- The will alone rarely unlocks bank accounts; banks rely on formal court authority to release funds.

- Executor access bank accounts before probate usually only happens if the account has a surviving joint owner or a named beneficiary (POD/TOD).

- For sole-owned accounts, your main job before probate is securing the account rather than withdrawing money.

- We recommend organizing a specific “first visit” packet to stop automatic payments and gather balances without forcing immediate withdrawals.

Navigating the “Can I Do This Yet?” Phase of Banking

I often see families walking into a bank lobby holding a pristine, original will, fully expecting that document to act as a key. They walk up to the teller, present the will and the death certificate, and ask to pay for the funeral or cover the deceased’s utility bills. Almost universally, the bank politely declines.

If you are in this exact situation, feeling frustrated and wondering about executor access bank accounts before probate, you are not alone. In my day-to-day work helping people organize estate paperwork, this is one of the most common early roadblocks. You know you are the named executor. The will clearly states it. So why is the bank treating you like a stranger?

The short answer is that a will is a list of wishes, not a legal shield for the bank. Before probate begins, your ability to access or manage an account depends entirely on how the account is structured. Today, I want to walk you through the practical reality of what banks typically look for, what you can actually do right now, and how to keep your records clean while you wait for official authority.

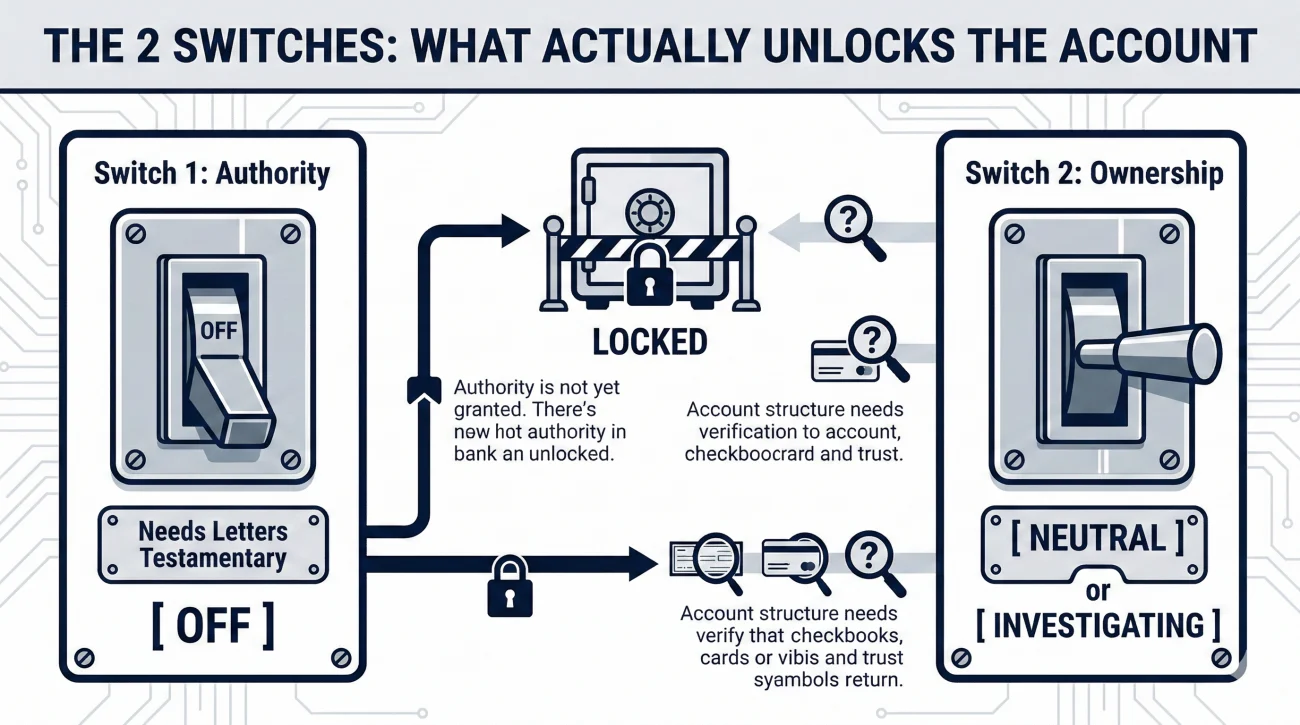

The Two Invisible Switches Banks Check

When you sit across from a bank manager, they are not interpreting the fairness of the will. They are looking at their computer screen for two specific “switches” to be flipped. If neither switch is flipped, their system simply will not allow them to grant you access.

Switch 1: The Authority Switch

Banks are highly risk-averse institutions. Because a will can theoretically be challenged or replaced by a newer version, they wait for a judge to validate it. They need formal court documents (often called Letters Testamentary or Letters of Administration) to flip this switch. Before probate, this switch is firmly in the “off” position.

Switch 2: The Ownership Switch

This is the switch that sometimes allows money to move before probate. The bank looks at the account title. The ownership type dictates everything about your next steps.

| Account Type | What The Bank Sees | Typical Pre-Probate Access |

|---|---|---|

| Sole Ownership (No Beneficiaries) | Only the deceased has rights. | Locked. Requires court authority. |

| Joint Ownership | Both people fully own the funds. | Surviving owner usually retains full access. |

| Payable on Death (POD) | Funds transfer directly outside the will. | Beneficiary can claim funds with ID and death certificate. |

A Real-World Scenario: Dealing with Mixed Accounts

It is incredibly common to face a mix of account types. Last month, I reviewed a file where an executor was completely overwhelmed by medical bills. The deceased had a joint checking account with their spouse, a sole-owned savings account, and a CD with a named POD beneficiary. The executor was trying to unlock them all at once and hitting a brick wall.

I helped them map out a phased approach. First, the surviving spouse continued using the joint checking account to pay the immediate utility bills. Next, the POD beneficiary walked into the branch with their ID and a certified death certificate, claiming the CD funds within a few days. That left only the sole-owned savings account frozen. By separating the pile, the executor realized they had enough bridge funds to survive the probate wait time without panicking about the frozen savings account.

Sole-Owned Accounts: Shifting Your Immediate Goal

If the checking or savings account was owned solely by the person who passed away, that account is effectively frozen the moment the bank learns of the death. I remember mapping out a document trail for a family holding a stack of final invoices, but because the account was sole-owned, the bank could not release a single dollar.

When you are dealing with a sole-owned account before probate, your goal must shift. You are no longer trying to withdraw money. Your goal is to notify the bank, secure the funds, and get a clear picture of the balance for your initial inventory.

Subject: Request for account securing requirements

Hello [Bank Representative Name],

I am the named executor for the estate of [Deceased Name]. We are preparing to file for probate, but I need to notify the bank of their passing today.

I have a certified copy of the death certificate. Can you please provide a written checklist of the steps required to secure the account and stop any outgoing automatic payments while we wait for court appointment?

Thank you,

[Your Name]

This approach works beautifully because it shows the bank you understand their rules. You are asking for their written procedure to protect the account rather than arguing for access they cannot legally give.

Joint and POD Accounts: What Actually Happens at the Branch

If you discover a joint account or a Payable on Death (POD) designation, the process is usually much smoother. From the bank’s perspective, these funds bypass the probate process entirely.

In practice, claiming a POD account is a direct transaction between the beneficiary and the bank. When I prepare someone for this, I tell them to expect to fill out a specific bank claim form. They will need to present their personal identification and a certified copy of the death certificate. The bank reviews the documents, confirms the identity matches the POD form on file, and typically transfers the funds to the beneficiary’s chosen account within a few business days.

Believing the executor must collect and manage all POD funds to distribute them according to the will.

Understanding that POD funds are claimed directly by the beneficiary, bypassing the executor’s control completely.

Small-Estate Routes: Why Thresholds Are Tricky

I occasionally sit with clients who realize the only asset left is a single checking account with $12,000 in it. Going through full, formal probate for that amount feels incredibly counterproductive. This is where a workaround called a “small estate affidavit” (or similar simplified procedure) comes in.

If the estate qualifies, the bank may accept a specific, notarized state form instead of formal court letters, allowing access much faster. However, there is a major trap here.

Families often see a small checking balance and assume they qualify because the local threshold might be set at $50,000 or $100,000. But that limit typically applies to the total value of all estate assets combined, not just the bank balance. If they also owned a house or vehicles, you are likely over the limit. Always confirm your jurisdiction’s specific rules on what counts toward that threshold before assuming you can skip probate.

What to Bring to the Bank on Your First Visit

Even though you cannot withdraw money from a sole-owned account, your first visit to the branch is crucial for stopping fraud and gathering information. I recommend building a specific “first visit” packet before you walk in the door.

- 📄 Multiple Certified Death Certificates: Bring originals. The bank will often scan them and return them to you, but some institutions require keeping one on file.

- 📄 Your Personal ID: A valid driver’s license or passport.

- 📄 The Original Will: Even though it does not grant you access yet, many banks ask to scan a copy into their system to note who the likely executor will be.

- 📄 Account Numbers: Bring any recent statements, debit cards, or checkbooks you found to help the banker locate all associated profiles.

For a complete breakdown of what banks will ask for later in the process, review our executor bank documents checklist.

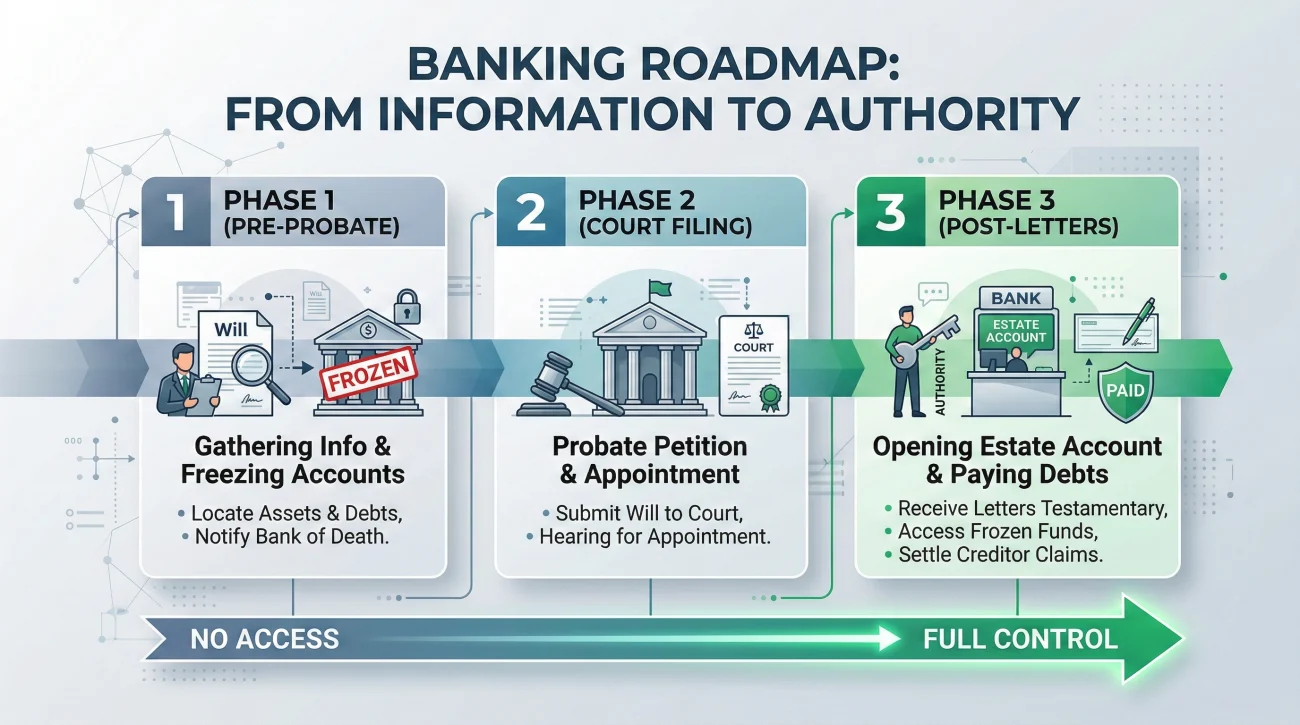

The Timeline: What You Can Do Now vs. Later

I always tell my clients that the waiting period feels much less overwhelming when you can see the entire roadmap. Here is how your ability to act will likely evolve over the coming weeks.

Immediately (Before Probate)

Right now, your main job is simply gathering information. By logging the death certificate, you freeze the accounts and stop the outgoing payments. You can usually request a “date of death balance,” which you will need to prepare your initial court petition.

Later (After Court Appointment)

Once your petition is approved and a judge formally issues your Letters Testamentary, the landscape changes entirely. You will return to the bank with those official documents and an Estate EIN. At that stage, you finally gain the authority to open a dedicated estate account, transfer the frozen funds into it, and begin paying the deceased’s outstanding debts safely.

When to Consider Hiring an Estate Attorney

I firmly believe that an organized executor can handle many administrative tasks without paying hourly legal fees. However, banking roadblocks can occasionally signal complex underlying issues. I suggest pausing and consulting an estate professional if you hit any of these friction points:

- ✅ You cannot determine if the total assets fall under the small estate threshold.

- ✅ There is a dispute among family members about who should be listed on the account.

- ✅ The bank informs you that the POD beneficiary named on the account is also deceased.

- ✅ The deceased held business accounts that are suddenly frozen, halting payroll or operations.

An attorney provides more than just legal interpretation; they add a layer of formal leverage that can escalate requests effectively when your standard communications with the local branch manager stall.

Common Myths and Risky Assumptions Before Probate

When bills are piling up, the pressure to act can lead to terrible decisions. One of the most common mistakes I see involves well-meaning family members trying to bypass the bank’s normal procedures because they have the deceased’s online banking password or ATM PIN.

The temptation to just log in and pay the electric bill is incredibly high. I strongly advise against this under any circumstances.

Key Point: Logging into an account pretending to be the deceased obscures the financial records and violates the bank’s terms of service. If beneficiaries ever question where money went, your defense is severely compromised because you operated outside the legal audit trail.

If you decide you absolutely must pay an urgent bill out of your own pocket to prevent a shutoff, keep meticulous records. Save every receipt and document exactly what you paid for so you can formally request reimbursement from the estate once the estate account is open.

Final Thoughts: Looking Ahead to the Next Milestone

The gap between reading the will and actually holding court authority is often the most stressful phase of the entire executor process. You feel a heavy responsibility, yet you have no real power at the teller window. Accept the bank’s freeze for what it is: a protective pause, not a personal rejection.

Your goal today is not to force the vault open, but to map the landscape. Once you have notified the bank and stopped the automatic payments, you have successfully completed the banking tasks for this phase. Your next major milestone is not at the bank at all. It is time to shift your focus to the court, file your probate petition, and secure the official appointment that will eventually unlock those frozen accounts.

⚠️ Boundaries Note: I am sharing operational workflows based on standard banking practices. This guide is not legal or tax advice. Always verify requirements with your specific financial institution or local court system.

❓ FAQ

🏦 What if the deceased had accounts at multiple banks?

You will need to notify each institution separately. Banks do not automatically share this information. Gather a certified death certificate for each bank, as their procedures and timelines for freezing accounts will operate independently.

⏳ Can the executor be held personally liable if they wait too long to begin probate?

Potentially, yes. If unnecessary delays cause harm to the estate (like letting a house go into foreclosure or ignoring accumulating penalties), beneficiaries or creditors could claim the executor breached their fiduciary duty. Check local timelines for filing the will.

👻 What happens if the named POD beneficiary is also deceased?

If the primary POD beneficiary passes away before the account owner and no alternate beneficiary was named, the funds typically revert back to the general estate. At that point, the account will require formal probate authority to access.

💼 Do I need to bring the original will or just a copy to the bank?

Bring the original will on your first visit, but expect to take it back home. Banks often prefer to review or scan the original to verify the named executor, but the court is the entity that ultimately keeps the original document during probate.

🛑 Can the bank force me to use the funds to pay their specific credit card debt?

If the deceased had a credit card and a checking account at the same bank, the bank may have a “right of setoff” allowing them to use the funds to clear the debt. This varies heavily by bank policy and state law, which is why securing the account quickly is vital.

📜 Will the bank automatically notify the probate court about the account balances?

No. The bank does not report directly to the court. It is your responsibility as the executor to gather the date-of-death balances from the bank and include them in the official inventory you file with the probate court.

👥 If I am a joint owner, do I still need to show the bank a death certificate?

Yes. Even though you retain access to the money, you still need to provide a certified death certificate so the bank can officially remove the deceased person’s name and social security number from the account profile.

💸 How do I handle incoming checks made out to the deceased person right now?

Keep them in a secure folder. Do not try to endorse them yourself or deposit them into your personal account. Once you receive your court letters, you will open an estate account where those checks can be safely deposited.

🏛️ What happens if the bank account was held in a living trust?

If the account is titled in the name of a trust, it generally bypasses probate. The successor trustee named in the trust document will handle the account according to the trust’s instructions, completely separate from the executor’s timeline.

📝 Can the bank give me legal advice on which probate path to choose?

No. Bank employees are strictly prohibited from giving legal advice. They can tell you what their specific institution requires to release funds, but they cannot tell you whether a small estate affidavit or full probate is legally appropriate for your situation.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.