authority, the immediate reaction is usually confusion and frustration. I completely understand how maddening this feels. You are trying to do the right thing, pay the final bills, and secure the assets, so why is the institution ignoring the document?

The truth is, the bank is not necessarily trying to make your life difficult. When the bank won’t talk to executor candidates, it usually comes down to a fundamental misunderstanding of what a will actually does in the eyes of a financial institution. Today, I want to share exactly what the bank is waiting for and how you can move forward without getting stuck in a loop of unhelpful branch visits.

What a Bank is Actually Trying to Verify

To understand why the bank rejects the will, it helps to look at the situation from their risk department’s perspective. If they release funds to the wrong person, the bank can be held financially liable for the loss. Before they will speak to anyone new about a frozen account, they typically need to verify three specific things with absolute certainty.

- 🔎 Identity: Does your ID perfectly match the name on the documents you are providing?

- 📜 Authority: Do you have the active, current legal right to touch this specific money right now?

- 🏦 Ownership Type: Was this account solely owned, jointly owned, or designated to go to a specific beneficiary?

Why a Will Alone Often Doesn’t Unlock Access

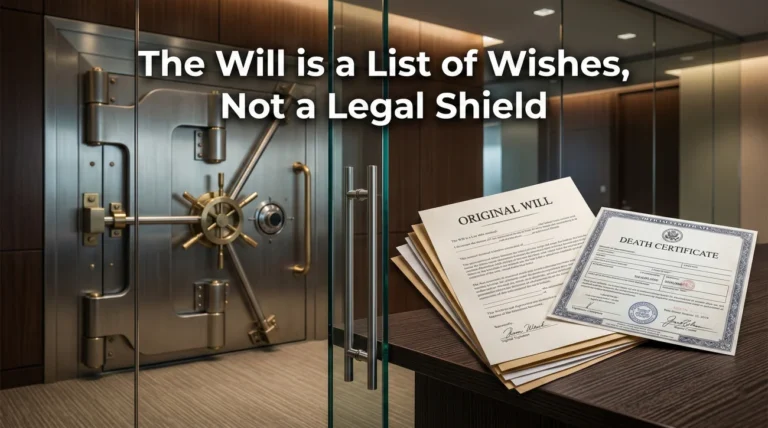

A will might help establish your identity, but it usually fails the bank’s test for active legal authority. The core issue is that a will is essentially a list of the deceased person’s wishes. A piece of paper drawn up by a lawyer, even if notarized, is not a court order.

The bank teller has no way of knowing if the will you are holding is the absolute final version or if another family member holds a newer one. Because they cannot independently verify it, they simply cannot act on it.

Believing the will is a magic key that instantly unlocks bank doors the moment someone passes away.

Understanding that the will is just your application to the court to get the actual authority the bank requires.

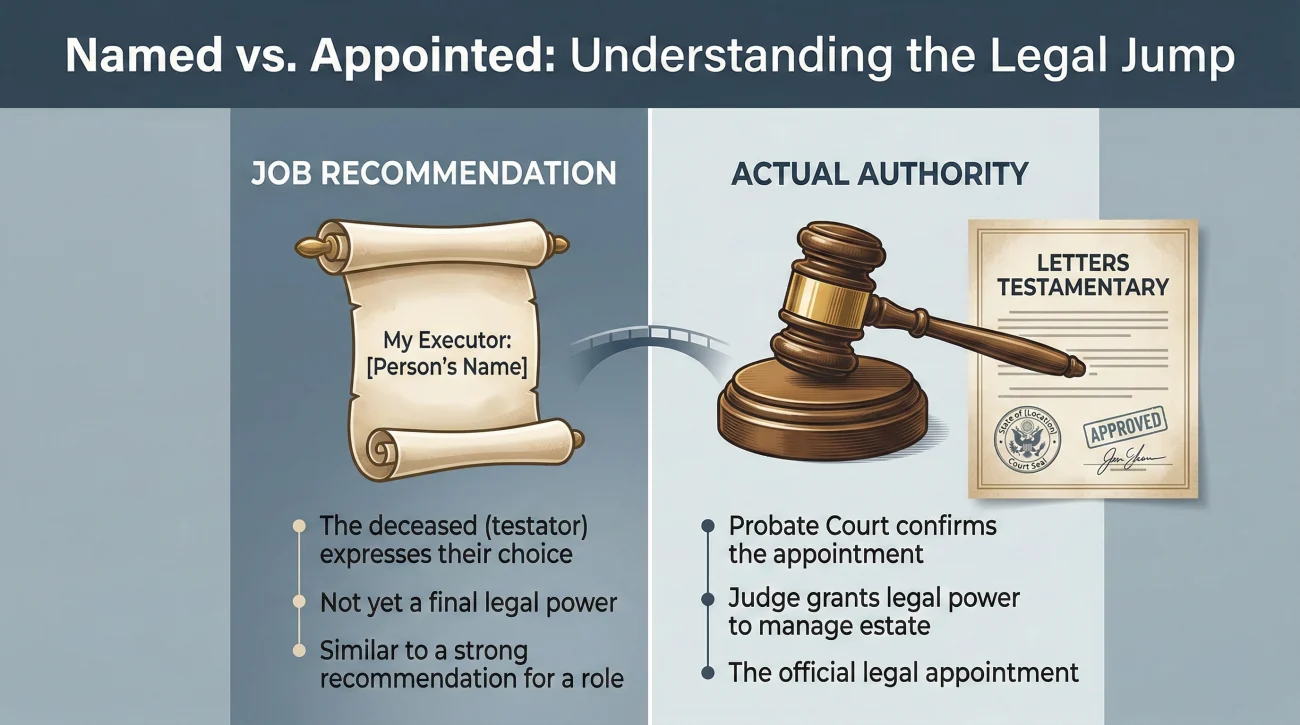

The Difference Between “Named” and “Appointed”

This brings us to the most common point of confusion in estate administration. There is a massive operational difference between being named as an executor and being appointed as one.

Key Point: Being named in a will is simply a nomination. Being appointed by a court is what actually grants you the legal power to act.

Think of the will as a job recommendation. The deceased person highly recommended you for the job. However, until the local probate court reviews that recommendation, verifies the will, and officially gives you the job, you do not have the authority to manage the estate. So, if the will does not work, what does?

The Role of Court Appointment and the Typical Timeline

You have to apply for the position through your local probate court. This process results in the official document banks are waiting for, commonly called Letters Testamentary.

What does this actually look like in practice? While local court rules vary, a practical timeline usually follows this path:

- 1️⃣ Notify: Inform the bank of the passing to secure the accounts.

- 2️⃣ File: Submit the original will and death certificate to the probate court.

- 3️⃣ Review: The court reviews the documents to ensure the will is legally valid.

- 4️⃣ Appoint: The court officially appoints you and issues the stamped Letters Testamentary.

- 5️⃣ Return: You take these official Letters back to the bank to unlock access.

I often get asked about the reverse situation: What if there is no will at all? If someone passes away without a will, the process is very similar. The court will simply issue a document called Letters of Administration instead, which serves the exact same purpose for the bank.

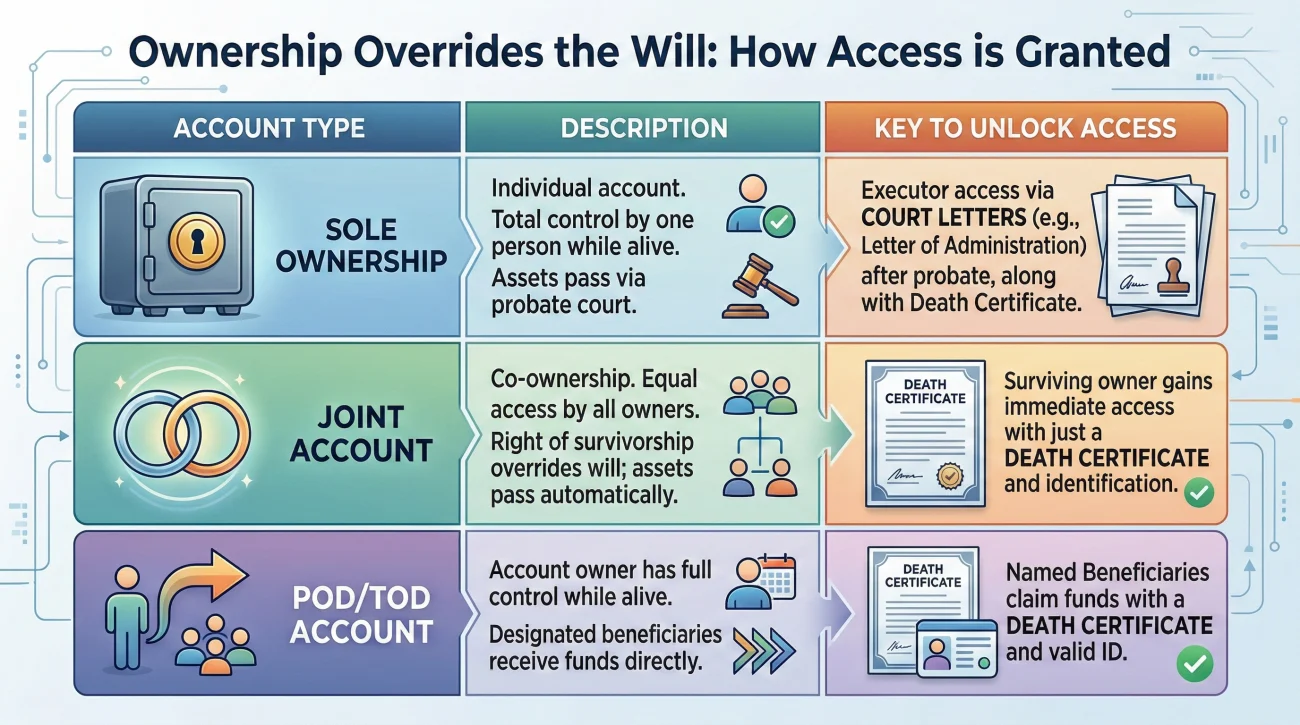

Account Types That Change Everything

Before you start fighting for probate authority for bank access, you must identify the account type. Sometimes the will and the court letters do not matter at all because the ownership structure of the account overrides them.

| Account Ownership Type | Typical Bank Requirement After Death |

|---|---|

| Sole Ownership (No Beneficiaries) | Usually frozen. Requires court appointment (Letters) or a small estate process to access. |

| Joint Account with Rights of Survivorship | Often transfers directly to the surviving owner. Usually just requires a certified death certificate. |

| Payable on Death (POD) / Transfer on Death (TOD) | Transfers directly to the named beneficiary. Usually requires the beneficiary’s ID and a certified death certificate. |

⚠️ Warning: If an account is Joint or POD, the bank usually will not care what the will says, and they will only deal with the surviving joint owner or the named beneficiary.

The Small Estate Alternative

If you are dealing with solely owned accounts, there is one more thing to check before committing to the full court process. Many jurisdictions offer a simplified option, often called a Small Estate Affidavit, for estates that fall below a certain dollar value.

If the estate qualifies, this process allows you to bypass formal court hearings. You typically fill out a sworn statement, have it notarized, and present it directly to the bank along with the death certificate. Your attorney or the local court clerk can tell you if this simplified path is an option in your area.

What “Next Proof” Usually Looks Like

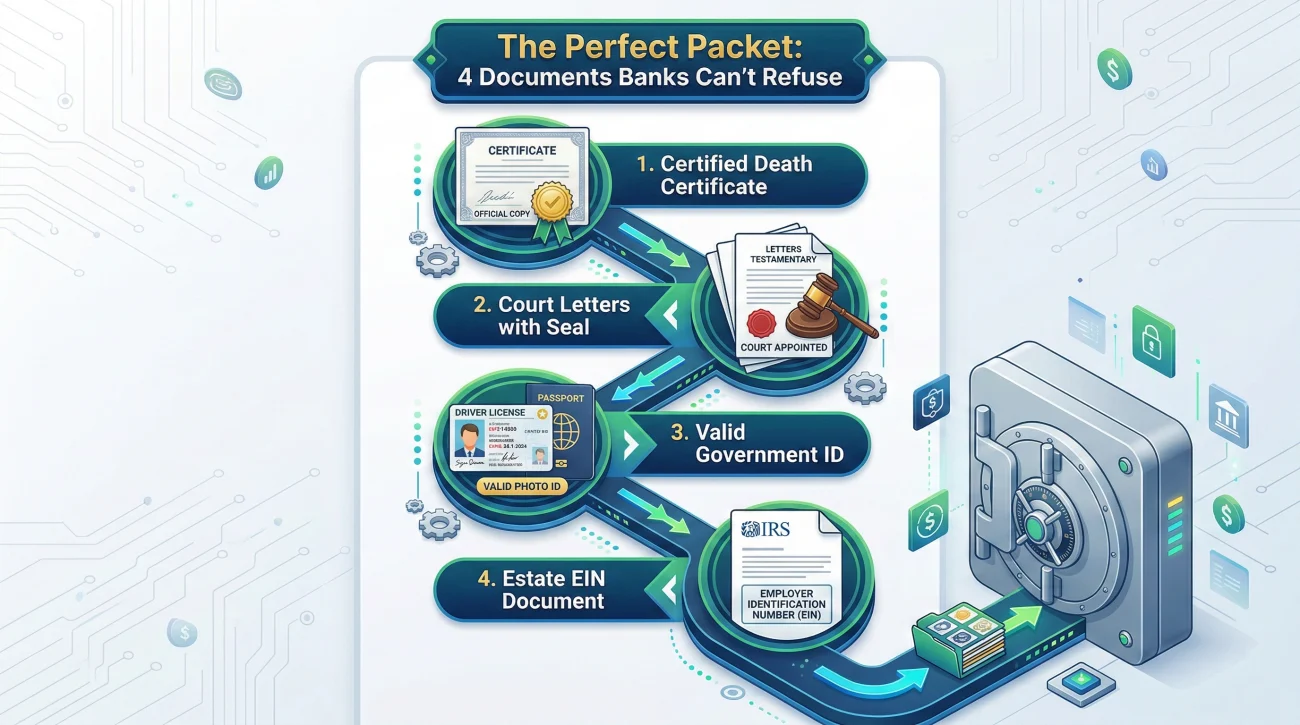

Preparation makes a massive difference here. I recently saw two very different outcomes. One executor was stuck in a three-month loop of branch visits because they kept bringing the will and hoping for a different answer. Another executor handled a nearly identical estate but secured full access in just three weeks because they waited to get their official Letters and walked into the bank with a perfectly organized packet.

When you are ready to go back to the bank, a common, highly effective packet to gain access typically includes the following core components:

- 📄 A certified copy of the death certificate.

- ✅ An original, officially sealed copy of the court appointment document (like Letters Testamentary).

- ✅ Your current, valid, unexpired government-issued identification.

- ✅ The estate’s Employer Identification Number (EIN), which is often required before they will open a new estate account or move funds.

Note: If you are unsure about the EIN, see our FAQ below for a quick guide on how to obtain one.

How to Avoid Escalation Drama

One of the most common mistakes I see is executors getting into heated arguments with branch staff. The teller does not make the legal rules, and the branch manager is bound by the policies set by their legal department. Pushing too hard may simply cause the bank to flag the account as contentious.

Through trial and error, I’ve learned that you need to gently pivot the conversation. The goal is to force the bank to give you their exact, legally approved requirements in writing. This prevents the terrible missing document loop where they seem to ask for just one new thing every single time you visit.

When a representative pushes back on the will, I use a very specific, neutral response that shifts the burden of proof directly back to the institution:

“I understand the will is not sufficient for your verification process. To ensure I don’t waste your time or mine on the next visit, can you please provide me with a written, itemized list of the exact documents your legal department requires to grant executor access to these specific accounts?”

If you are communicating with a bank’s back-office estate department via email or a secure portal rather than speaking to a teller in person, you have to be even more deliberate. I rely on a structured communication formula to keep the message strictly focused on next steps.

[Action] + [What you need in writing] + [Confirmation request]

Here is how I typically map that formula into a real message. Notice how it acknowledges their rule while demanding clarity in return:

Hello,

I am the named executor for the estate of [Name]. I understand you cannot grant account access based solely on the last will and testament.

Please provide a comprehensive, written list of all legal documents and forms your institution requires to formally recognize my authority.

Kindly confirm receipt of this request and let me know the standard processing time for your reply.

Final Note: Dealing with Multiple Banks

If the deceased person had accounts at three or four different financial institutions, be prepared for three or four completely different internal processes. One bank might accept a digital scan of your Letters, while another might demand to hold the physical, sealed copy in their hands.

To keep your sanity, never hand over your only original copy of a court document. Request multiple certified copies from the court upfront. Treat each bank as a separate project, log every conversation individually, and always remember to politely ask for their specific requirements in writing.

💡 Pro Tip: Stop relying on verbal answers from bank tellers. Every time you interact with a financial institution regarding an estate, log the date, the person you spoke with, and ask for their instructions in writing. This habit alone will save you countless hours of frustration.

❓ FAQ

🗣️ Why is the bank refusing to look at the will?

Banks usually refuse to act on a will because they cannot independently verify if it is the final, valid version. They wait for an official court document to protect themselves from liability.

📞 Will the bank contact the probate court directly to verify my will?

No. The bank will not initiate contact with the court or do the research for you. The entire burden is on you to obtain the correct court documents and present them to the branch.

⏳ How long does it take to get the paperwork the bank wants?

The timeline varies wildly. Obtaining court appointment documents can take anywhere from a few weeks to several months, depending entirely on the local court’s current backlog and processes.

📄 What document overrides a will at the bank?

For account access, official court documents like Letters Testamentary override a will. Additionally, the account’s ownership structure, like Joint survivorship or Payable on Death (POD) designations, will completely bypass the will.

💳 Can I use the deceased’s debit card to pay their funeral bill if I have the will?

Using a deceased person’s debit card or online login is widely considered improper and can trigger fraud alerts, freezing the account completely. It is always safer to pay from your own funds and seek proper reimbursement later once the estate is open.

🛑 Why did the bank freeze the account when I showed them the will?

The moment a bank is notified of a death, their policy is usually to freeze solely owned accounts immediately to prevent unauthorized withdrawals until formal court authority is established.

📝 Do I need to leave the original will with the bank?

You should never leave the original, single copy of a will with a bank branch. The bank typically only needs to see court appointment documents, and if they do need the will, they should make a copy and return the original to you.

🤝 Does a joint account holder need to show the will?

In most cases, no. If the account is a true Joint account with rights of survivorship, the surviving owner usually only needs to present a certified death certificate to update the account, completely bypassing the will and the estate.

🏢 Who do I talk to at the bank if the branch manager says no?

If the branch manager rejects your paperwork, ask to be connected to the bank’s specialized “Estate Department” or “Bereavement Services” team. They are typically better trained in exact document requirements than front-line branch staff.

🗂️ How do I get an EIN for the estate bank account?

You can usually apply for an Employer Identification Number (EIN) for the estate for free directly through the official IRS website. Many banks require this tax ID before they will open a new estate checking account.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.