- An estate bank account is a temporary financial hub used to collect the deceased person’s assets and pay their final bills.

- It creates a clear, clean boundary between your personal money and the estate’s money, which is critical for your own protection.

- You typically need one if you are receiving checks made payable to the “Estate of” the deceased, or if you are selling physical assets like a house or a car.

- If all assets passed directly to beneficiaries through joint ownership or Payable-on-Death (POD) designations, an estate account may be less necessary.

- Opening this account requires specific documentation, usually including a tax ID number (EIN) and proof of your court appointment.

That Moment the Old Account Stops Working

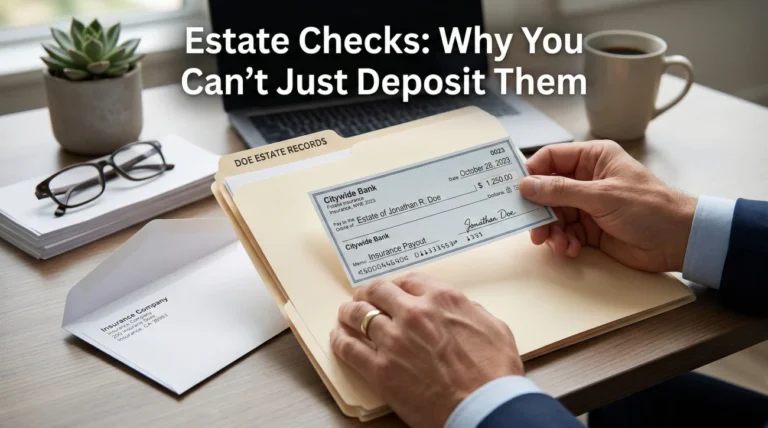

When I talk to people who have just stepped into the role of executor, there is almost always a specific moment when the reality of the banking process hits them. It usually happens in the first few weeks. You open the mail and find a refund check from the deceased person’s utility company. Or perhaps a check from a closed insurance policy arrives. You look at the payee line, and it does not say the person’s name. It says: “Pay to the order of the Estate of [Name].”

In a normal week, you would just endorse the check and deposit it via an app on your phone. But as an executor, if you try to deposit that check into your personal checking account, the bank will almost certainly reject it. If you try to deposit it into the deceased person’s old checking account, you will likely find that the account has been frozen following the notification of their passing.

This is exactly the moment when people start asking: do you need an estate bank account? Is it a strict requirement, or just an optional organizational tool?

In my experience helping families organize their administration paperwork, the answer is rarely about strict legal requirements right out of the gate. Instead, it is about practical friction. You need a place to put the money that belongs to the estate, and you need a way to pay the bills that the estate owes. An estate checking account solves both of these problems while building a protective wall around your personal finances.

Let us walk through how these accounts actually work in the real world, the signs that indicate you probably need to open one, and how it changes your day-to-day workflow as you settle the estate.

The Core Purpose: Separation and Auditability

Before we look at the decision map, it helps to understand what an executor estate account actually is. In simple terms, it is a brand-new checking or savings account opened in the name of the estate, not in your personal name, and not in the deceased person’s name alone.

The core purpose of this account is to serve as a temporary financial funnel. Think of it like a secure transit hub. Money from a life insurance policy or a house sale arrives on one track, and payments for final property taxes or medical bills depart from another. The account itself is just the station managing the traffic; it does not permanently own the funds.

Key Point: An estate account is essentially a liability shield. It proves objectively to the court, the IRS, and the family that you never once used your position to benefit your personal finances.

In my day-to-day work guiding executors through this paperwork, I see how crucial this audit trail becomes. When you are the executor, you are managing money that does not belong to you. Eventually, you will have to show your work. Beneficiaries will want to know how much money was in the estate and what it was spent on. In many cases, a court will require a formal accounting.

If all the estate’s transactions happen inside one dedicated checking account, generating that report is incredibly straightforward. You just look at the bank statements. Every deposit is an estate asset collected. Every withdrawal is an estate expense paid. The math proves itself.

A Common Point of Friction

One pattern I often see is an executor trying to avoid the “hassle” of opening a new account because the estate seems small. They think, “I will just keep track of it in a notebook.” Six months later, someone asks a question about a specific utility payment from four months ago. The executor has to dig through their personal bank statements, find the charge, and try to remember if that specific $45 was for their own water bill or the deceased person’s empty house.

An estate checking account eliminates this memory game entirely. If the transaction is on the estate bank statement, it was an estate expense. If it is not, it was not.

Decision Map: When It Is Usually Worth Opening One

So, how do you know if you are in a situation that requires this step? While every situation is unique, there are very common triggers that tell you it is time to schedule an appointment at the bank.

You will likely find that you need an estate bank account if you encounter any of the following scenarios:

- 📄 You receive checks payable to the estate. As we saw in the opening scenario, if a refund or payout is made out to the “Estate of” the deceased, a dedicated estate account is practically the only place a banking institution will allow you to deposit it.

- ✅ You are selling physical property. If the estate includes a house, a vehicle, or valuable personal property that you are selling, the proceeds from those sales belong to the estate. The title company or buyer will need a safe, official place to wire those funds.

- 📄 There are ongoing bills to pay. If you need to keep the lights on at a property, pay property taxes, or cover storage unit fees while you sort through belongings, you need a mechanism to pay those bills. You could write checks from the estate account, keeping the paper trail perfectly clean.

- ✅ You are consolidating multiple scattered accounts. Often, a person dies with money spread across a checking account, a savings account at a different bank, and perhaps a small credit union account. Moving all those separate balances into one central estate checking account makes tracking infinitely easier.

💡 Pro Tip: If you are unsure whether you will need an account, it is often safer to open one early. Having an empty estate account ready to go is much less stressful than receiving a large check and having to wait two weeks for the bank and court paperwork to clear before you can secure the funds.

When It May Be Less Necessary

It is important to note that not every single situation requires this administrative step. There are times when opening a new account might actually just be extra paperwork.

For example, if the deceased person held all their accounts jointly with a surviving spouse, the surviving spouse typically becomes the sole owner of those accounts immediately upon death. There is no “estate money” to separate, because the money legally belongs to the survivor.

Similarly, if every single asset had a clear Payable-on-Death (POD) or Transfer-on-Death (TOD) beneficiary designated, those assets usually bypass the estate entirely. The bank distributes the funds directly to the named people. In these cases, where no assets are flowing through the executor’s hands, an estate account may not be needed.

The Trap of Commingling: Why Mixing Funds Causes Trouble

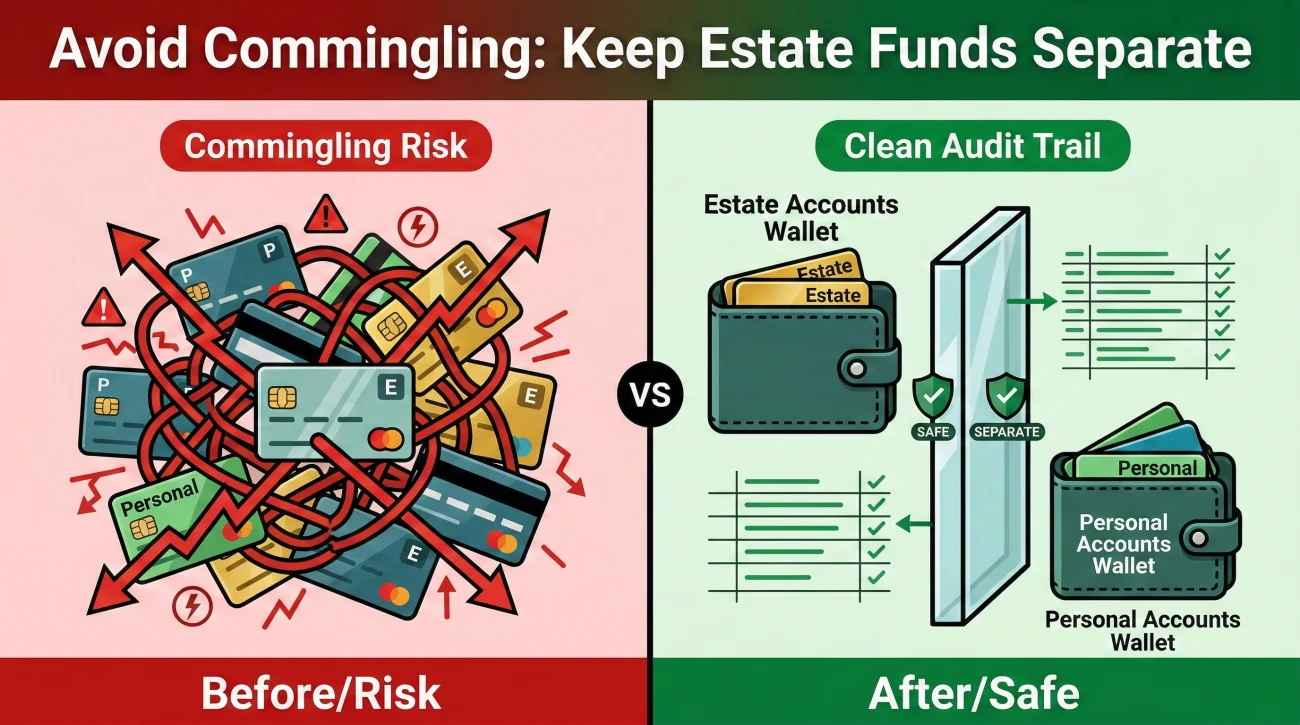

If there is one operational rule I try to emphasize to anyone acting as an executor, it is this: keep estate funds separate. The technical term for mixing your personal money with the estate’s money is “commingling,” and it is one of the fastest ways to turn a smooth process into a deeply stressful one.

The temptation to commingle is incredibly human. You are at the hardware store buying trash bags and cleaning supplies to clear out the deceased person’s apartment. You are in a hurry, so you just swipe your personal debit card, telling yourself you will transfer some estate money later to pay yourself back.

While this seems harmless, these small actions destroy the integrity of your audit trail. When you commingle estate money, you blur the lines of ownership. If a beneficiary later questions a financial decision, or if a creditor asks for proof that the estate is insolvent, a commingled record looks messy and, in the worst cases, suspicious.

Swiping your personal card at the hardware store, writing yourself a reimbursement check from the estate later, and hoping you don’t lose the crumpled paper receipt to prove why you took the money.

Swiping the estate account’s debit card directly at the hardware store. The transaction automatically appears on the estate bank statement with the vendor’s name and exact date.

How Separation Protects You From Liability

To truly understand why we avoid mixing funds, look at the difference in your liability level when someone eventually asks to review your work.

| When Questioned By: | Using Personal/Mixed Accounts | Using a Dedicated Estate Account |

|---|---|---|

| A skeptical beneficiary | You have to show personal bank statements and redact your private grocery trips to prove an estate expense. | You hand over a clean estate bank statement. There are no personal transactions visible. |

| The Probate Court | The judge may require complex forensic accounting to untangle what belongs to whom. | The beginning balance, minus expenses, perfectly matches the final distribution amount. |

Recognizing this risk is usually what prompts people to finally schedule a trip to the branch. But getting the account open requires preparation.

Before You Head to the Bank: A High-Level Prep List

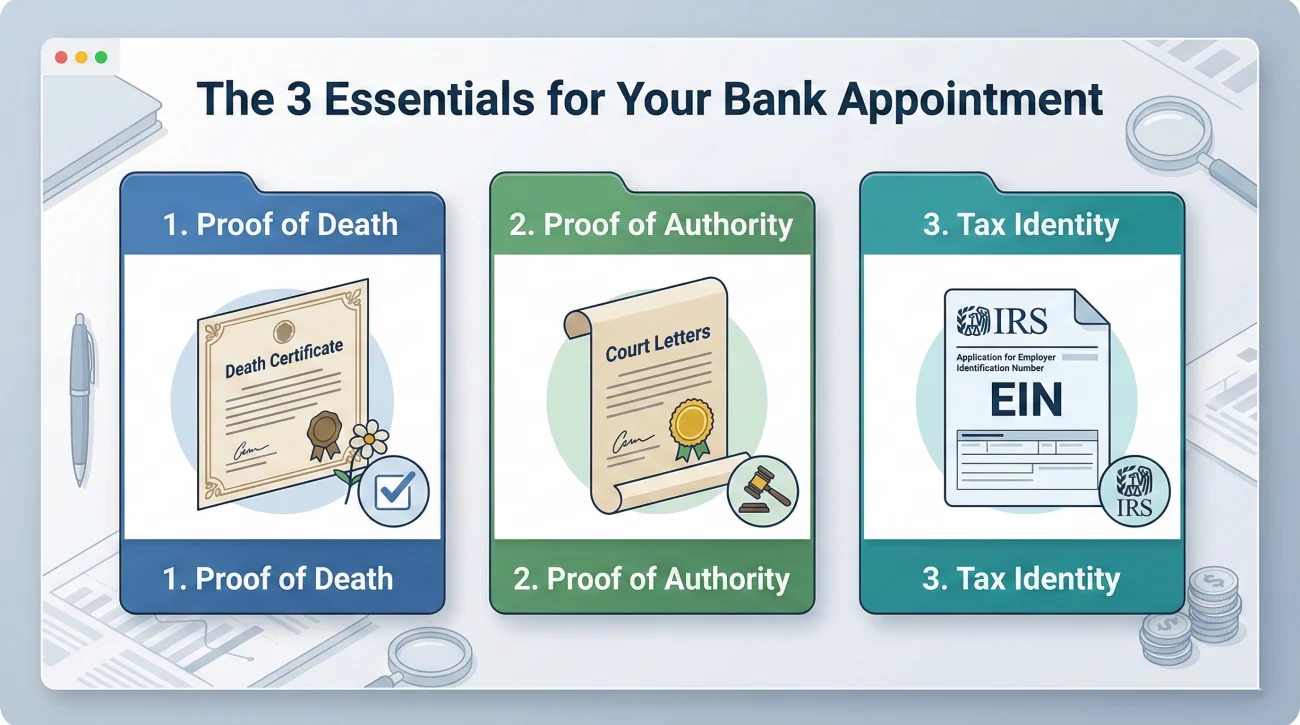

If you have looked at your situation and decided that an estate account is the right path, you cannot simply walk into a branch and ask them to open one based on your word. Banks are heavily regulated, and they need specific proof of your identity, your authority, and the estate’s tax status.

While we won’t go into the granular details of every document here, you should conceptually prepare to gather three main things:

- Proof of Death: Usually a certified copy of the death certificate.

- Proof of Authority: The official court document naming you as the executor or administrator (often called Letters Testamentary or Letters of Administration). A will alone is typically not enough to open an account.

- Tax Identity: An estate is treated as a separate entity for tax purposes. You will almost always need to obtain an Employer Identification Number (EIN) from the IRS for the estate. The bank will use this number, rather than the deceased’s Social Security Number, to open the account.

<strong⚠️ Warning: Never assume the branch manager is available for this specific task. Opening an estate account takes time and often requires someone familiar with the institution’s bereavement protocols. Always call ahead and make an appointment specifically to “open an estate account.”

💡 Pro Tip: When you call to make that appointment, explicitly ask if they charge monthly maintenance fees for estate accounts. Not all banks are created equal here. Some community banks or credit unions offer much better fee structures for these temporary accounts than massive national chains.

If you are ready to take action, your next step should be to look deeply into the specific paperwork. Go to our guide on “Opening an Estate Bank Account: What Banks Commonly Ask For” to build your actual document packet.

How Your Daily Workflow Changes

Once you have successfully navigated the branch visit and opened the account, your daily administrative life changes significantly. The initial stress of “where do I put this?” disappears.

When mail arrives containing invoices for medical bills or property taxes, you no longer have to worry about how to front the cash. You simply open your executor folder, pull out the estate checkbook (or use the estate’s online bill pay), and settle the debt directly from the estate’s funds.

This is also a great time to establish clear communication hygiene with the beneficiaries. When you open the account, it is often helpful to send a brief, neutral update so everyone knows the administration process is moving forward smoothly in a structured way.

Here is an example of a simple, copy-paste safe script you might use in an email update:

Subject: Estate Update – Banking established

Hello everyone,

I wanted to provide a quick update on the administration process. I have successfully opened the dedicated estate bank account this week.

Going forward, all incoming funds (such as refunds or asset sales) will be deposited directly into this account, and all final bills and expenses will be paid from it. This ensures we have a perfectly clean paper trail for the final accounting.

I am currently in the process of gathering the outstanding final invoices. I will send another update when we move to the next phase.

Best regards,

[Your Name]

A message like this does not make promises about money, but it heavily reassures the readers that you are acting carefully and treating the funds with respect.

If you are trying to understand the full landscape of banking as an executor, including what happens to different types of accounts, I highly recommend reviewing our core guide on the executor banking checklist. It provides the broad map you need before diving into specific tasks.

The Finish Line: When Does the Account Close?

A common question I hear after helping someone set this up is: “How long am I stuck managing this?”

It is important to remember that an estate account is not designed to live forever. It stays open during the active probate or administration process, which often lasts anywhere from six months to over a year, depending on the complexity of the assets and local creditor waiting periods.

You keep the account active until every single valid creditor is paid, final tax returns are filed, and the court clears you to distribute the remaining funds. Once you write the final distribution checks to the beneficiaries and the account balance hits zero, you close the account for good. The financial funnel has done its job, and it is dismantled.

Final Thoughts on the Burden of Banking

Stepping into the executor role often feels like being handed a second full-time job while you are still trying to process a personal loss. The sheer volume of mail, decisions, and strict banking rules can be exhausting.

Opening an estate account is one of those early administrative hurdles that feels daunting at first, but ultimately buys you the most valuable thing an executor can have: peace of mind. It takes the financial pressure off your personal shoulders and stops the constant, nagging worry of “Did I write that down correctly?”

You are doing a difficult, heavy job for your family. Setting up clean, impenetrable boundaries between your money and the estate’s money early on is one of the kindest ways you can take care of yourself while you take care of their legacy.

❓ FAQ

🗂️ Do I have to open an estate account by law?

While there is no “executor police” forcing you to open one on day one, practical reality will force your hand. If the estate receives even a single check made out to the deceased person’s estate, you will need this account to legally cash or deposit it.

⏱️ How long do I have to open an estate account?

There is generally no strict ticking clock for opening the account itself. However, you usually open it as soon as you receive your official court appointment (Letters), because you will need the account to start depositing estate funds and paying ongoing bills without mixing your own money.

💸 Can I just deposit an estate check into my personal account?

Usually, no. Banks have strict fraud prevention policies regarding payee names. If a check is payable to the “Estate of” someone, trying to deposit it into an account that only has your personal name on it will typically result in the check being rejected.

🏦 Can I use the deceased person’s old checking account instead?

Typically, once a bank is notified of a person’s death, sole-owned accounts are frozen to prevent unauthorized withdrawals. You usually cannot continue to use their old account as an ongoing operating account for the estate.

💳 How do I pay estate bills before the account is open?

If urgent bills (like utilities to prevent frozen pipes) must be paid before you have bank access, executors sometimes pay from their personal funds. If you do this, keep meticulous receipts and logs so you can properly reimburse yourself from the estate account later.

🧾 What if there is no money to open the estate account?

Some banks require a minimum deposit to open an account. If the estate has no liquid cash initially, an executor may front the minimum deposit from personal funds, keeping clear documentation to ensure they are reimbursed once physical assets (like a house) are sold.

👥 Can there be two signers on an estate checking account?

Yes. If the court appointed two people as co-executors, banks will commonly require both names on the account. Depending on the bank’s policy, they may require both signatures on checks, or allow either person to sign independently.

📱 Do estate accounts have debit cards or online banking?

This depends entirely on the specific institution’s policies. Many banks do offer online access and debit cards for estate accounts to make paying final bills easier, but some limit access to paper checks only to maintain a stricter physical paper trail.

🛑 What happens if I make a mistake and pay a personal bill from the estate account?

Mistakes happen. If you accidentally use the estate account for a personal expense, the most common practice is to immediately deposit a personal check back into the estate account for the exact amount, and add a clear note in your timeline log explaining the error and the immediate correction.

🔒 Who can see the transactions in the estate account?

Directly, only the authorized signers (the executors) and the bank. However, indirectly, the beneficiaries and the court will eventually see the transaction history when you provide the final accounting report before closing the estate.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.