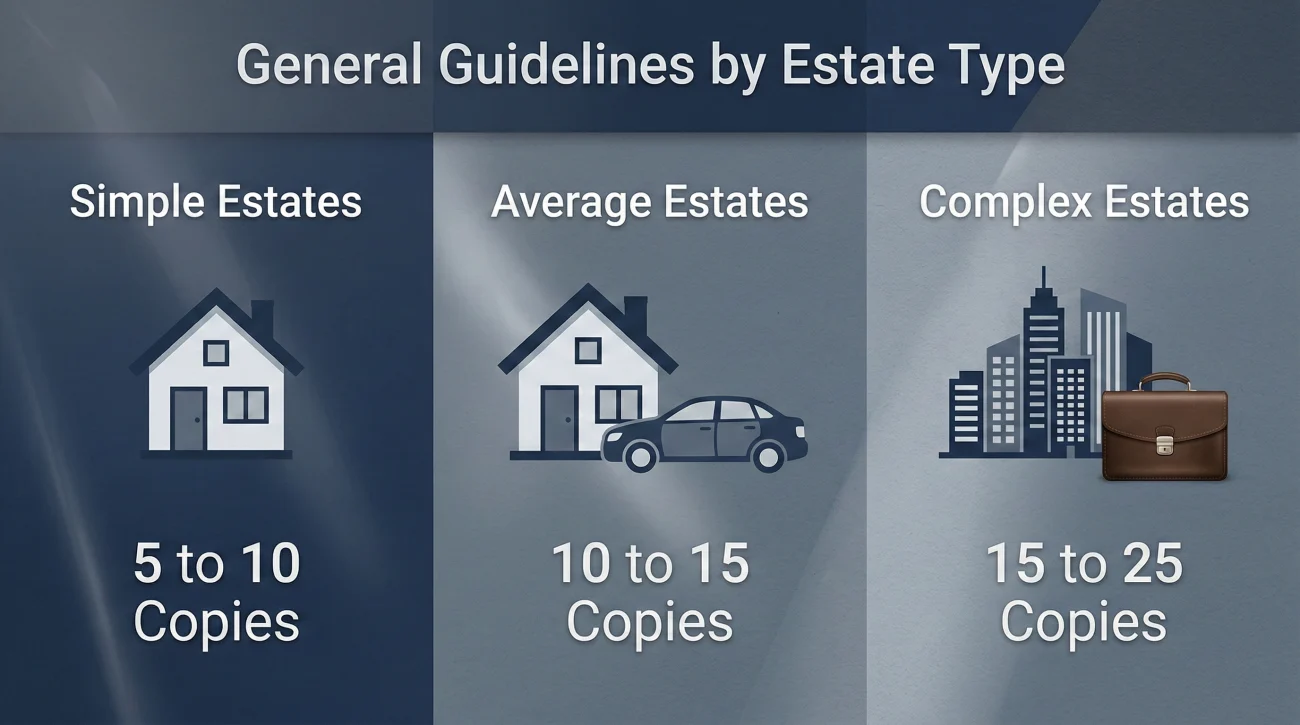

- The Baseline Rule: Most standard estates require between 5 and 10 certified copies, while complex estates with multiple properties or disparate accounts may need 15 to 25.

- Not Everyone Needs an Original: Many modern institutions will accept a high-quality PDF scan, but you must ask for their requirements in writing first.

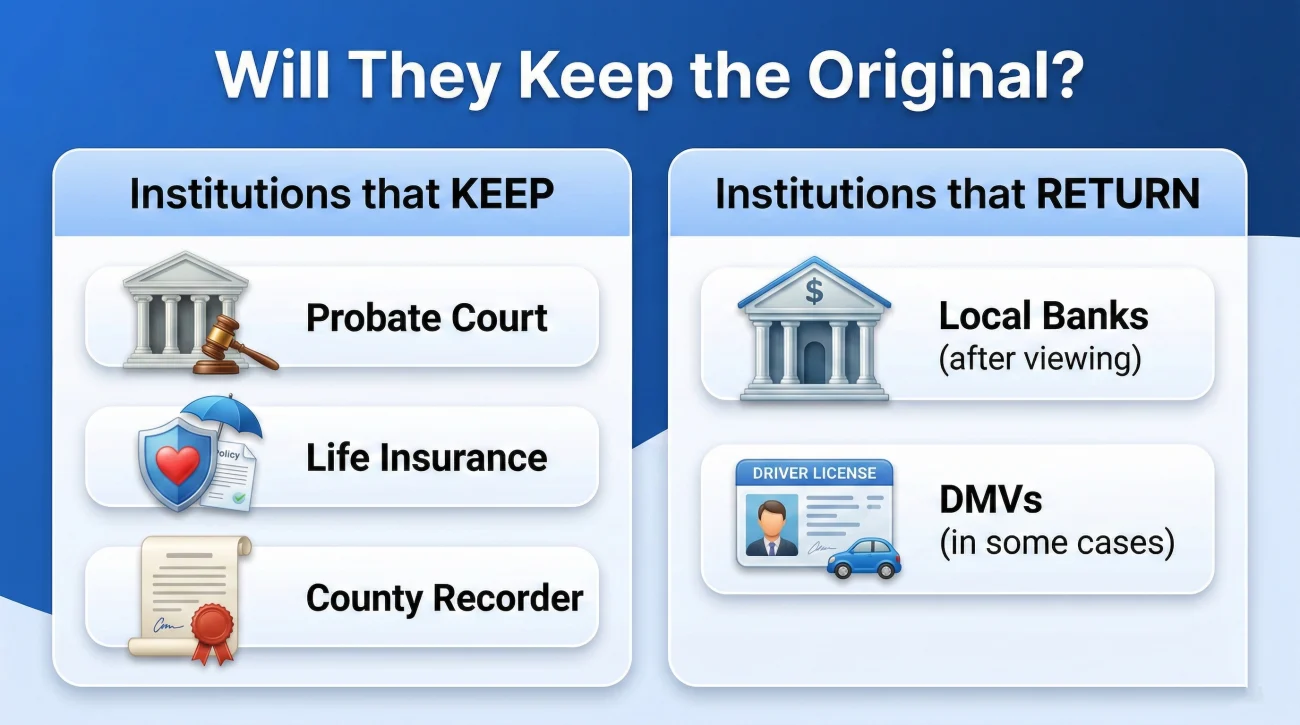

- The “Return” Reality: Some banks and agencies will make a photocopy of your certified original and mail it back to you; others are required to keep it permanently.

- Track Your Copies: Treat certified certificates like cash. Keep a running log of who you sent them to, when, and whether you expect them to be returned.

The Funeral Home Dilemma: Making the Call

If you are stepping into the role of an estate administrator, one of the very first concrete decisions you will be asked to make usually happens at the funeral home. The director will look at you and ask how many copies you want to order. It is a surprisingly stressful question when you are already overwhelmed.

I recently helped a family where the executor panicked at this exact moment and ordered 30 certified copies, “just to be safe.” Six months later, 22 of those documents were still sitting unused in a manila envelope. At $25 a piece, that was over $500 of estate funds wasted purely out of caution.

On the flip side, if you order too few, you risk stalling the entire administration process weeks later when you run out and have to wait for the county to process a new batch. There is no magic, universal number because every estate footprint is different.

However, there is a very practical way to figure this out without guessing. I want to walk you through a realistic framework for estimating your baseline needs, avoiding unnecessary costs, and tracking the documents you actually mail out.

Understanding What “Certified” Actually Means

Before you calculate a number, it helps to understand what institutions are actually asking for when they demand “proof of passing.”

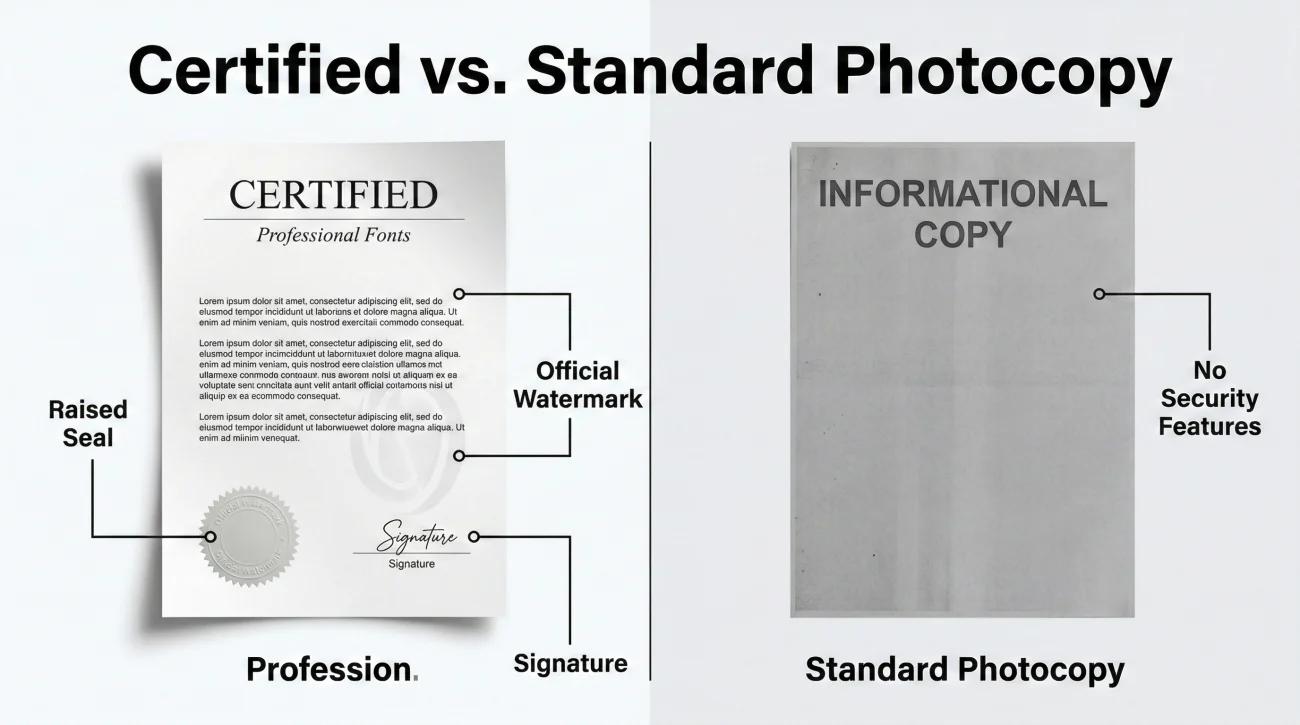

A certified death certificate is an official document issued by the state or county vital records office. It typically has a raised seal, a watermark, or a specific colored stamp that proves it is an authentic original, not a photocopy. When financial institutions or government agencies ask for a certified copy, they are specifically looking for these physical security features to prevent fraud.

An informational copy, or a simple photocopy you make on your home scanner, lacks these security features. While a basic photocopy is useless for transferring a house deed, it is often perfectly fine for closing a gym membership or canceling a streaming service.

The Shift Toward Digital Acceptance

A pattern I commonly see in recent years is that many national credit card companies and utility providers have updated their systems. Instead of forcing you to mail a physical piece of paper, they provide a secure portal where you can upload a clear PDF scan of the certified document. This administrative shift can save you a significant amount of money if you know to ask for it.

The Baseline Rule of Thumb for Standard Estates

If you are forced to give a number immediately and have not had time to look at the deceased person’s paperwork, here is a practical range that covers most scenarios I see in day-to-day operations.

- 📄 Simple Estates (5 to 10 copies): This applies if the person rented their home, had one primary bank account, one or two credit cards, and a straightforward life insurance policy.

- ✅ Average Estates (10 to 15 copies): This covers homeowners with a mortgage, multiple banking institutions, a couple of retirement accounts, life insurance, and a vehicle.

- 📂 Complex Estates (15 to 25 copies): You will lean toward this number if there is real estate in multiple states, numerous individual stock certificates, complex business ownerships, or dozens of separate financial institutions.

Key Point: Certified copies usually cost between $15 and $30 each depending on the county. It is always better to over-order slightly (by three to five copies) to avoid administrative delays later, but you do not need an original for every single minor account.

It is important to remember that the probate court itself usually only needs one or two certified copies to open the estate file. The bulk of the certificates you order will actually be sent to banks, insurers, and transfer agents.

How to Build Your Custom Estimate

If you have a few days before you need to place the order, the smartest approach is to sketch out the estate’s footprint. Do not guess; count. I always recommend building a quick inventory list. If you are just starting out and need a roadmap to organize this initial phase, reviewing a solid executor first steps checklist can help you ground your plan.

Here is how I usually help people map out their document needs. Assign one potential certificate to each of the following major categories.

1. Banks and Credit Unions

Count the distinct financial institutions, not the number of accounts. If the person had checking, savings, and a CD all at one bank, you generally only need one death certificate for that bank. If they used three different banks, assume you need three certificates.

2. Life Insurance and Retirement

Life insurance companies are notoriously strict. They almost always require an original, certified copy mailed directly to their claims department. If there are three separate policies with three different companies, allocate three certificates. The same applies to 401(k) or IRA custodians.

3. Real Estate and Titles

Transferring property deeds requires rigid documentation. You will likely need to record a certified death certificate with the county clerk or recorder of deeds in every county where the person owned property. Allocate one copy per county.

| Institution Type | Likely Requirement | Expected Return? |

|---|---|---|

| Probate Court | Certified Original | Kept for permanent file |

| Life Insurance | Certified Original | Usually kept |

| Local Bank Branch | Certified Original (to view) | Usually copied and returned immediately |

| Credit Card Companies | Photocopy or PDF upload | N/A (Digital or copy) |

| Utility Companies | Photocopy or PDF upload | N/A (Digital or copy) |

Now that you have a rough count based on this framework, the next major hurdle is making sure you don’t accidentally waste them on institutions that don’t actually need the physical paper.

Communication Scripts to Save Your Originals

Never put a $25 certified original in the mail to close a $40 minor debt without asking questions first. Protecting your document inventory means proactively clarifying what an institution actually requires before you send anything.

If you are communicating via email or a secure message center, you can use a script like this to verify their policy:

Subject: Document requirements for account closure – [Deceased Name]

Hello,

I am administering the estate for [Deceased Name]. I am preparing the required documentation to update this account.

Could you please reply with a written list of your required documents? Additionally, please confirm if you require a physical, certified original death certificate sent via mail, or if your department accepts a high-quality PDF scan of the certified document through a secure upload.

I look forward to your written confirmation so I can provide exactly what you need.

Thank you,

[Your Name]

💡 Pro Tip: If you are on the phone with a utility or telecom provider, simply ask: “Does your department accept a fax or a secure digital upload of the certificate, or is a physical original strictly required?” Note their answer, the date, and the representative’s name in your call log.

The “Keep vs. Return” Reality: Why Tracking Matters

A critical piece of administrative hygiene is understanding that your stack of certificates is a fluid inventory. Some copies will come back to you; others are gone forever.

For example, if you walk into a local bank branch where the manager knows you, they will often take your certified copy, look at the watermark, photocopy it for their internal file, and hand the original right back to you across the desk. You just completed a task without permanently losing a certificate.

Conversely, the probate court will keep one. The county recorder for real estate will keep one. Many life insurance companies will keep one.

Because of this mixed behavior, relying on memory is a bad idea. When files go missing, the loop of confusion usually starts because the executor cannot remember if they mailed their last original to the mortgage company or the auto lender.

Keeping all certificates in a messy pile, grabbing one whenever a piece of mail arrives, and suddenly realizing you have zero left when the IRS asks for one.

Using a simple tracking sheet with three columns: Institution Name, Date Mailed, and Expected Return (Yes/No). You always know exactly how many active originals you have in your possession.

The Priority Rule: Who Gets Them First?

If you realize your stack is running low, you must prioritize. Probate court and life insurance companies should always get your first available originals. The court unlocks your legal authority, and the insurance provides the liquidity to pay funeral expenses or ongoing bills. A gym membership or a cable bill can wait in line until you secure more copies.

Common Mistakes When Ordering

In day-to-day admin work, I frequently observe a few specific pitfalls when families deal with these documents.

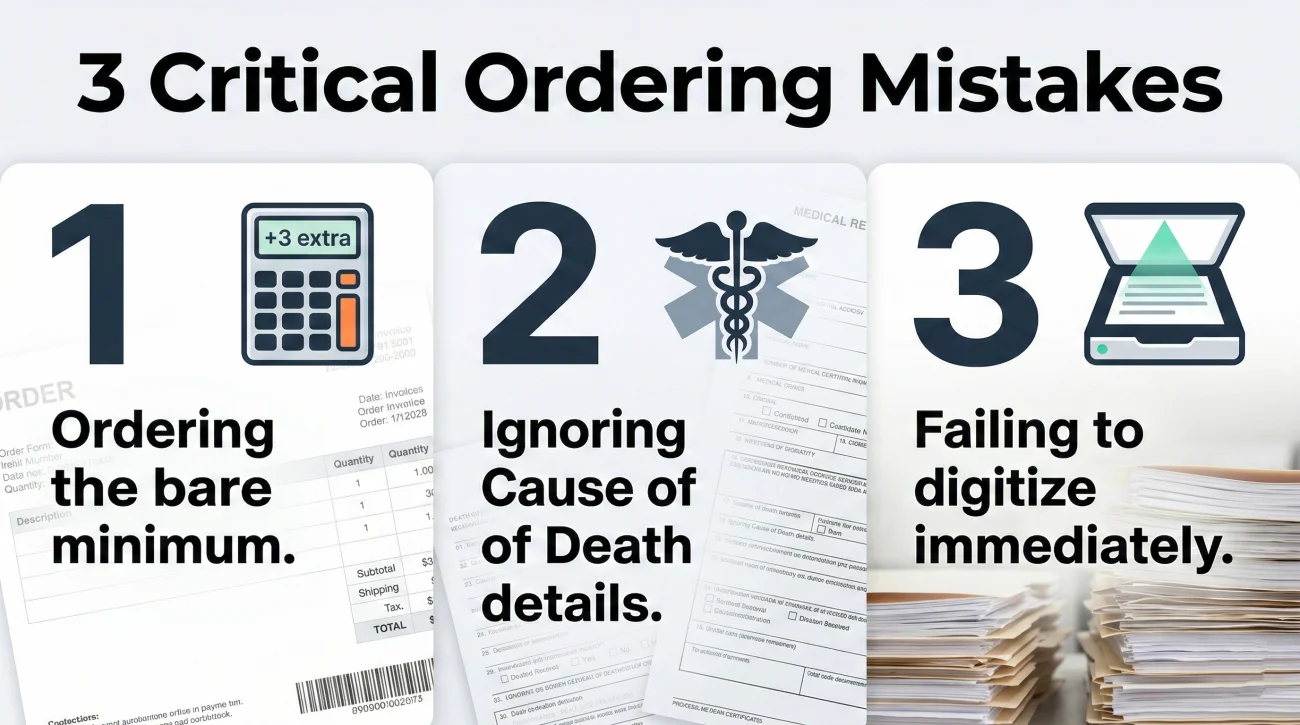

Mistake 1: Ordering exactly what you think you need

If you count 7 accounts and order exactly 7 certificates, you are leaving zero room for error. Mail gets lost. Institutions misplace files. A surprise retirement account turns up three months later. Always pad your final number. The extra cost upfront is vastly cheaper than the stress of dealing with shortages later.

Mistake 2: Not understanding “Cause of Death” redactions

Depending on the location, some jurisdictions offer two versions of the death certificate: one that lists the medical cause of death, and one that redacts (hides) it. Life insurance companies almost always require the version showing the cause of death to process a claim. Title companies and banks usually do not care. Ensure you order at least a few copies that include the cause of death if you are handling insurance payouts.

Mistake 3: Failing to digitize immediately

Before you mail a single certificate out of your house, scan it. Create a high-quality, color PDF of the document, front and back. Name the digital file clearly, something like Doe_John_Certified_Death_Certificate_Scan.pdf. Having this clear digital file ready to attach to emails will save you countless physical copies.

Navigating Errors, Shortages, and International Needs

Even with perfect planning, things go wrong. Knowing how to handle these operational hurdles quickly is part of being an effective executor.

What If There is a Typo?

One of the most frustrating bottlenecks I see is an executor receiving 15 certificates only to realize the deceased’s date of birth or social security number is off by a single digit. Do not mail those out. Banks and insurance companies will reject them. You have to go back through the funeral home or the attending physician to file a formal amendment with vital records. It takes time, but it is mandatory.

How to Order More Later

If you run out of certificates three months into the process, the funeral home will likely no longer be able to order them for you. You will need to request them directly from the county health department or vital records office. In many states, you can do this online using a service like VitalChek, or by mailing a notarized request form directly to the county clerk.

International Assets and the Apostille

If the deceased owned property in another country or was a citizen of another nation, a standard certified death certificate will often be rejected by foreign institutions. In these cases, you will need an “Apostille.” This is a specialized, international authentication attached directly to the document.

How to get it: You cannot ask the funeral home or the probate court for an apostille. You must mail a recent, certified copy of the death certificate directly to the Secretary of State’s authentication office in the state where the death occurred. You will typically need to include their specific apostille request form, a self-addressed stamped return envelope, and the required processing fee.

Final Steps Before You Order

Figuring out your final document count doesn’t require a crystal ball. Take a deep breath, sit down with a piece of paper, and list the major financial pillars of the person’s life: their banks, their home, their car, and their insurance.

Count your major categories, add your safety net of three to five extra copies, and hand that final number to the funeral director with confidence. Once the envelopes arrive, your primary job is simply to protect the inventory. Treat the stack like cash, log every outgoing piece of paper, and you will maintain a calm, organized workflow without constant administrative delays.

❓ FAQ

🛑 How many certified death certificates do I need to close a bank account?

You generally need one certified copy per banking institution, not per account. If you visit a local branch, they will often view the certified original, make an internal copy, and return the original to you.

🏦 Can I use a photocopy of a death certificate for credit cards?

In many cases, yes. Most major credit card issuers have shifted to accepting clear photocopies or secure PDF uploads rather than demanding physical, certified originals through the mail.

⚖️ How many death certificates for probate court?

Most probate courts require one certified original to formally open the estate file. Check with your specific county clerk, but one is the standard starting point for the court itself.

⏳ How long does it take to get more death certificates if I run out?

If you order through the county vital records office or health department later, processing and mailing can take anywhere from two to six weeks, which is why ordering extra upfront is highly recommended.

💸 Why do certified death certificates cost so much?

The fees (often $15 to $30 each) are set by local county or state governments to cover administrative costs, secure paper, and anti-fraud measures like raised seals and watermarks.

📬 Do I need to send an original death certificate to the IRS?

If you are filing a final tax return, you commonly need to attach a copy of the death certificate, but the IRS generally accepts a clear photocopy; they rarely demand a certified original.

🚗 Will the DMV keep the original death certificate to transfer a car title?

Often, yes. Many state motor vehicle departments require a certified original to process a title transfer and will keep it for their permanent records.

📄 What is the difference between a certified and informational death certificate?

A certified copy has physical security features (like a raised seal) proving it was issued by the government. An informational copy is a standard photocopy that lacks legal security features.

📱 Can I just email a picture of the death certificate to cancel cell phone service?

Many telecom and utility providers now accept digital uploads or faxes. Always call and ask for their specific procedure before mailing an expensive original document.

🔄 Do life insurance companies return the death certificate?

Usually, no. Life insurance companies generally require a certified original to process the death benefit payout and will retain it in their files permanently.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.