- The “Starter Packet” is a core set of 4 to 5 foundational documents that will unblock 90% of your initial interactions with financial institutions.

- Banks reject documents primarily due to compliance rules (like KYC laws) and poor digital file hygiene, not just to make your life difficult.

- Never mail your final physical certified document. Force institutions to accept secure digital PDFs or verify physical copies in-branch.

- Do not guess document requirements. Use the provided email script to force institutions to state exactly what they need in writing.

- Building an outbound tracking log is mandatory. Sending a document without tracking the confirmation of receipt is how estates get delayed by months.

The Paperwork Trap That Paralyzes New Executors

Over the last decade of helping families organize their estate workflows, I have watched hundreds of executors hit the exact same wall during their first month. They start making phone calls to banks, utility companies, and insurers with good intentions. But every single phone call ends the same way: an agent asks for a different piece of paper, the executor scrambles to find it, drops it in the mail, and waits.

Three weeks later, the bank sends a generic letter saying the document was “unacceptable” or lost in their mailroom. The executor is back to square one, but now they are exhausted and frustrated.

This reactive cycle is the number one cause of estate delays. When you are managing an estate, you cannot act like a customer asking for a favor; you have to operate like a project manager. That shift starts by building what I call the Starter Packet.

Instead of hunting for documents one by one every time a clerk asks for them, you spend your first few days assembling a single, bulletproof folder (both physical and digital). This packet contains the core proofs that satisfy the strict compliance departments of modern institutions. Once it is built, you stop reacting. When an agency demands proof, you simply attach the perfectly named PDF and move on with your day.

Assembling Your Core Proofs: The Foundational Documents

Financial institutions are heavily regulated by federal “Know Your Customer” (KYC) and anti-fraud laws. When someone dies, accounts are frozen to prevent unauthorized access. Before any bank will even confirm an account balance to you, you must definitively prove two things: the account holder has passed, and you are the legal representative. Your Starter Packet addresses these two gates immediately.

Before gathering these, establish one unbreakable rule: never mail your final physical original of any core document. Probate courts require physical originals. If an institution demands an original, take it to a local branch manager to verify and copy, rather than risking it in the mail.

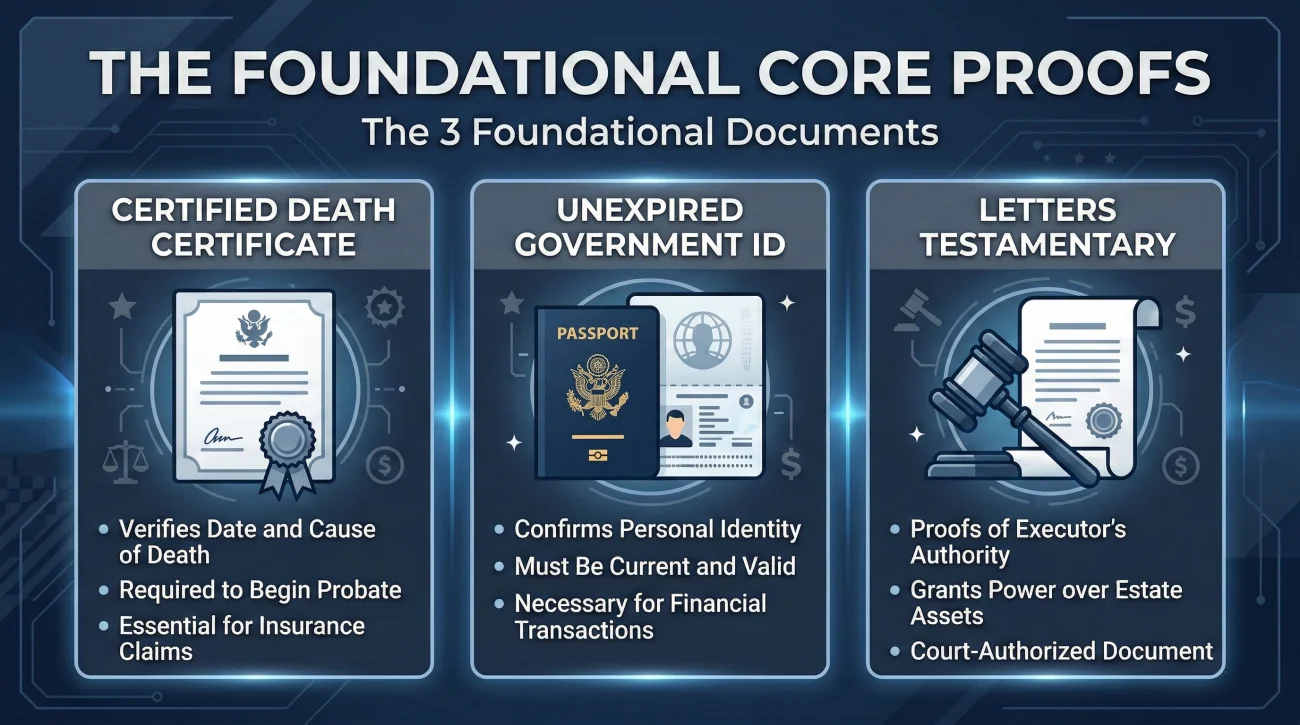

The Certified Death Certificate

This is the engine of the entire administrative process. You will need multiple official, certified copies from the vital records office. A photocopy you made at the library will not work for initial verification; legal departments look for raised seals, specific watermarks, or multi-colored ink.

Here is a technical detail that trips up many first-time executors: depending on the jurisdiction, there are often two versions of a death certificate (a “short form” and a “long form”). Always verify which version you hold, as different institutions require different forms. Check the FAQ below to see exactly when the long form is mandatory.

As soon as you receive the physical copies, lay them flat under good lighting and scan them as high-resolution PDFs. (Always scan in full color, not grayscale or black-and-white, as institutions look for colored ink and seals to verify authenticity). Do not use a warped, shadowy JPEG picture taken on your phone.

⚠️ Warning: Applying the unbreakable rule, never mail your physical certified death certificate to a processing center. Force the institution to accept a secure digital PDF. If they refuse, take the original to a local branch manager. Ask the manager to photocopy it, stamp it “Original Seen and Verified,” upload it to their internal corporate portal, and hand your physical copy right back to you.

Your Unexpired Government ID

Because of identity theft concerns, institutions need to verify *you*. Scan your current, unexpired driver’s license or passport. A surprising number of delays happen simply because an executor sends an ID that expired two months ago. Ensure it is a color scan where all text is legible.

Authority Indicators (Court Letters or the Will)

Eventually, you will likely receive official court documents (commonly known as Letters Testamentary or Letters of Administration) that legally authorize you to act. Until the court issues these, your power is heavily restricted.

However, you should not wait for court appointment to build your packet. If a will exists, keep a clean copy of it in your Starter Packet. While a will alone does not grant you access to funds, providing a copy of it alongside the death certificate is often enough to achieve triage goals, like getting the post office to route mail, asking a utility provider to keep the heat on, or notifying a credit bureau to flag the file for fraud prevention.

Asset Discovery: Gathering the Paper Trail Safely

Once your identity and authority documents are secured, your foundational packet is complete. The next logical step is to map out the financial paper trail so you know exactly which institutions to contact.

A common mistake here is feeling pressured to find every single penny immediately. You do not need a perfect balance sheet in week one. You are simply acting as an archivist, looking for breadcrumbs.

The Physical Statement Sweep

Your goal is to locate the most recent statement for every potential asset. If the deceased received physical mail, your job is to carefully monitor the mailbox for 30 to 45 days. You are looking for bank accounts, retirement fund summaries, investment portfolios, and property tax bills.

- 📄 The last two months of primary checking/savings statements

- 📄 The most recent federal tax return (Form 1040)

- 📄 Current mortgage statements or vehicle titles

- 📄 Any correspondence from life insurance providers

Digital-First Estates: The Inbox Audit

What if the deceased was entirely paperless? This is the reality for most modern estates. If you have legal access to their computer or email (without bypassing security locks illegally), you need to perform an inbox audit.

In one recent estate case, a family spent three months looking for a lost retirement account. We solved it in five minutes simply by searching the deceased’s email inbox for the terms “account summary,” “your policy,” and “tax document ready.” We found a 1099-DIV form attached to a two-year-old email from an online investment firm, revealing an unknown $40,000 brokerage account.

If you cannot access the email, look for a password manager app on their desktop or physical notebooks near their workspace. Often, just seeing the names of the institutions they saved passwords for is enough to add them to your contact list.

If the sheer volume of paper in the house is overwhelming, trying to sort financial documents on day one is usually counterproductive. A better approach is to step back and follow a reliable executor first steps checklist to stabilize the home and secure valuables before diving into the financial weeds.

Auditing the Outflow: The Obligations Folder

Stopping unnecessary financial bleeding is just as important as gathering assets. You must create a dedicated sub-folder for recurring bills and tackle them methodically.

The modern estate is littered with invisible auto-pays. To find these, look directly at the “Withdrawals” or “Electronic Transfers” section of the primary checking account statement. When you spot a recurring charge, write down the merchant name, the date it hits every month, and the exact dollar amount in your tracking log. If you see a charge you do not recognize, circle it. Put any corresponding physical bills into this Obligations folder.

Key Point: You may not have the legal authority to cancel a subscription until the court officially appoints you. But by auditing the auto-pays now, you create an exact “hit list” of companies to shut down the very day your authority is granted.

Once your hit list is built, you need an execution strategy. I frequently see executors spend an hour on hold trying to formally cancel a $12 streaming service. Do not do this. If you notify the bank to freeze the primary checking account, those minor automated charges will simply bounce and cancel themselves eventually.

Instead, focus your immediate energy on property preservation. Identify the accounts for winter heating, water, and property insurance. Call these providers directly. A frozen and burst pipe due to an unpaid gas bill will create a disaster that eclipses any other administrative headache. Protect the physical assets first; let the digital subscriptions fail on their own.

Organization: Physical Folders and Digital Naming Hygiene

In my workflow reviews, I frequently see estates stalled for weeks simply because the executor kept all incoming correspondence in an unsorted pile on their dining table. You can gather all the right documents, but if you fail at basic organization, you will still experience massive delays. This is where the most easily preventable errors occur.

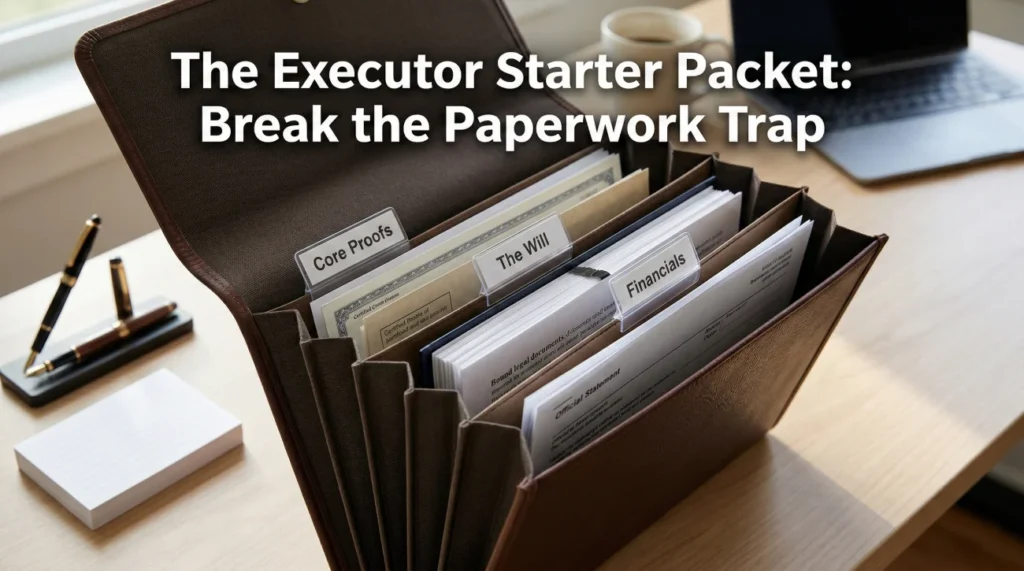

The Physical Accordion File

Do not rely on loose stacks of paper or standard manila folders that easily spill on the floor. Go to an office supply store and buy a heavy-duty, multi-pocket accordion folder. Label the tabs clearly so you can grab what you need without searching.

| Tab Name | What Goes Inside |

|---|---|

| Core Proofs | Certified death certificates, copy of your ID, official court letters |

| The Will | Original will, trust documents, attorney contact info |

| Financial (In) | Bank statements, investment summaries, insurance policies |

| Bills (Out) | Utility bills, credit card statements, property tax notices |

| Correspondence | Printed emails and letters sent to/from institutions |

Digital Naming Hygiene

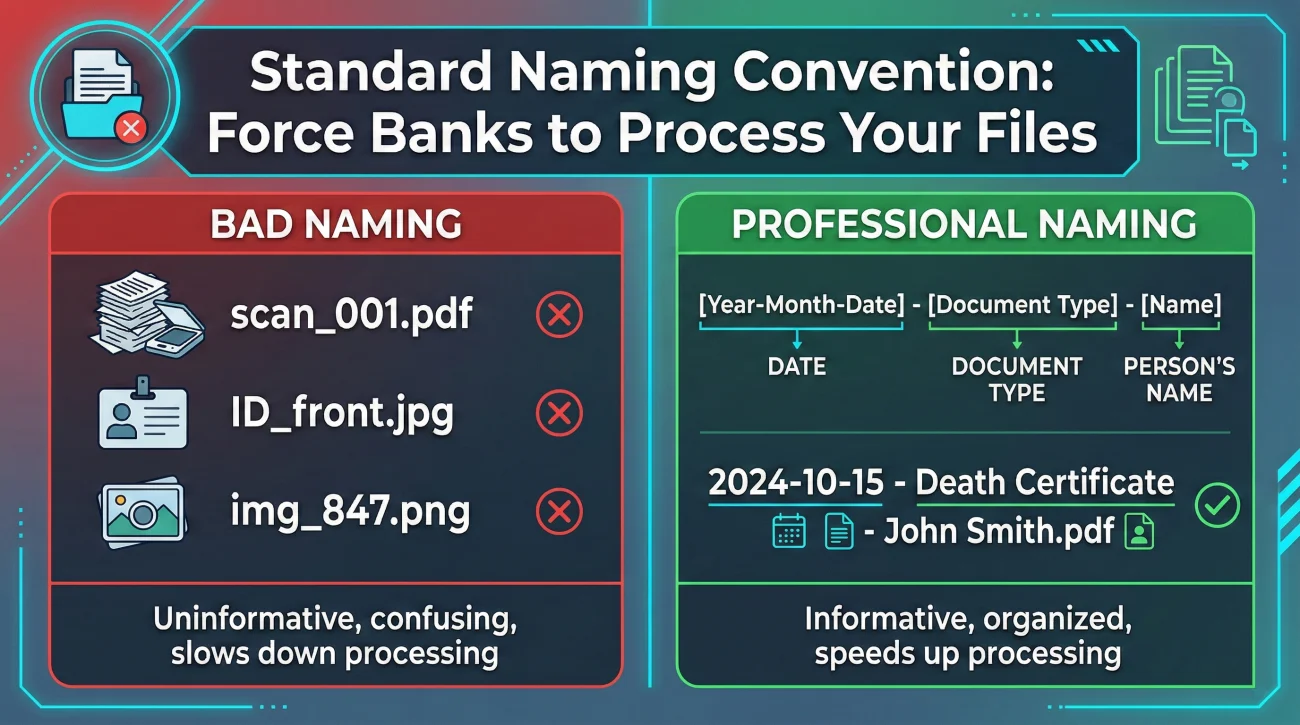

Corporate mailrooms and legal departments use intake software and clerks who process hundreds of files a day. If you email a clerk a file named scan_001.pdf, you are forcing them to open it, read it, determine what it is, and rename it for their internal system. Often, if a file is misnamed or blurry, the clerk will simply flag it as “insufficient” and move on to the next case.

You must adopt a strict naming convention that tells the receiver exactly what they are looking at before they even click on it. The industry standard format is: [Year-Month-Date] - [Document Type] - [Name of Deceased]

img_84729.jpg

scan_new_final.pdf

ID_front.pdf

2024-10-15 – Death Certificate – John Smith.pdf

2024-10-16 – Court Letters Testamentary – John Smith.pdf

2024-10-16 – Executor ID – Morgan Pierce.pdf

When you attach files using the “After” naming convention, you instantly signal that you are organized and serious. Clerks are far more likely to process your request smoothly because you have essentially done their data entry for them.

Communication Hygiene: Forcing the Bank’s Hand

The handoff is the most dangerous part of the document workflow. Mailing a packet to a generic P.O. Box without tracking, or emailing a general support address without getting a reply, is a recipe for missing files. You must take control of the narrative.

In my workflow audits, I frequently find that a large percentage of “lost” documents were actually sent to a generic retail customer support email rather than a dedicated estate department. Always ask if they have an “Estate Services” or “Bereavement” team. Major institutions like Chase and Fidelity have dedicated portals that completely bypass the retail chaos.

Script 1: Never Guess the Requirements

Before you send a single document, force the institution to state their exact requirements in writing. This creates an audit trail and prevents them from moving the goalposts a month later.

Subject: Estate of [Deceased Name] – Request for Written Document Requirements

Hello,

I am handling the estate administration for the late [Deceased Name], who held an account with your institution (Account ending in [Last 4 digits]).

Before I submit any files, please reply to this email with a complete, itemized list of all documents your legal department requires to process a notification of death and place a protective hold on the account.

Please also confirm whether your department accepts secure PDF copies via email/portal, or if physical mail is strictly mandatory.

Thank you,

[Your Name]

Script 2: The Accountability Cover Letter

When you are ready to send your correctly named PDFs, use a structured cover letter format that itemizes the attachments and demands an acknowledgment.

Subject: Estate of [Deceased Name] – Requested Documents Attached

Hello,

As requested in our previous correspondence on [Date], please find the required documents attached for the estate of [Deceased Name].

Attached to this message, you will find:

1. 2024-10-15 – Death Certificate – [Deceased Name].pdf

2. 2024-10-16 – Court Appointment Letters – [Deceased Name].pdf

3. 2024-10-16 – Executor ID – [Your Name].pdf

Please reply to this email to confirm receipt of these documents and advise on the timeline for the next steps.

Thank you,

[Your Name]

What to Do When Your Packet Is Rejected

Sometimes, even when you send everything perfectly, a front-line clerk will reject your packet due to a misunderstanding of their own policies. Do not panic and do not immediately resend the documents blindly.

Your escalation path is simple: first, request the rejection reason in writing. If it makes no sense, ask to speak directly to a Branch Manager or the Estate Department supervisor. If the internal team is unresponsive, you can file a complaint with the bank’s internal ombudsman or regulatory body, citing your tracked correspondence as proof of their delay.

The 48-Hour Triage List: Who Gets the Packet First?

Once your Starter Packet is built, you might feel the urge to email every single company on your list at once. Resist this urge. Managing 15 simultaneous document requests will overwhelm you. You need to triage.

In the first 48 hours after your packet is ready, focus only on these high-priority contacts:

- 1️⃣ The Primary Bank: To freeze the main checking and savings accounts against fraud.

- 2️⃣ Property Insurance: To notify them of the death and ensure the house remains covered while unoccupied.

- 3️⃣ The Employer or Pension Provider: To stop overpayments that the estate would later have to refund.

- 4️⃣ Life Insurance Providers: Because their claims process often takes the longest to pay out.

- 5️⃣ Major Credit Bureaus: To place a deceased alert on the credit file, preventing immediate identity theft.

The Output Tracker: Trust Nothing but Written Confirmation

As you move past your initial triage list and scale this process across five banks, two insurers, and three utility companies, your memory will fail you. Did you send the life insurance company the long-form death certificate, or just the standard one? Did the mortgage lender acknowledge receipt of your court letters?

You need a Document Request Tracker. Create columns for: Institution Name, Document Requested, Date Sent, Delivery Method, and Date Confirmed Received. It should look something like this:

| Institution | Document Requested | Date Sent | Delivery Method | Confirmed Received |

|---|---|---|---|---|

| Chase Bank | Death Cert (Short), ID, Will copy | Oct 15 | Secure Portal Upload | Oct 18 (via email) |

❌ Note: The most common operational failure I see is an executor logging a task as “Done” on the day they put the envelope in the mail. A document task is never done when you send it. It is only “Done” on the day the institution explicitly confirms they received and accepted it.

Maintaining this tracker creates a closed loop of accountability. Once your packet is built, your priority targets are triaged, and your tracking log is running, you have effectively laid the operational foundation for the rest of the estate administration.

Final

Managing an estate is a marathon of paperwork, and the Starter Packet is your primary defense mechanism against the chaos. Yes, hunting down statements and scanning IDs feels like tedious administrative work. But the friction you eliminate by doing this properly upfront is immense.

Tomorrow morning, do not make any random phone calls. Sit down, gather your certified death certificates, your ID, and the will. Scan them clearly. Name the files using the strict date convention, and put them in one dedicated folder on your computer.

By treating this setup phase seriously, you protect yourself from the endless loop of missing files and rejected applications. You will still have questions as you encounter strange bank policies and unique assets, which is exactly why we have compiled the most common edge cases below.

❓ FAQ

🪪 What happens if the executor’s ID is expired?

If your ID is expired, you will likely fail the institution’s mandatory KYC (Know Your Customer) identity verification. This will result in an immediate hard stop on your application. You must renew your driver’s license or passport before attempting to access or transfer estate funds.

📄 When does an institution actually need the “long form” death certificate?

Most banks accept the standard short form. However, life insurance companies almost always require the long form (which lists the cause of death) to investigate potential policy exclusions, such as suicide clauses or accidental death riders, before they will authorize a payout.

👥 What if the will names two people as co-executors?

If you are a co-executor, institutions will generally require core proofs from both of you. You will need to include both IDs and both signatures on formal requests. It is highly recommended that co-executors use the exact same Starter Packet and agree on who will be the primary point of communication to avoid confusing the banks.

🤷♂️ What if the deceased did not have a will at all?

If there is no will (dying intestate), you obviously cannot include it in your packet. Instead, you will rely heavily on your death certificate and your ID to perform basic notifications until the probate court officially appoints an Administrator to handle the estate.

🤝 Do I need court letters if the bank account was held jointly?

Usually, no. If a checking or savings account was held jointly with right of survivorship, the surviving owner typically only needs to present the certified death certificate and their own ID to the bank to remove the deceased’s name from the account. It often bypasses the probate court entirely.

🖋️ There is a spelling error on the death certificate. Can I still use it?

Usually, no. Financial institutions are incredibly strict about name matching. If the deceased’s name on the death certificate does not perfectly match the name on the bank account, you must contact the vital records office or the funeral director immediately to request a formal amendment.

🌐 What if the original documents are in a foreign language?

If the death occurred overseas or documents are in another language, US banks and courts will require a certified, notarized English translation. You cannot simply translate it yourself; it must be done by an accredited, professional translation service before it goes into your packet.

🛡️ Is it safe to email my ID and the death certificate?

Emailing sensitive documents carries inherent risk. Always ask the institution if they have a secure, encrypted upload portal first. If email is the only option, confirm you are sending it to a verified corporate domain, never a personal email address.

📬 Should I send my original will in the mail to the bank?

No. Applying the unbreakable rule mentioned earlier, the original will must be fiercely protected for the probate court. Financial institutions and creditors only need clear photocopies or digital PDF scans of the will unless a specific local court rule dictates otherwise.

📵 What if the deceased’s phone is locked and I need it for 2FA?

Do not attempt to guess the passcode, as too many failures will permanently wipe the device. You will need to contact the cellular carrier directly. This usually involves taking your physical core proofs into a corporate retail store (not an authorized dealer) or uploading them to their bereavement portal. Processing can take 3 to 14 business days, so start early.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.