- The main objective: You must ensure the government knows about the passing to stop benefits and prevent complicated overpayment issues.

- The workflow: Funeral directors typically file the initial electronic report, but executors must verify that the system actually updated.

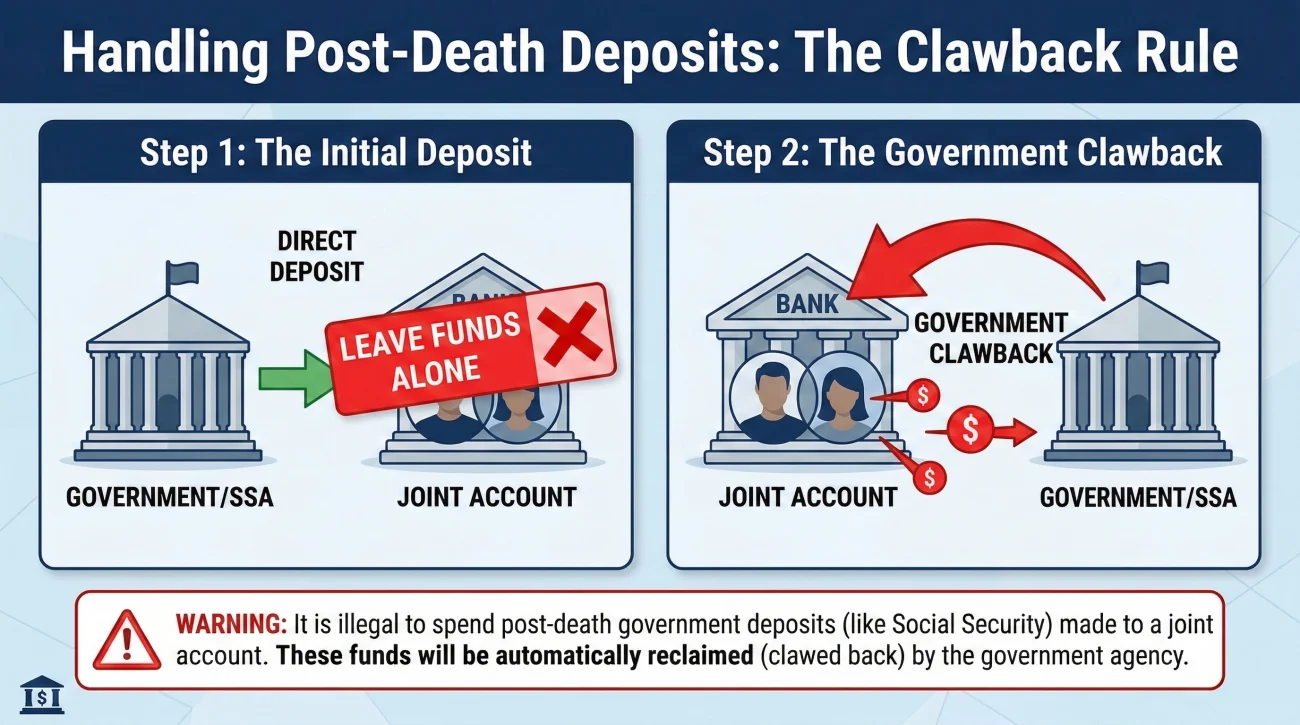

- The financial rule: Never spend any benefit deposits that arrive after the month of death. The government will automatically claw them back.

- The next phase: Once the passing is reported, the focus immediately shifts to securing survivor benefits for a spouse or dependents.

The Reality of Managing Agency Notifications After a Loss

When you step into the role of an executor or administrator, you quickly realize that your job is less about making grand decisions and more about managing a massive flow of information. One of the very first operational hurdles you will face is figuring out how to notify Social Security of a death. It sounds like a simple administrative box to check, but in reality, it is a process that requires careful attention, a paper trail, and a lot of patience.

In my experience supporting estate administration workflows, I see families get tripped up here frequently. People often assume that because the government is a massive, connected entity, updating one office automatically updates everything else. Unfortunately, that is not how the system works on the ground. A delayed social security death notification can lead to unexpected deposits, complex accounting errors later on, and stressful letters demanding money back.

Before we get into the phone scripts and tracking methods, here is the basic timeline of how this notification process usually unfolds in the real world:

- 🗓️ Day 0 to 3: The funeral home submits the initial electronic death report.

- 🗓️ Week 2 to 3: The executor calls the agency to verify the system updated successfully.

- 🗓️ Week 4 and beyond: The executor monitors bank accounts for automated clawbacks of any final overpaid deposits.

I want to walk you through exactly what happens during these phases, what you need to confirm, and how to protect the estate’s finances while the paperwork catches up with reality. If you are just getting your bearings, you should also review the complete executor first steps checklist to ensure you have your baseline priorities in order.

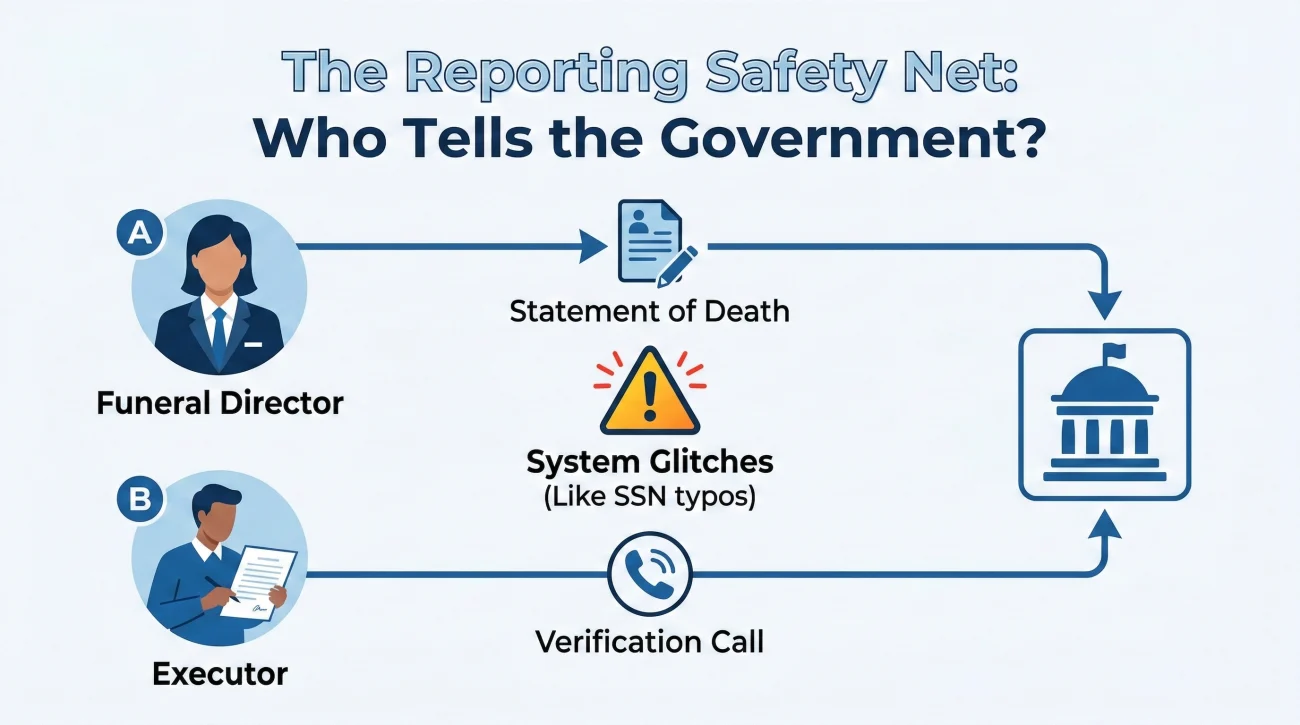

Who Typically Reports the Death (and Handling the Glitches)

There is a widespread misunderstanding about who actually holds the responsibility for the initial agency report. In the vast majority of cases, you do not have to be the first person to break the news to the government.

The Funeral Director’s Role

When you sit down with a funeral home, they will ask you for the deceased person’s Social Security Number. They use this number to generate the death certificate and to file an electronic form called the Statement of Death by Funeral Director. This is a highly efficient system designed to alert the agency quickly so that benefit payments can be paused.

When There Is No Funeral Home

If the family is handling the disposition without a traditional funeral director, which is becoming more common, this automated safety net does not exist. In these cases, the responsibility to report falls directly on the executor or the surviving next of kin. You must contact the agency directly by phone as your very first administrative action to halt any outgoing payments.

The Verification Step and Escalation Path

Here is a field note from my day-to-day admin work: the digital handoff between the funeral home and the government is the most common place where data goes missing. Sometimes a digit in the SSN is transcribed incorrectly. Sometimes the electronic system simply glitches.

As an executor, your role shifts to verification. A few weeks after the passing, you must make a follow-up phone call to your local office to verify that the agency actually processed the report. If you call and they have no record of the passing, do not panic, but do escalate. Ask to speak to a supervisor, request a case reference number for the error, and offer to send a certified copy of the death certificate via certified mail to force the update in their system.

⚠️ Warning: Do not rely on third-party online services that claim they will “notify all government agencies for you” for a fee. Stick to the official channels to prevent fraud and identity theft.

What Information Is Commonly Requested?

When you pick up the phone to confirm the report or escalate a missing file, you need to be prepared. Calling government agencies involves long hold times, and the last thing you want is to finally reach a representative only to realize you do not have the right piece of paper in front of you.

Having a specific “call file” sitting on your desk before you dial is a basic but essential habit. You usually do not need to send them a physical death certificate for a routine confirmation, but you absolutely need the data printed on it.

| Information Required | Why They Need It |

|---|---|

| Full Legal Name | To locate the exact profile, including any middle initials used on official documents. |

| Social Security Number | The primary identifier. Have the card or a tax document handy to ensure zero typos. |

| Exact Date of Birth | Used as a secondary security verification measure by phone representatives. |

| Exact Date of Death | Crucial for determining which final benefit payment the estate is entitled to keep. |

| Your Contact Information | To log who is calling and establish a point of contact for any surviving spouse benefits. |

A common mistake executors make is trying to handle these calls while driving or multitasking. You need to be seated, with a pen, a notebook, and the deceased’s core documents in front of you. Once you provide this precise information, the representative updates the master file.

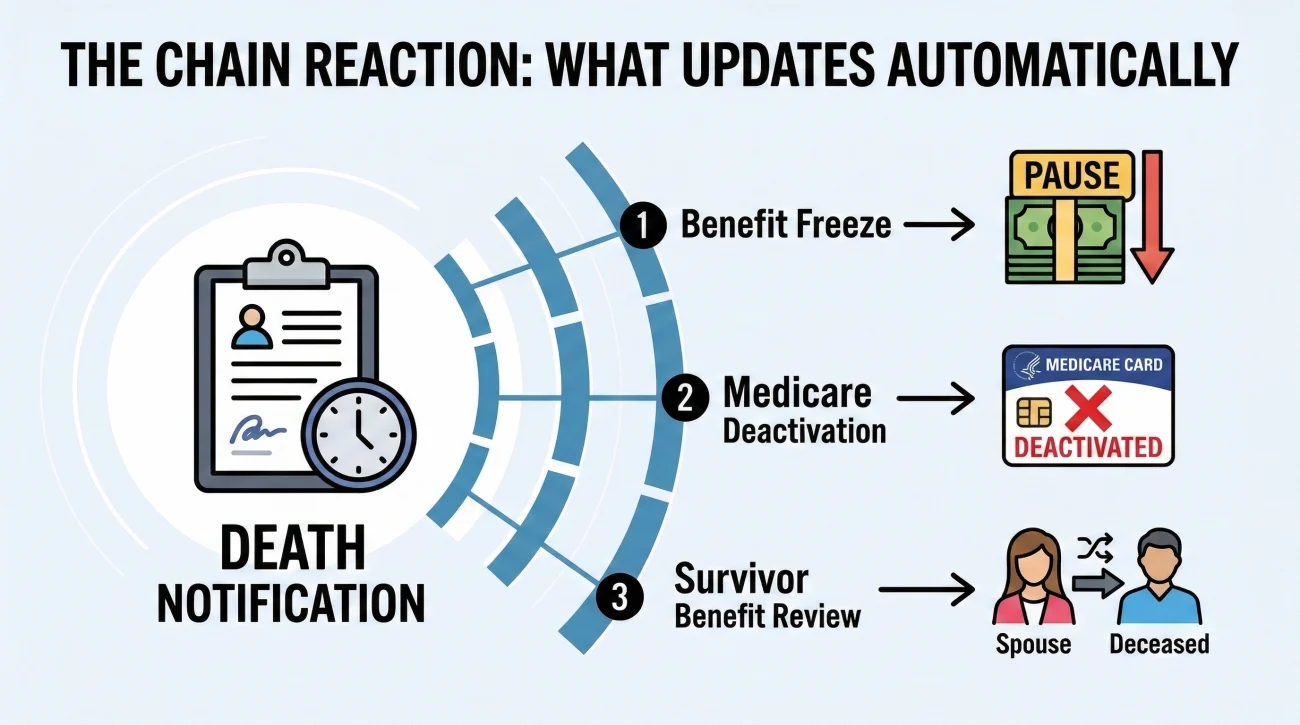

What Happens Behind the Scenes After Notification

This single update triggers a chain reaction across several government systems. Once the agency successfully processes the notification, understanding these automated mechanisms helps you anticipate what will happen with the deceased’s bank accounts and health coverage.

The Benefit Freeze (and The Prorating Rule)

The most immediate change is that future benefit payments are stopped. However, the timing depends entirely on the type of benefit and the exact date of passing. For standard retirement or disability benefits, the most important rule here is often counterintuitive:

Key Point: Standard retirement benefits are not prorated for the month of death. You must live the entire month to be entitled to that month’s payment.

If a person passes away on July 25th, they are not entitled to the benefit payment for July, which is normally deposited in August. It is also important to note that if the deceased received Supplemental Security Income (SSI), the rules are even stricter. SSI is need-based, and entitlement ends on the exact date of death, with no grace periods.

Medicare Deactivation

Another system that updates behind the scenes is Medicare. Because Medicare Part A and Part B are tied directly to the same centralized database, reporting the passing will trigger the cancellation of Medicare coverage. You generally will not receive a phone call about this; instead, watch the mail for a final Medicare Summary Notice indicating the closure. This is a detail you should log in your master timeline so you know when the premium deductions officially ended.

Handling Unexpected Deposits and Joint Accounts

In the real world of estate administration, timing is rarely perfect. Even if you and the funeral director do everything right, you may still see a direct deposit land in the checking account shortly after the passing. How you handle this deposit is a critical test of your executor discipline.

A typical pattern I see involves a surviving child who is a joint account holder. They see the government deposit land, assume that because their name is on the account the funds are safe to use for funeral expenses, and spend it. While a joint owner does have legal access to the bank account, neither the joint owner nor the estate is entitled to keep post-death government benefits. A week later, the government “clawback” hits the account. Because the funds are gone, the account is drawn into the negative, triggering overdraft fees, bank freezes, and a cascade of panicked phone calls.

💡 Pro Tip: The golden rule is simple: if a benefit arrives after the passing, leave it exactly where it landed. Do not move it to an estate account. Do not use it to pay the electric bill. Let the electronic reversal happen naturally.

If you need to speak with the bank about a deposit you suspect should not be there, you can use a calm, practical script like this to get clarity without escalating the situation:

Script: Inquiring about a post-death deposit

“Hello, I am calling regarding the account for [Name]. We recently notified the bank of their passing on [Date]. I see a government benefit deposit posted on [Date]. Can you confirm if the agency has initiated the reversal request yet, and is there a note on the file preventing the account from being fully closed until that clears?”

The Next Step: Transitioning to Survivor Benefits

Stopping the deceased’s payments is only half the equation. If there is a surviving spouse or dependent children, the conversation must immediately pivot to survivor benefits. Many families wait too long to initiate this step, losing out on critical transitional income. Delaying this application is a common mistake that can actually cost you months of retroactive payments, so do not put it off.

When you make your verification phone call, you should explicitly state if there is a surviving spouse. The representative will review the deceased’s earnings record against the spouse’s record to determine if a higher benefit amount is available. In many cases, a surviving spouse can step up to receive 100% of the deceased worker’s benefit amount if it is higher than their own.

This is a separate application process and requires a dedicated phone appointment. As the executor, part of your communication hygiene involves ensuring the surviving spouse knows they need to schedule this intake interview, as the government will not automatically adjust the monthly payout without confirming the survivor’s current details.

Template: The Contact Log and Confirmation Tracker

You cannot manage what you do not track. The sheer volume of phone calls, reference numbers, and representative names you will accumulate in the first few weeks is staggering. Creating a simple spreadsheet or a dedicated page in a notebook specifically for institutional contacts is highly effective.

When you call an agency back to check on a status, being able to provide the exact date, time, and name of the previous person you spoke with changes the entire dynamic of the conversation. Here are the exact columns your contact log should include for these interactions:

- 📞 Date and Time: The exact moment the call started.

- 👤 Representative Name and ID: Always ask for their ID or extension number immediately.

- 🎯 Purpose of Contact: E.g., “Confirming receipt of funeral home report.”

- ✅ Outcome/Answer: What they explicitly told you. “Confirmed in system, benefits stopped.”

- 🔢 Reference Number: If they generate a ticket or case number, record it.

- 📅 Next Follow-up Date: When you need to check back if the issue is unresolved.

Using a formula for your follow-ups ensures you keep the momentum going without being overly aggressive. A good rule of thumb is:

[Action logged] + [Wait 14 days] + [Follow-up to confirm status]

Final Thoughts on Navigating the Notification Process

Handling the social security death notification is a perfect example of what estate administration is really about: verification, documentation, and patience. You are not closing accounts forever today; you are simply stopping the bleeding of overpayments and setting the stage for survivor benefits.

Make the call, log the reference number, fiercely guard the final deposit from being spent, and let the system correct itself. Once that confirmation is secured in your logbook, you can safely turn your attention away from the government and focus on the rest of the estate inventory.

❓ FAQ

🌐 Can I report a death to Social Security online?

No. Currently, the agency does not allow you to report a death online. If a funeral home does not handle the electronic submission, you must call your local office or the national toll-free number directly.

💳 What if the deceased received benefits on a Direct Express debit card?

If benefits were loaded onto a Direct Express card, do not use the card after the date of passing. The government will automatically withdraw any overpaid funds directly from the card balance once the death is processed.

👨⚖️ What happens if there was a Representative Payee managing the funds?

A Representative Payee’s authority to manage funds ends immediately upon the beneficiary’s death. They must stop using the account, leave any remaining funds in place, and return any benefits received after the death.

💼 Does the executor receive the $255 lump-sum death benefit?

Typically, no. The $255 lump-sum death payment is generally only payable to a surviving spouse who was living with the deceased, or to eligible dependent children. It rarely goes directly to the estate itself.

🏦 Do I need to open an estate account before the government clawback happens?

No. The clawback will target the original account where the funds were deposited. Keep that original account open until the government successfully reverses the overpayment, then proceed with transferring remaining funds to an estate account.

📄 What if the Social Security Number on the death certificate is wrong?

A wrong SSN on the death certificate will cause the agency to reject the electronic report. You must contact the funeral director or vital records office immediately to amend the death certificate before the government systems can be successfully updated.

🇺🇸 Does reporting to Social Security automatically notify the VA?

No. The Department of Veterans Affairs (VA) operates its own systems. If the deceased was receiving VA benefits, the executor or family must contact the VA separately to report the passing and stop those specific payments.

📬 I received a paper benefit check in the mail after the death. What do I do?

Do not cash or deposit the check. You must return it to the agency as soon as possible. Cashing a post-death benefit check is a serious violation and will result in immediate demands for repayment.

🛑 How do I know if the Medicare cancellation actually went through?

Medicare cancellation is usually automated alongside the Social Security report. You will know it processed when premium deductions stop appearing on bank statements, or when you receive a final Medicare Summary Notice in the mail.

⏱️ Is there a legal penalty for a delayed death report?

While an honest administrative delay is rarely treated as a crime, the financial liability is absolute. The estate (or the joint account holder) is strictly liable for repaying every dollar of overpayment that accrues due to a delayed report.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.