- The primary goal of week one is to secure the estate, not to finalize it. Pause, breathe, and focus on protection.

- Secure the physical property, lock up vehicles, and place a temporary hold on the mail to prevent fraud and theft.

- Set up a rigid, single-source file system and a call log immediately to capture all incoming information without losing details.

- Do not pay the deceased person’s bills from your own pocket or distribute assets during this initial seven-day window.

The Reality of Week One: Why Slowing Down Saves Time

In my day-to-day work supporting estate administration, and seeing patterns across hundreds of probate cases nationwide, I see a very common reaction. When someone steps into the role of an executor, their first instinct is usually to start running. They want to call every bank, pay every pending bill, and immediately start cleaning out the deceased person’s house. It is a completely natural response to the stress and grief of the situation.

But rushing is exactly where the missing document loops begin. An effective executor first week checklist is actually about doing less, not more. Your job in these first seven days is to stabilize the situation, protect the property, and set up your tracking systems. You do not need to have all the answers right now, and you certainly do not need to resolve financial matters immediately.

By focusing strictly on stabilization, you prevent the chaotic back-and-forth that delays the process later on. Let us walk through the seven specific moves you should prioritize this week to build a solid foundation for everything that comes next.

Move 1: Secure Property and Critical Items

The very first operational step is physical security. When an estate is left unsecured, things tend to go missing. Sometimes it is opportunistic theft, but very often it is well-meaning family members who stop by to collect a memento they believe they were promised. I always remind new executors that as the person responsible for the estate, you need to protect the assets so they can be properly accounted for later.

Start by changing the locks on the primary residence if there is any doubt about who has keys. Lock all vehicles and secure the keys in a central, safe location. If there are obvious valuables in plain sight, such as jewelry, cash, or small electronics, move them to a locked safe or a secure, documented location.

💡 Pro Tip: Take your smartphone and slowly walk through every room of the house, recording a video. Open closets and cabinets. This creates an immediate, time-stamped visual baseline of the property’s condition and contents. If a question arises later about whether an item was present at the time of death, you have the video to reference.

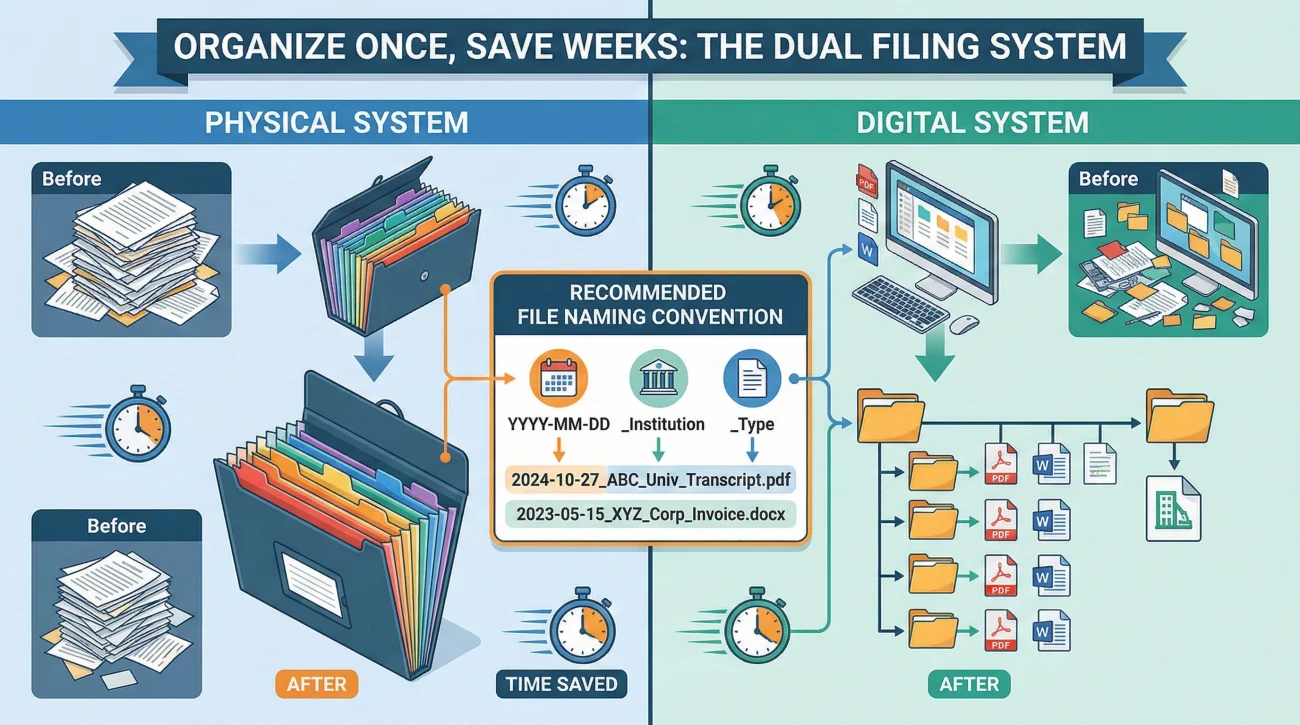

Move 2: Create a Single Starter File System

Paperwork is going to arrive fast. If you rely on the “kitchen table method” of stacking mail into loose piles, you will inevitably lose a critical document. Setting up your filing system in week one is the best defense against administrative headaches.

I always recommend setting up two parallel systems: one physical and one digital. For the physical system, buy a simple expanding accordion folder and label the slots. For the digital system, create a main folder on your computer and establish a strict naming convention for every scanned document.

A good file naming habit prevents you from opening twenty different PDFs labeled “Scan_001.pdf” when looking for a specific life insurance policy.

Format: YYYY-MM-DD_InstitutionName_DocumentType

Example: 2023-11-04_NationalWater_FinalBill.pdf

Example: 2023-10-15_HomeInsurance_PolicyDeclaration.pdf

Move 3: Start the Call Log and Request Tracker

You are going to make dozens, possibly hundreds, of phone calls over the coming months. Memory is not a reliable tool for an executor. When you call an institution, you will likely speak to a different representative every single time. Without a call log, you will find yourself repeating the same story and starting the process over from scratch.

Start a dedicated spreadsheet or a simple notebook specifically for estate business. Every time you pick up the phone, write down the date, the time, the number you dialed, the name of the representative, and most importantly, the reference number for the call.

“Called the electric company on Tuesday. They said they would close the account.”

“Nov 12, 10:15 AM. Spoke with Agent Sarah (ID #4592). Requested final reading for Nov 30. Reference number for this request: req-99382. Advised final bill will mail on Dec 5.”

Having that reference number shifts the burden of proof. When you follow up, you are no longer asking “Can someone help me?” Instead, you are stating, “I am calling to check the status of ticket number req-99382.” It changes the entire dynamic of the conversation.

Move 4: Compile the Institutions List

You cannot notify institutions until you know who they are. In the first week, your goal is discovery, not action. You are acting as an investigator, gathering clues about the deceased person’s financial and domestic footprint.

Do not guess. Build your list based on physical evidence. Look at the physical mail that arrives over the first few days, check the wallet for cards, and look around the house for recurring service providers. To make this easier, I use a Master Discovery Checklist to ensure no category is forgotten.

Master Discovery Checklist to start building:

- 🏦 Banking: Checking, savings, safety deposit boxes, local credit unions.

- 🛡️ Insurance: Life insurance, homeowners or renters policies, auto insurance.

- 📈 Retirement: 401k, IRA, pension providers, Medicare, Social Security.

- 🏠 Housing: Mortgage servicer, landlord, HOA management, property tax office.

- 💡 Utilities: Electricity, water, gas, internet, trash collection.

- 💳 Debts: Credit cards, auto loans, personal lines of credit.

- 🔄 Subscriptions: Streaming services, gym memberships, magazine deliveries.

Gathering these clues early is a vital part of your executor first steps checklist. Once you have this initial footprint documented, the actual process of officially notifying banks and closing accounts in the coming weeks will be much more manageable.

Move 5: Identify the Will Status and Next Questions

Dealing with legal documents while grieving carries a heavy cognitive load. It is normal to feel overwhelmed when searching through personal papers. Take your time. Locating the original last will and testament is a critical milestone in week one because it dictates who actually has the authority to act.

Check obvious places first like fireproof lockboxes, home office filing cabinets, the bottom drawer of a desk, or the freezer (a surprisingly common storage spot for important papers). If you know the name of the attorney who drafted their documents, add them to your call log to request a status check.

⚠️ Warning: If you find the original will, do not remove any staples. Do not attach paperclips to it. Courts can be incredibly strict about the physical integrity of an original will, and removing a staple can raise questions about whether pages were removed or altered.

What If There Is No Will?

In many of the estates I see, there is simply no will to be found. If you have searched everywhere and cannot locate one, the estate is considered “intestate.” Do not panic. The probate process still exists for this scenario. A local probate court will appoint an administrator (usually a close family member) to handle the estate according to your specific state formula. Your job in week one remains exactly the same: secure the property and gather information.

Move 6: Prevent Fraud and Stop Mail-Based Risk

An empty house with an overflowing mailbox is a highly visible target for identity theft and property crime. Managing the mail flow is one of your most urgent protective duties in week one.

In many cases, it is safer to place a temporary “Hold Mail” request with the postal service rather than immediately forwarding the mail to your own address. Forwarding mail can sometimes trigger automated address-change updates with banks and credit card companies. If those institutions detect an address change before you have officially notified them of the death, it can trigger fraud alerts and lock down the accounts, making your job much harder.

By holding the mail at the post office, you keep the property looking occupied and secure the documents in a federal facility until you are ready to pick them up and process them carefully.

Move 7: Schedule Decision Checkpoints for Week Two

Once the physical property and mail are locked down, the next biggest risk is not financial. It is familial. Executorship is a marathon, not a sprint, and people will have urgent questions about when they will receive money, what is happening to the house, or who gets specific personal items.

You need a standard, polite response that buys you time to organize. It is perfectly acceptable to defer questions while you get the administrative foundation in place.

Subject: Update on estate next steps

Hello family,

Thank you all for your support right now. I am currently taking the first administrative steps to organize the estate files and secure the house.

Right now, we are in a holding pattern while I gather the necessary documents. I will not have any specific answers about accounts or personal items for the next few weeks as I work through the initial process. I will send another update by [Date] once I have a clearer timeline.

Best regards,

[Your Name]

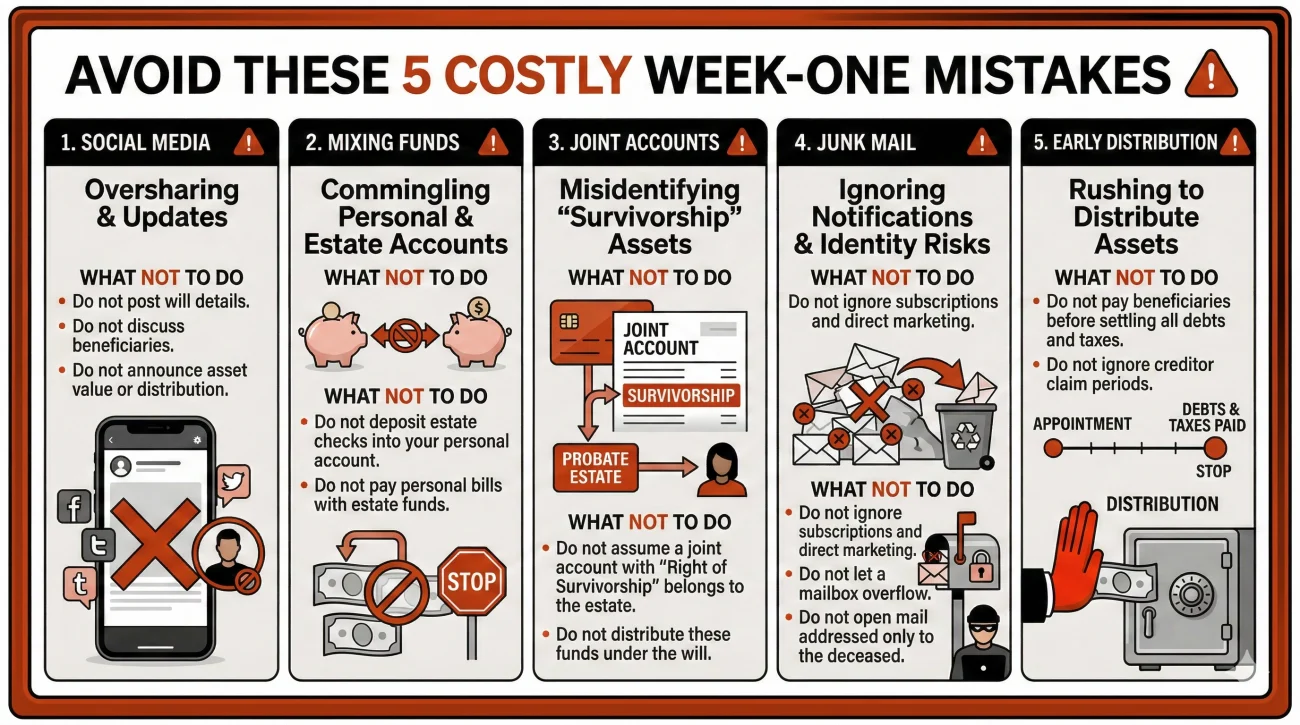

Common Week-One Mistakes

When executors feel rushed, errors happen. Avoiding these common early missteps will save you weeks of corrective work down the line.

Announcing the Death on Social Media Too Early

Posting a public tribute on Facebook or Instagram before the house is physically secured is a major security risk. Unfortunately, burglars and scammers actively monitor obituaries and social media to target empty homes. Secure the property first before making widespread public announcements.

Mixing Personal and Estate Funds

The most frequent mistake I see is an executor paying for the deceased’s utilities, mortgage, or final bills using their own personal checking account. While well-intentioned, this creates a tangled accounting mess. In most cases, bills can wait a few weeks until you have proper authority to access the estate’s funds to pay the estate’s debts.

Misunderstanding Joint Accounts

Many people assume that if a bank account is held jointly, it automatically transfers without any paperwork. While joint accounts generally bypass probate, you still must formally notify the bank, provide a death certificate, and have the deceased person’s name removed to properly update the tax reporting status.

Throwing Away “Junk” Mail Too Quickly

Do not be quick to shred unsolicited mail in the first week. What looks like a generic flyer from an insurance company might actually be the only notice of a premium due on a valid life insurance policy. Keep all mail in a designated box for at least thirty days before deciding what is truly garbage.

Distributing Items Without a Record

Allowing relatives to take books, furniture, or small items from the house during the first week is a major pitfall. Distributing property before you have a full inventory can create friction among beneficiaries and violate your duty to protect the estate. Simply state that everything must remain in place until the formal inventory is complete.

Mini-Template: Week-One Tracker

When you are overwhelmed, breaking tasks down by the day helps reduce anxiety. Here is a visual sequence of how these tasks map out over the first seven days:

- Days 1 to 2: Physical security (locks, keys, video inventory).

- Days 2 to 3: Stop vulnerabilities (post office mail hold).

- Days 3 to 5: Organization (set up folders, find the will, start call log).

- Days 5 to 7: Discovery and communication (build institution list, email family).

Use this basic table to track your stabilization efforts. You can copy this structure into a spreadsheet or draw it in your notebook.

| Priority Task | Target Date | Status / Notes |

|---|---|---|

| Secure primary residence keys/locks | Day 1-2 | |

| Take video inventory of all rooms | Day 1-2 | |

| Place 30-day hold on mail | Day 2-3 | |

| Set up physical and digital file folders | Day 3-4 | |

| Locate original will and important papers | Day 4-5 | |

| Draft list of known accounts/institutions | Day 5-6 | |

| Send update message to beneficiaries | Day 7 |

Final Thoughts on the First Week

The first week after a loss is intensely overwhelming, and stepping into the executor role can feel like carrying a weight you did not train for. Remember that patience is your strongest asset right now. If you feel pressured to fix everything immediately, step back.

By prioritizing property security, establishing your document tracking habits early, and setting realistic boundaries with family members, you are doing exactly what a responsible executor should do. Do not let the urgency of incoming mail or demanding phone calls dictate your pace. Set up your tracking logs, protect the assets, and trust that a slow, methodical start is the best way to prevent months of administrative chaos later.

❓ FAQ

📅 How long do I actually have to start the executor process?

There is no universal 24-hour deadline to begin probate. While you should secure the property and find the will quickly, filing official court paperwork can usually wait several weeks. Always check your local court’s website, but do not feel rushed to file on day one.

📞 What do I say when I call the bank to report a death?

Keep it brief. Inform them of the passing, ask them to place a note on the account, and request a written list of their specific requirements to close the account later. Do not try to move money or access funds during this initial call.

💸 Who pays for the funeral if the bank accounts are frozen?

Many banks will allow funeral expenses to be paid directly from the deceased’s frozen account if you present a valid invoice from the funeral home. Alternatively, a family member can pay upfront and be reimbursed by the estate later once funds are accessible.

🐕 What should I do with the deceased person’s pets?

Immediate care is the priority. Arrange for a trusted friend, family member, or temporary boarding service to care for the pets. Pets are technically considered property of the estate, so keep records of any money you spend on their care for future reimbursement.

💻 Can I use their phone or computer to cancel subscriptions?

Logging into someone else’s accounts using their passwords often violates terms of service. Instead of trying to hack into twenty different accounts, it is usually faster and safer to simply cancel or freeze the underlying credit card paying for those subscriptions.

🗄️ Do I need to keep every single piece of medical mail?

Yes, for now. Keep all Explanation of Benefits (EOB) letters and medical bills in a specific folder. Do not pay them yet, as medical debt is often negotiated or settled differently through the probate process down the line.

🤝 If I am a co-executor, who should make the phone calls?

You should nominate one person to be the primary point of contact for institutions. If both co-executors call the same bank on different days, it creates duplicate records, confuses representatives, and drastically slows down your requests.

📝 Is a printed online bank statement enough for probate?

An online statement is great for your discovery phase in week one. However, courts and agencies will eventually require an official “Date of Death Balance Letter” generated directly by the bank to prove the exact value of the account on the day they passed.

🚗 Should I cancel the car insurance right away?

Absolutely not. The vehicle still needs coverage against theft, fire, or damage while it is sitting in the driveway. Wait to cancel or change the auto insurance policy until the vehicle is formally sold or transferred to a beneficiary.

🛑 How do I politely tell family members to stop asking for money?

Blame the legal process. You can simply say, “I am legally required to freeze all distributions until the court and creditors are satisfied. I will keep everyone updated, but nothing can be moved right now.” Put this in writing to set a firm boundary.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.