- The core separation: A non-probate asset checklist helps you identify accounts and properties that transfer directly to someone else via built-in contracts, completely outside the traditional court process.

- The printable tracker: Use our structured template below to log the asset type, suspected mechanism, date contacted, and receipt of written confirmation.

- Red flags to watch for: Look for acronyms like POD, TOD, or JTWROS on statements, or multiple names listed on property deeds, which indicate the asset may skip the estate.

- Handling edge cases: If a named beneficiary is deceased or a minor, or if you are dealing with digital wallets without clear beneficiary forms, the administrative process will require specific inquiries to the holding institution.

The Invisible Estate: When Assets Skip Your Paperwork

I once reviewed a case where an executor was trying to divide a $400,000 retirement account equally among three siblings because a Will drafted in 2019 clearly instructed it. However, the brokerage account had a beneficiary form on file from 2003 naming only one sibling. Tensions flared instantly, and the executor was caught in the middle without the right paperwork to explain what happened.

As someone who helps executors build document packets and coordinate with financial institutions, I see this exact scenario play out constantly. In modern estate administration, a massive portion of a person’s wealth is specifically designed to skip the traditional estate process entirely. For an executor, this creates a frustrating dynamic. You are responsible for organizing the estate, yet some of the largest accounts are legally invisible to you.

The form on file at the institution almost always wins. That is exactly why I strongly advocate for building a comprehensive non probate assets checklist from day one.

Even though you may not control these items, keeping a strict, documented log of what they are and where they went is the most effective way to protect yourself and provide absolute transparency to the family. Let us walk through the red flags that identify these assets, the exact timeline expectations, and the master tracker you need to build a paper trail that leaves no room for guessing.

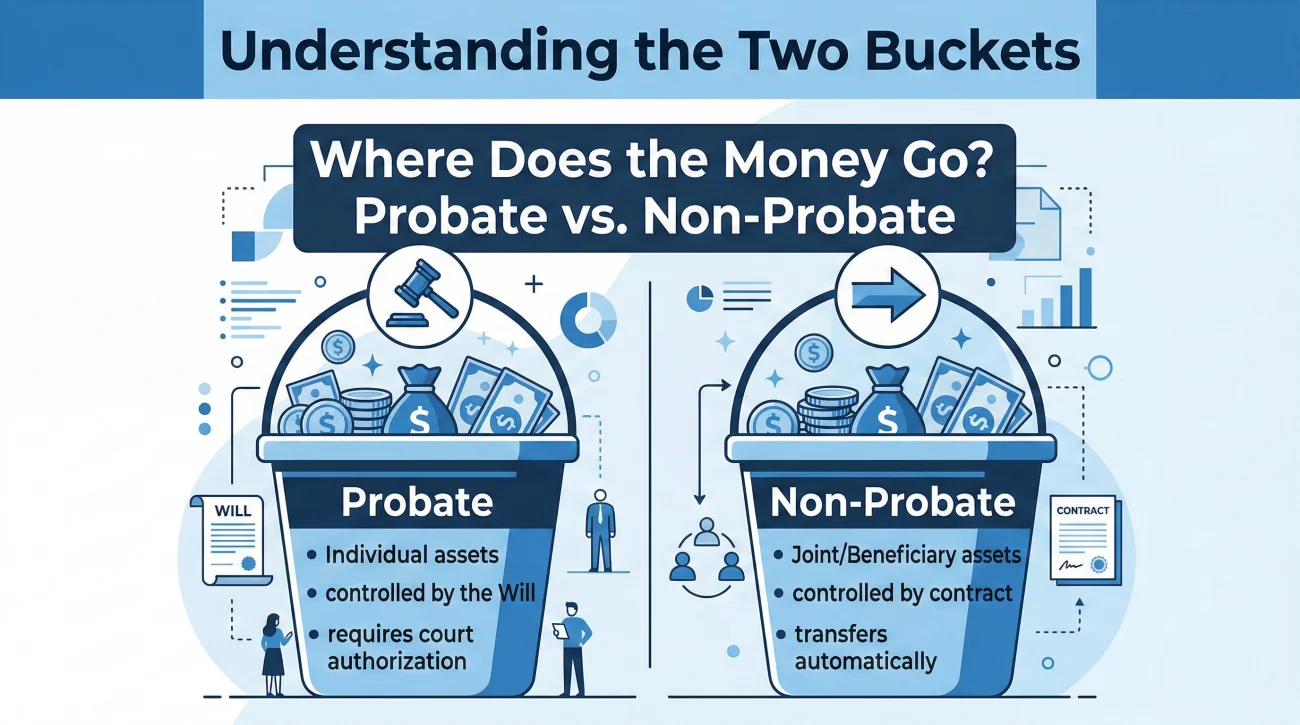

Probate vs. Non-Probate Assets in Plain English

To keep your files organized, it helps to mentally separate the deceased person’s belongings into two distinct buckets. Understanding the boundary between these two buckets will save you dozens of wasted phone calls.

If you are wondering exactly what assets do not go through probate, it comes down entirely to the underlying contract or title.

The Probate Bucket

These are assets owned entirely in the deceased person’s individual name, with no built-in instructions on what happens next. The legal system has to step in to authorize you to move the funds or title. The instructions for this bucket are usually found in the Last Will and Testament.

The Non-Probate Bucket

These are assets that have a built-in next step hardwired into their contract or title. The moment the owner passes away, the asset automatically looks at its own contract and transfers directly to the designated person or entity. The Will generally has absolutely no power over these items.

“I am the executor, so I need to gather all the bank accounts and divide them according to the Will.”

“If a bank account has a Payable on Death form attached to it, the funds go directly to that named person immediately. The institution follows the contract, not the executor.”

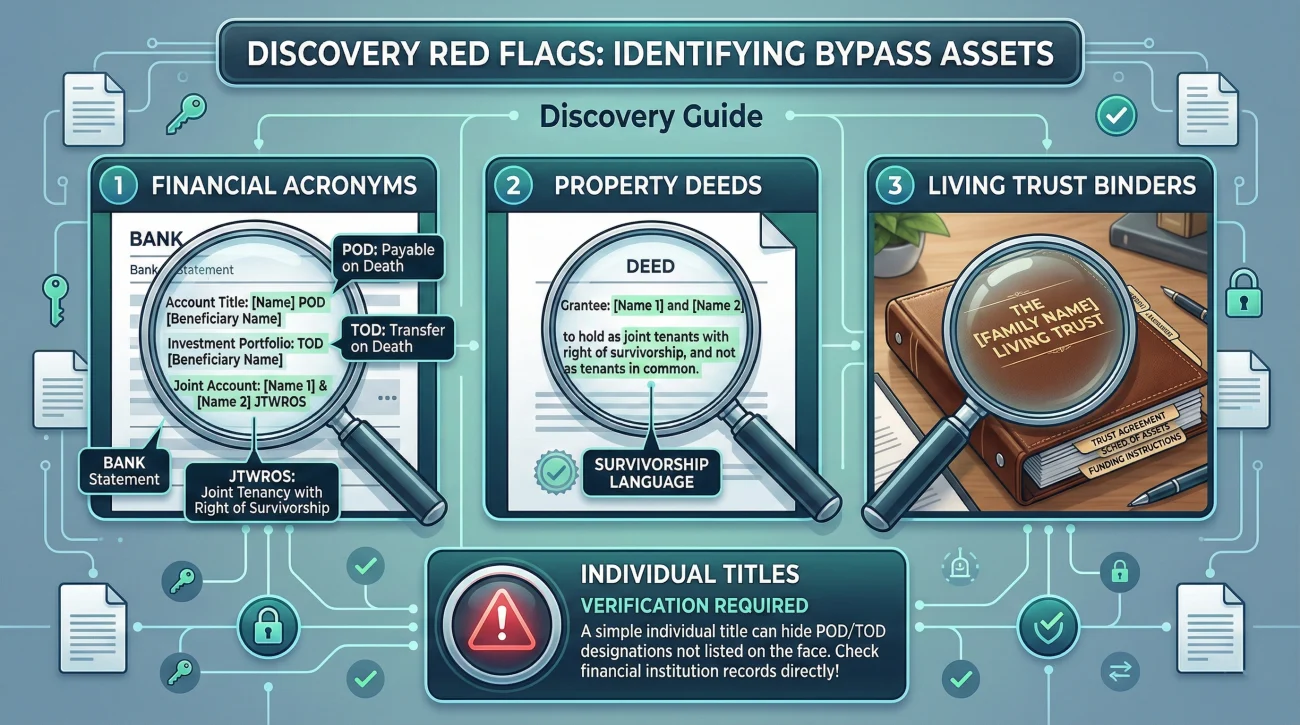

Discovery Red Flags: Clues You Are Looking At A Bypass Asset

Before you start calling banks, you need to know what to look for in the physical paperwork. In my day-to-day work, I teach executors to look for specific administrative clues that strongly suggest an asset belongs on the non probate assets list. If you see any of the following, flag the document immediately.

Acronyms on Financial Statements

Banks and brokerages often print the account type right on the monthly statement header next to the account owner’s name. Look for these specific acronyms:

- 📄 POD: Payable on Death (usually on checking or savings accounts).

- 📄 TOD: Transfer on Death (usually on investment or brokerage accounts).

- 📄 JT TEN or JTWROS: Joint Tenants with Right of Survivorship.

Multiple Names on Property Deeds

If you pull a copy of the house deed and see the deceased person’s name alongside someone else’s, pay close attention to the phrasing. Words like “joint tenants” or “survivorship” usually mean the surviving owner absorbs the full property instantly, triggering a joint tenancy probate bypass.

Living Trust Binders

Finding a thick, expensive binder labeled “Revocable Living Trust” is a major clue. A trust is essentially a legal box. If the deceased person correctly re-titled their house or bank accounts into the name of that trust, those assets bypass the court. The trust document itself dictates the next steps.

⚠️ Warning: Finding a trust binder is not enough. I frequently see families with beautiful trust documents, but the deceased person never actually went to the bank to change their account titles to the trust. If the account title is still in their individual name, it might still end up in the probate bucket. Always verify the actual title with the institution.

The Printable Master Tracking Checklist

If you have no control over these assets, why should you spend time logging them? Because clarity prevents conflict. When a beneficiary account transfers silently and you have no record of it, it looks like missing money to the rest of the family. By logging these items, you build an airtight record that proves exactly why a specific account did not go into the main probate bucket.

When you sit down to build your estate asset inventory checklist, you need a highly structured way to log inquiries and responses. Here is the exact master tracker framework I recommend mapping out on a spreadsheet or a printed log.

| Asset Type | Account No. (Last 4) | Institution | Suspected Mechanism | Date Contacted | Written Confirmation Rcvd | Filed In |

|---|---|---|---|---|---|---|

| Checking | x1234 | Local Credit Union | Joint Owner | Oct 10 | Oct 15 (Letter) | Folder 2A |

| Life Insurance | x9988 | Big Insurance Co. | Beneficiary Form | Oct 12 | Oct 20 (Claim Initiated) | Folder 2B |

| Primary Home | N/A | County Records | Trust Owned | Oct 14 | Oct 16 (Deed pulled) | Folder 2C |

| Brokerage | x5567 | National Broker | TOD Form | Oct 15 | Pending | Pending Log |

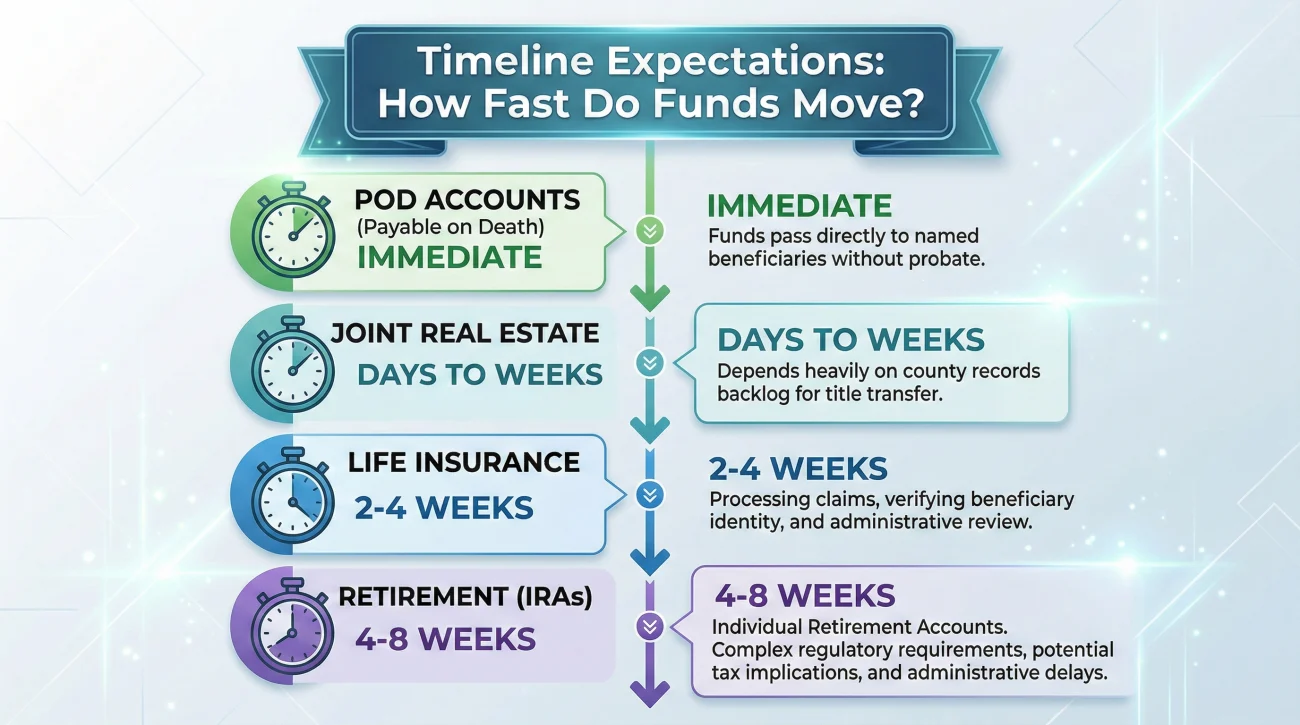

Timeline Expectations: How Long Do Transfers Take?

Executors are constantly asked by family members when a specific non-probate asset will be distributed. It is vital that you do not make promises you cannot keep, because the holding institution controls the timeline, not you.

Based on standard administrative patterns, here are the general timeline expectations you can communicate to the family, assuming the beneficiaries submit all required claim forms and death certificates promptly:

- ⏳ Life Insurance Policies: Typically 2 to 4 weeks after the claim packet is marked complete by the insurer.

- ⏳ Retirement Accounts (IRAs): Typically 4 to 8 weeks. These take longer because beneficiaries often have to open a new inherited account at the same institution before the funds can physically move.

- ⏳ POD Bank Accounts: Usually immediate upon presentation of a death certificate and identification by the named beneficiary at a local branch.

- ⏳ Real Estate (Joint Tenancy): Often requires filing an affidavit of death and a death certificate with the county recorder, which can take anywhere from a few days to a few weeks depending on county backlogs.

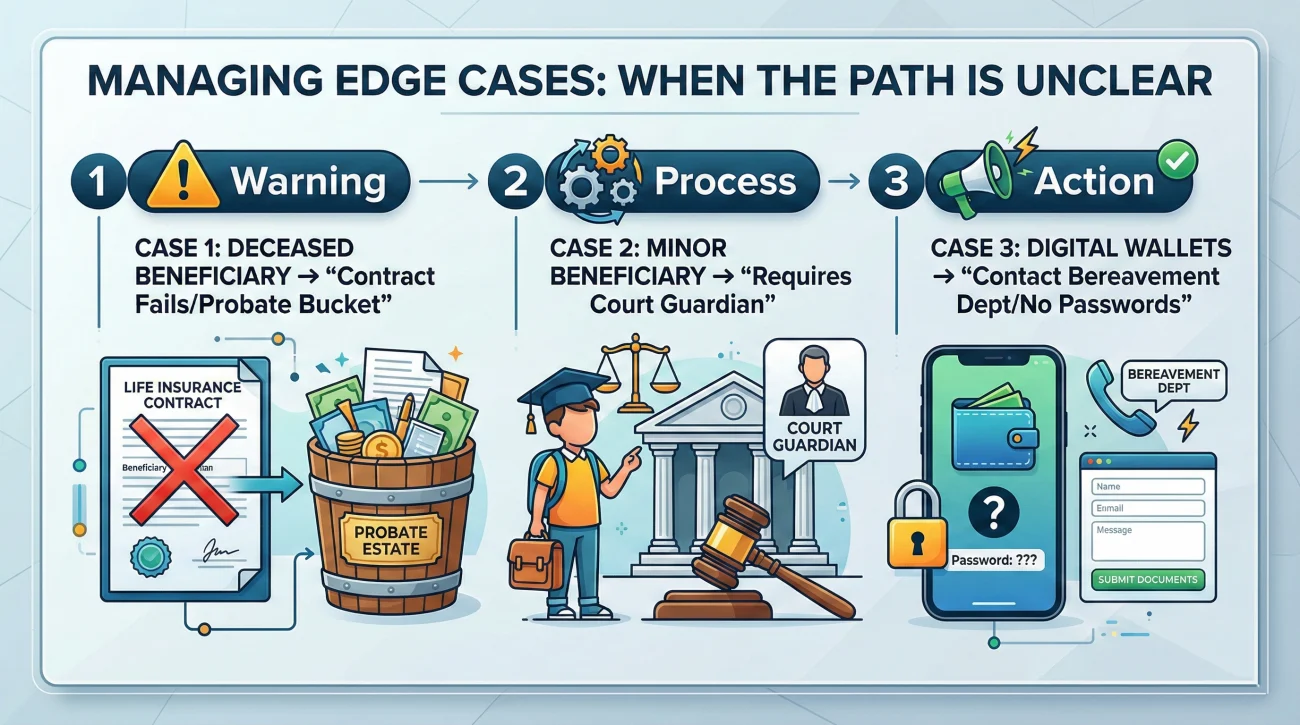

Administrative Edge Cases: When Things Get Messy

The standard process assumes a healthy, adult beneficiary is ready to claim the account. In reality, you will frequently encounter administrative roadblocks. Here is how to handle the process when the path is unclear.

The Beneficiary Passed Away Years Ago

If you discover that the sole named beneficiary on a POD account died before the account owner, the institution will look for a contingent (backup) beneficiary on the form. If there is no contingent listed, the contract essentially fails. In most cases, the account will revert back to the deceased person’s individual name and drop straight into the probate bucket. You will need to ask the institution for their specific procedure to re-title the account to the estate.

The Beneficiary is a Minor

Institutions will rarely write a $50,000 check to a twelve-year-old. If a minor is named on a life insurance policy or retirement account, the process halts. The institution will typically require a court-appointed financial guardian to be established before releasing funds. As the executor, your job is simply to ask the institution for their required guardianship documentation list and pass that list to the minor’s surviving parent or guardian.

Digital Assets and Wallets

Modern digital accounts like cryptocurrency exchanges, PayPal balances, or Venmo accounts are a massive gray area. Many of these platforms do not offer traditional Transfer on Death forms. Without a built-in contract, these balances frequently default to the estate. If you locate digital funds, do not attempt to use the deceased’s passwords to transfer the money. Contact the platform’s official bereavement or legal department and request their specific estate transfer paperwork.

Communication Hygiene: The Neutral Status Request

The most common documentation mistake I see is an executor accepting a verbal status update over the phone. A customer service rep says, “Oh yes, there is a beneficiary, it won’t go through the estate.” Six months later, the family demands proof, and you have zero paper trail.

Never accept a verbal status. When reaching out to clarify the probate vs non probate assets status, your communication should be strictly neutral. You are not demanding access to funds; you are simply an administrator requesting clarity for your inventory.

Here is a safe, practical script you can adapt.

Subject: Estate Inventory Inquiry: Account ending in [Last 4 Digits]: [Name of Deceased]

Hello [Department / Contact Name],

I am the appointed executor for the estate of [Name], who passed away on [Date]. I am currently compiling the formal asset inventory for the estate records.

Regarding the account ending in [Last 4 Digits], could you please provide written confirmation indicating whether this account is subject to probate, or if it transfers directly via a valid beneficiary designation (such as POD or TOD) currently on file?

I am not requesting the disbursement of funds at this time, nor am I requesting the names of the beneficiaries if privacy policies restrict it. I simply need written verification of the account’s transfer status for my official log.

Please let me know if you require a copy of the death certificate or my appointment documents to process this administrative request.

Thank you for your assistance,

[Your Name]

Executor for the Estate of [Name]

Notice the structure of this message:

[State your role] + [Specify the account] + [Ask for written status only] + [Acknowledge their privacy rules]

This approach disarms the compliance team. It shows you understand standard banking privacy protocols and are just trying to do your administrative duty.

Two Dangerous Misconceptions to Avoid

Assuming a Beneficiary Must Share

Family members often assume that if one sibling is named as the sole POD beneficiary on a checking account, that sibling is legally required to split the money with the others to honor the “spirit” of the Will. Operationally, this is completely false once the asset falls into the non-probate bucket. The named beneficiary becomes the sole legal owner of those funds the moment of death. Whether they choose to gift portions of it to others later is a personal choice, not an executor mandate.

Assuming You Must Execute the Transfer

Executors often burn hours trying to fill out claim forms for beneficiaries of beneficiary designated accounts probate bypass items. You do not need to do this. The financial institution views the beneficiary as their new client. Your role is simply to provide the beneficiary with the contact information for the institution and perhaps a copy of the death certificate. They must initiate the claim themselves.

Final Thoughts: Prove Why The Buckets Look Different

Managing an estate is largely an exercise in gathering facts and organizing them so they make sense to a stressed group of people. When dealing with assets that bypass your direct control, the temptation is always to ignore them entirely because they are not your legal responsibility.

But think back to that $400,000 retirement account I mentioned at the start. The executor in that case did not fail because the money was missing; they failed because they did not have the immediate paper trail to prove why the money landed in the non-probate bucket instead of the shared probate bucket. When you take the time to log these bypass assets, secure the written confirmations, and build a clear tracker, you remove the mystery. You are no longer just doing administrative paperwork; you are actively preventing family fractures.

❓ FAQ

👶 What happens if the named beneficiary on an account is a minor?

Financial institutions generally will not release funds directly to a minor. The process usually pauses until a court appoints a legal financial guardian for the child. Ask the institution for their specific required guardianship forms to share with the family.

🪦 What if the primary beneficiary passed away before the account owner?

The institution will look for a contingent (backup) beneficiary on the form. If no contingent beneficiary is listed, the contract typically fails, and the asset reverts back to the deceased person’s estate, meaning it must now go through probate.

📱 Do digital wallets like PayPal or Venmo have payable-on-death options?

Most standard digital payment apps do not currently offer clean Transfer on Death features. Without a beneficiary designation on file, balances in these apps usually become property of the estate and require executor intervention to claim.

🏡 Should the estate continue paying the mortgage on a joint-tenancy house?

If the house passes directly to a surviving joint owner, that new owner is generally responsible for the upkeep and mortgage. However, executors should track any transition period carefully and confirm with a professional to ensure the property is not foreclosed on during the handover.

🏦 Will the bank notify me when a POD account is emptied by the beneficiary?

No. Once the account owner passes, the bank views the POD beneficiary as their client. Due to privacy rules, they will not usually alert the executor when the funds are transferred or the account is closed.

📄 Do I need to give the heirs the death certificate to claim their accounts?

While you are not legally required to act as their personal courier, providing a certified copy of the death certificate to known beneficiaries is a standard courtesy that speeds up the transfer process and helps close out the estate faster.

🔍 How do I track a life insurance policy if I cannot find the original paperwork?

Review the deceased person’s past checking account statements. Look for recurring monthly or annual payments to insurance companies. You can use those transaction records to contact the insurer and ask about policy status.

💳 Can a surviving spouse just keep using a joint checking account?

Generally, yes. If the account is set up as joint with right of survivorship, the surviving spouse retains full, uninterrupted access to the funds. The executor simply logs the account as a non-probate joint asset.

🏢 What if an account has a TOD form but the institution lost it?

If the institution has no record of the form and no copy can be found, they will likely treat the account as an estate asset. This often requires legal escalation if the family disputes it, but your immediate job is to log the account status as “disputed/pending.”

🛡️ Are non-probate assets protected from the deceased person’s creditors?

This varies heavily depending on the type of asset and local jurisdiction. Life insurance might be protected, while a joint checking account might not be. Log every asset thoroughly, as your professionals will need this list to handle creditor claims accurately.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.