- Month one is about gaining control, not finishing the job. Focus on securing property, starting your paper trail, and gathering information.

- Week 1 is for stabilization: securing the house, finding immediate documents, and starting a communication log.

- Week 2 focuses on authority prep: receiving death certificates, locating the original will, and figuring out local next steps.

- Week 3 is for discovery: monitoring the mail, mapping out digital traces, and building a rough inventory of what exists.

- Week 4 is for planning: preparing to open an estate account, structuring your creditor list, and setting up your month-two roadmap.

- Never pay the deceased person’s debts from your personal funds in the first month just to stop the billing letters.

Setting the Pace for Month One

When you step into the role of managing an estate, the immediate feeling is usually a profound sense of overload. You have family members asking questions, mail piling up, and a vague sense that there are legal clocks ticking in the background. In my years helping people organize estate paperwork, I notice a common pattern: executors often burn themselves out in the first fourteen days trying to solve problems they do not even have the authority to fix yet.

You cannot finalize an estate in thirty days. In most cases, you cannot even distribute a single item in that timeframe. The true goal of your executor timeline first month is simply to stabilize the situation. You need to secure what is there, stop the bleeding of unnecessary risks like fraud, and build a reliable system for the mountain of paper that is about to arrive.

I wrote this guide to give you a realistic, week-by-week sequence that actually works in the real world. This is not a list of abstract legal concepts. It is an operational roadmap designed to keep you from making the common early mistakes that cause delays six months down the line. If you follow this pacing, you will reach the end of your first month with a clear head, a highly organized file system, and everything you need to begin the official work.

How This Sequence Keeps You on Track

If you have been searching for guidance online, you have likely found lists of duties that throw everything at you at once, mixing up day-one tasks like locking the front door with month-eight tasks like paying final taxes. That approach is a recipe for panic.

This timeline is strictly chronological. We are only looking at the first roughly thirty days. If you are brand new to this role and need a broad understanding of your overall duties from start to finish, I highly recommend reading our executor first steps checklist first to get your bearings. However, if you are ready to know exactly what you should be doing on day three versus day twenty, keep reading.

My core philosophy for this executor timeline is simple: do not do work today that will have to be repeated tomorrow. Every action in this first month is about building a solid foundation so that when you finally deal with financial institutions or local authorities, you get things right on the first try.

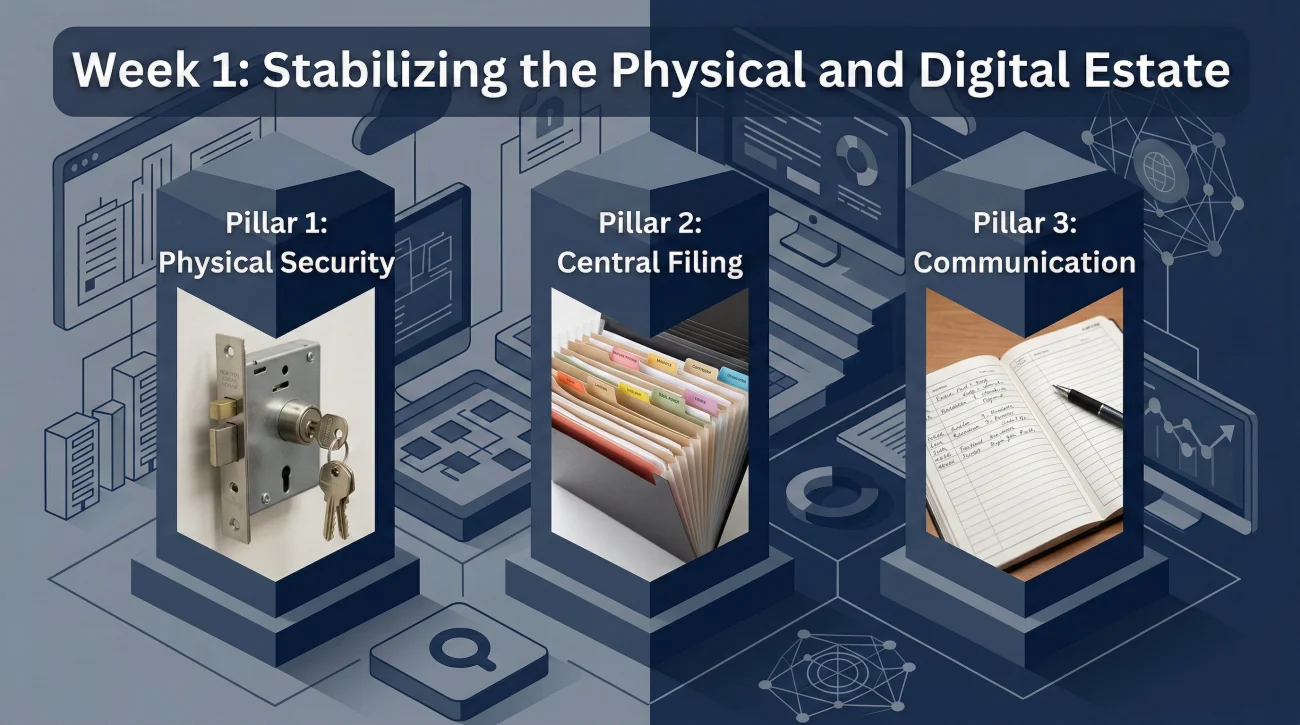

Week 1: Stabilize, Secure, and Start Records

The first seven days are almost never about official legal filings. They are about physical security and basic organization. Your primary job is to ensure nothing gets lost, stolen, or thrown away by mistake.

Secure the Physical Property

I frequently see executors overlook basic security because they are focused on finding the will. Before you do anything else, secure the physical assets. Lock the doors, check the windows, and remove perishable food from the refrigerator. If the person lived alone, make sure you collect any spare keys hidden outside. Do not let family members start taking “keepsakes” out of the house. You need an accurate picture of what was left behind, and items walking out the door in week one is a classic cause of future family conflict.

🔆 Tip: If you live out of state, your first phone call should be to a trusted neighbor or local locksmith to rekey the doors. If someone is still living in the house, “securing the property” means having a clear, documented conversation about what cannot be removed, rather than changing the locks.

Create Your Single Source of Truth

You need a central place to put things. This sounds trivial, but it is the number one operational failure I see. Create one physical box or accordion folder, and one digital folder on your computer. From this day forward, every piece of mail, every receipt, and every note goes into this system.

Leaving mail on the kitchen counter, writing confirmation numbers on sticky notes, and saving digital files to a random downloads folder.

Logging every call in a dedicated spreadsheet, putting all physical mail in a central intake tray, and naming digital files with a clear date format.

Start the Call Log

You are going to make a lot of phone calls. Start a call log immediately. A simple notebook or a spreadsheet works fine. Every time you call a funeral home, a utility company, or a relative, write down the date, the time, who you spoke with, and what they told you. When an institution inevitably loses your paperwork three weeks from now, being able to say, “I spoke to Sarah on the 14th at 2 PM and she confirmed receipt” is an incredibly powerful tool.

Week 2: Authority Prep and Information Gathering

By the second week, the immediate shock has often passed, and the bureaucratic gears start turning. This week is usually when the physical death certificates arrive, which unlocks your ability to start asking institutions real questions.

Process the Death Certificates

When the certified copies arrive, do not just throw them in a drawer. Immediately scan one high-quality copy to your computer as a PDF. Many initial notifications, especially for credit bureaus or subscription cancellations, only require a digital upload or a photocopy. Save the hard, certified copies with the raised seals for the major institutions that demand them, like financial accounts and property transfers.

💡 Pro Tip: Always keep at least one certified original death certificate safely in your own master file. Never mail out your absolute last original copy. If an institution requires one, mail it with tracking and always request a return receipt.

Locate and Protect the Original Will

If you have not found the original will yet, week two is the time for a dedicated search. Check the home office, safe deposit boxes (if you have legal access), and reach out to the attorney who may have drafted it. If you find it, handle it with extreme care. Do not remove staples, do not use paperclips, and do not fold it in new ways. Courts are often very strict about the physical condition of an original will. Make a photocopy or scan for your working reference, and put the original in a safe place.

If you absolutely cannot find a will after a thorough search, the estate is considered “intestate.” Do not panic; the local court has a default process for this scenario, but you will still need to follow the exact same stabilization steps outlined here.

Understand Your Local Landscape

This is the week to figure out what the rules are in your specific location. Every jurisdiction has different timelines and requirements for officially opening an estate. You are not necessarily filing papers this week, but you need to know the rules of the game.

Hello,

I am the named executor for [Name], who passed away recently. I am currently gathering the necessary documents to prepare for the administrative process.

Could you please provide a checklist of the required documents for our jurisdiction, and advise if there are any strict deadlines I need to be aware of within the first 60 days?

Thank you for your guidance.

You can send a polite email like this to a local professional or check the official county website to ensure you do not miss any quiet deadlines. Once you understand the local rules and have your core documents in hand, you are ready to shift your focus from immediate security to uncovering the financial picture.

Week 3: Inventory and Account Discovery

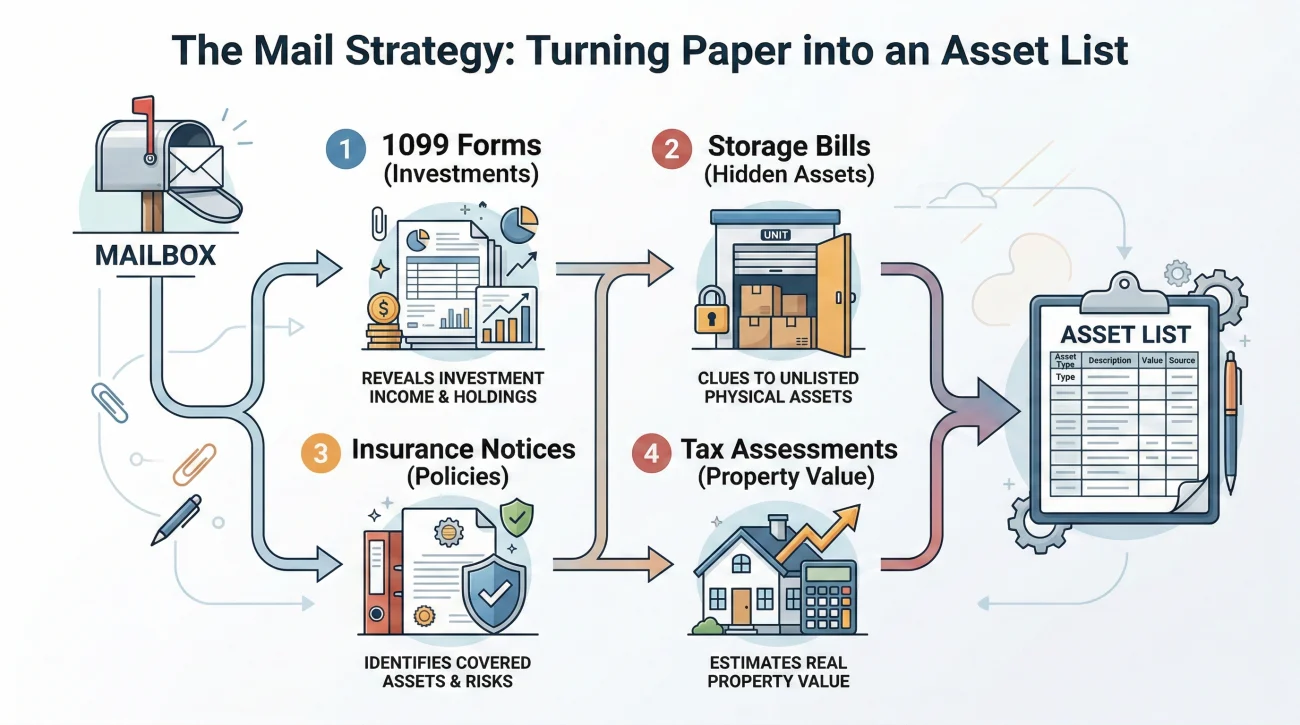

Week three requires patience. This is when the mail becomes your best friend. Many people hide their financial lives, sometimes even from their spouses. The most reliable way to figure out what someone owned and owed is to watch the paper trail unfold.

The Mail Forwarding Strategy

If the house is empty, you likely initiated mail forwarding in week one. By week three, the forwarded mail should be arriving steadily. Open everything that looks official. You are looking for bank statements, property tax bills, insurance premium notices, and credit card statements. Log every single one of these into an evolving list of assets and debts.

| What You Find in the Mail | What It Tells You to Do Next |

|---|---|

| A stray 1099 tax form | Indicates an investment account or income source you need to track down. |

| A bill for a storage unit | Immediate red flag: you need to secure this unit before the contents are auctioned off. |

| A premium notice for life insurance | Confirmation of an active policy. Add to your list of institutions to notify. |

| A property tax assessment | Confirms parcel numbers and values needed for your future inventory. |

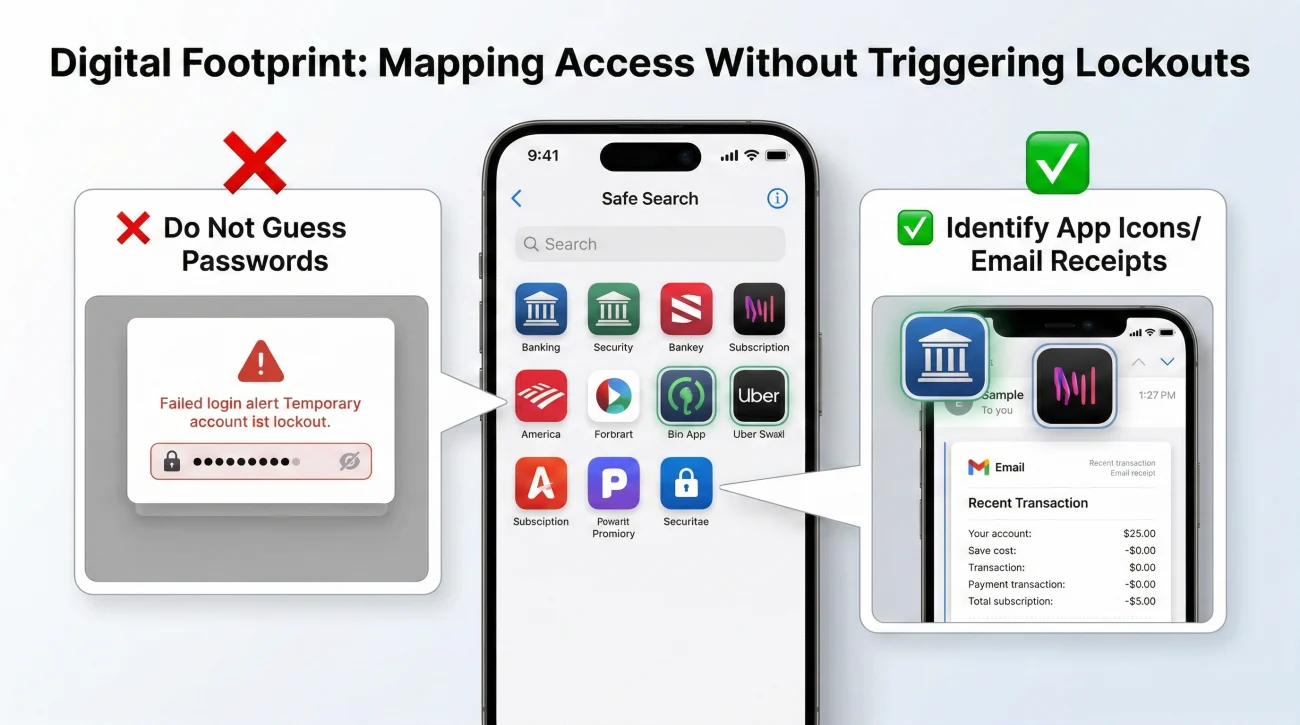

Mapping the Digital Footprint

While you are watching the physical mail, start mapping the digital footprint. I cannot stress this enough: do not attempt to log into their accounts using their passwords. Bypassing security can trigger fraud alerts that will lock the accounts down permanently, making your job ten times harder.

Instead, look at their smartphone or computer screen if it is open, and write down which banking apps are installed. Look for automatic email receipts for subscriptions if you have open access to a shared computer. Check recent delivery boxes for recurring physical subscriptions. Do not guess passwords. Instead, gather the device models, phone numbers, and associated email addresses. You will use these later to contact the specialized bereavement teams of those digital providers.

Key Point: Most hidden debts and forgotten accounts reveal themselves within two to three billing cycles. Your patience this week saves you from having to file amended court inventory forms later.

With a rough map of the estate’s assets taking shape, you can begin preparing for the official responsibilities that start in month two.

Week 4: Plan the Next Phase

As you approach the end of your executor first month checklist, you should have a solid foundation. You know what the immediate assets are, you have the death certificates, and the house is secure. Now, you pivot from stabilization to preparation for the official administrative phase.

Prepare for the Estate Account

You cannot usually open an estate bank account until the probate court grants you official authority. In many places, this takes the form of a court-stamped document commonly referred to as “Letters Testamentary” or “Letters of Administration”, depending on your specific state. However, you can prepare for it in week four. Identify a local bank that is easy for you to work with. Call them, explain your upcoming needs, and ask exactly what documents they will require from you when the time comes. This prevents the frustrating scenario of walking into a branch later and being turned away because you are missing a specific form.

Structure Your Creditor List

By now, the bills are arriving. You will see credit cards, utility bills, and perhaps medical debt. Create a master list of all potential creditors. Note the account numbers, the balances claimed, and the contact information.

⚠️ Warning: Do not pay these debts yet, and absolutely do not pay them from your personal checking account. Estates have a strict hierarchy of who gets paid first. If you pay a credit card bill now, and it turns out the estate does not have enough money to cover funeral expenses or taxes later, you might be held personally responsible for the mistake.

Manage Beneficiary Expectations

Week four is usually when beneficiaries start asking, “When do I get my inheritance?” or “Can I just take that old watch now?” This is a critical moment for setting clear boundaries.

You need a standard, polite response that buys you time and establishes the rules.

Hello everyone,

I want to provide a quick update. I am currently in the process of gathering the necessary documents, securing the property, and building a full inventory of the accounts, which is required before we can move forward with any next steps.

The administrative process takes time, and no items or funds can be distributed until all official requirements and debts are settled. I will keep you updated as we hit major milestones, but for now, please know that things are progressing safely and steadily.

Thank you for your patience.

Before we wrap up the first month’s timeline, let’s separate the truly urgent tasks from the ones that are artificially stressing you out.

What Cannot Wait (The High-Priority Items)

While I advise pacing yourself, there are a few things in the first month that truly cannot wait. These are items where delay creates permanent damage or financial loss.

- 🛑 Securing physical property: Empty houses attract trouble. Locks, lights, and stopping mail buildup are day-one priorities.

- 🛑 Fraud prevention: If you suspect the person’s wallet or phone was stolen, notifying credit bureaus to place a freeze is critical to stop identity theft.

- 🛑 Time-sensitive benefits: If there is a surviving spouse who depends on specific survivor benefits or pensions, getting those notifications rolling early is essential for their financial survival.

- 🛑 Paying the property insurance: If the homeowner’s insurance policy is about to lapse due to a missed payment, you must keep it active. An uninsured, empty home is a massive liability.

What Can Absolutely Wait Without Risk

To reduce your stress, you must understand what you can safely ignore during month one. Many executors panic over things that are actually months away from being due.

- ✅ Paying unsecured debts: As mentioned in week four, those credit card bills can safely sit in a folder. You have no obligation to settle them until the estate’s overall financial health is officially determined.

- ✅ Distributing personal items: Do not let anyone take furniture, jewelry, or vehicles. Everything stays until the inventory is complete.

- ✅ Filing taxes: Unless the person died right before the April deadline, you generally have time to figure out the tax situation. Do not rush to file complicated returns in week two.

- ✅ Closing complex investment accounts: You cannot usually close these without official authority anyway. Let them sit, just collect the statements to track the values.

Final Thoughts on Month One

Completing the executor timeline first month is about establishing order and protecting the estate, not racing to the finish line. If you reach day thirty and you have a secure property, a neat stack of death certificates, a running call log, and a good idea of what the person owned, you are doing a fantastic job.

Do not judge your progress by how much money has moved or how many accounts are closed. In fact, if you have moved money around in month one, you might be moving too fast. Judge your progress by the quality of your records. As you move into month two, the groundwork you laid, such as your single folder system, your meticulous notes, and your calm communication, will be the exact tools you rely on to manage the complex administrative hurdles ahead.

❓ FAQ

📝 How do I prove I am the executor before I have court papers?

You cannot fully prove it yet, but you can use the death certificate and a copy of the will to freeze accounts or start gathering information. Official money transfers will require the actual court-issued documents.

🏠 What if a family member is living in the deceased person’s house?

Do not attempt to evict them immediately. Document the arrangement, secure valuables, clarify who is paying utilities during the transition, and consult a local professional about tenant laws.

💻 Can I use their phone to transfer money if I know the PIN?

No. Even if you have the passcode, transferring funds after death without official authority can be viewed as misappropriation and often triggers permanent fraud lockdowns on the accounts.

📬 Should I open mail addressed to the deceased person?

Yes. As the person handling the estate, you need to open the mail to identify creditors, locate hidden assets, and find active subscriptions. Keep everything organized in your central folder.

💳 What happens to credit card debt if there is no money in the estate?

The debt usually dies with the person. Family members and the executor are not personally responsible for paying it out of their own pockets, provided they did not co-sign the account.

🚗 Can I drive the deceased person’s car to keep it running?

It is generally advised not to. Insurance coverage often changes or lapses upon the owner’s death, making driving the vehicle a significant liability risk for the estate and the driver.

📑 Do I need to hire a lawyer in the first week?

Not necessarily. Use week one to gather the will, death certificates, and a basic financial overview so that when you do consult a professional, your time with them is highly efficient.

🗑️ Is it safe to throw away old paperwork I find in the house?

Do not shred anything in the first month. Keep past tax returns, property deeds, and financial statements. Box up the rest securely until the estate administration is fully closed.

🏦 How do banks know when someone dies?

Often, the Social Security Administration notifies them electronically, or a joint account holder reports it in person. Once notified, the bank will automatically freeze the individual accounts.

✈️ How do I manage an estate if I live in a different state?

You will likely need to travel at least once to secure physical property and search for the will. After that, most communication and document gathering can be handled remotely with local professional help.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.