- The gap between someone passing away and you gaining official bank access is often the most stressful period for managing bills.

- Do not use the deceased person’s debit cards, checks, or online login credentials to pay bills, even if you know the passwords.

- If you choose to front money for urgent expenses (like property insurance), strict documentation is your only safety net for future reimbursement.

- Communication with creditors is key. Many companies offer temporary bereavement holds if you notify them and ask for requirements in writing.

- Keep all personal funds completely separate from eventual estate funds to avoid accusations of commingling.

The Pressure of Urgent Invoices When Accounts Are Frozen

The mail keeps arriving, the utility bills are due, a property insurance premium is pending, but the deceased person’s bank accounts are entirely frozen. You are stuck in a waiting period, trying to figure out the rules for paying bills as executor without bank access.

It feels incredibly urgent, which often pushes perfectly well-meaning people into making administrative missteps that complicate the entire probate process down the line. This guide will walk you through how to navigate that stressful gap safely. We will look at what people commonly do, what risks you absolutely need to avoid, and how to build a paper trail that protects you.

Why Improvising with the Deceased’s Accounts is a Trap

When faced with a stack of estate bills after death, the most tempting shortcut is to use the tools that are sitting right there on the desk. You might know their iPad password. You might have their debit card and PIN. You might see a stack of pre-signed blank checks.

I cannot stress this enough: using the deceased person’s credentials to pay bills after they have passed is a significant risk. Even if you are the sole beneficiary, and even if you are just paying the electric bill for the house you are inheriting, the financial system views the moment of death as a hard stop for that person’s individual authority.

⚠️ Warning: Logging into a deceased person’s online banking to transfer funds or pay a bill can be flagged by the bank’s security algorithms. This often results in a total lockdown of the profile, making it much harder for you to gather the historical statements you will need later.

Beyond the bank’s security systems, there is the issue of auditability. When the probate court or the beneficiaries eventually review the accounting, they will see transactions occurring after the date of death. If those transactions came directly out of the deceased’s account without official executor authorization, it looks highly suspicious.

In day-to-day admin work, I see this pattern constantly. An executor uses the deceased’s debit card to pay for property repairs “to keep the house safe.” Three months later, a sibling questions the transaction, and the executor has to spend weeks proving it was a legitimate estate expense, rather than a personal cash grab. The intention was pure, but the method destroyed the transparency.

Common “Bridge” Approaches People Discuss

If you cannot use their accounts, and you do not yet have an estate account, how do these bills actually get handled? There are a few common approaches that executors typically utilize during this waiting period.

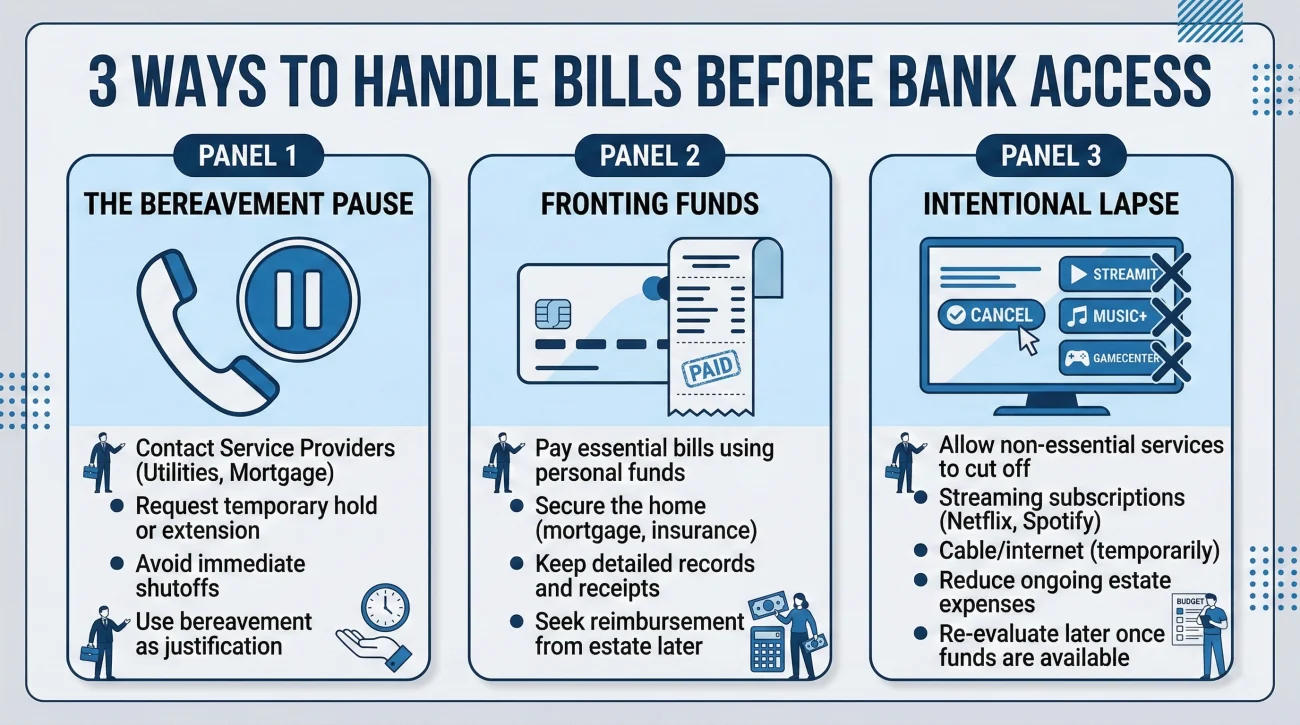

Approach 1: The Bereavement Pause

This is often the safest and most underutilized tool. Many major institutions, such as mortgage lenders, utility providers, and large credit card companies, have protocols for the death of a customer. When you notify them of the death, their first step is usually to freeze the account to prevent fraud. This is actually a massive benefit for you, because while the account is locked down, they will also typically place a temporary hold on collections or late fees. You are essentially asking for grace time while the court processes your appointment.

Approach 2: Fronting the Money (Paying Out of Pocket)

Sometimes, a bill is too critical to pause. The most common example is property insurance. If the deceased owned a home, letting the homeowner’s insurance lapse is a massive risk to the estate’s value. In these scenarios, the executor or a family member will often pay the premium using their own personal funds. This is extremely common, but it is also where the most administrative damage occurs if not documented perfectly.

Approach 3: Letting Non-Essentials Lapse

Part of your job early on is triage. Not everything needs to be saved. If a bill arrives for a premium cable package, a magazine subscription, or a gym membership, the standard practice is to simply notify the vendor of the death and let the service cancel itself for non-payment. You do not need to front your own money to keep their Netflix active. Focus your energy, and potentially your personal funds, only on expenses that preserve the value of the estate, like keeping the heat on in a house to prevent frozen pipes or securing physical property.

Key Point: The period before you have official bank access is about preservation, not clearing the ledger. Your goal is simply to keep the estate safe and stable until you have the authority to manage the money properly.

What If You Are a Joint Account Holder?

A common exception to the “frozen account” rule is a joint checking account. If you and the deceased person were joint owners, that account usually bypasses probate entirely. You typically retain full and immediate access to the funds.

However, this creates a different kind of trap. Because you have access, it is incredibly tempting to just start paying all the deceased person’s individual debts directly out of this account.

I often see a surviving spouse use a joint checking account to pay the deceased’s personal credit card bill just to get it out of the way. While legal, you have to remember that in many cases, the money in that joint account now belongs entirely to you. If you use it to pay estate debts before understanding if the estate actually has enough of its own assets to cover them, you might be giving away your own money unnecessarily. My advice is always to pause. Secure the house, pay the essential utilities, but wait to pay unsecured individual debts until you have a full picture.

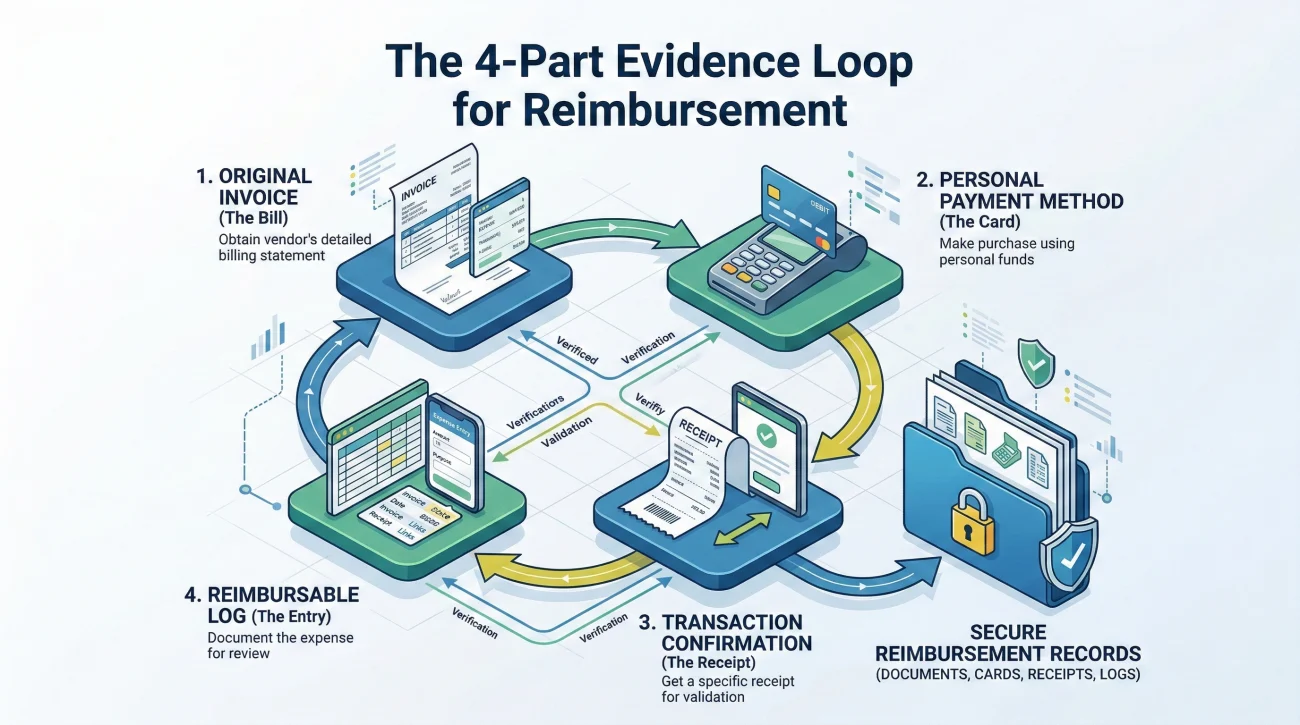

What to Document if You Decide to Front Expenses

If you determine that an expense is critical to preserving the estate, and you decide to pay it using your own money before probate is open, your recordkeeping must be flawless. You are essentially giving a loan to the estate, and you will eventually need to prove to the court (and the beneficiaries) that this loan was valid.

For every single out-of-pocket payment, you need a closed loop of documentation. I recommend building a simple habit using this formula for your files:

[Date Paid] + [Exact Amount] + [Vendor Name] + [Clear Estate Purpose]

Let’s look at a realistic micro-example. Imagine you need to pay a $150 utility bill to keep the electricity on at the deceased’s house. You pay it online using your personal Visa card.

You pay the bill, close the browser, and figure you will just remember it later. Maybe you write “$150 power bill” on a sticky note. Six months later, you reimburse yourself $150 from the estate, but the beneficiaries ask to see the proof. You have to spend hours digging through your personal credit card statements to find the line item, and you have no original invoice to prove it was for the deceased’s house.

You download the actual utility invoice showing the deceased’s address and the amount due. You pay it with your card. You save the confirmation email. You log into your personal banking and print a PDF of that specific transaction. You save all three pieces of paper together in a physical folder labeled “Out of Pocket Reimbursables,” and you log it immediately on a tracking sheet.

To keep this organized, I recommend setting up a simple tracking spreadsheet immediately. Here are the columns I always suggest executors use:

- 📊 Date Paid: When the transaction cleared your personal account.

- 📊 Vendor/Payee: Who received the money.

- 📊 Exact Amount: Down to the penny.

- 📊 Method of Payment: e.g., “Personal Visa ending in 1234”.

- 📊 Estate Purpose: e.g., “Preserve asset: Winterize house”.

- 📊 Receipt Location: e.g., “Blue Folder, Section 2”.

Every time you front money, ask yourself: “If a stranger looked at this piece of paper a year from now, would it be painfully obvious that I paid this for the estate?” If the answer is no, you need better documentation.

Handling Checks and Refunds in the Gap Period

During this waiting period, you will likely receive money in the mail. A utility deposit refund, an insurance premium overpayment, or a final paycheck might arrive, made payable to “The Estate of [Name]” or simply to the deceased person.

I regularly see executors try to deposit a $200 refund check into their own personal checking account via mobile deposit, planning to “just credit the estate later.” Almost every time, the bank flags the mismatch, reverses the deposit, and sometimes freezes the executor’s personal account for suspicious activity.

The rule here is absolute: do not endorse or deposit these checks into your personal account. Keep them safe in your physical document folder. Once the official estate checking account is open, you can deposit them all at once properly.

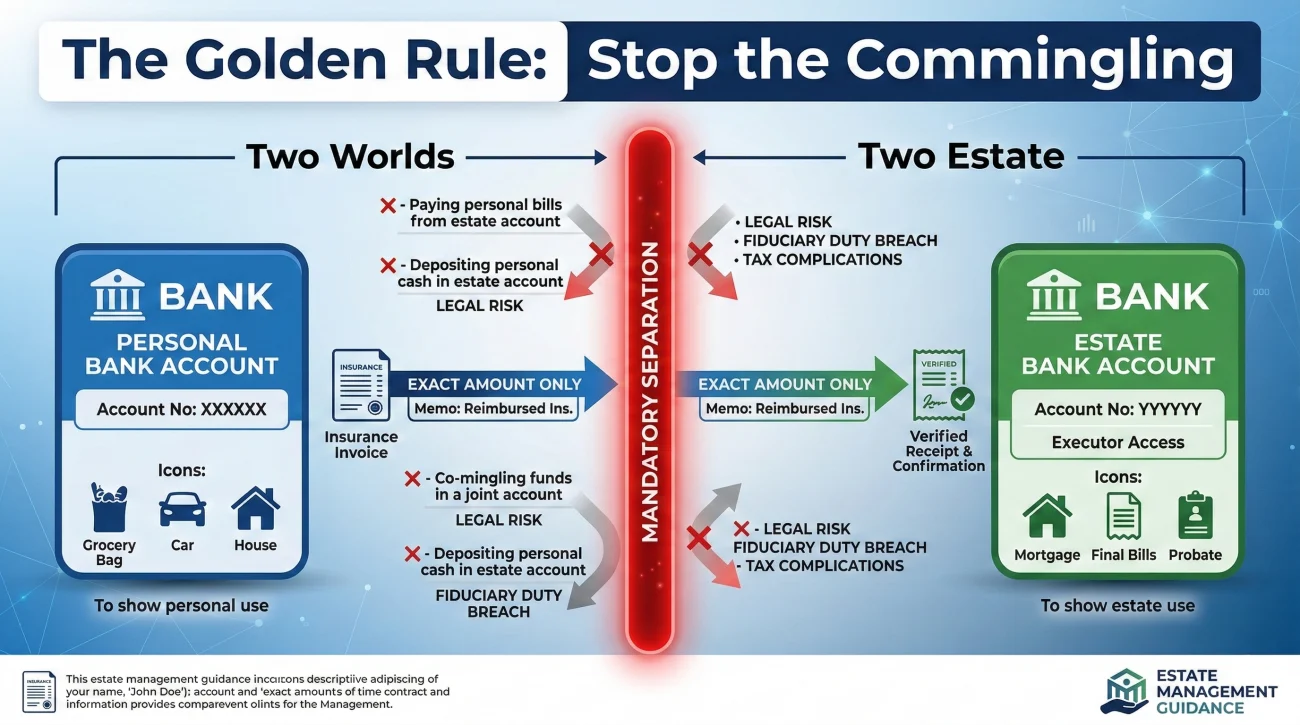

How to Avoid Commingling and Confusion

That temptation to deposit an estate check into your personal account is just one example of a broader issue. In the world of estate administration, “commingling” is a dangerous word. It means mixing estate money with your own personal money. When you eventually receive your court authority, your very next step should be setting up the proper financial structure to keep these worlds entirely separate. I highly recommend reviewing our complete Executor Banking Checklist to understand how estate accounts function.

To avoid commingling when you eventually reimburse yourself, follow these operational rules:

- ✅ Wait for the estate account: Do not try to write a check from the deceased’s old account directly to yourself as reimbursement. I once saw an executor do this because they found a pre-signed blank check; the bank flagged it, and the court demanded a formal hearing to clear the transaction.

- ✅ Use exact amounts: If your tracked out-of-pocket expenses equal $432.18, write yourself a reimbursement check for exactly $432.18. Do not round up to $450 “for your time.” Exact matching amounts make auditing simple and prevent beneficiary disputes.

- ✅ Note the memo line: Always write exactly what the reimbursement is for on the memo line of the check (e.g., “Reimb: Oct-Nov Home Ins”). A blank memo line leaves too much room for future questions.

Once you understand how to keep your own money completely separated from the estate’s money, the next challenge is deciding which bills actually justify pulling out your personal credit card in the first place.

The Types of Expenses That Typically Trigger Questions

Not all bills are created equal. When deciding what to pay out of pocket before you have bank access, it helps to know how beneficiaries and auditors typically view different types of expenses. Some are universally accepted as necessary, while others often invite scrutiny.

| Expense Category | Common Approach Before Probate | Level of Future Scrutiny |

|---|---|---|

| Property & Home Insurance | High priority. Often paid out of pocket to prevent policy lapse and protect the asset. | Very Low. Everyone understands the house needs to be insured. |

| Basic Utilities (Water/Power) | Often paid out of pocket if the property is being prepped for sale or holds valuable assets. | Low. Seen as basic preservation. |

| Mortgage Payments | Variable. Often paused by notifying the lender of the death, though some families front the cost to avoid complex arrears. | Medium. Requires a clear paper trail, as amounts are large. |

| Credit Card Minimums | Usually ignored or paused. Unsecured debt is typically handled much later in the probate process. | High. Paying unsecured debt early can violate state creditor priority rules. |

| Personal Subscriptions (Gym, Streaming) | Let them lapse. Notify vendor of death. | High. Beneficiaries will question why you spent your money (expecting estate reimbursement) on a useless service. |

⚠️ Warning: If you suspect the estate owes more money than it has (an “insolvent” estate), be extremely careful about paying any bills out of pocket. State laws strictly dictate the priority of who gets paid first when funds are short. A common mistake I see is an executor paying off a $5,000 credit card bill immediately, only to realize later the estate doesn’t have enough to pay the final tax bill or funeral costs. In those cases, the executor may never be reimbursed.

When Creditors Call and Demand Immediate Payment

While you are waiting for bank access, some creditors might become aggressive. Collection agencies are known to call relatives and executors, implying that the debt must be paid immediately or suggesting that you are personally responsible for it.

In my experience, collection agents will often call the executor directly and apply heavy pressure. I have seen executors panic and pay a $3,000 medical bill with their own savings just to stop the harassing phone calls. You are generally not personally responsible for the deceased person’s debts unless you co-signed for them.

If a creditor pressures you, you do not need to argue. A calm, repetitive response is your best shield. Say: “The estate is currently in the probate process. I am waiting for official court appointment and do not have access to funds. Please send all claims in writing to [Your Address].” Then, log the call and hang up.

Communicating with Beneficiaries About Unpaid Bills

Silence breeds suspicion. If there are other beneficiaries involved, they might be getting anxious about the mail piling up at the deceased’s house. They might worry that the house will go into foreclosure or that the power will be shut off.

One of the most effective ways to reduce friction is to over-communicate about your process, even when the process is simply “we are waiting.” You do not need their permission to handle basic administrative delays, but keeping them informed shows that you are organized and in control of the situation.

If you have decided to hold off on paying certain bills until the bank grants you access, you can use a simple, neutral script to update the family.

Subject: Quick update on estate administration and mail

Hello everyone,

I wanted to provide a brief update on where things stand. We are currently waiting for the court to process the official paperwork. Until that is complete, the bank accounts remain frozen, which is standard procedure.

I am actively monitoring the mail and sorting the incoming bills. I have already contacted the major providers (like the mortgage company and utilities) to notify them of the passing and have requested that they place a temporary hold on the accounts.

I am keeping a detailed log of all incoming invoices. Once the estate bank account is officially open, I will process these outstanding items. If any critical asset preservation bills require immediate payment before then, I am tracking those carefully with receipts.

I will let you know as soon as the bank gives us the green light to move forward. Let me know if you have any questions.

Best,

[Your Name]

Final Thoughts: Protecting Your Own Boundaries

The waiting period before you receive your official court authority is functionally an administrative limbo. It is easy to let the anxiety of unpaid bills consume your daily life, but as an executor, you must protect your own boundaries.

You do not have to be a 24/7 administrator. You are allowed to let the phone go to voicemail and process the mail just once a week. The probate system is inherently slow, and the financial world is built to accommodate these delays. By setting clear boundaries for your own time, you ensure you have the mental energy required for the heavier tasks that come later in the probate process.

❓ FAQ

💸 If I pay with my own money, am I guaranteed to get it back?

Generally, legitimate estate expenses paid out of pocket are reimbursed once the estate account is open. However, if the estate is insolvent (has more debt than money) or if your documentation is poor, reimbursement is not guaranteed.

💳 Should I keep paying their credit card minimums out of pocket?

Most executors do not front money for unsecured debts like credit cards. These debts are usually settled much later in the probate process. Notify the card issuer of the death to stop late fees from compounding.

🏦 Will the bank reimburse me directly once the account is open?

No, the bank does not manage your reimbursements. Once you open the estate account, you (acting as the executor) will review your own expense logs and write a reimbursement check from the estate account to your personal account.

🧾 What happens if I lose a receipt for an estate expense?

Without a receipt, it is very difficult to prove the expense was legitimate. If you lose one, try to get a duplicate from the vendor immediately. A line item on your personal bank statement is often not enough proof on its own.

🚗 How do I handle car payments before probate starts?

Contact the auto lender immediately to notify them of the death. Some will offer a grace period. If they threaten repossession and the car holds significant equity for the estate, you may need to front the payment and document it carefully.

🛑 What if I accidentally paid a bill from my personal account without keeping the receipt?

Reach out to the vendor immediately and request a historical statement or duplicate invoice showing the property address and the payment applied. Attach this to your bank statement showing the matching outbound funds.

📞 Can creditors force me to pay out of pocket if the estate has no money?

No. Unless you co-signed the loan or are legally bound by a specific state law (like some spousal medical debt laws), you are not personally responsible for the deceased’s debts. Never let a collection agent convince you otherwise.

⏳ How long does it usually take to get bank access to pay these?

It varies widely depending on your local court’s backlog. It can take anywhere from a few weeks to several months to receive the official Letters required by the bank to open an estate account.

📱 How do I cancel their cell phone plan without the PIN?

Call the provider’s bereavement or fraud department directly. They typically do not need the PIN if you can provide a copy of the death certificate and your ID to prove you are handling the affairs, allowing them to close the account and stop billing.

✉️ Should I write “Return to Sender” on bills I can’t pay yet?

No, keep them. Writing “Return to Sender” or “Deceased” and putting them back in the mail means you lose the exact paper trail of what the estate owes. Open them, log the amounts in your spreadsheet, and store them securely until you have official bank access.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.