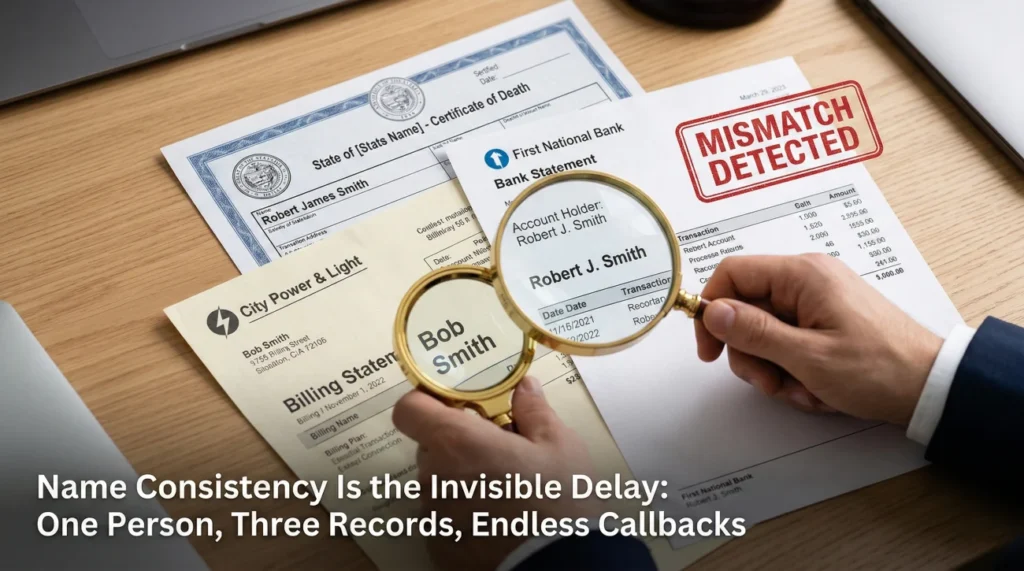

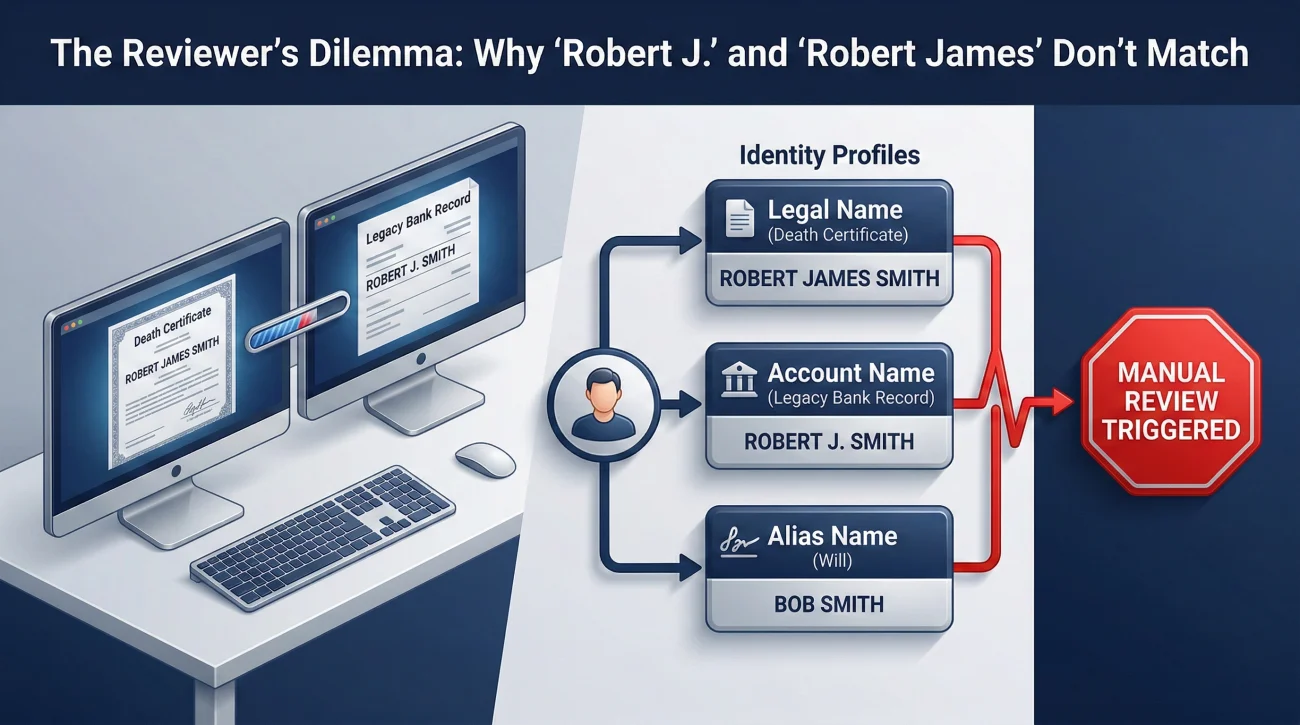

- Identity mismatch is a major cause of administrative delays. To a compliance reviewer, “Robert Smith” and “Robert J. Smith” are often treated as two different people.

- Institutions reject documents not to be difficult, but to manage liability. If names do not align perfectly across the death certificate, the will, and the account statements, manual review is triggered.

- Do not try to argue with customer service about name variants. Instead, build a written mapping trail (an AKA or Alias list) to connect all document variations into a single, verifiable narrative.

- Always keep a structured record of which name variant is attached to which specific asset, reducing the endless “we need one more document” callback loop.

The Loop of Endless Verification

You mailed the packet three weeks ago. It had the death certificate, the official court documents, and the account numbers. Today, you get a letter back from the financial institution saying they cannot process your request because the documents “failed verification” or they “need additional proof of identity.” You swear you already sent everything.

In my experience helping families organize estate administration files, this is the exact moment an executor feels like they have hit a concrete wall. The natural reaction is frustration. You might think the institution is deliberately stalling or that the representative you spoke with lost your file. While lost files do happen, the most common culprit is entirely invisible to the executor but glaringly obvious to the institution’s compliance department: name inconsistency.

Key Point: Most estate administration delays are not complex legal problems. They are paperwork discrepancies. A missing middle initial is enough to freeze an account transfer for weeks.

I want to walk you through exactly why this happens and how you can fix it. When I look at a stalled executor packet, the first thing I check is not the account balance or the date of death. I check the spelling of the deceased person’s name across every single piece of paper. You would be surprised how rarely they match.

Why the Reviewer Sees Three Different People

To understand the delay, I always suggest looking at the situation through the eyes of a back-office reviewer. This person has never met you and never met the deceased. They are looking at a screen, comparing your uploaded PDF to a digital record that might have been created thirty years ago.

Let us say your father’s legal name was Robert James Smith. That is what is printed on his death certificate. However, when he opened his brokerage account in 1985, he used Robert J. Smith. His utility bills simply say R. Smith. And to complicate things further, the court-issued authority documents might list him as Robert Smith.

When the reviewer compares the death certificate (Robert James Smith) to the account file (Robert J. Smith), their risk management software flags a mismatch. The bank is heavily regulated and terrified of releasing funds to the wrong party. According to standard executor guidance published by legal and professional organizations, institutions must verify identity with absolute certainty before transferring ownership.

⚠️ Warning: The reviewer usually does not have the authority to “just assume” Robert J. Smith and Robert James Smith are the same person. They have to follow a strict protocol, which often means kicking the file back to you.

This is where the invisible delay happens. They mail you a generic rejection letter. You call them, wait on hold, and argue that it is obviously the same person. The phone representative agrees with you, but tells you the back office makes the final call. The cycle repeats.

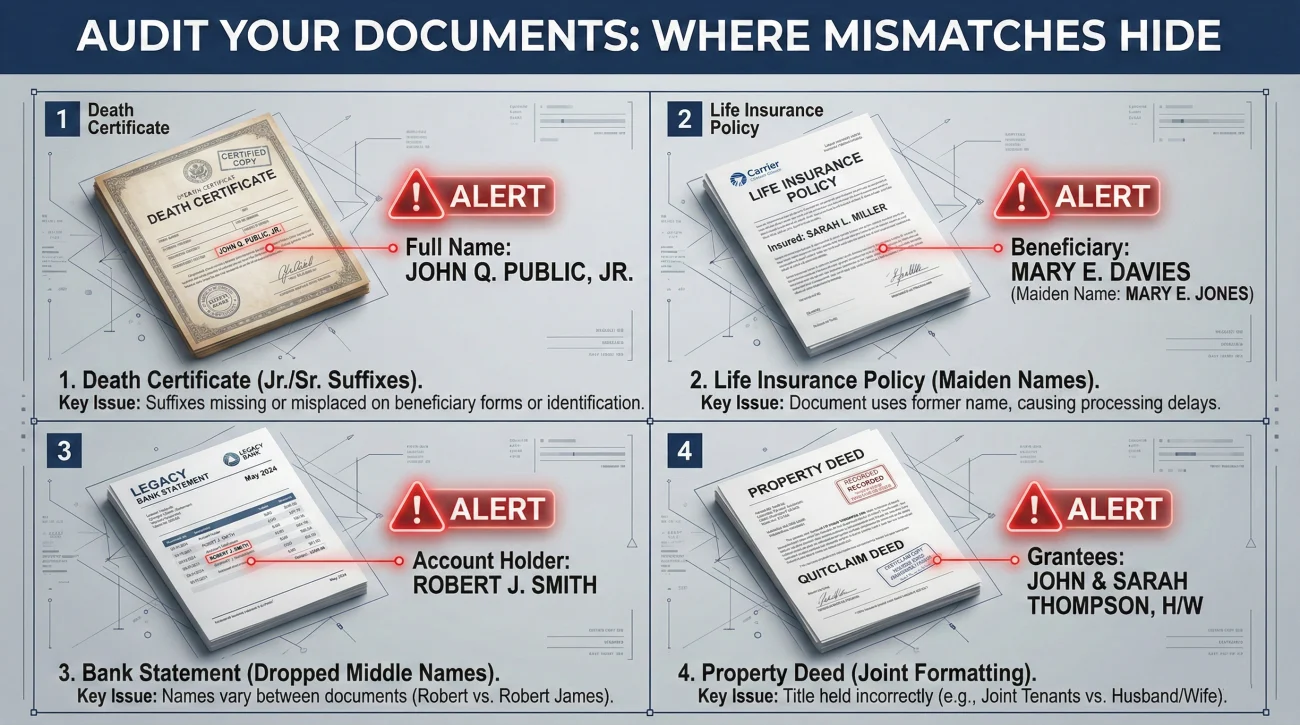

Where Name Mismatches Typically Hide

Before you send another packet, you need to audit your own documents. In day-to-day admin work, I see mismatches hiding in very predictable places. If you know where to look, you can catch the discrepancies before the institution does.

| Document Source | Common Naming Issues |

|---|---|

| The Death Certificate | Often uses the full legal name, including a maiden name or a suffix like Jr. or Sr. |

| The Will | May use a nickname, drop a middle initial, or include “Also Known As” (AKA) variants. |

| Financial Statements | Frequently abbreviated. Legacy accounts often drop middle names entirely. |

| Property Deeds | Might include a spouse’s name formatted jointly, or use a completely different middle name spelling. |

The Maiden Name and Divorce Complication

One of the most frequent patterns I see involves maiden names. A person might use their married name on their daily checking account, but an old life insurance policy might still be registered under their maiden name. If the death certificate only lists the married name, the life insurance company will hit the brakes.

A similar, often more complex issue arises with divorce. A person might change their name from their maiden name to a married name, and then legally revert to their maiden name later in life. This creates a scattered paper trail where old asset records might still carry the married name, while the death certificate and recent documents show the maiden name. They need a documented bridge between these identities.

The Suffix Confusion (Jr., Sr., III)

If your father was a “Senior” and you are a “Junior,” name consistency is vital. A common trap occurs when the senior passes away, and the junior eventually stops using the “Jr.” suffix in daily life. Years later, when the junior passes, the death certificate might omit the suffix, but an old brokerage account still lists “Robert Smith Jr.” This creates a two-way confusion that institutions treat very cautiously to avoid releasing funds to the wrong living relative.

Stripped Diacritics and Accents

As systems digitized over the decades, many financial institutions stripped accents, hyphens, and diacritics from their databases. A legal name like “García” or “Müller” might appear on a modern death certificate with the correct markers, but look entirely different, or be fused into a single string, on a legacy bank statement. This digital stripping is a frequent trigger for automated mismatch flags.

The Strategy for Proving Identity Without Changing Reality

You cannot change the name on a thirty-year-old account statement. Getting a death certificate amended is a long, difficult process. Before deciding how to map the identity, you need to determine the threshold of the error. If the death certificate has a catastrophic spelling error (e.g., a completely wrong first name), you may have no choice but to amend it through the vital records office.

However, for minor variations like dropped initials, missing suffixes, or maiden names, an AKA map anchored by the deceased’s Social Security Number (SSN) is usually sufficient. Since the SSN rarely changes, it serves as the ultimate bridge between conflicting name formats.

When I help set up an executor first steps workflow, I always emphasize that you must do the thinking for the reviewer. Connect the dots on paper so they do not have to guess.

💡 Pro Tip: If the will lists aliases (e.g., “Robert James Smith, also known as Robert J. Smith”), highlight this section. It serves as a powerful bridge document for institutions because it was legally executed while the person was alive.

If you do not have aliases listed in the will, use your cover letter to explicitly state the connection, and provide supporting evidence. According to estate execution guidelines from major brokerages, clear documentation and recordkeeping are the only ways to satisfy strict compliance requirements.

Mailing the death certificate and hoping the bank figures out that “Rob Smith” on the statement is the same person.

Including a cover letter noting the discrepancy, attaching the death certificate, and including a copy of a W-2 that shows both the legal name and the matching Social Security Number.

Handling the “We Need More Proof” Call

Sometimes, an institution’s internal policy requires an identity discrepancy to be resolved on their own proprietary forms. Because of this, even with perfect document hygiene, you might still get a rejection based on name consistency. When this happens, the goal is to stop guessing and get their exact requirements in writing.

I frequently see executors waste hours arguing on the phone. Do not argue. Ask for the compliance rule. You need to know exactly what the back office requires to bridge the name gap.

“I understand the name on the account does not perfectly match the death certificate. Rather than guessing, can you please ask the back-office review team to provide a written list of acceptable documents that will link the two names?”

Here is a safe, practical script you can use when communicating via email or secure message with an institution that has flagged a name inconsistency:

Subject: Request for name verification requirements – Estate of [Legal Name]

Hello,

I received the notice that the document packet for account [Account Number] was delayed due to a name variation. The account is listed under [Name on Account], while the death certificate lists [Name on Certificate].

To ensure I provide exactly what your review team needs, please reply with a written checklist of acceptable documents that your institution requires to verify this alias/name variation. Once I receive your list, I will promptly gather the correct items and resubmit the packet.

Thank you,

[Your Name]

Executor

Notice the structure of this request. It works effectively because it:

- ✔️ Acknowledges the mismatch up front without being defensive.

- ✔️ Asks for the specific compliance requirements in writing.

- ✔️ Commits to providing exactly what they ask for, stopping the debate.

By forcing them to give you a checklist, you remove the guesswork. You also create a paper trail in your document tracker, proving that you are actively trying to resolve the issue according to their rules.

Logging the Variants

To keep yourself sane, I highly recommend creating a simple tracking log. In your master estate spreadsheet, add a column dedicated entirely to “Name on Account.” This allows you to see at a glance that the life insurance is under a maiden name, the checking account is under a nickname, and the property deed uses a middle initial. This level of executor recordkeeping will save you weeks of frustration and prevent you from sending the wrong cover letter to the wrong institution.

Final Thoughts on Document Consistency

Closing an estate is largely an exercise in translating a lifetime of messy reality into a neat stack of paperwork. It is incredibly frustrating to feel like your progress is being held hostage by a missing middle initial. However, once you adopt the mindset of the back-office reviewer, the process becomes much more manageable.

Remember, the institution is protecting itself from liability. Your job is not to convince them over the phone; your job is to build a documented bridge that makes it easy for them to say yes. Track the variations, build your alias map, and always insist on getting their requirements in writing. If you approach the paperwork systematically, you can break the loop of endless callbacks and keep the estate moving forward.

Sources & Reference Material

- 📄 Vanguard Estate Services: An example of a major brokerage’s required documentation and recordkeeping procedures during an estate transition. View Vanguard’s transition hub.

- ✅ American Bar Association (ABA): Guidelines for Individual Executors & Trustees, explaining the fiduciary duty to verify identity and gather accurate documentation. Read the guidelines.

❓ FAQ

📝 What happens if the name on the death certificate is slightly wrong?

If the error is significant, you may need to contact the vital records office or the funeral home to request an amendment. If it is a minor variation (like a dropped middle initial), you can often use secondary identification or court documents to bridge the gap for financial institutions.

⚖️ Do I need a lawyer if the bank says the names do not match?

Not always. Many name mismatch issues are purely administrative. You should first ask the institution for a written list of acceptable documents to prove the alias. If they refuse everything or if the estate is locked, consulting a professional is a wise next step.

🕵️ How do I prove my parent used a nickname on their accounts?

Institutions often look for a paper trail. Providing old utility bills, tax returns, or cancelled checks that show the nickname associated with the deceased person’s primary address or social security number can often satisfy the review team.

🏛️ Will the probate court fix a misspelled middle name?

Courts do not issue death certificates, so they cannot fix that document. However, when you file for probate, you can often petition the court to list the deceased person under their legal name alongside any known aliases (AKAs), which creates an official record of the variations.

💳 Why is the financial institution asking for my ID too?

They are legally required to verify the identity of the person claiming the funds. Just as they must verify the deceased person’s identity, they must ensure the executor matches the name listed on the court-issued authority documents.

🚫 Can I just cross out the wrong name on a document and write the right one?

Never alter an official document. Crossing out names or dates on a death certificate, will, or court order will almost certainly cause the document to be rejected for fraud, creating massive delays.

📄 What is an AKA or Alias document in estate administration?

It is not usually a single document, but rather a trail of proof. Sometimes the will includes a clause stating “Also Known As.” Other times, it is a court document that officially recognizes that “Robert J. Smith” and “Robert James Smith” are the same individual.

⏳ How long does a manual name review take at a bank?

Manual reviews typically take anywhere from 7 to 21 business days, depending on the institution’s backlog. This is why getting the document packet perfectly aligned before sending it is so critical to your timeline.

💍 Should I use the deceased’s maiden name on the final tax return?

Tax documents should generally match the name tied to the person’s Social Security Number in the government’s system. If they legally changed their name upon marriage and registered it, use the married name.

📞 What do I say when customer service keeps rejecting my paperwork over a name issue?

Politely end the debate and ask the representative to send you a written, itemized checklist from their compliance department detailing exactly how to bridge the discrepancy.

⚠️ Disclosure: I'm not an attorney and nothing on this site is legal or tax advice. The content covers process, organization, and workflow—the operational side of estate administration. For legal interpretation, jurisdiction-specific deadlines, contested situations, or tax matters, please work with a licensed professional in your state.