- Estate valuation evidence proves what an asset was worth on the specific date the person passed away, which establishes the baseline for all future reporting.

- Online account access decays quickly. Capture historical pricing, balances, and property condition before passwords stop working or physical items are moved.

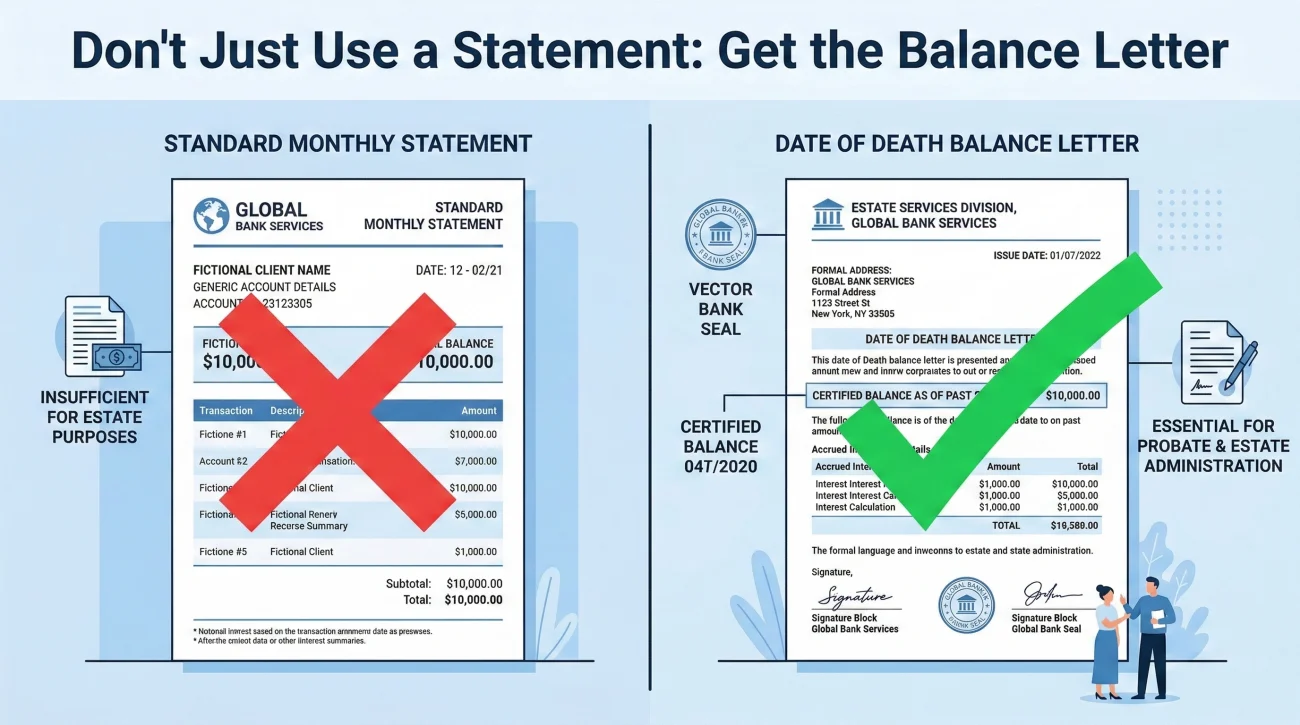

- For bank accounts, a standard monthly statement is not enough; request a specific “date of death balance letter” from the institution.

- Do not forget the liabilities. You must document the exact payoff balances of mortgages, auto loans, and credit cards on the date of death to calculate the estate’s net value.

- Store all valuation documents digitally using a strict, consistent file naming convention so you never have to search for proof when an accountant asks for it.

The Reality of Proving What Things Are Worth

When I help families organize estate administration documents, one of the most common roadblocks we hit happens months into the process. We are sitting at a table looking at a list of assets, and an accountant or an attorney asks a simple question: “What was this exactly worth on the day they passed away?”

Usually, there is a pause. The executor might have a bank statement from three weeks after the death, or a Zillow printout from yesterday, but they do not have the exact date of death value evidence. This creates a stressful, frantic scramble to dig up historical data that is often much harder to access after the fact.

In my experience, building an estate valuation evidence checklist is not about making educated guesses. It is about freezing time. As an executor, your job is to gather and protect the proof of what things were worth at that specific moment. You do not need to be a tax expert to do this. You just need a practical, organized system to capture the documentation before accounts are closed, vehicles are driven, and physical items are sold.

Before you can effectively gather valuation evidence, you must have a clear picture of what the estate actually contains. If you have not built that foundation yet, I highly recommend starting with the core estate asset inventory checklist to get your master list in place. Once you have your assets mapped out, you can start hunting for the evidence to back them up.

Why Gathering Valuation Evidence Matters Early

There is a phenomenon in estate administration that I call “data decay.” In the weeks following a passing, passwords stop working, online banking portals lock down for security, and market conditions shift. The longer you wait, the harder it becomes to find reliable records.

A pattern I see often is an executor assuming that because an account is frozen, the value is safe and they can check it later. However, many institutions will completely disable online access once they are notified of a death. Suddenly, you cannot just log in and download the statement that covers the date of death. You have to submit formal paperwork just to get a basic balance letter, which can delay your workflow by weeks.

Key Point: Gathering valuation evidence early is a defensive measure. You are collecting proof while it is still relatively easy to access, saving yourself from frustrating administrative loops later.

You are collecting this evidence primarily for the professionals who will help you later. Tax preparers, appraisers, and sometimes the court will rely on your estate appraisal documents to establish baselines. If you provide them with clean, clearly labeled evidence, their work moves faster, which usually means fewer billable hours draining the estate.

Evidence by Asset Type: Cash and Bank Accounts

Bank accounts seem like the easiest asset to value, but they frequently cause headaches. A standard monthly bank statement rarely cuts off exactly on the date of death. It might show the balance three days prior or two weeks after. In many cases, everyday transactions or automatic bill pays continue clearing in those intervening days.

To create a bulletproof estate valuation record for cash accounts, you need the institution to verify the exact balance on the specific day.

What to Request from the Bank

When you formally notify the bank of the passing, you should specifically ask for a “Date of Death Balance Letter.” This is a formal document generated by the bank that states exactly how much was in checking, savings, and CD accounts on that day, including any interest that had accrued but had not yet been paid out.

⚠️ Warning: Do not rely on a screenshot of a banking app taken a week later. Mobile app screenshots often lack account numbers, official logos, and specific dates, making them weak evidence.

If you are communicating with a bank representative in writing, here is a simple script you can use to ensure you get the right document:

Subject: Date of Death Balance Request – Account ending in [Last 4 Digits]

Hello [Name/Department],

As part of the estate administration for [Name of Deceased], I am requesting a formal Date of Death Balance Letter for all accounts held under their name, specifically including account ending in [Last 4 Digits].

Please ensure this document reflects the exact balance, including any accrued interest, as of [Date of Death].

Could you please confirm the process and timeline for providing this letter?

Thank you,

[Your Name]

Evidence by Asset Type: Investment Portfolios

Investment accounts, such as brokerage accounts, IRAs, and mutual funds, fluctuate constantly. The value of a stock portfolio at 9:00 AM might be completely different by 4:00 PM on the same day.

When figuring out the executor valuation checklist for investments, the goal is to capture the statement that covers the date of death. However, simply looking at the bottom line or closing price of a monthly statement is often insufficient.

Tax professionals usually require a specific calculation based on the high and low trading prices of each specific stock or bond on that exact day. For example, if a stock closed at $49, you might assume that is the value. But if it traded at a high of $52 and a low of $48 that day, the standard reporting rule typically requires the mean value: $50 per share. Doing this manually for a portfolio of fifty stocks is a nightmare.

I always tell executors: do not try to do this math yourself. Your job is to gather the official records so the professionals can calculate it easily.

- 📄 The full monthly statement: Download or request the complete statement that includes the date of death. Ensure it shows the number of shares held for every single position.

- 📄 The date of death summary: Many major brokerages have a specialized “Estate Processing” department. You can request a date of death valuation report directly from them, and they will run the specific high/low calculations for you automatically.

- ✅ Dividend records: Keep an eye out for any dividends that were declared before the death but paid out afterward, as these often need to be tracked separately.

While investment accounts require precise mathematical averages, physical assets like real estate demand a completely different approach to capturing value.

Evidence by Asset Type: Real Estate

Real estate is usually the largest asset in an estate, and valuing it correctly is crucial. Relying on property tax assessments is a common mistake. Tax assessed values are often years behind the actual market value and can create heavily skewed estate records.

In day-to-day admin work, I see families rely on a quick Zillow search. While a printout of an online estimate is better than nothing in the very early discovery phase, it is rarely accepted as formal date of death value evidence by tax authorities or the court.

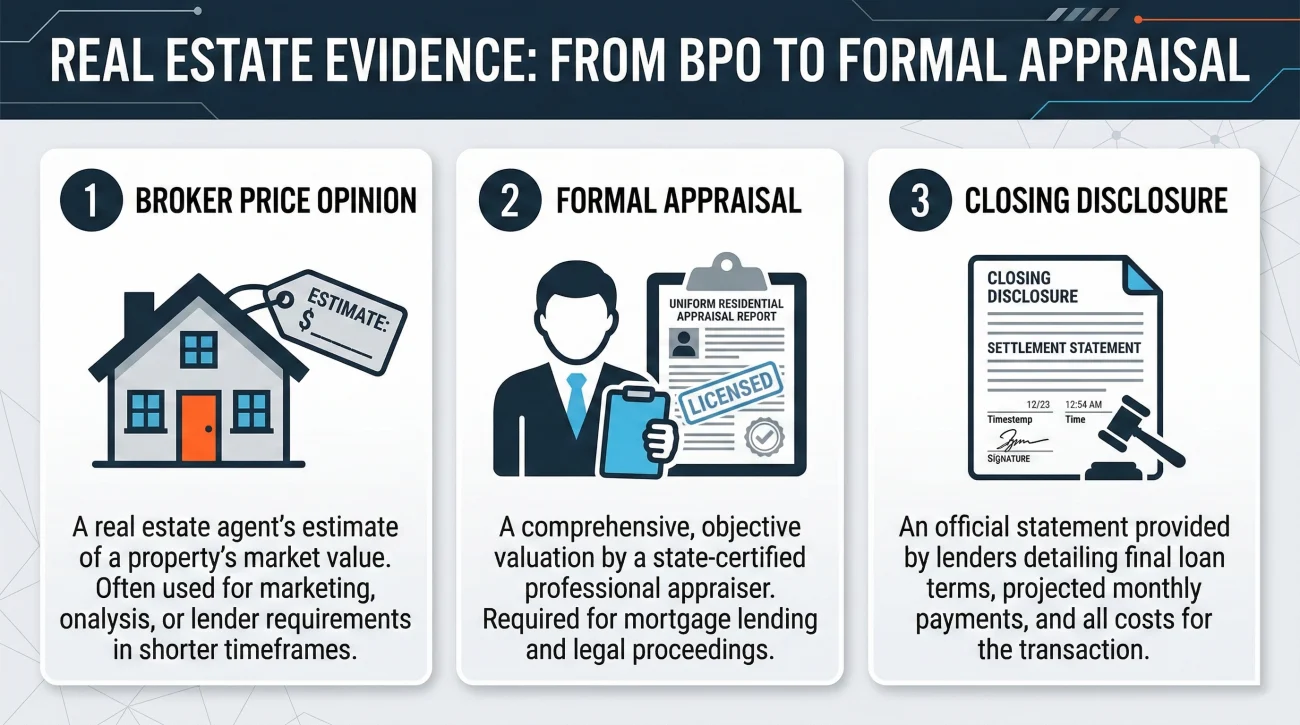

For a solid executor valuation checklist, you generally have three tiers of evidence for property:

| Evidence Type | What It Is | When It Is Usually Used |

|---|---|---|

| Broker Price Opinion (BPO) | A real estate agent reviews the property and comparable recent sales to estimate value. | Often acceptable for simple estates where the family plans to sell the house immediately. |

| Formal Appraisal | A licensed appraiser visits the property, measures, assesses condition, and writes a legally defensible report. | Used when keeping the house in the family, buying out siblings, or for complex tax situations. |

| Closing Disclosure | The final settlement paperwork if the house is sold shortly after the passing on the open market. | The actual sale price (within a few months) is often the strongest proof of value. |

Evidence by Asset Type: Vehicles

Vehicles depreciate, and their value is highly dependent on their condition. A common trap is an executor waiting six months to sell a car, only to realize they have no proof of what it was worth back on the date of death.

To protect yourself, take immediate action to capture the baseline value. You do not need a mechanic to do this. You just need a camera and an internet connection.

First, take clear photographs of the vehicle. Capture the exterior from all angles, the interior seats, the dashboard, and specifically take a close-up photo of the odometer showing the exact mileage. If there is a large dent in the door or a tear in the upholstery, take a picture of it. Condition matters deeply for valuation.

💡 Pro Tip: Go to Kelley Blue Book (KBB) or a similar valuation site. Enter the exact make, model, year, mileage, and condition based on your photos. Print that evaluation page to a PDF and save it. That printout, combined with your timestamped photos, creates an excellent estate valuation record.

Evidence by Asset Type: Personal Property

Cars have a clear market value tool. The harder challenge is everything inside the house. Documenting household contents can feel overwhelming. Do you need to value every single spoon, towel, and paperback book? Usually, no. If you try to itemize every object, the estate process will stall completely.

In day-to-day admin work, I tell executors to mentally divide personal property into three value tiers to avoid getting bogged down:

- ✅ Tier 1: Everyday Items (Under $500). This includes standard furniture, clothing, and kitchenware. A broad categorization is sufficient. Use the video or photo walkthrough method. Walk through the entire house, open cabinets, and take clear videos of every room. This proves what was there and its general condition without needing individual receipts.

- ✅ Tier 2: Mid-Value Items ($500 to $5,000). This includes power tools, high-end electronics, standard jewelry, or riding lawnmowers. Take individual photos of these items, capture serial numbers if possible, and try to locate recent purchase receipts or standard online comparable prices.

- ✅ Tier 3: High-Value Items (Over $5,000). This covers fine art, antiques, rare coin collections, or significant jewelry. These items absolutely require specific valuation evidence. Look for existing insurance riders (which often state an appraised value) or prepare to hire a specialist to provide a formal estate appraisal document.

When is a Formal Appraisal Actually Worth It?

Executors often ask me if they are required to pay a professional appraiser for everything in the house. In many cases, standard assets do not require it. However, there are specific triggers where spending estate funds on an appraisal is the safest and smartest move you can make to protect yourself.

Consider hiring a professional appraiser when:

- ✅ The asset is unique or hard to value: This includes commercial real estate, privately held business interests, or specialized collections where online comparables do not exist.

- ✅ Family tension is high: If siblings are arguing over who gets what, a neutral, third-party appraisal removes the emotion. You are no longer guessing the value; a professional is stating it as fact.

- ✅ The estate is approaching tax thresholds: If the total value of the estate is large enough that tax professionals are involved, they will almost always demand formal, defensible appraisals to protect against audits.

Always ask the appraiser to specifically state the “date of death value” in their final written report, rather than just the value on the day they inspected the item.

Don’t Forget the Other Side: Documenting Debt

Valuation is not just about what things are worth; it is also about what is owed against them. A common missing piece in an executor’s file is the exact liability load on the date of death. If a house is worth $400,000 but has a $300,000 mortgage against it, the net value to the estate is vastly different.

You must gather evidence of debt just as rigorously as you gather evidence of assets. Your debt documentation packet should include:

- 📄 Mortgage Payoff Statements: Do not just look at the monthly bill. Request a formal payoff quote as of the date of death, which includes exact principal and interest.

- 📄 HELOCs and Lines of Credit: Capture the exact drawn balance before the account is frozen.

- 📄 Auto Loan Balances: Map this directly to the vehicle valuation you pulled from KBB to show the net equity.

- 📄 Credit Card Balances: Pull the statements covering the date of death to prove exactly what the deceased owed before any post-death late fees or interest began accumulating.

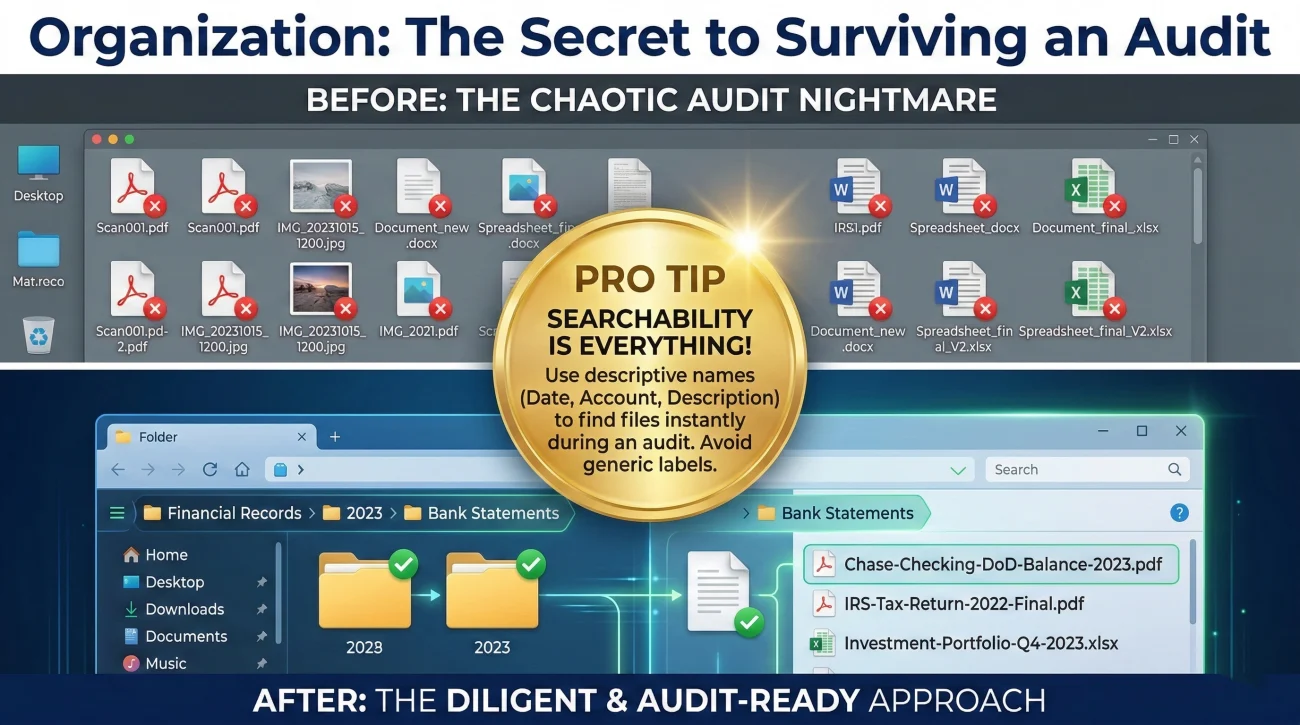

How to Store and Label Your Valuation Evidence

Having the evidence is only half the battle. If you save all these documents as “Scan001.pdf” and “image4.jpg” in a messy folder on your desktop, you will be miserable when it comes time to hand them over to an accountant.

You need a clean, predictable filing system. Create one master folder on your computer named “Estate Records – [Name].” Inside that, create a subfolder called “Valuation Evidence.”

Every time you receive a document, rename it immediately before saving it. A good file name tells you exactly what the document is without you having to open it. I recommend using a standard format that includes the asset, the document type, and the date.

bank_statement.pdf

Chase-Checking-4455_DoD-Balance-Letter_2023-11-04.pdf

Once the file is saved and named, go to your main estate asset inventory spreadsheet. In the row for that specific asset, there should be a column labeled “Valuation Proof.” Simply type the name of the file in that column. This creates a clear map. If anyone asks, “How do you know the Chase account had that exact amount?”, you can look at your tracker, see the file name, and pull it up in seconds.

Common Valuation Evidence Mistakes to Avoid

Even with a good checklist, it is easy to make missteps in the fog of estate administration. Being aware of these common pitfalls can save you from having to backtrack.

Relying on verbal estimates: If a jeweler looks at a ring and says, “Oh, that is probably worth a thousand dollars,” that is not evidence. You need it in writing. Always follow up and ask for a written statement or a formal appraisal on company letterhead.

Throwing away old mail too quickly: Executors often clean out the deceased’s desk and shred old statements. Stop. Those old property tax bills, insurance renewals, and previous appraisals are vital breadcrumbs. Even if they are a year old, they provide a baseline for your search.

Using the wrong date for weekend deaths: If the deceased passed away on a Saturday or a holiday when financial markets were closed, you cannot simply pick Friday’s closing numbers. Tax rules generally require an average of the trading days immediately before and after the weekend. Let the brokerage or accountant handle this specific calculation.

Final Thoughts

Estate administration is a marathon of paperwork, and gathering valuation evidence is often the heaviest lift in the entire process. It requires patience, organization, and a willingness to sit on hold with financial institutions.

But by securing these numbers early, you are doing much more than just pleasing accountants. You are protecting the estate from audits, preventing family disputes over guessing games, and giving yourself peace of mind. You are building a factual, defensible foundation so you can finally put the spreadsheets away, close the estate confidently, and focus on moving forward.

❓ FAQ

🗓️ What happens if they pass away on a weekend when markets are closed?

If the death occurs on a weekend or holiday, tax professionals typically use a calculation that averages the high and low trading prices of the trading days immediately before and after the date of death.

🏦 The bank only gives monthly statements, how do I get the exact day?

You must contact the bank’s estate or bereavement department and explicitly request a “date of death balance letter.” This formal document calculates the exact balance, including unposted interest, for that specific day.

📜 Can I use the local property tax assessment for the estate inventory?

Generally, no. Property tax assessments are often years behind the actual market value. You will typically need a Broker Price Opinion (BPO), a formal appraisal, or recent closing documents to establish a defensible baseline.

🚗 If a vehicle is totaled in the accident that caused the death, how is it valued?

For estate purposes, the vehicle is usually valued at its pre-accident condition. However, you will also need to track the pending auto insurance payout as a completely separate asset belonging to the estate.

📉 What if the stock market crashed the day after they died?

The standard baseline remains the value on the actual date of death. Fluctuations that happen afterward do not change that initial baseline, though tax professionals have specific rules on how to report those subsequent losses during administration.

🔐 Do I need to hire an appraiser to look inside a safe deposit box?

Depending on local state laws and bank policies, you often need a bank officer and a neutral witness present when opening a box. You must thoroughly inventory and photograph the contents before bringing in an appraiser for specific high-value items found inside.

🏃 What if an heir already took a valuable item before it was appraised?

You should request they return it temporarily for a formal valuation. If that is impossible, they must agree in writing to a professional estimated value (based on photos or old receipts) so that amount can be properly deducted from their final share of the estate.

🗂️ Are these valuation documents part of the public probate record?

The final total inventory value is often filed publicly with the probate court. However, your underlying granular evidence, like specific bank account numbers, passwords, and detailed brokerage statements, is typically kept private in your own executor files.

⚖️ What if two appraisers give me completely different values for the same item?

If appraisals conflict significantly, the court or tax authorities will look at the methodology. You do not necessarily have to pick the higher value; you should rely on the report that is more thoroughly documented and well-reasoned by an independent, qualified professional.

🔎 What if I discover a new asset a year later?

You still must find its historical value on the original date of death, not the date you discovered it. Once you have that evidence, you may need to file a supplemental inventory with the court or your accountant.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.