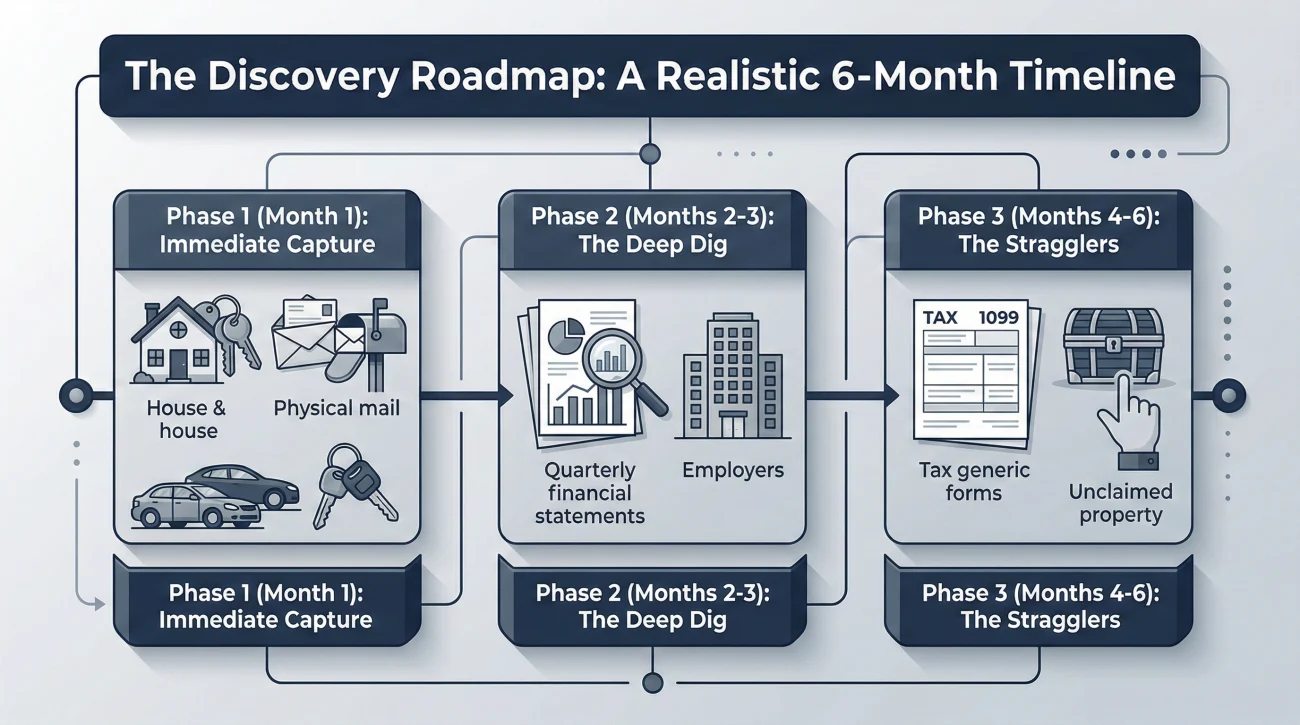

- Expect the discovery phase to take three to six months; use a structured timeline rather than rushing to find everything in week one.

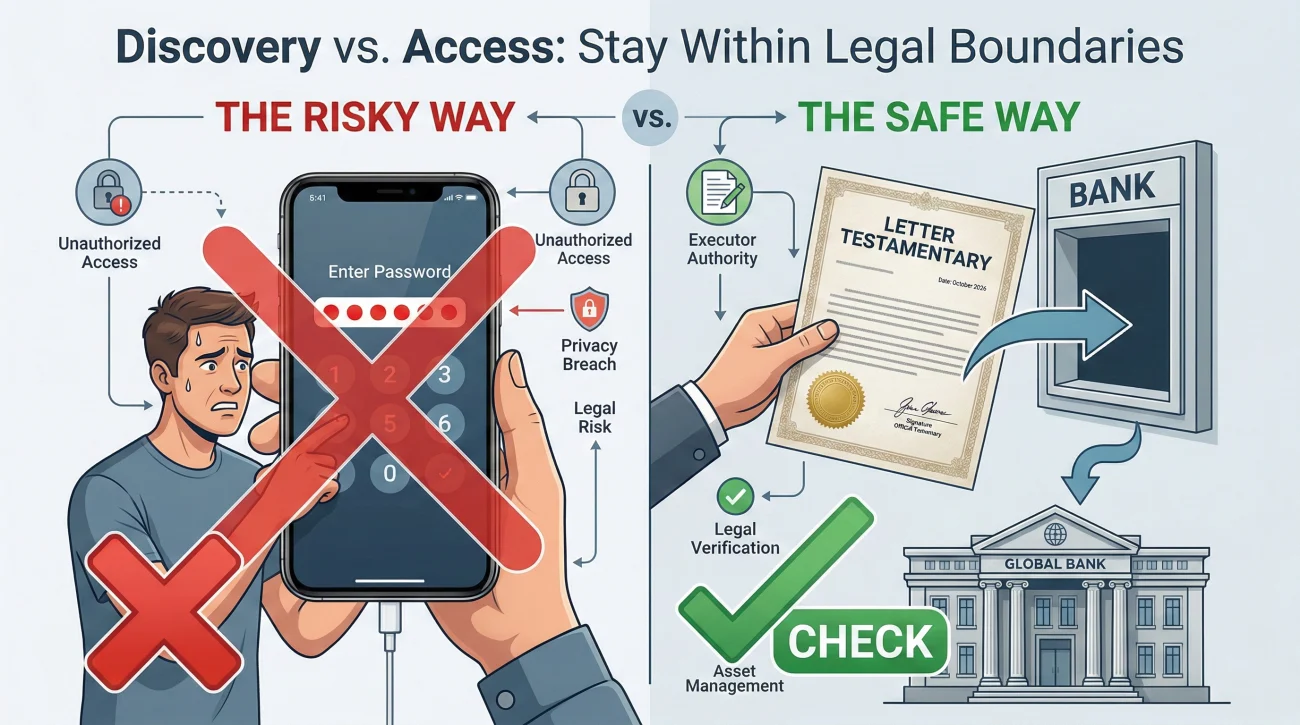

- Never bypass security by using the deceased’s passwords or Face ID; instead, secure physical devices and look for secondary clues like lock-screen notifications.

- If paper trails are non-existent, pull IRS Form 4506-T (Wage and Income Transcript) to force historical financial data into the light.

- When calling institutions, bypass the frontline tellers and ask directly for the “Estate Handling” or “Deceased Accounts” department.

- Run a mandatory check on national unclaimed property databases (like MissingMoney) around month six to catch forgotten utility deposits and old accounts.

The Reality of Uncovering a Scattered Estate

One of the most overwhelming moments for any executor is sitting down at a desk, looking at a stack of disorganized papers, and wondering how to find all assets of a deceased person without missing anything critical. Over the years of supporting estate administrations, the most common phone call I receive starts with this exact sense of panic.

Here is the reality: in about 8 out of 10 cases I see, there is no master list. Even highly organized people leave behind fragmented financial lives. You might find a checkbook, but miss an online-only savings account. You might know about the house, but overlook a forgotten life insurance policy from a past employer.

Your goal right now is not to immediately transfer funds or close accounts. Your immediate job is simply discovery and documentation. In this guide, I will walk you through the exact, step-by-step search framework seasoned professionals use to map out financial accounts, physical properties, and hidden policies using official, verifiable methods.

A Realistic Asset Discovery Timeline

One of the biggest mistakes executors make is assuming they need to find everything before filing for probate. To reduce your anxiety, it helps to understand what a normal, healthy discovery timeline actually looks like in practice.

- ⏳ Month 1 (Immediate Capture): Securing the physical house, collecting mail, finding the latest tax returns, and logging obvious physical assets (wallet, cars, real estate).

- ⏳ Months 2 to 3 (The Deep Dig): Forwarding mail to catch quarterly statements, interviewing former employers and advisors, and sending official notification packets to known banks to request Date of Death (DOD) balances.

- ⏳ Months 4 to 6 (The Stragglers): Catching annual tax documents (1099s), investigating complex digital assets, and running unclaimed property searches for long-forgotten funds.

Treat this as a phased operation. If you do not have all the answers on day ten, you are not failing; the system is simply taking its natural course.

Hard Boundaries: Discovery vs. Access

Before you start your investigation, we need to establish the single most important rule of estate administration. A completely understandable reaction is to try and log into the deceased person’s phone, laptop, or banking apps to “just see what’s there.”

⚠️ Warning: Do not use the deceased person’s usernames, passwords, Face ID, or fingerprints to access their financial accounts. This violates institutional terms of service and will complicate your legal standing.

Financial institutions run sophisticated algorithms to detect unusual login behavior, especially if a death has been reported to the Social Security Administration. If a system flags a posthumous login, their fraud department will hard-freeze the account. I have seen families get locked out of desperately needed funds for months because someone tried to bypass the official process.

Guessing a password to log into an investment portal, triggering a fraud alert that requires weeks of extra legal affidavits to unlock.

Finding a statement, logging the account number, and sending an official notification with your Letters Testamentary to request the balance.

What If They Lived a 100% Digital Life?

Increasingly, executors face a scenario where there is zero paper. The deceased opted out of paper mail, paid for everything via apps, and managed their life on a locked smartphone. How do you find assets when the paper trail does not exist?

Without bypassing security, you can still gather massive amounts of intelligence:

- ✅ Observe the Lock Screen: Keep their phone charged. Look for push notifications from banking apps, crypto exchanges, or automated investment platforms like Acorns or Robinhood.

- ✅ Check the Primary Checking Account: Once you gain official access to their main operating account, look at the outbound transfers. A monthly $500 transfer to an unknown entity is a glaring arrow pointing to an investment account.

- ✅ Look for Password Manager Bills: Check their credit card statements for annual charges to companies like 1Password or LastPass. Knowing a vault exists is the first step to requesting official access through the provider’s legacy contact process.

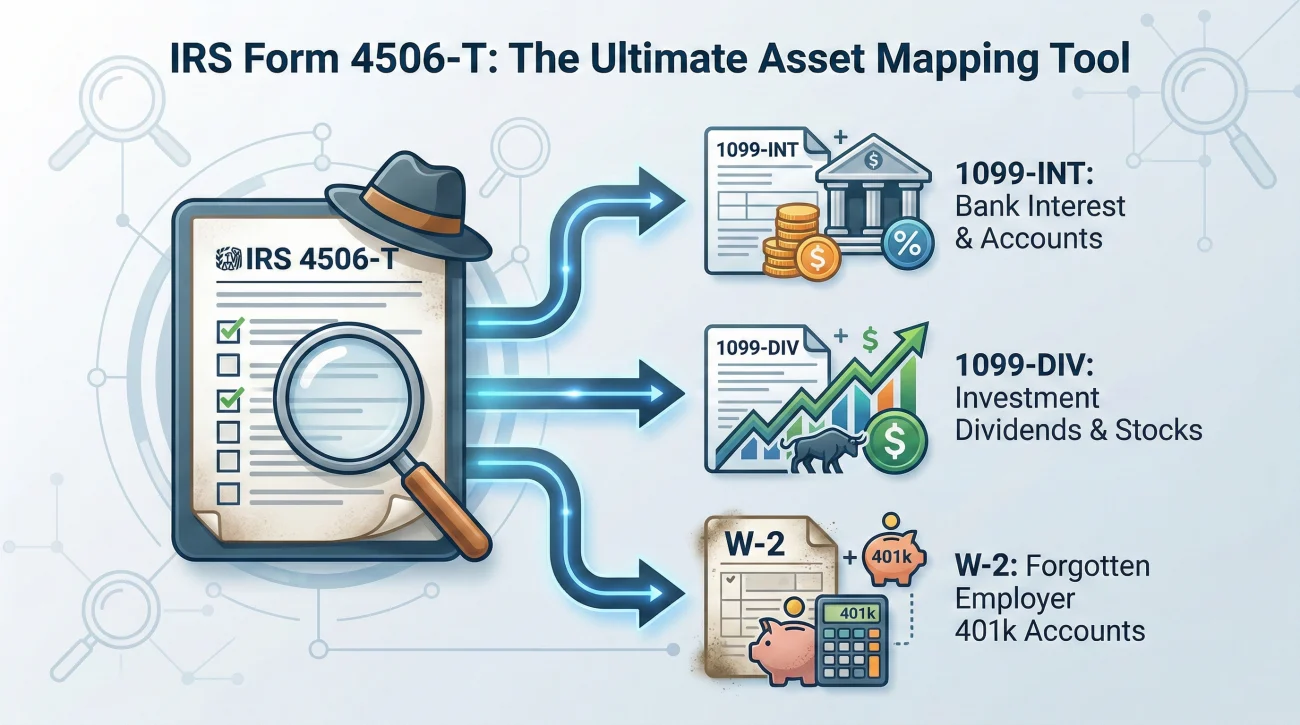

The Paper Trail: Using the IRS as Your Detective

If you do have access to paper, the single most valuable document you can find is the most recent tax return. Tax returns provide a historical snapshot of income-generating assets.

Look specifically for Schedule B (Interest and Ordinary Dividends). If they earned $10 in interest from a savings account, the name of the bank must be listed there. But what if you cannot find the tax returns?

💡 Pro Tip: If the paper trail is totally cold, you can file IRS Form 4506-T (Request for Transcript of Tax Return) as the authorized executor. Request the “Wage and Income Transcript.” This forces the IRS to hand over copies of every 1099 and W-2 reported by financial institutions against the deceased’s Social Security Number, giving you an exact map of where their money was held.

The People Trail: Advisors and Employers

Once the paper trail has been mapped, you must turn to the people who helped manage the deceased’s life. Often, professionals hold records of non-probate assets (like life insurance or 401ks) that bypass standard mail.

If the person was recently employed, their Human Resources department is a critical resource. Many people forget how to locate retirement accounts because they were set up decades ago and managed entirely through an employer portal.

Subject: Estate documentation inquiry for [Deceased Name]

Hello [HR Representative / Advisor Name],

I am acting as the executor for the estate of [Deceased Name], who passed away on [Date]. I am currently mapping all estate assets and benefits.

Could you please check your records and provide a written list of any active accounts, retirement plans, pensions, or group life insurance policies held on file for them?

Please reply with the exact documentation (e.g., Death Certificate, Letters of Office) you require from me to officially release account details.

Thank you for your guidance.

Notice the framing of this script. It does not demand money; it simply asks for a list and the institution’s specific requirements, establishing you as a professional, organized executor.

The Institution Trail: How to Talk to Banks

This is where many executors hit a wall. You have the name of a bank, you call the 1-800 number, and you get shut down by a customer service representative because of privacy laws. Frontline tellers and general support staff are not trained in estate administration.

Key Point: When contacting a financial institution, immediately bypass general support. State: “I am the executor of a deceased client. Please transfer me to your Estate Handling, Deceased Accounts, or Bereavement department.”

These specialized departments speak your language. When you reach them, you will need to prepare a standard documentation packet. While requirements vary slightly, you should always have PDFs ready of:

- 📄 The official Death Certificate

- 📄 Your court-issued authority document (Letters Testamentary / Letters of Administration)

- 📄 The Estate’s EIN (Employer Identification Number, obtained from the IRS)

- 📄 Your personal photo ID

Your sole objective in this first interaction is to request the “Date of Death Balance” for your inventory. You are not liquidating the account yet.

Handling Complex Digital Assets (Crypto)

In modern estates, uncovering digital assets goes beyond standard bank accounts. Cryptocurrency represents a massive risk area for executors. If you find a device that looks like a heavy USB thumb drive (such as a Ledger or Trezor device), or a piece of paper with 12 to 24 random words written on it (a seed phrase), you have likely found cold storage crypto.

Do not plug this device into your computer and try to guess the PIN. Many of these hardware wallets are designed to permanently wipe their data after three incorrect attempts. Your duty here is preservation. Secure the physical device in a safe, log its existence on your inventory, and consult a professional who specializes in digital asset recovery.

The Unclaimed Property Search (Crucial Step)

Around month four or five, after the initial dust settles, you must perform a sweep for unclaimed property. Every year, billions of dollars are turned over to state governments because institutions lose contact with the account holder. This includes uncashed payroll checks, forgotten utility deposits, and dormant savings accounts.

I remember working on a seemingly simple estate where we ran a routine check and uncovered a $42,000 Health Savings Account. The only clue it existed was a historical $3 maintenance fee that had been quietly draining a checking account years prior. The bank eventually lost contact and sent the funds to the state.

As the executor, you should search the official, free national database at MissingMoney.com (endorsed by the National Association of Unclaimed Property Administrators). Search using the deceased’s name in every state they have ever lived in. If you find a hit, the site will direct you to the specific state’s treasury portal to file an official executor claim.

Managing Beneficiary Expectations

One operational reality you will face is pressure from beneficiaries. Family members often have assumptions about “hidden millions” or secret accounts. When you do not find them immediately, suspicion can breed disputes.

The best way to protect yourself is absolute transparency regarding your process, not just your findings. By sharing your blank search logs and explaining the systematic steps you are taking (like requesting tax transcripts and monitoring mail), you shift the narrative. You show them that asset discovery is a rigorous, documented process, proving you are fulfilling your fiduciary duty responsibly.

Building Your Search Log

With information flowing in from the IRS, HR departments, and state databases, your memory will fail you. You must build a master search log. This log tracks who you contacted, when, and what the next action is, preventing duplicate work and missed follow-ups.

| Institution Name | Clue Source | Date Contacted | Status / Next Step |

|---|---|---|---|

| Example Credit Union | Schedule B on 2022 Tax Return | Oct 12 – Called Estate Dept | Mailing Letters & EIN Oct 15 |

| State Treasury (Unclaimed) | MissingMoney Search | Oct 14 – Submitted claim form | Awaiting claim ID via email |

Once an institution confirms an asset and provides the exact DOD balance, it moves off this temporary search log and onto your permanent estate asset inventory checklist. Keeping this strict workflow separates the “maybe” items from the verified, legal estate assets.

Commonly Missed Assets Checklist

As you conclude the active discovery phase, cross-reference your findings against these frequently overlooked items:

- 📄 Utility and Security Deposits: If the deceased rented an apartment or had long-standing utility accounts, there may be cash deposits held by those companies that belong to the estate.

- 📄 Health Savings Accounts (HSAs): These are often completely separate from standard health insurance portals and can hold significant funds that do not automatically transfer without documentation.

- 📄 Overpaid Medical Bills: If there was a long hospital stay before death, it is highly common for insurance adjustments to result in refund checks mailed to the estate months later.

- 📄 Safe Deposit Boxes: Check bank statements for annual box rental fees. You will need a specific appointment and your court documents to inventory the contents.

Final Thoughts on the Discovery Phase

Finding all the assets of a deceased person is a test of organizational endurance, not speed. By treating it as a structured investigation, leveraging tax transcripts, utilizing proper banking channels, and hunting for unclaimed property, you protect the estate and your own liability.

Stay disciplined with your search log, require all institutional requirements in writing, and remember that uncovering the full financial picture simply takes time. You will likely still face administrative hurdles and frustrating phone calls, but by building a documented map first, you ensure those inevitable challenges are manageable rather than completely overwhelming.

❓ FAQ

🏦 What happens if a bank account is not discovered until after probate is closed?

In many jurisdictions, the estate must be formally reopened through the court to grant the executor authority to claim and distribute the newly discovered funds.

💳 How do I stop automatic payments if I don’t know the login?

You do not need the login. Once you notify the bank of the death and provide the required documents, the bank will freeze the account, which automatically rejects all future ACH pulls and subscription charges.

📜 Can an executor request tax returns from the IRS if they are missing?

Yes. By filing IRS Form 4506 along with your Letters Testamentary, you can obtain copies of previously filed tax returns to help trace financial accounts.

🚗 How do I find out if there are liens against the deceased’s vehicles?

You can request a title record search through the state’s Department of Motor Vehicles (DMV), which will explicitly list any active lienholders or loans recorded against the vehicle’s VIN.

💼 Are pensions considered estate assets?

Most traditional pensions cease upon death or transfer to a surviving spouse via beneficiary designation, meaning they usually bypass the probate estate entirely. However, you must still contact the plan administrator to report the death.

🏠 How do I verify property ownership in another state?

Search the online property appraiser or county tax assessor databases in the specific counties where you suspect they owned property, using the deceased’s legal name.

🔒 What should I do with a safe deposit box key if I don’t know the bank?

Examine the key for a manufacturer stamp or numbering system, then check bank statements for annual rental fees. If nothing appears, you may have to call local bank branches near their home to ask if they hold an active lease under the deceased’s name.

📈 Do I need to value stocks on the exact day they died?

Yes, standard practice requires establishing the Date of Death (DOD) value for all assets. For fluctuating assets like stocks, this usually involves calculating the average of the high and low trading prices on that specific calendar day.

📱 Is it my job to download their personal photos from cloud storage?

While personal photos lack financial value, they hold immense sentimental value. Your duty is to secure the account (often through legacy contact features) to prevent deletion before the family can retrieve them.

🕵️♂️ Should I hire a private investigator to find hidden offshore accounts?

Unless there is highly credible, documented evidence of significant offshore wealth (like specific tax reporting forms), hiring a PI is generally an unnecessary estate expense. Focus on standard domestic paper trails first.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.