- Your immediate job is to locate and inventory the business paperwork without accidentally mixing estate funds with operating funds.

- Start by following the paper trail. Tax returns (Schedule C or K-1 forms) and basic corporate formation documents prove the business exists.

- Modern estates often include digital businesses. You must actively look for 1099-K forms, merchant accounts, and domain renewal receipts.

- Prioritize finding the Operating Agreement and any Buy-Sell Agreements. These act as the rulebook for what happens to the shares next.

The Complexity of Inherited Business Assets

When I sit down with someone who has just taken on the role of an executor, there is usually a moment of quiet panic when they open a piece of mail and see an “LLC” or “Inc.” attached to the deceased person’s name. Sorting through personal bank accounts is one thing, but dealing with a business feels like stepping into a minefield of liability.

I always start by telling them to take a deep breath. In the early days of estate administration, your goal is simply to build a comprehensive business interests inventory checklist. You are on a fact finding mission. You just need to figure out what exists, gather the paperwork that proves it, and put it in a safe place.

In my experience, the biggest mistakes happen when executors try to do too much too soon. They try to interpret complex shareholder agreements or accidentally mix personal estate money with business operating funds. This guide is built to help you avoid those traps. We are going to walk through exactly how to find these assets, prioritize the document search, and list them cleanly.

What Actually Counts as a Business Interest?

Before you can inventory anything, you need to know what you are looking for. Often, people assume a “business interest” means a brick and mortar store with employees. While that is certainly true, the reality of modern estates is usually much more subtle.

When I review an estate business documents checklist, I look for a wide variety of income generating structures. The structure dictates how complex the inventory will be.

Common Types of Business Assets

- 📄 Sole Proprietorships: The deceased operated a freelance consulting gig or a service under their own name. This is closely tied to their personal liability.

- 📄 Single Member LLCs: A formal business entity where the deceased was the only owner. Very common for independent contractors.

- 📄 Partnerships and Multi Member LLCs: The deceased owned a percentage of a business alongside other living people.

- 📄 Closely Held Corporations: Private shares in a family business that are not traded on public stock exchanges.

Key Point: Even if the business was losing money or barely operating at the time of death, you still must document its existence. You cannot simply ignore it because it seems inactive.

How to Find the Hidden Business Assets

Sometimes you know about the business because the deceased talked about it every day. Other times, it is a complete surprise. I have worked on cases where the family had no idea the deceased owned a 15 percent stake in a local commercial property until a random tax document showed up in the mail six months later.

To build an accurate executor business assets checklist, you have to follow the administrative exhaust that every business leaves behind.

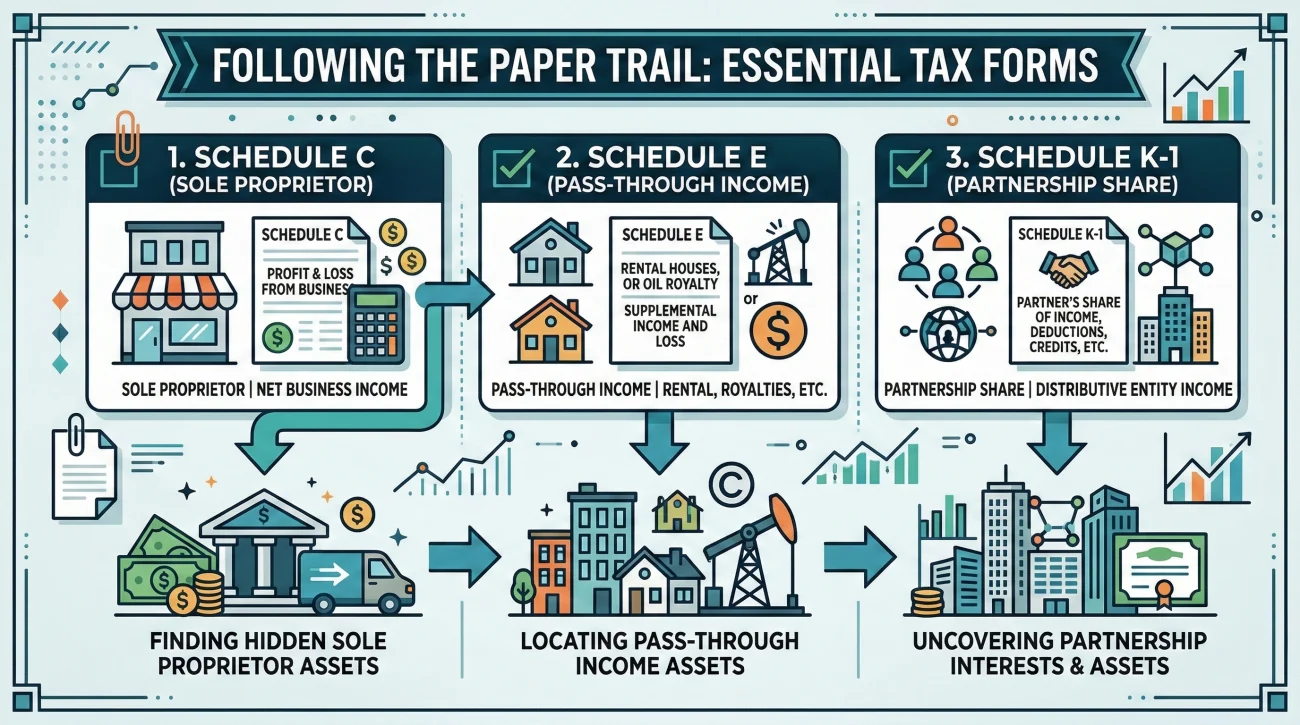

Following the Tax Trail

The absolute best place to start is the deceased person’s recent tax returns. Tax documents rarely lie about income sources. If you can locate the tax returns from the last three years, look for these specific forms:

- ✅ Schedule C: This indicates profit or loss from a sole proprietorship. If you see this, they were running a business without a formal corporate wrapper.

- ✅ Schedule E: This often shows income from rental real estate, royalties, or pass through entities.

- ✅ Schedule K-1: This is the golden ticket. A K-1 form proves that the deceased was a partner or shareholder in an LLC, partnership, or S-Corporation. It will usually list the exact name of the entity and the percentage of ownership.

Requesting Information from the CPA

If you cannot find the physical tax returns, your next step is to contact the deceased person’s accountant. You just need the raw data to add to your inventory right now.

Subject: Estate of [Deceased Name] – Request for Recent Tax Records

Hello [Name of CPA],

I am the acting executor for the estate of [Deceased Name]. As part of my initial duties, I am building a complete inventory of all assets, including any business interests or private shares.

Could you please provide a secure copy of the personal tax returns for the last three years, along with any K-1 forms or business returns you have on file for them?

I have attached a copy of my appointment documents and the death certificate for your records. Please let me know what your process is for securely transferring these files.

Thank you,

[Your Name]

Whenever I write these requests, I stick to a strict structure to avoid endless back-and-forth emails. You can use this simple formula for almost any professional correspondence during the estate process:

[Action] + [What you need in writing] + [Confirmation request]

Notice how the email above follows this exact logic. We stated our action (building an inventory), listed exactly what we needed (returns and K-1s), and asked for their secure transfer process as the confirmation step. It leaves no room for confusion.

Hunting for Digital Business Assets

In recent years, I have seen a massive spike in estates where the primary business asset is entirely online. I have worked on cases where the most valuable asset was not a local bank account, but a monetized YouTube channel or an established e-commerce store. These can be highly valuable, but they are incredibly easy to miss because there is no physical office to walk into.

When I help executors untangle these digital footprints, I always remind them that you cannot simply look for traditional stock certificates here. You have to actively hunt for digital trails.

What to Look For

- 💻 Merchant Accounts: Look through their personal and business email for receipts or statements from Stripe, PayPal, Square, or Shopify. These platforms issue a 1099-K tax form if the account generated significant revenue.

- 💻 Monetized Content: Check for recurring deposits from Google AdSense (YouTube), Substack, Patreon, or Amazon Affiliate programs.

- 💻 Domains and Hosting: An established domain name can be a sellable asset. Search emails for GoDaddy, Namecheap, or AWS renewal invoices.

When you find these, log them in your inventory. Do not attempt to guess their passwords to log in, as that can trigger fraud alerts and permanently lock the accounts. Your goal is to document the account ID and the platform name.

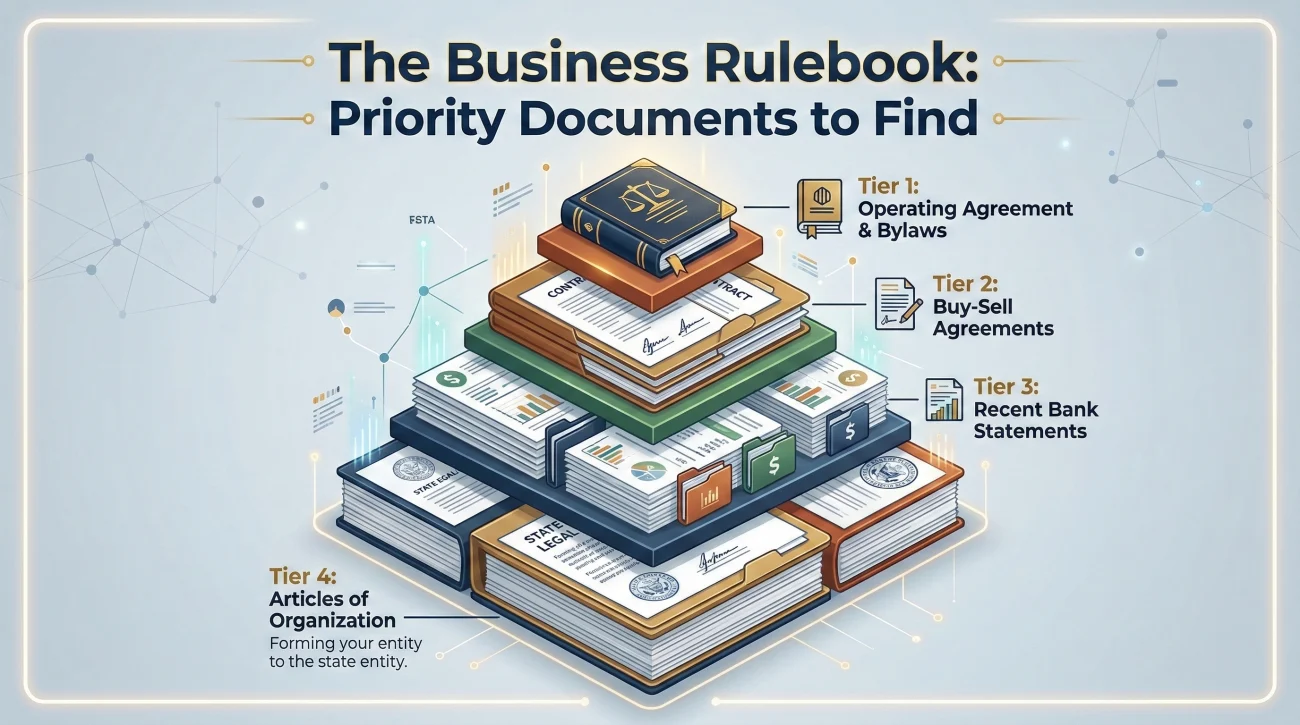

Triage: Core Documents to Locate

Once you know a business exists, you need to gather the governing documents. Think of this as collecting the rulebook for the company. When I help executors map out these document packets, I always advise them to prioritize the search so they do not get overwhelmed.

Week 1 Priority: The Rulebooks

These are the documents that dictate what happens right now.

- 📄 The Operating Agreement or Bylaws: This is the most critical document. In many cases, it contains a specific succession clause detailing exactly who gets the voting rights if an owner dies.

- 📄 Buy-Sell Agreements: This is usually a thick legal packet, sometimes labeled “Cross Purchase” or “Redemption Agreement”. It is a pre-signed contract among owners that dictates how shares must be bought out by the surviving partners upon death.

- 📄 Recent Bank Statements: Secure the last three months of statements for any business checking accounts to understand the cash flow.

Week 2 Priority: The Foundation

These items prove the business structure.

- 📄 Articles of Organization: The official state filing that created the business.

- 📄 EIN Assignment Letter: The document from the IRS showing the official tax ID number.

💡 Pro Tip: Before you spend hours calling state agencies to get copies of formation documents, check the deceased’s email inbox. Search for terms like “Operating Agreement”, “State Filing”, or “Registered Agent”. Owners almost always email these PDFs to themselves.

Handling Minority Holdings and Private Shares

Transitioning from tracking a storefront to tracking a silent partnership requires a mindset shift. If the deceased was an angel investor or held private shares in a startup, the evidence usually lives entirely on paper.

This falls under the umbrella of a shares and ownership documents checklist.

Where to Look for Proof

For older companies, you might actually find physical stock certificates in a safe deposit box. They often have intricate borders and gold foil seals. Do not throw these away, even if the company name has changed. They are vital proof of ownership.

For modern startups, ownership is tracked digitally on a Cap Table (capitalization table). You will need to look for an “Investor Rights Agreement” or a “Subscription Agreement” in their files.

If you know they were a minority partner but you cannot find the paperwork, keep your communication with the company incredibly brief and focused only on document retrieval.

Subject: Estate of [Deceased Name] – Request for Corporate Records

Hello [Managing Partner Name],

I am writing to you as the executor of the estate for [Deceased Name]. As part of my legal duty to inventory all assets, I am collecting documentation regarding their ownership stake in [Company Name].

Could you please provide a copy of the current Operating Agreement, any existing Buy-Sell agreements, and the most recent K-1 issued to them?

Please let me know if you need to see my official appointment documents before releasing these records.

Thank you for your help during this process,

[Your Name]

Notice how we are relying on the exact same communication formula here: [Action] (collecting documentation) + [What you need in writing] (Operating Agreement, Buy-Sell, K-1) + [Confirmation request] (asking if they need to see your appointment documents). By sticking strictly to this formula and removing any emotion, you force the surviving partners to respond to administrative facts rather than getting defensive about the business operations.

Red Flags: When to Stop Fact Finding

When you are building your business ownership records after death, you must watch out for situations that require immediate legal intervention. In my years of doing this, the worst messes I have seen always stem from an executor trying to “keep the business running” without legal cover. If you encounter any of the following scenarios, I strongly advise you to pause your inventory work immediately and flag the issue for your estate attorney.

⚠️ Warning: Do not attempt to sign any new business contracts, hire or fire employees, or transfer money out of the business accounts until you have clear, written legal guidance on your authority to do so.

Situations That Require Emergency Action

- 🛑 Active Payroll: If the business has employees expecting paychecks on Friday, and the deceased was the only authorized signer, you need a court to grant emergency access to payroll.

- 🛑 Hostile Partners: If surviving business partners refuse to communicate or refuse to hand over the operating agreement, stop emailing them. Let the attorney handle the document requests to avoid escalating the conflict.

- 🛑 Expiring Licenses: If the business relies on a specialized professional license that belonged only to the deceased, the business may legally have to pause operations immediately. I have seen companies face severe fines for operating a day after the licensed owner passed.

- 🛑 Personal Guarantees: If you find documents showing the deceased personally guaranteed a business loan or lease, the estate itself may be liable for that debt.

Trying to read a 50 page operating agreement to figure out if you are allowed to sell the business equipment to pay for the funeral.

Scanning the operating agreement into your secure folder and emailing it to the lawyer with a note saying, “Please advise on what this says about selling assets.”

The Business Interest Inventory Tracker

Once you have navigated those tricky document requests and safely bypassed any legal red flags, you need a central place to organize your findings. A scattered pile of K-1s and formation documents is useless. You need a structured format that you can present when a professional asks, “how to inventory business ownership for an estate?”

This tracking row will eventually become a sub section of your main estate inventory. If you have not set up your master system yet, review the estate asset inventory checklist to see how all these pieces fit together.

Here are the core columns you should use to log your findings:

| Entity Name & Type | Estimated Ownership % | Known Partners/Contacts | Document Evidence Located | Current Status / Next Step |

|---|---|---|---|---|

| Smith Consulting LLC (Single Member) | 100% | None | Articles of Org, 2022 Tax Return | Pending attorney review of operating agreement. |

| Main Street Properties LLP (Partnership) | 25% (per K-1) | John Doe (Managing Partner) | 2022 K-1, Need Operating Agreement | Emailed John Doe on 10/12 requesting docs. |

| Tech Startup Inc. (Private Shares) | Unknown | Jane Smith (CEO) | Email mentioning share purchase in 2019 | Flagged for attorney to send formal inquiry. |

Final

Closing an estate that includes business assets is a marathon, and the inventory phase you are in right now is just mile one.

Your power in this process comes from organization. By focusing strictly on the paper trail, capturing the right documents early, and keeping a meticulous log, you are setting the stage for a clean evaluation.

Once your tracker is populated, your immediate next step is to hand this exact log, along with your secure folder of operating agreements, directly to the estate attorney or business appraiser. Let them take the wheel on interpreting the rules and negotiating with surviving partners. Your job here is done, and you can safely move on to inventorying the rest of the physical estate.

❓ FAQ

🗂️ How do I find a business if there are no tax returns available?

Monitor the deceased person’s physical mail and email for invoices from a Registered Agent, state franchise tax board notices, or domain name renewal receipts. These are recurring expenses that every business must pay to stay active.

🏢 What happens to the daily operations of an LLC when the sole owner dies?

Unless the Operating Agreement specifies a succession plan or appoints a manager upon death, the business operations usually freeze. Banks will lock the accounts once they are notified of the death to prevent unauthorized transactions.

💻 How do I inventory an Amazon or Shopify e-commerce store?

Locate the Merchant ID number found on their monthly statement emails or 1099-K tax forms. Record the platform, the store URL, and the associated email address in your digital inventory log.

🏦 How do I handle a business bank account that is still receiving customer payments?

Do not close the account immediately. Notify the bank of the death and present your executor appointment documents. The bank will typically leave the account open to receive incoming deposits but will restrict outbound transfers until legal authority is established.

📑 What does a Buy-Sell agreement actually look like?

It is usually a separate, multi page legal contract signed by all the business partners. It may be titled “Cross-Purchase Agreement” or “Entity Redemption Agreement” and often includes formulas for calculating how much the shares are worth.

📜 What if I find a physical stock certificate that looks really old?

Log the certificate number, the number of shares, and the company name exactly as printed. Even if the company was bought out or changed its name decades ago, a broker or transfer agent can trace the certificate’s current value.

🤝 How do I deal with a surviving business partner who will not share documents?

Send one polite, written request for the documents. If they ignore it or refuse, do not argue. Record the refusal in your tracker and pass the issue to the estate attorney, who can issue a formal legal demand.

📅 Is there a strict deadline to complete the business inventory?

While courts have general inventory deadlines, business assets should be identified as quickly as possible. Delays can result in missed tax filings, expired licenses, or a drop in the company’s valuation.

💰 Should I hire a business appraiser before talking to the lawyer?

No. Gather the documents first. The estate attorney will review the operating agreements and recommend an appraiser who specializes in that specific industry and meets court standards.

🛑 Can I pay the deceased person’s business debts from their personal estate account?

Never mix funds. Business debts should generally be paid from the business account, and personal debts from the estate account. Paying business debts with estate money can complicate accounting and expose the estate to unnecessary liability.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.