- A last will and testament is only a nomination; it does not give you legal authority to access or freeze bank accounts.

- Banks manage financial liability first. They cannot risk releasing funds to the wrong person, so they require court-issued “letters” to prove your authority.

- Even after you provide the correct documents, bank legal departments often take weeks to review them. You must track your submissions and request confirmations in writing.

The “I Have the Will Right Here” Moment

In my experience mapping out estate workflows, there is one specific moment that catches almost every first-time executor off guard. You walk into a local bank branch carrying a folder containing a certified death certificate, the deceased person’s original will, and your photo ID. You sit down with a banker, expecting to close the account or transfer the funds into an estate account. Instead, the banker looks at the will, hands it back to you, and says, “I am sorry, but we cannot help you without court letters.”

This is incredibly frustrating. The will clearly states your name. The deceased person signed it. You know exactly what the document says. It feels like the bank is putting up an unnecessary legal wall or being intentionally difficult during a stressful time.

The reality is not about the bank being stubborn. When you discover firsthand that a will not enough for bank access, you are hitting a standardized risk-management protocol. The institution is not questioning the deceased person’s wishes; they are simply shielding themselves from fraud and financial liability.

To get past this bottleneck without burning your energy, I find it helps to understand the difference between what a family sees in a document packet and what a bank’s back-office reviewer sees. Once you learn to speak their language, the delays start to shrink.

Named vs. Appointed vs. Recognized

One of the most common reasons timelines slip in the first month is a misunderstanding of how authority actually transfers. In day-to-day admin work, the fastest wins usually come from understanding that authority happens in three distinct phases. If you try to skip a phase, the system rejects your request.

Phase 1: You Are Named

The will is essentially a set of instructions. When the deceased person wrote it, they nominated you for the job. However, a piece of paper sitting in a desk drawer does not have the power to bind third-party financial institutions. At this stage, you are selected by the family, but you do not yet have legal power over the assets.

Phase 2: You Are Appointed

To gain actual authority, the will must be validated by a probate court. The judge reviews the document, ensures it is the final version, and officially appoints you to the role. The output of this process is a court document. Depending on where you live, these are often called Letters Testamentary or Letters of Administration. This piece of paper is the actual key to the estate.

Phase 3: You Are Recognized

This is where the paperwork problem usually starts. Even with court letters in your hand, the bank does not instantly flip a switch. You hand the documents to a branch representative, but they do not make the final call. They scan your documents and send them to a centralized legal or estate review department. You only gain access to the funds once that back-office department “recognizes” your court-appointed authority.

Field Note: A common pattern I see is executors leaving the bank branch thinking the matter is resolved because the teller made copies of their documents. In reality, the teller just started the submission process. The actual review takes place in another state and often takes weeks.

What the Bank Is Actually Trying to Verify

When you are grieving and trying to settle affairs, the bank’s demands feel deeply personal. It helps to flip the perspective and look at the situation through the lens of a corporate risk manager. Banks are terrified of liability.

If a bank gives you fifty thousand dollars based purely on a paper will, and two weeks later someone else shows up with a newer will naming a different executor, the bank is in massive trouble. They could be held liable for giving away the money to the wrong person. Therefore, they do not interpret wills. They rely on the court system to do the interpreting for them.

| The Document | What You Think It Does | What the Bank Sees |

|---|---|---|

| The Last Will | Proves I am in charge. | An unverified nomination that carries high liability risk. |

| Death Certificate | Proves the account owner passed away. | Triggers the account freeze, but does not grant anyone access. |

| Court Letters | A formality I shouldn’t need. | The only acceptable, standardized signal of legal authority. |

Bank guidance commonly frames required documents as a specific equation: Proof of Death + Proof of Authority + Proof of Identity. If any one of those variables is missing or unclear, the file goes into a pending status, often without anyone calling to tell you.

When the Will (and Letters) Might Not Matter at All

To make matters slightly more confusing, there are common scenarios where you might not need court letters to deal with an account. This is a typical point where files go missing or family communication breaks down, because the rules seem inconsistent.

Certain accounts bypass the probate process entirely. These are often governed by contracts rather than the will. If the deceased person set up the account in a specific way, the funds transfer directly to the named individual, and the bank will not need your court letters to process that specific transfer.

- ✅ Joint Accounts: If the account was co-owned with rights of survivorship, the surviving owner typically takes full control immediately after presenting the death certificate.

- ✅ Payable-on-Death (POD): The person named as the POD beneficiary claims the funds directly, bypassing the estate entirely.

- ✅ Transfer-on-Death (TOD) Brokerage Accounts: While conceptually similar to POD, investment accounts often have specific TOD designations. Brokerages usually have separate bereavement departments with distinct workflows compared to local banks.

Conversely, if an account has no joint owner and no listed beneficiary, it defaults to the estate. This is the exact scenario where court letters become absolutely mandatory.

Assuming every single account requires you to mail in court letters and wait for back-office approval.

Asking the institution upfront if the account has a designated POD beneficiary or joint owner before submitting the full estate packet.

Once you have identified which accounts actually belong to the estate and require formal court approval, your next job is to present that proof to the bank in a way they cannot easily reject.

How to Build a Reviewer-Friendly Authority Packet

Because the bank’s review department operates at scale, handling thousands of estate cases a month, delays often come from unreadable packets or missing mapping. If you send a scattered fax with no cover sheet, it will get pushed to the bottom of the pile.

When you are ready to formally notify a financial institution and request access, you should build a unified packet. This reduces the “one more document” loop where they keep asking for things you thought you already provided.

Step 1: The Preparatory Call

Before you mail or fax anything, call the institution’s estate or bereavement department. Do not rely on what a front-desk branch worker tells you, as they rarely handle these cases start to finish.

Script: Requesting Exact Requirements

Hello, I am the appointed executor for the estate of [Name]. I have my court letters and the certified death certificate ready. Before I send them in, can you please provide a written checklist of exactly what your back-office review team requires to process this, and the direct fax number or mailing address I should use?

Step 2: Assemble the Core Documents

Keep a master folder on your computer (or a physical binder) with clean, flat, well-lit scans of your core items. A standard executor bank documents checklist packet usually includes:

- A clear cover sheet with your contact info, the deceased’s name, and the account numbers in question.

- The certified death certificate.

- The court-issued letters of authority.

- A copy of your government-issued ID.

- The bank’s specific intake form, if they require one.

⚠️ Warning: Do not use the deceased person’s online banking credentials to log in and transfer the money yourself. Even if you have their passwords, doing so violates the bank’s terms of service and can trigger fraud alerts that freeze the funds indefinitely.

Step 3: Track the Submission

Once you submit the packet, do not just wait. The most common mistake I see is an executor assuming silence means the process is moving forward. Silence usually means the file is stuck.

- ➡️ Send the complete packet via their requested method.

- ➡️ Ask for a specific processing timeline (e.g., “Should I expect to hear back in 10 or 14 business days?”).

- ➡️ Set a calendar reminder to call them back the day after that timeline expires.

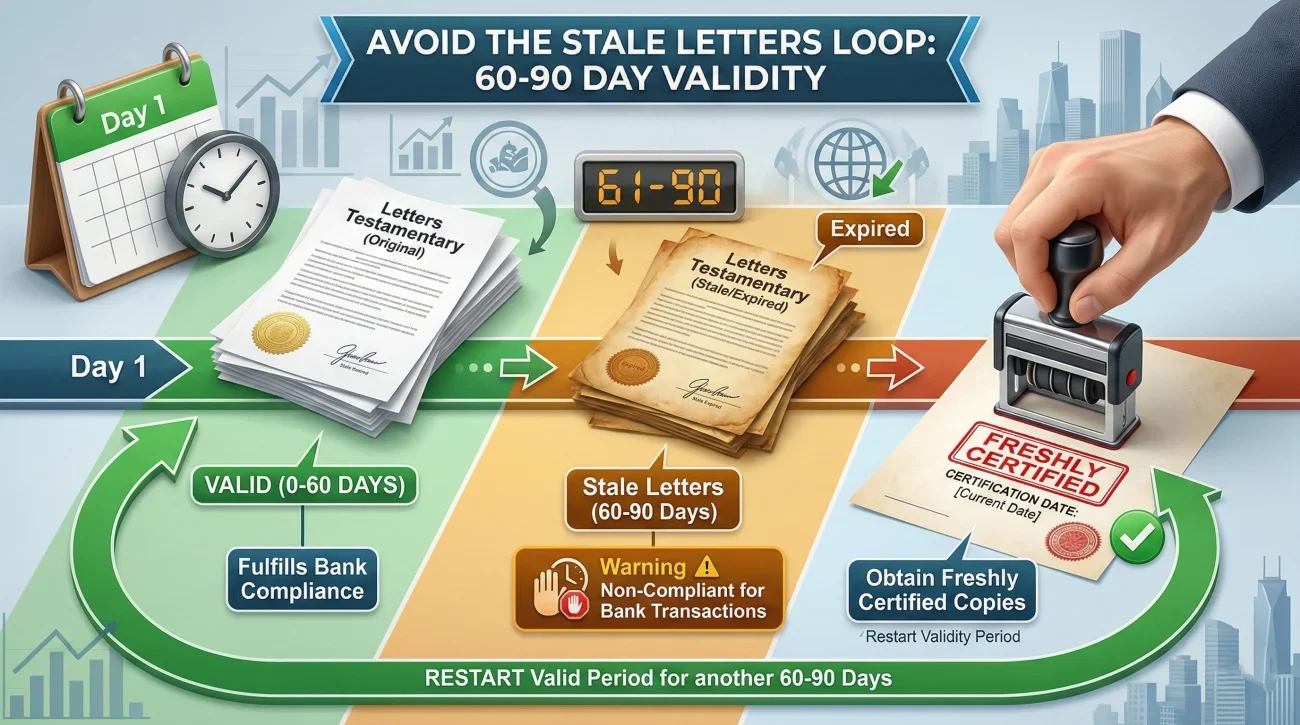

The “Stale Letters” Recertification Loop

There is a specific hurdle that catches many executors weeks into the process. You finally get an institution on the phone, and they tell you that your court letters are “too old.” In many cases, financial institutions will only accept court letters that have been certified or stamped within the last 60 to 90 days.

If the probate process has dragged on, or if you discovered a forgotten bank account a year after the person died, your original letters might be considered stale by the bank’s internal policy. The court has not revoked your authority, but the bank wants proof that your authority has not been revoked.

When this happens, do not argue with the phone representative about the law. It is a corporate policy, and the representative cannot override it. Instead, you will generally need to request an updated, freshly stamped copy of your letters from the court clerk. Once you have the updated document, use a clear tracking message to submit it.

Subject: Updated Court Certification – Estate of [Name] – Reference #[File Number]

Hello [Department/Contact Name],

Attached is the newly certified copy of the court letters of authority for the Estate of [Name], as requested on our call on [Date]. This certification was issued on [Date on stamp].

Please confirm receipt of this document and let me know if the legal department has everything they need to finalize the account transition.

Thank you,

[Your Name]

Executor, Estate of [Name]

Another variation of this delay happens with out-of-state accounts. If your letters were issued in New York but the bank branch or property is in Florida, the institution might reject your letters, requiring what is known as “ancillary probate” in their state. Always verify if the institution operates nationally or requires state-specific documentation.

Whether dealing with out-of-state rules or stale documents, the process requires patience. But patience does not mean passively waiting. In fact, passive waiting often leads to the most common administrative traps.

Common Mistakes When Dealing with the Bank

I find that understanding what not to do is just as important as knowing the next step. Avoiding these operational missteps will save you hours of sitting on hold listening to hold music.

Mistake 1: Showing up without an appointment

Branch managers are busy. If you walk in unannounced with a stack of estate documents, you will likely be asked to wait a long time or come back later. Always call ahead.

Mistake 2: Taking out a personal loan for estate expenses

Sometimes, the bank process takes so long that executors panic about funeral bills and use their own credit cards. Many large banks have expedited protocols allowing them to pay funeral homes directly from a frozen account, even before court letters are issued, provided you supply the death certificate and the official funeral invoice. Always ask about this before using personal funds.

Mistake 3: Failing to log your calls

Every time you speak to the bank, write down the date, the time, the representative’s name, and the reference number for the call. When a document inevitably goes missing, having this log forces the bank to look up their own records rather than making you start over.

Final Thoughts on Gaining Access

The transition of authority from a person to an estate is heavily guarded by red tape. When you feel blocked by an institution that refuses to look at the will, remember that they are operating defensively. Your job is not to convince them with logic; your job is to provide the exact puzzle pieces their legal department requires.

By securing court appointment, organizing a clean packet, and relentlessly tracking your submissions, you remove the friction points that cause delays. Keep your documentation strict, communicate clearly, and always follow up.

Sources & References

To ensure accuracy and reflect real-world operational challenges, this guide incorporates concepts and data points from the following resources:

- U.S. Bank Knowledge Base: Explainer on required documents and next steps for estate settlement.

- American Bar Association (ABA): Guidelines for Individual Executors and Trustees (Context on securing assets and the necessity of formal court appointment).

❓ FAQ

🏦 Why won’t the bank let me see the account with just the will?

The bank’s risk department requires a court-issued document to prove that a judge has officially validated the will and granted you legal power over the funds.

📄 Do I need to bring the original will to the local branch?

Usually, the original will goes to the probate court, not the bank. The bank generally only needs the court-issued letters of authority and the certified death certificate, though you should always request their specific checklist.

⚖️ What exactly are letters of testamentary?

They are official documents issued by a probate court that prove you have the legal right to act on behalf of the deceased person’s estate. Banks rely on these, not the will, to grant account access.

⏳ How long does it take for a bank to review my executor documents?

It varies widely, but it commonly takes between one to four weeks for a bank’s back-office legal team to review the packet and officially change the account status. Always ask for a timeline when you submit.

🗣️ Will the bank tell me if there are beneficiaries on the account?

If you present the death certificate and you are the named beneficiary, they will tell you. If you are the executor, they will usually only confirm beneficiary status after your court letters have been fully reviewed and accepted by their legal department.

📅 Why is the bank asking for a newer copy of my court letters?

Many institutions have internal risk policies requiring court documents to be certified or stamped within the last 60 to 90 days. This proves to them that your authority has not been revoked by the court recently.

💳 Can I use the deceased’s debit card to pay their funeral expenses?

No. Using their credentials or cards after they pass away violates banking terms and can trigger fraud freezes. Instead, ask the bank if they can pay the funeral home directly from the frozen account upon receipt of the invoice and death certificate.

📞 What should I say when I call the bank for the first time?

Keep it simple. State that the account owner has passed away, you are the appointed executor, and you need to know the exact documents their estate review department requires to begin the process.

🗓️ Do I need an appointment to freeze a deceased person’s bank account?

Yes, it is highly recommended. Not all branch employees are trained in estate procedures. Calling ahead ensures you speak with a manager who knows how to properly scan and submit your documents to the back office.

📉 What happens if the bank loses my faxed executor documents?

This happens frequently. This is why you must save copies of everything, maintain a detailed call log, and track your submissions. If they lose it, you will simply have to resubmit your clean, organized packet.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.