- Gather before acting: Collect ownership, mortgage, insurance, and tax documents into a single “property packet” before contacting lenders or title companies.

- Scope of this step: This is an organization and indexing process. We are locating paperwork, not transferring titles or listing the house for sale.

- Index everything: Build a master index table to track which documents you have, what is missing, and where the physical copies are stored.

- Maintain insurance: Locating the current homeowners insurance policy is an immediate priority to ensure the property remains covered while unoccupied.

Why a Messy Property File Stalls the Entire Estate

When someone passes away, their home is often the largest single asset in the estate. It is also usually the one with the most paperwork attached to it. From deeds and property tax bills to obscure utility records and homeowners association rules, the paper trail can feel endless. In my experience working through estate administration workflows, I frequently see progress grind to an absolute halt simply because a single document is missing from the file.

It is incredibly common for an executor to jump straight to asking, “How do I sell this house?” or “How do I transfer the deed?” But before any professional, be it a real estate agent, an attorney, or a title company, can help you answer those questions, they need proof. If you approach them with a disorganized shoebox full of loose mail and old receipts, the process will immediately drag. You will face repeated requests for the same information, delays in verifying ownership, and potential lapses in essential services like insurance.

This real estate documents checklist is designed to help you methodically gather, categorize, and index every piece of paper related to the property first. By building a clean property packet early, you protect yourself from the constant stress of digging through filing cabinets every time a new question arises.

Establishing Boundaries: What This Checklist Does Not Cover

Before we start organizing files, it is crucial to set a hard boundary on what we are doing in this stage. Staying within your lane as an executor is the best way to keep your stress levels manageable.

❌ Note: This guide does not cover how to transfer a property title, how to interpret local real estate laws, or how to prepare a house for the market. Those steps require specific legal and real estate professionals.

Our only goal right now is documentation. We want to secure the records, understand what the deceased person owned, and figure out what obligations (like mortgages or taxes) are attached to the house. Once you have this property packet built, you will integrate these findings into your master estate asset inventory checklist. Having the documents indexed makes filling out your master inventory incredibly easy.

Layer 1: Ownership and Title Documents

The foundation of your property packet is proving that the deceased person actually owned the property, and understanding exactly how their name is listed on that ownership record.

One common misconception is that possessing a piece of paper automatically means it is the most current, legally binding version. People refinance, change titles, and put properties into trusts over the years. You want to gather what you can find at the house, but be prepared to verify it later against county records.

What to Look For

- 📄 The Deed: Look for documents labeled Warranty Deed, Quitclaim Deed, or Grant Deed. Pay close attention to the exact name on it. If it says “The [Name] Revocable Living Trust,” this property is governed by the trust, not the will, and you will need to locate that specific trust document.

- 📄 Title Insurance Policy: Usually a thick packet of papers from when the house was purchased or refinanced. This is incredibly helpful for future title searches.

- 📄 Property Survey: A map showing the exact boundaries of the land.

- 📄 Closing Disclosures or HUD-1 Statements: The final accounting paperwork from when the house was bought.

Many people keep their original deeds in a bank safe deposit box. If you suspect this is the case, be aware that you cannot simply show up with a key to retrieve it. You will generally need to present the death certificate and your official court appointment documents to the branch manager just to get access.

Key Point: If you cannot find the deed anywhere, do not panic. Deeds are public records. Log the missing document in your tracker and request a formal copy from the local county recorder’s office; it is a straightforward process.

Layer 2: Mortgage and Lien Records

Once you know they owned the house, you need to know who else has a financial claim to it. Lenders and creditors do not pause their requirements just because someone has passed away. Identifying debts attached to the property is a critical executor duty.

I often see executors assume a house is completely paid off because the deceased person was older, only to later discover a Home Equity Line of Credit (HELOC) that was being drawn against. You must hunt for the paper trail.

Debt Documents to Gather

- 📄 Recent Mortgage Statements: Look for the most recent monthly statement to find the account number, loan balance, and customer service contact info.

- 📄 Promissory Note: The original document outlining the terms of the loan.

- 📄 HELOC Statements: Look for any secondary loan statements or checks associated with a home equity line.

- 📄 Reverse Mortgage Paperwork: If applicable, this is urgent. Reverse mortgages have very strict timelines for resolution after the borrower passes away.

- 📄 Notice of Liens: Any paperwork indicating a contractor, tax authority, or other entity has placed a lien on the property.

When you find a mortgage statement, you will eventually need to notify the lender. Do not attempt to log into the deceased person’s online banking portal to poke around. Instead, keep a clean paper trail by requesting information in writing.

Here is a safe, neutral way to request status requirements from a mortgage company once you are officially appointed:

Subject: Estate Inquiry – Loan #[Insert Loan Number] – Request for Requirements

To the Mortgage Servicing Department,

I am the appointed executor for the estate of [Deceased Name], who passed away on [Date]. Their property at [Property Address] is secured by loan #[Loan Number].

Please provide me with a written list of the documents your department requires to officially update your records and authorize me to communicate regarding this loan.

I am currently gathering records and am not requesting any changes to the account at this time. Please send the required forms or instructions to [Your Mailing Address/Email].

Thank you,

[Your Name]

Executor for the Estate of [Deceased Name]

When communicating with lenders, I always stick to a simple formula: [Action] + [What you need in writing] + [Confirmation request]. This keeps the conversation strictly administrative, builds your paper trail, and prevents you from accidentally implying that you are taking over personal responsibility for the debt.

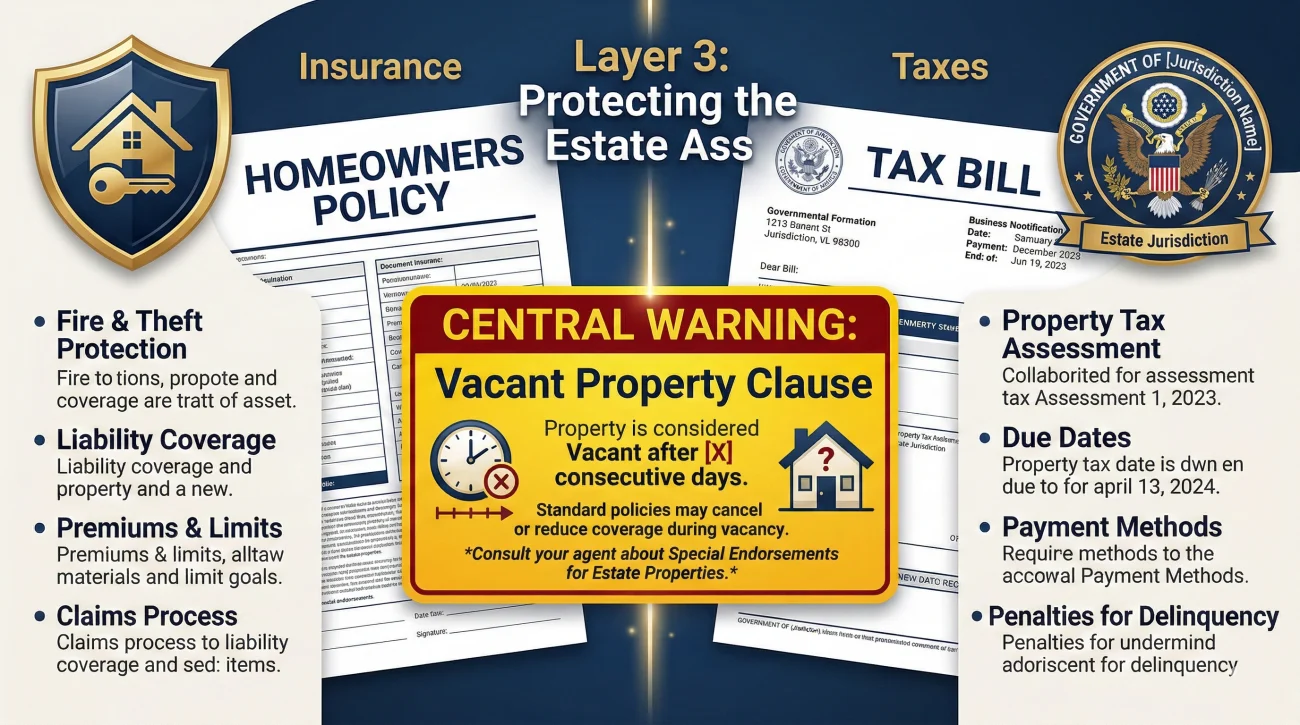

Layer 3: Property Insurance and Property Tax

This layer is about protecting the asset. If the house burns down or a pipe bursts while the estate is in progress, you need to know that the property is covered. Similarly, falling behind on property taxes can lead to severe penalties or even foreclosure down the line.

⚠️ Warning: Standard homeowners insurance policies often contain clauses that reduce or void coverage if a property is left vacant for a certain number of days (commonly 30 to 60 days). Locating the policy so you can eventually discuss “vacant property” coverage with the agent is an urgent administrative task.

Protection Documents to Gather

- 📄 Homeowners Insurance Policy Declarations Page: This summarizes the coverage, the premium, and the agent’s contact information.

- 📄 Flood or Earthquake Policies: These are often billed separately from the main homeowners policy.

- 📄 Recent Property Tax Bill: Shows the parcel number, assessed value, and whether taxes are paid up to date or in arrears.

- 📄 Proof of Payment: Bank statements or receipts proving the most recent insurance premiums and taxes were actually paid.

In many cases, property taxes and insurance are paid through an escrow account attached to the mortgage. If you see an escrow line item on the mortgage statement, note that in your records, but you still want to find the actual insurance policy document. While insurance protects the asset from massive disasters, the day-to-day preservation of the property falls under an entirely different set of records.

Layer 4: HOA, Utility, and Maintenance Records

“A stack of HVAC and roof receipts from the last five years isn’t junk mail. It is documented proof of the home’s condition that can directly aid an appraiser later on.”

This is the category that most people ignore because it feels like minor administrative housekeeping, but it always comes back to cause headaches. If you cancel the wrong utility without thinking, the power goes out, the heating stops, and a pipe bursts in the winter, a disaster that might not be covered if you haven’t sorted out the vacant property insurance clause yet.

Similarly, if the house is part of a Homeowners Association (HOA), ignoring their correspondence can be costly. HOAs have the power to place liens on a property for unpaid dues or unkempt lawns much faster than a standard creditor.

Operations Documents to Gather

- 📄 HOA Covenants and Dues Statements: Find the most recent bill and the contact information for the HOA management company.

- 📄 Utility Bills: Water, electric, gas, trash collection, and internet/cable. Keep them active until the property is transferred or sold.

- 📄 Major Repair Receipts: Look for invoices related to the roof, HVAC system, foundation work, or major remodels.

- 📄 Appliance Warranties: Manuals and warranties for the refrigerator, washer, dryer, and water heater.

The Property File Index System

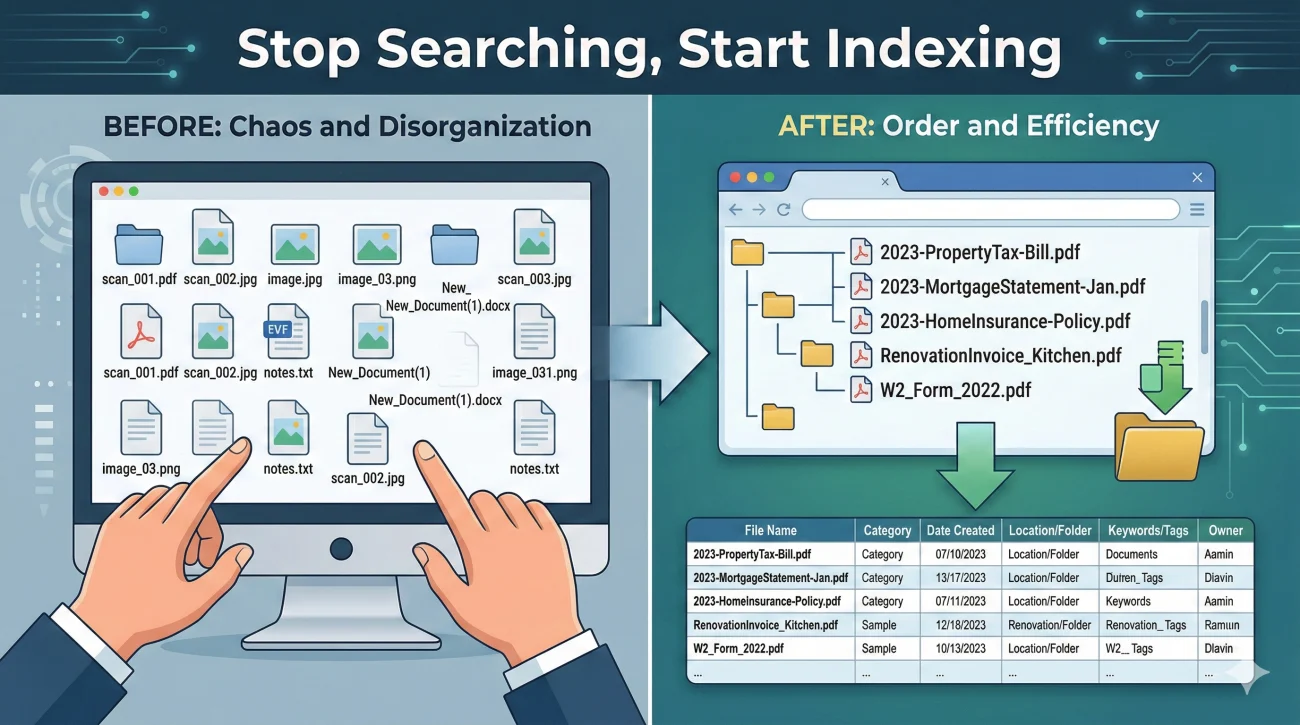

Now that you have gathered all these disparate pieces of paper, dumping them into a single cardboard box is a recipe for disaster. You need an index. An index is simply a log that tells you what documents you have, what format they are in, and where they live.

I highly recommend creating a digital folder on your computer for the estate, with a sub-folder specifically named “Real Estate Documents.” If you are scanning physical papers, how you name those files matters immensely. If you name a file “scan_001.pdf”, you will have to open it every time to see what it is. That wastes hours of your time.

house_doc.pdf

scan_1145.jpg

insurance.pdf

2023-PropertyTax-Bill.pdf

2018-Warranty-Deed.pdf

2024-StateFarm-HomeInsurance-DecPage.pdf

Below is a template for a Property Document Index. You can build this in a spreadsheet or write it in a notebook. The goal is to track the status of your records.

| Document Category | Specific Document Name | Located? (Yes/No) | Format (Paper/Digital) | Physical Location / File Path | Notes / Action Needed |

|---|---|---|---|---|---|

| Ownership | Warranty Deed | Yes | Paper copy only | Red Accordion Folder – Tab 1 | Need to scan a digital copy. |

| Mortgage | Chase Mortgage Statement (Oct) | Yes | Digital PDF | Estate Drive > Real Estate > Mortgages | Sent letter requesting executor access requirements on 11/12. |

| Insurance | Homeowners Policy | No | Unknown | N/A | Found bank statement showing payment to Allstate. Need to call to request policy copy. |

| HOA | Monthly Dues Statement | Yes | Paper | Red Accordion Folder – Tab 4 | Auto-draft from checking account. Needs tracking. |

💡 Pro Tip: If a document is missing (like the insurance policy in the table above), log it anyway. The index acts as your to-do list for what you need to request.

Common Mistakes When Gathering Real Estate Documents

Handling property paperwork is a heavy administrative burden. Over the course of organizing estate files, I consistently see a few specific patterns where well-meaning executors make things harder for themselves. Here is what to avoid.

Mailing Original Documents Without Tracking

Eventually, a title company or lender may ask you to send them a document. Never mail the sole original copy of a deed, a death certificate, or a letters testamentary via regular first-class mail. If it gets lost, replacing it is a nightmare. Always use certified mail with a tracking number, and always keep a scanned digital copy and a physical photocopy for your own records before it leaves your hands.

Ignoring the Mail Over the First 60 Days

A lot of crucial property information arrives in the mail in the months following a passing. Property tax assessments, notices of changes in insurance premiums, and utility past-due notices are easily missed if you are not diligently checking and forwarding the mail. Treat the incoming mail as an active discovery source for your document index.

Using the Deceased’s Credentials for Paperless Accounts

It is incredibly common to discover the deceased person opted into “paperless billing” for their utilities, HOA, or insurance, leaving you without physical statements. The instinct is to find their password notebook, log in, and download the bills. Do not do this. It violates terms of service and can lock you out permanently when the institution flags the login after a death notification.

Instead, use your official capacity. Mail a letter with the death certificate and your executor credentials to the company’s billing department requesting a “historical statement” or “final bill copy” to be mailed directly to your address. It takes slightly longer, but it creates a bulletproof, legal paper trail.

Final Thoughts on Securing the House Paperwork

Gathering real estate documents is rarely a one-day job. It requires patience, a bit of detective work, and a commitment to strict organization. By categorizing the paperwork into ownership, debts, insurance, and operations, you break a massive, overwhelming task down into manageable layers.

The ultimate goal here isn’t just to have a tidy folder; it is to secure your peace of mind. When a title agent asks you for an obscure property tax record three months from now, or the insurance company wants proof of roof maintenance, you won’t feel that spike of panic. You will simply open your index, pull the verified file, and keep the estate moving forward without unnecessary delays.

❓ FAQ

🏠 What documents do I need to sell a deceased person’s house?

Before listing, you generally need the current deed, the death certificate, your official executor appointment documents (Letters Testamentary), a payoff statement for any existing mortgages, and proof of property insurance. A title company will provide the specific final list required for closing.

🗄️ What if the property is located in a different state from where they lived?

You still need to gather all the same documents for your inventory, but out-of-state property often triggers an “ancillary probate” proceeding in that specific state. Keep these records meticulously organized, as you will likely need to share them with a secondary attorney in that jurisdiction.

🖨️ Do I need the original deed or is a copy okay?

For inventory and organizational purposes, a clear copy is perfectly fine. When it comes time to transfer title or sell, the title company or attorney will usually rely on the official recorded version filed with the county anyway.

📞 Who do I notify first about the house when someone dies?

To protect the physical and financial asset, prioritize your notifications in this order: 1) The homeowners insurance company, to ensure coverage remains valid if the home is vacant. 2) The mortgage lender, to prevent default actions while you set up the estate. 3) Utility providers, to keep the heat and water running to prevent physical damage. 4) The HOA, to pause automated fines for maintenance.

🛡️ How do I prove I am the executor to the home insurance company?

You will typically need to provide them with a copy of the death certificate and the official court document naming you as the executor (such as Letters Testamentary or Letters of Administration). Always ask for their requirements in writing.

💰 What if property taxes are due but the estate bank account isn’t open yet?

If deadlines are looming and the estate account is frozen or pending, executors sometimes pay the tax from their personal funds to avoid liens. If you do this, ensure you log it meticulously in your estate expense tracker so you can be reimbursed correctly once the estate funds are accessible.

📑 How long do I need to keep these real estate records?

As a general best practice, retain all property closing documents, final tax payments, and settlement statements for several years even after the estate is closed. Store them securely in your master transaction folder in case tax authorities or heirs raise questions later.

⚖️ How do I find out if there are liens on the property?

I usually recommend ordering a preliminary title report from a local title company right before you plan to list the house, or earlier if you suspect the deceased had hidden debts. This service officially uncovers any recorded judgments or tax liens attached to the house that you may have missed in their paperwork.

📝 Does a transfer on death deed replace the will?

Conceptually, a Transfer on Death (TOD) deed is designed to pass the property directly to the named beneficiary, bypassing probate. However, you must still document its existence in your inventory, obtain the death certificate, and usually file a specific affidavit with the county recorder to officially execute that transfer.

🔑 Should I change the locks on the house?

Yes, changing the locks should be one of your very first physical steps, even before you finish indexing the documents. You rarely know who has spare keys, such as neighbors, dog walkers, or estranged relatives. Securing the property protects the assets inside and ensures your insurance coverage remains valid.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.