- Most executors find that ordering between 5 and 10 certified copies covers a standard estate, while more complex estates may require 15 or more.

- Timing matters just as much as volume: institutions often reject copies issued more than 60 to 90 days ago, so avoid ordering massive batches too early.

- You can accurately estimate your needs by counting major asset categories, explicitly factoring in modern hurdles like digital accounts and crypto exchanges.

- Not every institution will keep your certified copy. Always actively ask if they can inspect the original and retain a photocopy to protect your inventory.

The Reality of Proving Your Authority

When you step into the role of executor, you quickly realize that your word alone is not enough to move the process forward. Third parties require concrete proof that you have the legal right to act. This is where your official court documents come in. But a very common hurdle I see people hit right at the starting line is simply not having enough physical copies of that proof to go around.

If you are wondering how many certified copies of letters testamentary do i need, you are asking the exact right question at the right time. I often hear from people who ordered just one or two copies, thinking they could make photocopies at a local print shop. They end up stalled for weeks when a major financial institution demands an original seal and refuses to process a transfer without it.

In my experience supporting estate administration workflows, the flow of paperwork can be overwhelming. You want to strike a practical balance to maintain your momentum. This guide is built to help you calculate an accurate baseline. We will walk through how to estimate your document needs based on the actual assets, how to navigate the strict verification processes of modern platforms, and how to prioritize your copies if you start running low.

Before you dive into the math, it is always helpful to understand how this step fits into the broader picture of your responsibilities. I highly recommend reviewing our complete Probate Court Checklist for Executors to see exactly where acquiring these documents sits in your overall workflow.

Why Institutions Insist on Certified Documents

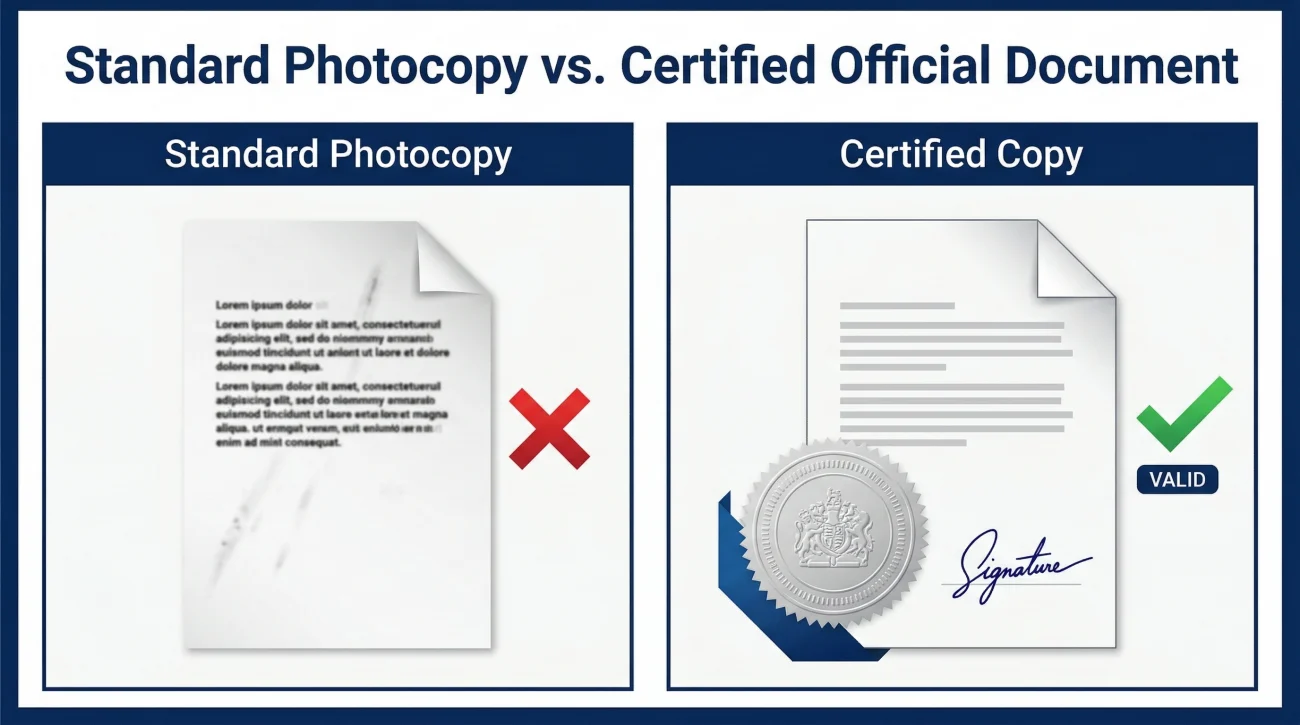

It is very common to feel frustrated when you hand over a crisp, perfectly legible photocopy of your court letters, only to be told it is unacceptable. To keep your administration moving, it helps to understand why the person on the other side of the desk is saying no.

A standard photocopy simply shows that a document existed at some point. A certified copy is different. It includes a physical raised seal, an ink stamp, or a specific watermark applied directly by the court clerk. This physical mark serves as an anti-fraud measure. It tells the third party that the document is authentic, unaltered, and currently recognized by the issuing authority.

When you ask yourself do banks require certified letters testamentary, the answer is almost always yes. Risk management departments at these institutions have strict protocols. They are handling sensitive financial transfers, closing accounts, and moving assets. If they release funds to someone without properly verifying their legal authority, the institution could be held liable for misdirected funds.

Key Point: Institutions are not demanding certified copies to make your job harder. They require them to satisfy their internal compliance and fraud-prevention policies before they can safely execute any irreversible actions.

Because these institutions rely entirely on the court’s validation to clear their own liability, you must ensure you are providing the correct type of authentication.

📌 Note: A common mistake is assuming a notarized photocopy is the same as a certified copy. A notary can only verify that a signature is authentic or that a copy matches an original in front of them. They cannot certify a court order. Only the court that issued the document can provide a valid certification.

The Baseline Rule of Thumb for Most Estates

Because every estate is uniquely structured, there is no single mandated number of copies you must acquire. However, we can use a baseline operational range to get you started. For a relatively simple estate, a safe starting point is typically 5 to 10 certified copies.

This range is not arbitrary. In a typical scenario, you will need one copy to permanently surrender to the title company for selling the primary residence, two copies to float between different local bank branches, one for the primary life insurance payout, and one for transferring a vehicle. That instantly consumes five copies. Having a few extras ensures that if one gets lost in the mail by a vendor, your entire workflow does not freeze.

If you are managing a more complex estate, you should adjust that baseline upward. A complex scenario might include multiple real estate properties in different counties (which often require separate court filings), investments held at several different brokerage firms, or numerous individual annuity contracts. In these cases, 10 to 15 copies may be more appropriate.

Whether you are asking about letters testamentary or wondering how many certified copies of letters of administration you need for an estate without a will, the calculation method remains exactly the same. The type of document does not change how third parties will scrutinize it.

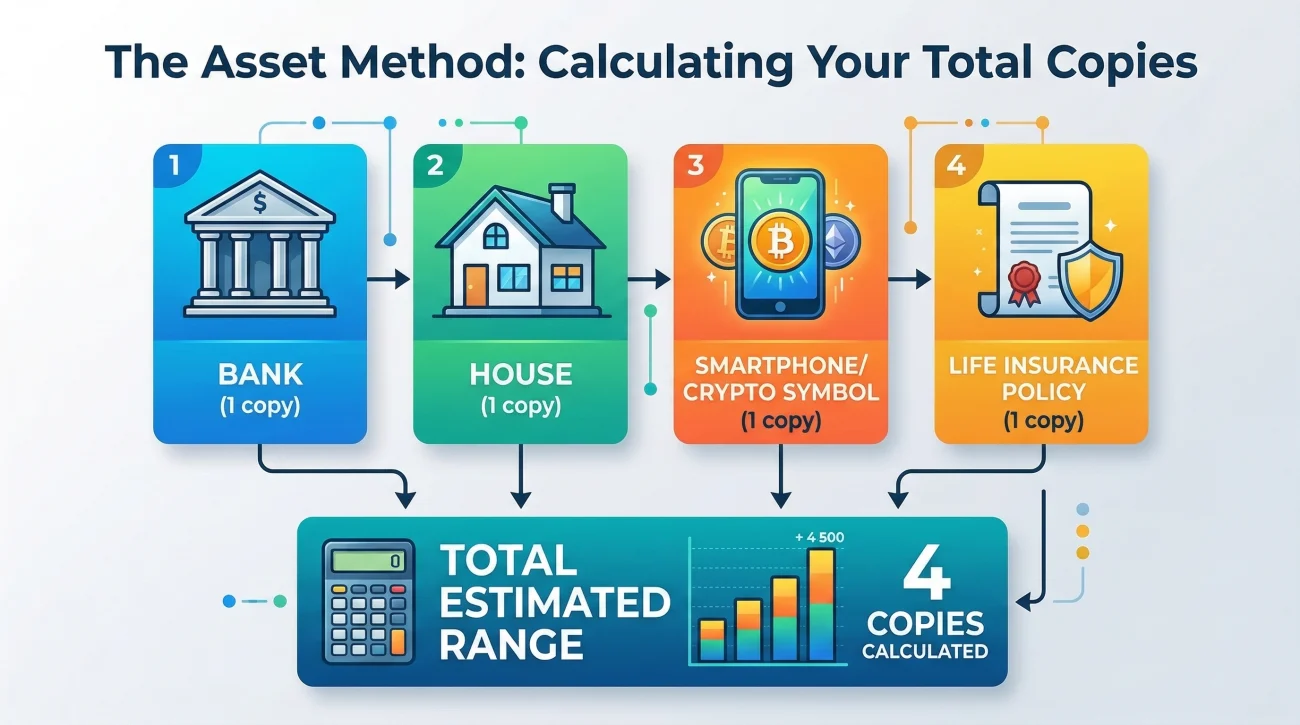

How to Estimate Your Needs: The Asset Method

Instead of guessing, the most reliable way to figure out your number is to map it directly to the estate’s inventory. Grab a notepad and start listing the entities that hold assets or require official notification of your authority. You will assign one potential copy to each major category.

| Asset or Institution Category | Estimated Copies Needed |

|---|---|

| Banking (Checking, Savings, Safe Deposit) | 1 per distinct financial institution |

| Real Estate and Title Companies | 1 per distinct property transaction |

| Brokerage and Investment Accounts | 1 per investment firm |

| Digital Assets and Crypto Exchanges | 1 per major platform (often strictly retained) |

| Life Insurance and Annuities | 1 per issuing company |

| Vehicles and DMV | 1 per state agency touchpoint |

It is crucial to note the distinction of “per institution” versus “per account.” If the deceased had three checking accounts and a credit card all under the exact same national bank brand, you usually only need to provide one certified copy to their centralized estate department to gain authority over all of those linked accounts.

One area where I see modern executors get caught off guard is digital assets. Cryptocurrency exchanges, online-only brokerages, and major digital platforms are notoriously strict about compliance. They almost never have a local branch you can visit to show your document in person, meaning you are forced to mail a physical original to their legal department, and they rarely return them.

💡 Pro Tip: Always keep one certified copy entirely untouched in your home filing system for “surprise” discoveries. It is incredibly common to uncover an out-of-state timeshare or an old, forgotten life insurance policy six months into the process. Having one clean master copy ready saves you from completely restarting the court request loop.

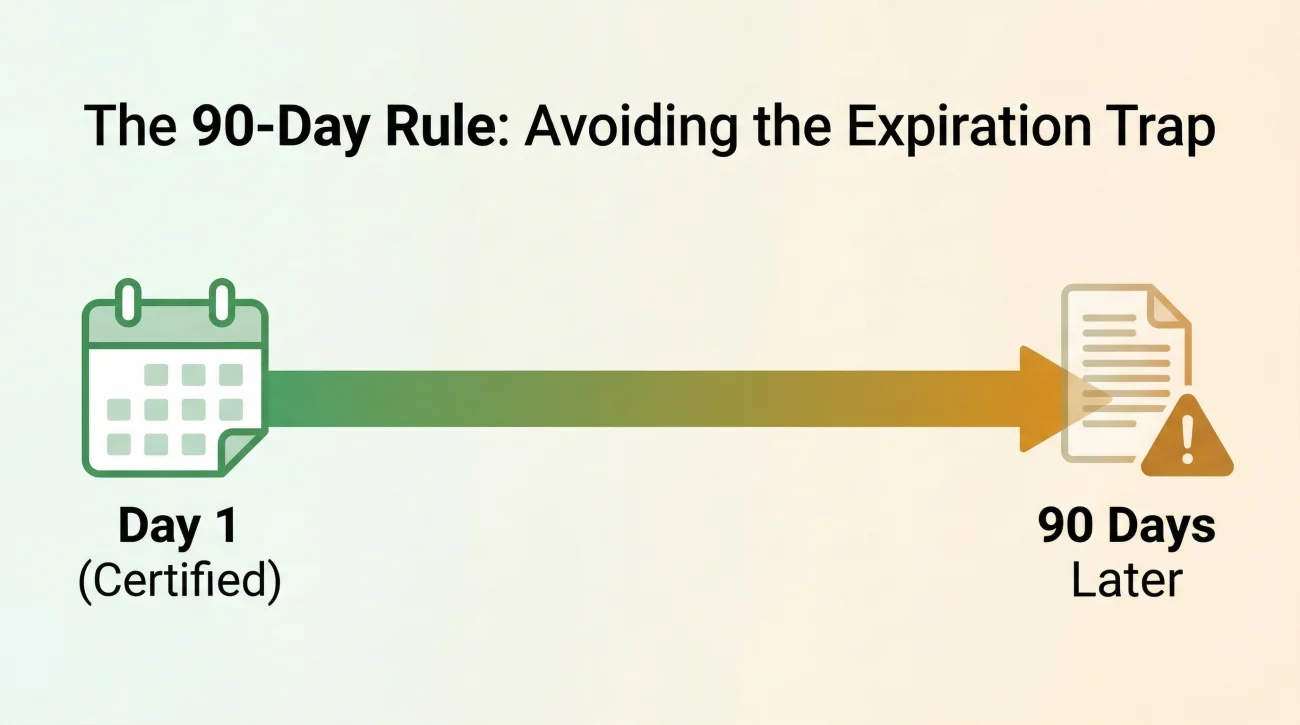

The Expiration Trap: When Timing Matters More Than Volume

A major nuance that catches many people by surprise is the concept of document staleness. While your underlying legal authority may not technically expire, the piece of paper itself effectively does in the eyes of financial compliance departments.

Many major banks and investment firms have strict internal policies stating they will only accept court documents that were certified within the last 60 to 90 days. If you order 30 copies on day one to “be safe,” but the estate involves complex real estate that takes eight months to sell, half of your expensive certified copies may be considered too old by the time you actually need to use them for final payouts.

Ordering 25 copies immediately after your court appointment, only to have institutions reject them five months later because the clerk’s stamp is “too old.”

Ordering an initial batch of 8 to handle immediate bank and insurance transfers, and planning to request a fresh batch later when it is time to close long-term investments.

This is why staggering your requests is often the smartest strategy. Use your initial batch to secure the primary bank accounts, establish the estate checking account, and secure the physical property. Once you are ready to tackle the secondary wave of asset liquidation months later, you can request a few fresh copies with a current date stamp to ensure smooth processing.

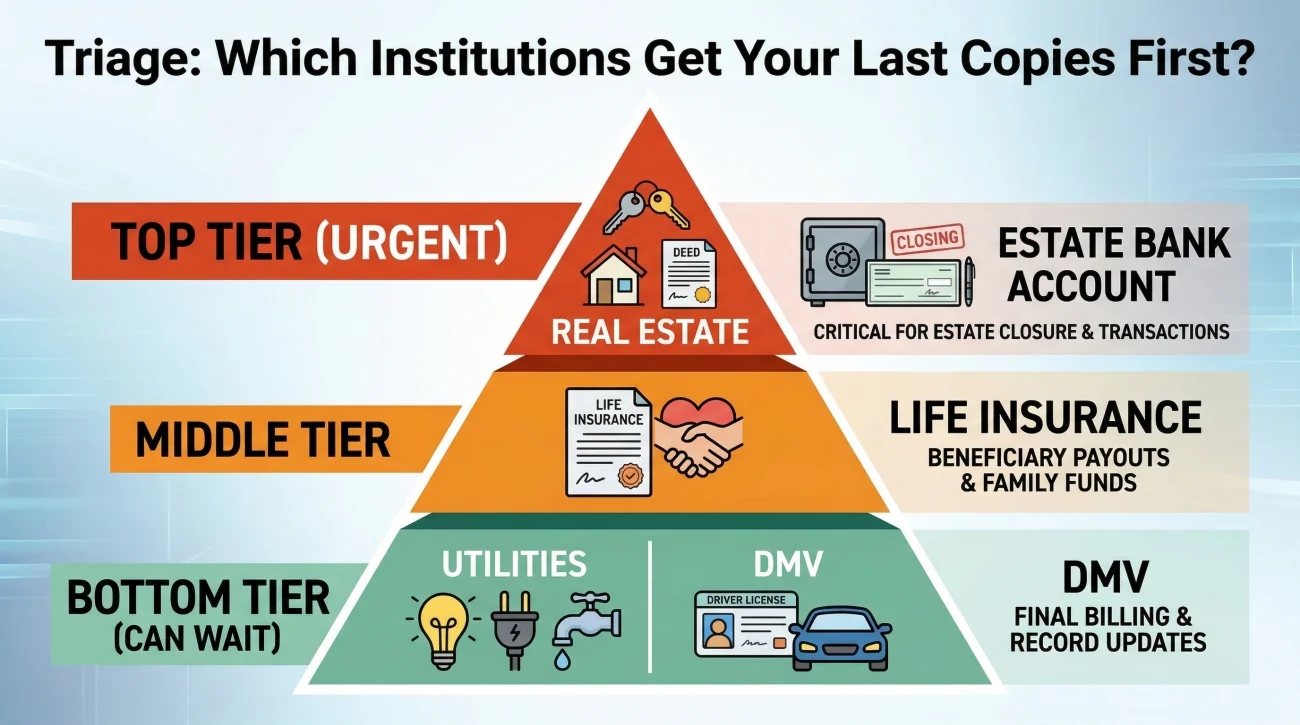

Prioritizing Copies When You Run Low

Even with careful planning, you might find yourself in a situation where you only have one or two certified copies left in your folder, but you have four different institutions asking for them. When this happens, you have to triage the requests based on their operational impact.

I find it most effective to prioritize transactions that have hard, legally binding deadlines or those that unlock significant liquidity for the estate. Real estate closings should almost always jump to the front of the line. Title companies will outright refuse to close a sale without an original copy for the county records, and missing a closing date can cost the estate money.

Next in line should be the primary estate bank account setup. You need a centralized place to hold funds to pay urgent bills, making this a high-priority transfer. Conversely, dealing with minor utility deposits, the DMV for an old vehicle, or closing a small subscription service can usually wait. Those entities are less likely to impose severe penalties for a few weeks of delay while you wait for fresh copies to arrive from the court.

The Document Tracking Habit

Once you have your stack of certified documents, the next operational challenge is keeping track of them. If you hand them out without logging where they went, you will quickly lose count of your remaining inventory and lose control of the workflow.

I always recommend setting up a dedicated document tracking log inside your primary executor notebook or a simple spreadsheet. Instead of just noting that you “sent paperwork to the bank,” you want to be precise. Log the date it left your control and the specific department that received it. Note the delivery method, especially if you used a tracking number, and clearly mark whether you expect that copy back.

This level of tracking hygiene saves an enormous amount of stress when disputes arise. If a title company claims they never received your authorization packet, you do not have to guess. You can check your log, pull the certified mail tracking number, and confidently confirm exactly when it was signed for. It transforms you from someone simply reacting to demands into someone actively managing the flow of information.

Communication Scripts to Preserve Your Copies

The best tracking system in the world won’t help if every institution keeps your paperwork permanently. One of the most effective ways to stretch your inventory is to aggressively protect the copies you have.

When you are preparing to communicate with an institution via mail, you can use a clear, polite script to clarify their retention policy before you drop anything in the post.

Subject: Document requirements for estate administration processing

Hello,

I am preparing the required document packet to update the file for this account. Your instructions mention providing my court letters of authority.

Could you please clarify your document retention policy? Do you require a physical certified copy to be kept permanently in your files, or can your department inspect the certified copy and return it to me via mail once processing is complete?

Thank you for your guidance.

If you are standing at a desk in person, the approach is even simpler. You want to present the document while verbally maintaining control of it.

“I have my official court documents here. Are you able to verify the seal, make a copy for your system, and return this original to me today?”

Using these communication habits means a single certified copy can sometimes do the work of three or four, traveling to different vendors and returning to your central file. Certain entities, particularly government agencies handling real estate recordings, will almost always keep the document permanently for the public record. But for standard financial maintenance, asking the question is a zero-risk way to protect your inventory.

Final Thoughts on Document Logistics

Handling estate paperwork is less about knowing the law and much more about mastering logistics. By treating your certified documents as limited physical assets, you protect yourself from unnecessary delays and extra trips to the courthouse.

The goal is to eliminate friction. Taking the time to count your asset touchpoints, stagger your orders to avoid the expiration trap, and fiercely track where every piece of paper travels will put you in a position of control. When you can confidently tell a vendor exactly when their legal department received your packet, you establish a tone of competence that makes the rest of your administrative duties significantly smoother.

❓ FAQ

🤔 Do I need a separate certified copy for every single bank account?

Usually, no. If multiple accounts are held at the exact same financial institution, one certified copy provided to their central estate or risk department is often enough to cover all linked accounts under that brand.

📮 Can I just make my own photocopies of the letters testamentary?

You can make photocopies for your own reference or for informal communications, but third parties like financial firms and title companies will generally reject standard photocopies for official transfers. They require the raised seal or stamp applied by the court.

🏦 Do banks require certified letters testamentary to close an account?

Yes, in almost all circumstances. Closing an account involves releasing funds, and the bank must verify your legal authority to receive those funds to comply with fraud prevention protocols.

🏛️ Where to get certified copies of letters testamentary if I run out?

You must request additional copies directly from the clerk of the specific court that originally granted your appointment. You cannot get them from a notary or a different county office.

⏳ How old can a certified copy be before it expires?

While the authority itself may not expire, many financial institutions have internal policies requiring the certification stamp to be recent, often dated within the last 60 to 90 days. Always verify the institution’s specific timeline requirements.

📄 How many certified copies of letters of administration are usually needed for a house sale?

You typically need at least one dedicated copy for real estate transactions. Title companies and county recording offices generally require an original certified document to be filed permanently with the property records.

🚗 Do the department of motor vehicles usually keep the certified copy?

It depends entirely on local branch procedures. Some clerks will verify the seal and return the document, while others are required to retain it with the vehicle transfer paperwork. Always ask before handing it over.

✉️ Should I mail my certified copies or provide them in person?

Providing them in person allows you to ask the representative to verify the seal and return the document immediately. If you must mail them, always use a trackable shipping method to ensure the document is not lost in standard transit.

💼 Can a financial advisor use a scanned PDF of my certified letters?

An advisor might use a scan to begin reviewing the account and preparing internal paperwork, but the actual compliance department that authorizes the release of funds will almost certainly require the physical certified copy before final execution.

🔄 Will institutions ever mail the certified copy back to me?

Some institutions will return the document if you explicitly request it in writing when you submit your packet. However, you should never assume it will be returned automatically; always clarify their retention policy first.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.